How to Become Financially Stable: 10 Steps That Actually Work

“I Feel Completely Lost With My Finances” : You’re Not Alone

Staring at a bank balance that is nowhere near where it needs to be, and feeling that dull dread settle in your chest that is a feeling most people experience and almost nobody talks about. It is not just a money problem. It is the 3am ceiling-staring, the tightness every time your phone buzzes with a notification, the exhausting loop of working hard and still coming up short every single month.

If you are wondering how to become financially stable and you feel lost right now, I want to say something directly: you are not alone, and you are not failing.

A 26-year-old in New York City shared something recently that I have not stopped thinking about. Earning $600 a week and watching it disappear rent, car insurance, utilities until there was barely anything left to show for the week. Living paycheck to paycheck had become their baseline, and the anxiety of it was constant. They wrote: “I am tired of living paycheck to paycheck and the constant anxiety that comes with it.” Someone replied: “At 26 you are hitting a zone where your needs and obligations feel like they are going up faster than your earnings. That is pretty normal.”

It is normal. But normal does not have to be permanent.

That validation is real and it matters. It does not, however, pay your bills.

What actually works is a roadmap built for where you are right now not one that assumes you have money sitting somewhere waiting to be invested, or that tells you skipping lattes is the answer. I have spent years working through personal finance frameworks, studying what separates people who break this cycle from those who stay stuck, and this article is the result of that. What I have consistently found: your sense of control over your finances predicts your financial well-being far more reliably than your salary does. The shift you need is not a bigger paycheck. It is a clear sequence of steps.

Everything below is in the exact order you should work through them. Start at Step 1.

What Does “Financially Stable” Actually Mean?

A lot of people think financially stable means debt-free, or comfortable, or that money just stops being a problem entirely. That is not quite what it means.

The financially stable meaning I work with is narrower and more precise: you cover all essential expenses without scrambling, you save a real percentage of your income every single month, and you hold a financial cushion big enough to absorb most emergencies without going into debt. You still depend on your paycheck. But money stops being a daily source of dread.

That is meaningfully different from being financially secure, where you could absorb a job loss for six or more months without panicking. And it is a long way from financial independence, where passive income covers your living expenses entirely. Stability is the foundation. Financial wellness that overall sense that your money situation is under your control starts the moment you build it.

Financial Stability vs. Financial Security vs. Financial Freedom

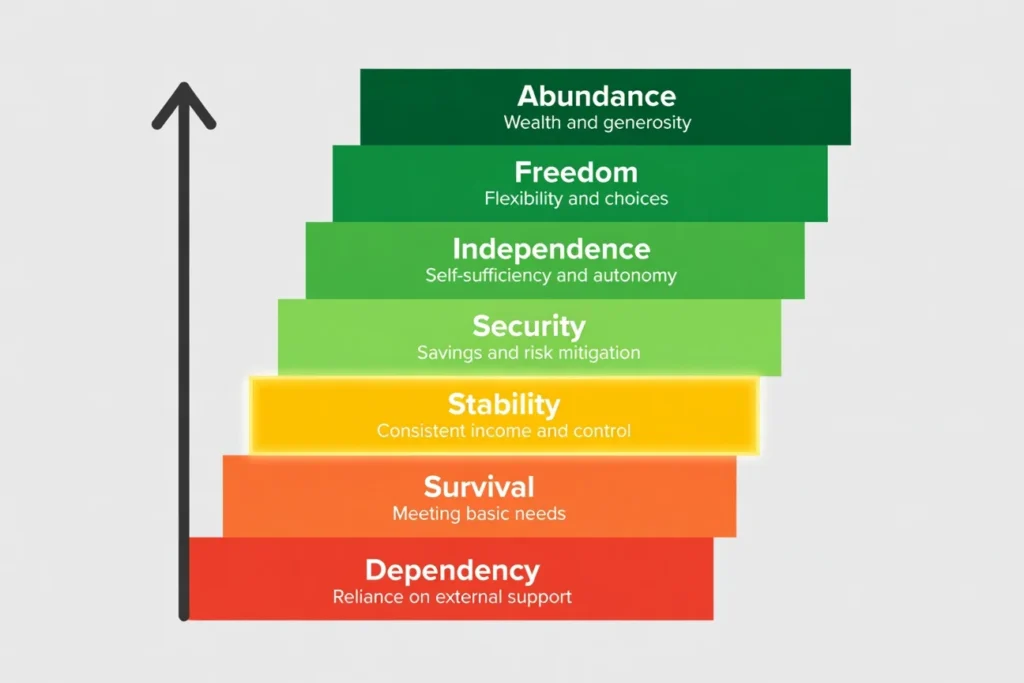

Think of personal finance as a seven-level staircase. Most people start somewhere on levels one or two and have no clear picture of what levels three through seven even look like. Here is where each level actually sits:

Levels 1 and 2 (Dependency and Survival): Income barely covers basic needs. Living paycheck to paycheck with no savings buffer and no room for anything unexpected. This is where financial anxiety lives.

Level 3 (Stability): Saving at least 20% of income monthly, holding a 3-6 month emergency fund. Still employed, still dependent on that paycheck but not stressed by normal expenses. This is the target for most people reading this.

Level 4 (Security): You could lose your job today and not reach for the credit card for six or more months. Solid financial cushion, no high-interest debt pulling you backward.

Level 5 (Independence Path): Investments are compounding meaningfully. You are actively building toward a point where work becomes a choice rather than a requirement.

Level 6 (Freedom): Passive income from investments, real estate, or scalable businesses covers all living expenses. Your job becomes optional.

Level 3 is a worthy, reachable goal. Chasing Level 6 before Level 3 is cemented is one of the main reasons people end up nowhere fast.

The One Number That Matters Most (It Is Not Net Worth)

Most financial advice fixates on net worth as the scoreboard. Net worth can be deeply misleading in ways that matter in practice.

Someone can own a $400,000 duplex, hold $60,000 in a retirement account, carry a $280,000 mortgage and a $15,000 car loan, and still be $200 short every month after all bills are paid. The property exists on paper. The stress exists in real time.

What I track instead and what you should care about first is monthly cash flow. What comes in versus what goes out. When that number is positive and growing, you are building something real. When it sits at zero, you are standing still regardless of what your net worth spreadsheet says.

Am I Financially Stable? Take This 2-Minute Self-Assessment

Do this before anything else. Answer yes or no to each of these eight questions. The point is honest clarity, not judgment.

- Do I pay all my bills on time every month without scrambling?

- Do I have at least $1,000 saved in a separate account (like a high-yield savings account) for emergencies?

- Am I free of high-interest credit card debt, or actively paying it down?

- Do I save at least 10% of my income each month?

- Could I cover a $1,000 unexpected expense without going into debt?

- Do I have health insurance and basic life or disability coverage?

- Do I contribute anything to a retirement account, even a small amount?

- Do I feel in control of money decisions, rather than constantly reacting to financial pressure?

Your score:

0 to 2 yes: You are in Survival Mode. Your one job right now is Steps 1 to 3. Nothing else.

3 to 4 yes: You are moving. Pick two steps from the list below and focus there this month.

5 to 6 yes: You are close. Find the gaps in the checklist below and close them systematically.

7 to 8 yes: You have reached stability or are nearly there. Shift your focus toward building Level 4 security.

The 8 Signs You Are Financially Stable

At Level 3, this is what your financial life actually looks like day to day:

- You have a dedicated emergency fund covering at least three months of expenses

- You are not living paycheck to paycheck

- High-interest debt is either gone or in active payoff mode

- You save 20% or more of your income consistently

- You are investing something for the future, even if the amount is modest

- Your credit score sits at 700 or above

- You have basic insurance coverage in place

- A $1,000 surprise expense does not derail your month

What Your Score Means and What to Do Next

A low score does not mean you are bad with money. It means the habits have not been built yet. That is fixable, and the fix is sequential. The ten steps below are numbered in the exact order you should work through them. Start at Step 1 regardless of whether your score was two or six.

How to Become Financially Stable: 10 Proven Steps

These ten steps are sequenced for a reason. Each one builds a specific foundation the next step depends on. Skipping ahead is the single most common reason people restart from scratch six months later. Work them in order.

Step 1: Face Your Numbers (Track Every Dollar for 30 Days)

Tracking is not about judgment. It is about getting an honest picture of where the money actually goes because most people’s mental accounting is off by 30 to 40 percent.

Go through your bank and credit card statements from the last two months. This is where the budgeting process actually starts not with an app or a template, but with the raw statements. Pull them up now if you can. Highlight or categorize every transaction. Calculate your total monthly income and your total monthly spending. Then split that spending into two buckets: core essentials (rent, utilities, food, medicine, transportation to work) and everything else.

This is not a judgment exercise. You are gathering data right now observing where the money actually went versus where you assumed it went.

Most people discover that two or three categories are quietly eating their budget. Subscriptions that auto-renew without notice. Dining out that happened more than they realized. Small impulse purchases that felt negligible one at a time. Effective expense management starts with naming every one of them. That is the entire first step.

Step 2: Set Your 3-Month, 6-Month, and 12-Month Financial Goals

Here is the difference between people who actually reach financial stability and people who stay stuck in good intentions: specificity. Not motivation. Not discipline. Specificity.

After you know your numbers from Step 1, build one clear target for each of three time windows. Financial planning without specific targets is just wishful thinking:

3-month goal: Track all spending for 30 days and save your first $500 toward an emergency fund.

6-month goal: Pay off one small debt completely, or grow savings to $1,500.

12-month goal: Zero credit card debt, a three-month emergency fund in place, saving 15% or more monthly.

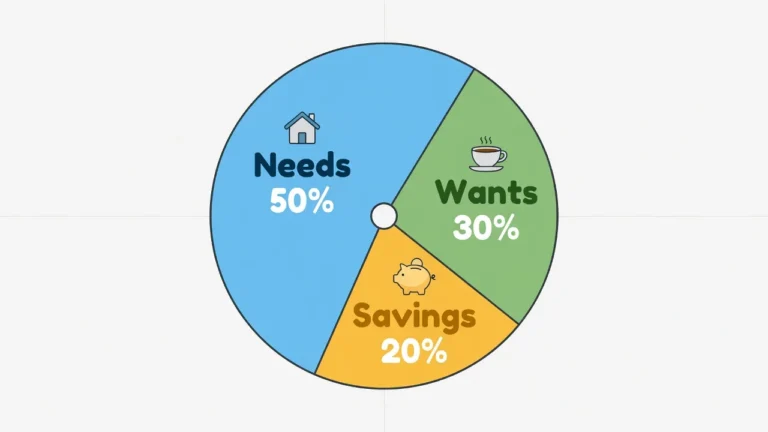

Write these down somewhere you will actually see them. Use the SMART framework as a check is each goal Specific, Measurable, Achievable, Relevant, and Time-bound? And if you need a starting point for dividing your income, the 50/30/20 rule 50% to needs, 30% to wants, 20% to savings and debt repayment gives you a workable baseline before you refine it to your specific situation. “Save money” fails every SMART test. “Save $200 per month by cutting dining out to twice a week” passes all of them.

Step 3: Build Your Starter Emergency Fund ($1,000 or 1 Month of Expenses)

This step comes before debt payoff. That surprises a lot of people. Here is exactly why it matters.

When you are in debt and an emergency hits and they will hit you either go deeper into debt to handle it or you wipe out the little savings you had built. Either way, you slide backward and the cycle restarts. The starter emergency fund is what breaks that cycle.

Save $1,000, or one month of your core essential expenses, whichever amount is higher. Keep this money in a high-yield savings account where it earns a little interest, stays liquid, and sits completely separate from your checking account. Do not invest it. Do not touch it unless a true emergency arrives — meaning something that cannot wait and cannot be solved any other way.

That financial cushion changes the entire emotional experience of managing money. You stop making financial decisions from a position of pure panic. And once that shift happens, every decision that follows is clearer.

Step 4: Attack High-Interest Debt Using the Snowball Method

Once your starter fund is solid, turn your full attention to high-interest debt especially credit card balances that compound against you every month you carry them.

List every debt from smallest balance to largest, ignoring interest rates for now. Make minimum payments on everything except the smallest. Every extra dollar you can find goes toward that smallest balance until it is completely gone. Then take that exact payment amount and roll it directly into the next debt on the list.

This is the debt snowball method, and it works not because it is mathematically optimal but because it builds momentum. Paying off a $400 credit card in two months is a real win. And that win changes how you approach the next three months.

If you prefer to work the math, the debt avalanche method targeting the highest interest rate first saves more money over the full repayment period. Both approaches work. Pick the debt avalanche if the math keeps you motivated. Pick the snowball if you need early wins to keep going. The only real failure here is abandoning the method at month three before it has had time to work.

Step 5: Automate Your Savings (The Pay Yourself First System)

Your brain has a simple rule about money sitting in your checking account: it is available, so it is spendable. That is not a flaw it is just how human psychology handles visible resources. Fighting it with willpower every payday is a losing strategy for nearly everyone.

The core of an effective savings strategy is automation. Set up an automatic transfer from your checking account to your savings account on the exact day your paycheck lands. Start at 10% of your income. Push toward 20% as quickly as your budget allows.

Open a separate savings account ideally at a different bank or a high-yield online account and treat it as your Freedom Fund. Label it that. The more friction between you and that money, the better. When the automatic transfer runs in the background, saving stops being a decision you have to make each payday. The money that stays in your main account is what you actually have to work with that month. And that mental boundary matters more than most people expect.

Step 6: Increase Your Income the Smart Way

There is a ceiling on how much you can cut. Expenses can only go so low before you are cutting into things that actually matter. Income has no ceiling it just takes longer to move.

If you are struggling to cover basics right now, quick cash solutions like a second job or extra shifts are the right short-term answer. The cash flow is immediate and you can throw every dollar of it at your debt or emergency fund.

But if you have some breathing room and you are thinking beyond the immediate situation, the smarter investment is high-income skills. Content creation, copywriting, social media management, digital products these all start as a side hustle and can scale into real income streams over time. The difference between these and gig delivery work is that gig work stops paying the moment you stop showing up. Delivery apps and similar platforms pay you for your time, and only for your time. A skill that produces content, a service, or a digital product can generate income on days you are not actively doing anything.

Fair warning: the first one to two years of building a scalable skill usually produces very little income. That is normal and not a signal to quit. Millionaires typically build multiple income streams over years, not months. Start with your primary income, stabilize it, and layer something scalable in when you have the capacity to do it without burning out.

Step 7: Live Below Your Means Without Feeling Deprived

There is a rule I use for everyday purchases: do not buy something unless you could buy three of it comfortably. If you cannot afford an item three times over, you cannot truly afford it once.

This is not about extreme frugality. It is about building and maintaining a gap between your income and your spending and keeping that gap intentionally wide. Living one or two levels below what you can technically afford prevents lifestyle creep, which is the wealth-killing pattern of automatically upgrading your lifestyle every time your income rises.

Think about someone earning a modest income and saving 50% of it, versus someone earning four times as much and saving nothing. The first person is building toward stability. The higher earner is not. Being financially comfortable is not about the size of your income it is about what you do with the gap.

Frugality done wrong feels like punishment. Done right, it feels like control. Every dollar you do not spend on something you barely wanted is compounding somewhere else and that gap between your income and your spending is where wealth actually grows.

Step 8: Build Your Credit Score the Right Way

Credit score improvement is not just about qualifying for better loan rates. A poor score affects rental approvals, some job applications, and even insurance premiums. It is an invisible tax on everything you try to build.

Three specific FICO score components account for roughly 80% of your total score:

Pay every bill on time. This single habit accounts for 35% of your FICO score. No other factor comes close.

Keep your credit utilization below 30%. If your credit limit is $5,000, keep your balance under $1,500. Below 10% utilization is ideal for the highest scores.

Do not close old accounts. Length of credit history accounts for 15% of your score. Closing an old card to simplify often backfires.

Credit score improvements typically take 30 to 90 days to show up after you make a change so do not expect instant results, but expect real ones. The most effective daily strategy: put regular expenses on a credit card and pay the full balance every single month. You build payment history, which is 35% of your FICO score, without paying a dollar of interest. That is the whole credit-building system in one sentence.

Step 9: Start Investing for Your Future (Even With $50 a Month)

Once the starter emergency fund is built and you have knocked out your high-interest debt, investing is the next step. This is where compound interest starts doing real work — and the earlier you start, the less you actually have to contribute to end up with a significant number.

Here is the priority order for most people:

- Contribute to your 401(k) at least up to the employer match. That match is free money. Never leave it on the table.

- Open a Roth IRA and contribute up to the annual limit. For most people in their 20s and early 30s who are in lower tax brackets now than they will be later, the Roth IRA is typically the better choice you pay taxes now and the account grows completely tax-free.

- Return to your 401(k) if you have more to invest after the IRA is funded.

For beginners, low-cost S&P 500 index funds are the most straightforward starting point. Funds like VOO or SPY provide automatic investment diversification across 500 large companies without requiring you to pick individual stocks. Historically the S&P 500 has returned approximately 10% annually over the long term, a figure supported by data going back to the index’s inception and including multiple major downturns. Past returns do not guarantee future results, but the long-term track record is what drives the recommendation.

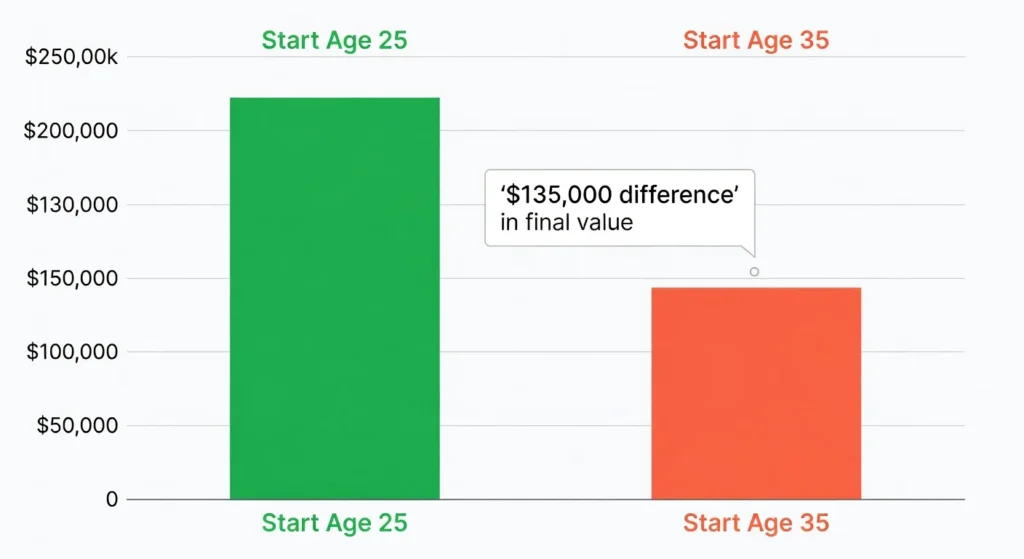

Here is the compound interest math that changes how you think about starting now. If you invest $100 a month starting at age 25 and earn an 8% average annual return, by age 60 you have roughly $230,000. If you start the same plan at 35, you end up with about $95,000 by the same age. Same $100. Same market. Ten years of difference costs $135,000 in final value and that gap widens dramatically at higher contribution amounts.

You do not need a thousand dollars sitting somewhere waiting. You need $50 a month and a Fidelity or Vanguard account. That is genuinely all it takes to start.

If your financial situation involves significant complexity multiple income sources, inheritance, or business income consulting a fee-only financial advisor before making major investment decisions is worth the cost.

Step 10: Protect Your Wealth With the Defense Strategy

Years of disciplined saving and investing can be erased by one uninsured medical event or an unexpected death in a household with dependents. That is not a scare tactic. That is the actual risk that insurance coverage is designed to absorb.

Three types matter most:

Term life insurance: If anyone depends on your income, get this. It pays your family if you die unexpectedly and is far more affordable than most people assume.

Health insurance: One serious medical emergency can set you back years financially. This is not optional at any income level.

Disability insurance: Most people never consider this, but your ability to earn income is your most valuable financial asset. Disability insurance protects it when everything else fails.

Whole life and universal life insurance policies are almost always the wrong choice for someone building financial stability. The premiums are dramatically higher than term life. The investment component consistently underperforms low-cost index funds over comparable time periods. Buy affordable term life insurance and invest the difference. That combination outperforms most bundled insurance-and-investment products over any 20-year period you compare.

Why You Keep Failing at Budgeting (And How to Fix It)

Financial success is 80% behavior and 20% knowledge. Most people already have enough knowledge to get started. The behavior is what actually kills the progress.

Most budgets fail for the same handful of reasons, and they are almost never the ones people expect. The restrictions go in too tight and snap within two weeks when life happens. Every problem gets targeted at once debt, savings, investing, monthly expenses and the attention spreads so thin that nothing actually moves. There is no automation in the system, so the whole process runs on money discipline and willpower, both of which are finite resources that run out. And when the progress is invisible after 60 days, most people quietly stop.

Someone described it well in a Reddit thread I came across: it is like working out. The information is not the problem. Showing up consistently is the problem. If you are restarting for the third time, going back to budgeting fundamentals often reveals the one behavioral piece you have been missing.

The Learning Loop Trap (Action Beats Perfection)

The learning loop is something I see constantly. Another podcast. Another book. Another video at 1.5x speed. All of it is about money, and all of it feels like progress. But nothing in the actual account changes.

The trap is that consuming financial literacy content triggers the same sense of accomplishment as doing the thing. And it is far more comfortable than trying something and getting it wrong.

Try things for three to six months even if you do it imperfectly. You will miss a savings transfer. The budget will break in month two when an unexpected expense hits. Those are not failures they are the normal friction of building habits that did not exist three months ago. The only real failure is treating the mess as proof that the whole process is pointless.

The 30-Day Focus Fix

If all of this feels overwhelming, here is the simplest entry point that actually produces results: pick ONE spending category for reducing expenses by 10% over the next 30 days. Just one. Ignore everything else entirely.

Maybe that is dining out. Maybe it is subscriptions you forgot were running. Maybe it is impulse purchases that happen online at 10pm. Pick the one that feels most achievable and focus there completely.

After 30 days, something will have actually changed. Not your whole financial life just one category. But that one real change is worth more psychologically than any plan you have written and then abandoned.

How to Be Financially Stable With Low Income (Under $35k a Year)

The most common objection I hear when people read through these steps is: “This sounds logical, but I do not make enough money.”

I understand why it feels that way. But stability is about surplus the gap between your income and your expenses not the size of your income alone.

As I mentioned in the definition section, the Reddit poster earning $600 a week in New York City was dealing with one of the most expensive cities in the world. That is a genuinely hard situation. But the financial principles that create stability work at every income level, even if the timeline stretches longer.

Here is the formula that actually drives everything: Income minus Expenses equals Investment Power. If that number is $50, you are building something. If it is zero, nothing moves regardless of what your income level is. The entire strategy for budgeting on a low income is about widening that gap from whatever starting point you have.

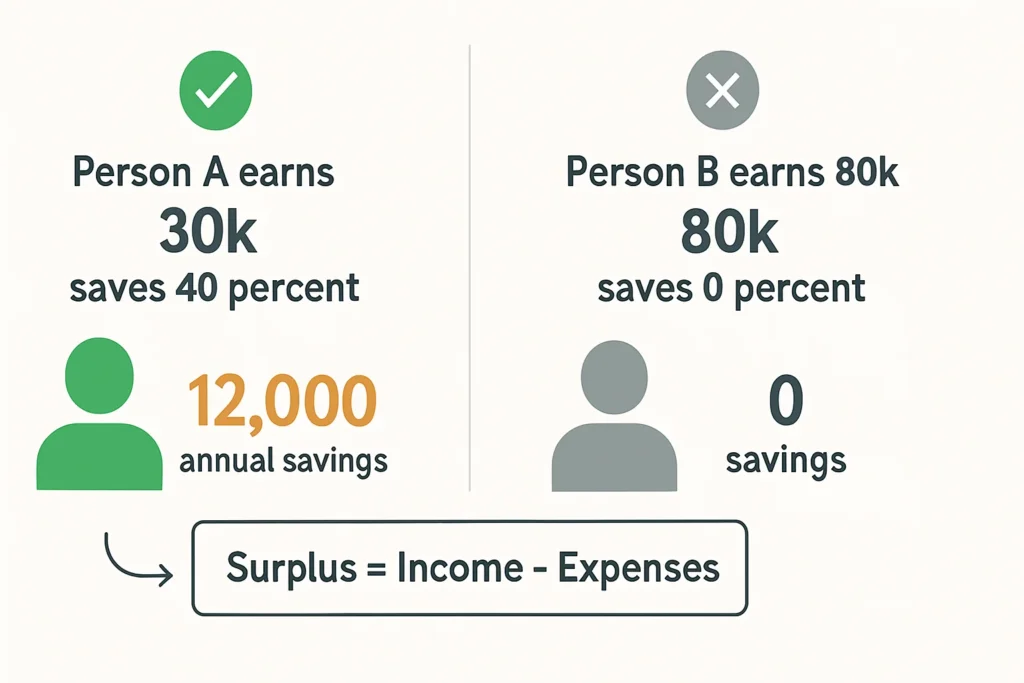

The Surplus Formula (Why $30k Saving 40% Beats $80k Saving 0%)

A person earning $30,000 a year and saving 40% of it is in a stronger financial position than someone earning $80,000 and saving nothing. The first person is building a financial cushion, paying down debt, and investing. The second is one missed paycheck from crisis.

Income level sets the difficulty. Behavior determines the outcome. The savings strategy is the same at both income levels what changes is the timeline.

4 Hacks to Slash Major Expenses Without Feeling Poor

On a tight income, the biggest leverage comes from attacking your three largest expenses: housing, transportation, and food. Everything else is small by comparison.

House hacking: If you own or rent, consider renting a spare room to offset your housing cost. Some people buy small multi-unit properties, live in one unit, and rent the others effectively living for free or close to it. I have seen this single move eliminate a person’s largest expense entirely.

Car hacking: Buy a reliable used car that has already taken its steepest depreciation hit. A three to five year old vehicle with low mileage performs identically to a new one for a fraction of the monthly cost.

Brand hacking: Generic store brands for food, cleaning supplies, and personal care products are often manufactured by the same companies as the premium versions. Choosing generics on staple items consistently saves hundreds per year with zero quality difference.

Tax hacking: Every dollar contributed to a traditional 401(k) reduces your taxable income immediately. You pay less tax right now while simultaneously building for the future. That is a double benefit most low-income earners overlook completely.

These four hacks target your largest expense categories. For more tight budget strategies that work across every spending area, the pattern is the same: find where the big dollars are going and make one strategic change at a time.

When You Are in Survival Mode: The Immediate Next Step

If you are in survival mode financially right now, do not try to implement ten steps simultaneously. Do one thing this week.

Pull up your last seven days of transactions. Find one expense you did not need. Calculate what cutting that expense saves per month. Set that amount aside somewhere separate, even if it is only $25.

That $25 is your start. Not because $25 changes your finances it does not. But because the act of separating money intentionally, even $25, represents a different behavior than you had yesterday. And behavior is the only thing that changes the numbers over time.

Financial Stability in Your 20s: Start Now, Thank Yourself at 30

If you are in your twenties right now, the genuine advantage you have over someone starting this process at 40 is time. Not income. Not discipline. Time. And time is the only thing compound interest needs to do something extraordinary with a very ordinary amount of money. Understanding where you should be financially by 30 gives you a clear target to work toward during this critical decade.

The twenties are genuinely hard financially. Student loans, entry-level salaries, peer pressure to appear successful, the fear of missing out on experiences all of it pulls in opposite directions simultaneously. I get it. But the decisions you make between 22 and 30 have an outsized impact on where you land at 40, in ways that are mathematically difficult to compensate for later.

Why Starting at 25 vs. 35 Equals a $500,000 Difference

Here is the math without any fluff. Invest $100 per month starting at age 25, assume an 8% average annual return, and by age 60 you have roughly $230,000. Start the same plan at 35 and that number drops to about $95,000. Same $100 a month. Same market. Ten fewer years means you lose approximately $135,000 in final value and at higher monthly contribution amounts, that gap scales well into the hundreds of thousands, which is where the headline figure comes from.

Note that these figures use an 8% annual return assumption, which is a conservative estimate of the S&P 500’s long-term historical average. Actual returns vary by year and are not guaranteed.

Even $50 a month in an IRA invested in a low-cost index fund makes a meaningful difference over decades. A Fidelity or Vanguard account takes about 15 minutes to open online. The compounding math does not care whether you feel ready.

The Biggest Money Mistake 20-Somethings Make (Lifestyle Inflation)

You get your first real raise. The instinct is to upgrade the apartment, eat out more, and finally buy the car you have been thinking about. That instinct is natural. It is also one of the fastest ways to stay financially stuck.

This is lifestyle creep. When spending habits rise to match every income increase, the savings gap stays at zero or shrinks further. Controlling spending habits becomes essential when income rises otherwise every raise disappears into a slightly upgraded lifestyle.

The approach that actually works: increase your savings rate when income increases, not your spending. Live at exactly the same level for six months after a raise and redirect the difference into savings and investments. You will not feel deprived. And in two years you will be dramatically further ahead than your peers who spent the raise.

Rewire Your Money Mindset Before You Touch Your Budget

Tactics fail without the right mental foundation underneath them. Not because the tactics are wrong the steps in this article work. But invisible beliefs inherited from childhood about money management, earning, and worthiness quietly override every tactical decision you make as an adult.

Most of our beliefs about money were absorbed in childhood, often from watching parents navigate financial stress, and those inherited scripts run in the background of every financial decision without us realizing it.

The Brainwashing Phase (Why Some People Succeed and Others Do Not)

One of the most effective reframes I have encountered is what some financial educators call the brainwashing phase. Immerse yourself in content that normalizes financial progress. Read one financial literacy book per month. Listen to a personal finance podcast daily during a commute or workout.

Not to fill your head with more tactics. But to normalize the idea that financial independence is possible within five to ten years rather than forty. When your brain stops treating that possibility as unusual, your daily behaviors quietly shift to support it. The immersion is the mechanism, not the information.

Scarcity vs. Abundance: The Lola vs. Athena Framework

Picture two people. Lola has a scarcity mindset. She cuts every expense possible and keeps whatever is left in a savings account because investing feels risky. Every financial decision runs through the lens of “how do I spend less?”

Athena has an abundance mindset. She tracks spending too but focuses her energy on increasing her earning power. She builds skills, creates assets, and moves money into investments. She spends thoughtfully but does not obsess over penny-pinching.

Over ten years, Athena builds meaningful wealth while Lola, despite her diligence, stays roughly where she started. The difference is not income or discipline it is where the focus goes. Cutting back is a valid tool. But it is a tool with diminishing returns, and inflation will quietly eat everything you save if growing income is never part of the equation.

Challenge Your Inherited Money Beliefs

Take a moment and write down three things you heard your parents say about money. “We cannot afford that.” “Money does not grow on trees.” “People like us do not have savings.”

Now ask yourself whether those beliefs are actually true, or whether they are just familiar.

Making these beliefs conscious is the first step to rewriting them. Money is a tool. It amplifies who you already are. Giving it more negative meaning than that keeps it in control of you instead of the other way around.

7 Expensive Mistakes That Keep People Broke (Stop Doing These)

Every one of these mistakes is something I have seen repeatedly. And in most cases, the person making them had read enough to know better. Knowing and doing are different problems.

Mistake 1: Believing Saving Alone Beats Inflation

Cash sitting in a regular bank account earning 1% against 3 to 4% annual inflation is not saving it is slow spending. Understanding how much your savings actually earn versus inflation reveals why investing becomes necessary after your emergency fund is complete.

Over a decade, your savings lose meaningful real purchasing power regardless of the balance. After building your 3-6 month emergency fund in a liquid account, invest the surplus. That is not optional it is the only way to stay ahead of inflation over time.

Mistake 2: The Lifestyle Creep Trap (Earn More, Spend More)

Every time income rises, lifestyle follows it upward. Spending habits expand. The savings rate stays flat or drops. The fix is to automate a savings rate increase before you touch the new income. If you spend it first, the decision has already been made for you.

Mistake 3: Trading Time for Money Instead of Building Assets

Delivery apps and gig work solve short-term cash flow problems. They do not build long-term wealth because the income stops the moment you stop working. Scalable skills and income-producing assets work even when you are not actively doing anything and that distinction compounds dramatically over five years.

Mistake 4: Investing Your Emergency Fund for Better Returns

When a real emergency hits during a market downturn, you are forced to sell investments at a loss to cover it. Your emergency fund must stay liquid in a high-yield savings account. One market correction during the wrong month can turn a smart investment decision into a costly one.

Mistake 5: Trying to Fix Everything at Once

Trying to fix debt, savings, and investing simultaneously is how people end up with three half-finished financial goals and zero completed ones. Work the steps in order. The focus required to actually close one goal is what makes the next one possible.

Mistake 6: Focusing on Net Worth Instead of Cash Flow

A high net worth built in illiquid assets does not prevent financial stress if monthly cash flow is negative. Monthly cash flow is the number to watch. A growing positive number means you are building. Net worth on paper means very little if you are still anxious about next month’s bills.

Mistake 7: Skipping the Defense (Insurance)

One medical emergency that adequate insurance coverage would have handled for a monthly premium can take five years to recover from financially. That is the actual tradeoff. Insurance is not an expense. It is the cost of protecting everything else you are building.

Your Financial Stability Timeline: What to Expect Month by Month

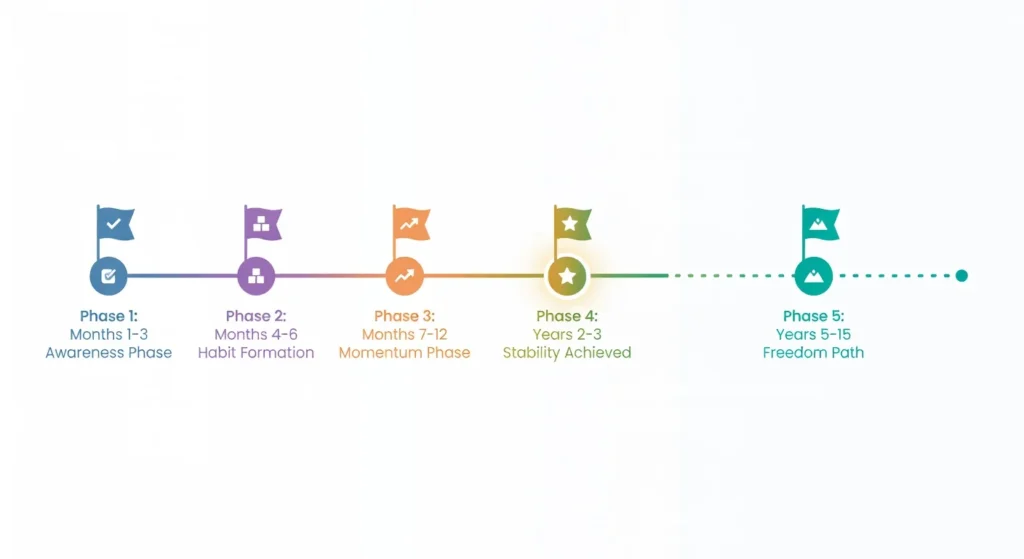

People quit this process mostly because the timeline is not what they expected. Not because the steps are wrong. Here is an honest breakdown of what to expect so you can calibrate accordingly and not quit at month four when you are actually on track.

Months 1 to 3: The Awareness Phase

You are learning your actual numbers. Tracking spending and probably finding expenses that genuinely surprise you subscriptions you forgot about, categories that ran way over. The financial goal for this phase is to save your first $1,000 and establish one or two new habits. Progress feels invisible here. It is supposed to. You are building infrastructure, not seeing results yet.

Months 4 to 6: The Habit Formation Phase

Automation starts working for you. Transfers happen without any decision on your end. If you have debt, the snowball is rolling and you may have paid off your first balance. The resistance that made the first 90 days hard starts to ease not because the habits became effortless, but because they became familiar.

Months 7 to 12: The Momentum Phase

Your emergency fund is growing. At least one debt is gone. Confidence increases in a real, observable way. This is the phase where people who started with zero confidence begin making financial decisions without spiraling into anxiety afterward. That shift is the actual milestone — not the balance numbers.

Years 2 to 3: Full Stability Achieved

A three to six month emergency fund is complete. High-interest debt is gone. You are saving 20% or more and investing consistently toward retirement savings. Financial decisions feel manageable rather than terrifying. This is Level 3 stability. Most people who reach it describe it less as excitement and more as a quiet, unfamiliar sense of relief.

Years 5 to 15: The Path to Financial Freedom

If you want more than stability, this is the longer road. Building passive income from investments, real estate, or scalable businesses takes years of consistent effort. But the foundation you built in years one through three is what makes this phase even possible to attempt. Without it, the longer journey never gets started.

Tools and Resources to Make This Easier

The right tools do not replace the process, but they remove enough friction that people actually stick to it. Here are the specific ones worth your time.

Budgeting Tools (Free and Paid)

Notes app or Excel: The simplest starting point. Categorize your transactions by hand for the first 30 days. Free, fast, and fully under your control.

YNAB (You Need a Budget): A paid app built around zero-based budgeting and envelope budgeting principles — every dollar gets assigned to a specific category before you spend it, which eliminates the “where did that money go” problem entirely. Particularly useful for people who have tried free tools and not stuck with them.

Google Sheets: A free alternative to Excel with downloadable budgeting templates that handle the calculations automatically.

Investment Platforms for Beginners

Fidelity, Vanguard, and Schwab are the three platforms I recommend most consistently for beginner investors. All three offer low-cost index funds, Roth IRA and traditional IRA accounts, and genuinely useful educational resources. None of the three charge account minimums for basic index fund investing.

For a first investment, a target-date retirement fund or an S&P 500 index fund like VOO handles investment diversification automatically and requires almost no ongoing decisions from you.

Books and Podcasts to Accelerate Learning

Three books I consistently see recommended by people who made lasting financial change:

Rich Dad Poor Dad by Robert Kiyosaki reframes how you think about assets, liabilities, and the role money plays in building versus consuming.

Think and Grow Rich by Napoleon Hill focuses on mindset and the psychology of wealth building over time.

You Need a Budget by Jesse Mecham is a practical guide to the zero-based budgeting philosophy that the YNAB app is built on.

For daily reinforcement, personal finance podcasts during a commute or workout build consistent exposure to financial thinking without requiring dedicated reading time.

Your Next Action: Start This Week, Not Someday

Reading this and doing nothing with it is how this ends up as another piece of content that left you feeling informed without changing your situation. That is not what I want for you, and it is probably not why you read this far.

The commenter who replied to that 26-year-old in New York put it plainly: “The hardest thing to do is start when anxiety of everything else builds up. You have got this. Start small.” That is the honest version of the advice. Not motivational packaging just the truth about how the first step actually works.

Financial stability is not the result of one big right decision. It is the result of 200 small ones made consistently over the next 18 to 24 months. Start with the seven actions below.

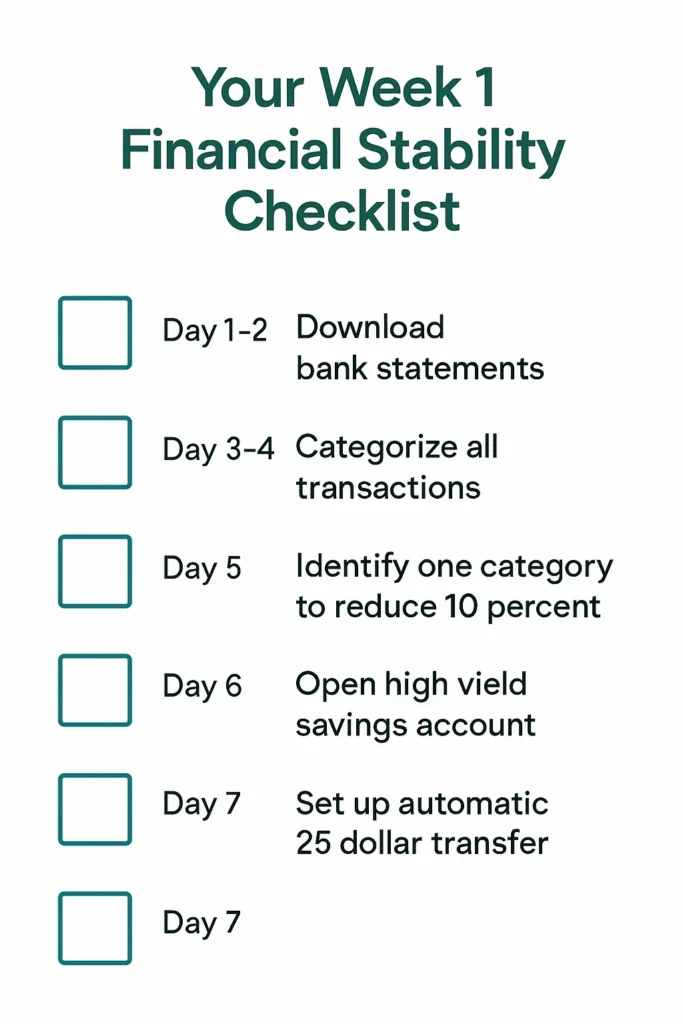

Your Week 1 Checklist (Copy This)

Day 1 and 2: Download your bank and credit card statements from the last two months.

Day 3 and 4: Open a spreadsheet or your notes app and categorize every transaction into three buckets: essentials, lifestyle spending, and subscriptions.

Day 5: Identify one spending category where you can reduce by 10% this month.

Day 6: Open a free high-yield savings account at an online bank if you do not already have one separate from your checking account.

Day 7: Set up an automatic transfer of at least $25 on your next payday, from checking to that savings account.

Seven days. Seven actions. None of them require money you do not have, a financial advisor, or anything other than 30 minutes and a spreadsheet. Do them in order.

Remember: Consistency Beats Perfection

There will be months where the budget breaks. An unexpected bill, a rough week, a purchase you regret those are going to happen. That is not a character problem. It is just what an 18-month process looks like when real life is running alongside it.

The people who reach financial stability are not the ones who never slip. They are the ones who slip and come back without treating it as proof that the whole thing was pointless.

Financial wellness is a practice, not a destination. And the version of you that comes back after a setback knowing what went wrong and why is genuinely better at this than the version who never tried.

Frequently Asked Questions About Becoming Financially Stable

Q: How long does it actually take to become financially stable?

The timeline depends almost entirely on the gap between your income and expenses. If you are starting from paycheck to paycheck, expect three to six months to save your first $1,000 and build consistent tracking habits. Paying off high-interest debt typically takes six to twelve months, depending on total balance and income. Reaching full stability a three to six month emergency fund, 20% savings rate, investing consistently generally takes 12 to 24 months. Financial freedom, where passive income covers your expenses, takes five to fifteen years. Behavior determines the timeline more than income level does.

Q: Can I become financially stable if I only make $30,000 per year?

Yes, and here is exactly why. Stability is about the surplus between income and expenses, not the income number itself. Someone earning $30,000 and saving 40% of it is more financially stable than someone earning $80,000 and saving nothing. The path involves reducing the three major expenses — housing, transportation, food — tracking spending to find waste, and gradually building income through skills. The path is longer at $30k than at $60k, but the framework is identical. For specific saving strategies for low-income earners, the focus shifts from complex tactics to simple high-impact changes that create immediate breathing room.

Q: Should I pay off debt or save for an emergency fund first?

Save a starter emergency fund of $1,000 first. Then attack high-interest debt. Then build the full three to six month emergency fund. The starter fund exists to prevent you from going back into debt every time life throws something unexpected at you during the debt payoff phase. Never clear out savings entirely to pay debt you will almost certainly need to borrow again before the debt is gone, and that puts you back at the beginning. Once your $1,000 buffer is in place, accelerated debt payoff strategies can help you clear high-interest balances faster than minimum payments alone.

Q: What is the difference between financial stability and financial freedom?

Financial stability means you save 20% or more monthly, hold a solid emergency fund, and feel no daily money stress but you still depend on your job. Financial freedom means your investment income covers all living expenses and employment becomes entirely optional. Stability is achievable in one to two years. Freedom typically takes five to fifteen years of consistent work built on top of that stability foundation. Most people find that reaching stability alone changes their daily relationship with money enough to make the longer journey feel genuinely worth pursuing.

Q: Do I really need to invest, or can I just save money in my bank account?

You need to invest. Saving without investing is not neutral — it is slow financial erosion. Inflation typically runs at three to four percent per year. If your savings account earns one percent, you are losing real purchasing power every year your money sits there. The emergency fund stays liquid in a high-yield savings account. Everything above that gets invested in low-cost index funds. The S&P 500 has historically returned approximately ten percent annually over long periods. Saving alone cannot match that, and over 20 years the gap is enormous.

Q: I tried budgeting before and it did not stick. What am I doing wrong?

You are probably treating it as a math problem when it is a behavior problem. The most common reasons budgets fail: the restrictions are too strict and snap when one hard week arrives, you are trying to fix too many things at once, and nothing is automated so willpower runs out within a month. The fix is three things: pick one spending category to reduce by 10% this month instead of overhauling everything, automate your savings transfer so willpower is no longer part of the equation, and track without making any cuts for the first 30 days before you restrict anything. The automation piece is the one most people skip. When saving happens automatically, the decision is already made. Understanding the key components of successful budgeting reveals why automation, tracking, and focused goals matter more than willpower ever will.

Q: What should I invest in as a complete beginner?

Start with a low-cost S&P 500 index fund inside a tax-advantaged account. If your employer offers a 401(k) match, contribute at least enough to capture the full match first that is free money. Then open a Roth IRA through Fidelity, Vanguard, or Schwab and invest in a fund like VOO or a target-date fund matching your retirement year. Invest consistently every month without trying to time the market. Start consistent, leave it alone, and let compound interest work over time. The market rewards patience more reliably than it rewards skill for most beginning investors.

Q: How much should I have in my emergency fund?

Phase 1: Save $1,000 or one month of essential expenses as your starter fund before tackling debt. Phase 2: After paying off high-interest debt, build to three to six months of essential expenses in a high-yield savings account. If you are a single-income household or work in an unstable industry, aim for six to twelve months. Single-income households and people in unstable industries should aim for the higher end six months of expenses is not paranoia, it is the cushion that keeps a job loss from becoming a debt spiral. Keep the entire emergency fund liquid. Never invest your emergency fund.