What Are High Yield Savings Accounts? (2026 Complete Guide)

Rates and figures in this guide reflect information verified as of early 2026. Savings rates change frequently always confirm the current APY directly with the bank before opening an account.

When I first came across high-yield savings accounts, my reaction was skepticism, not excitement. My money had always lived in the same big-bank checking account, earning what I now realize was essentially nothing. What I eventually discovered changed how I handle every dollar I save and it started with understanding what these accounts actually are and why they pay so much more.

So what are high yield savings accounts, exactly? They’re deposit accounts typically offered by online banks and some credit unions that pay significantly higher interest rates than the savings accounts most people grew up using. We’re talking 20 to 50 times more interest, not a marginal improvement. That gap is large enough to matter on any balance worth saving.

The rate gap is more dramatic than most people expect. Traditional brick-and-mortar banks typically pay between 0.01% and 0.10% on savings accounts, and while the national average sits slightly higher, it still hovers well below 1%. High-yield savings accounts, meanwhile, are currently paying between 4% and 5% or more depending on the bank and the current rate environment.

These are legitimate interest-bearing accounts, typically offered by online banks, and they operate just like the savings accounts you already know. You deposit money, it’s held securely, and you earn interest. The only real difference is the size of that return.

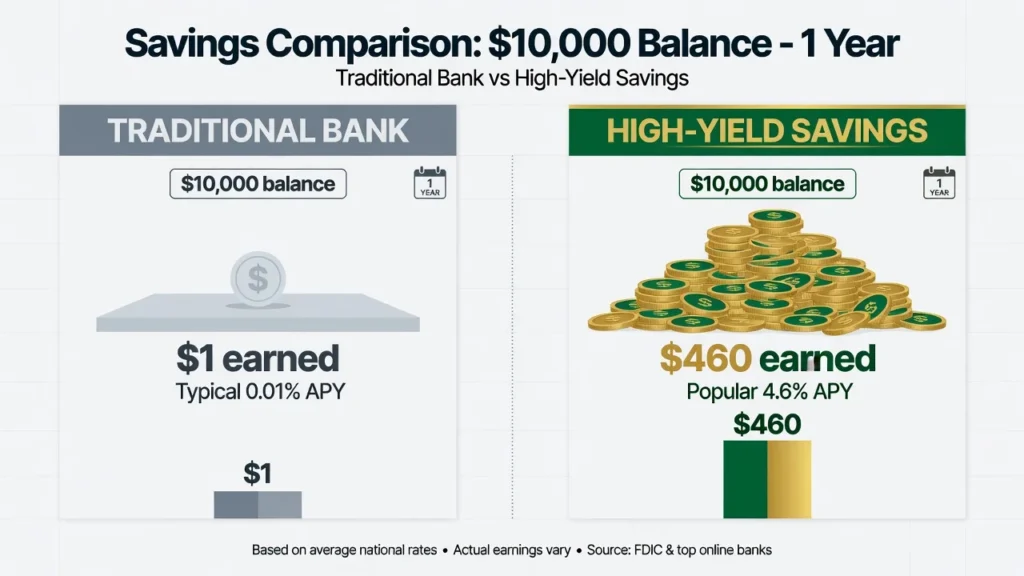

I ran these numbers myself during my research. Put $10,000 in a traditional bank at 0.01%, and after a full year you’ve earned exactly $1. One dollar. That same $10,000 sitting in a high-yield savings account at 4.6% APY earns roughly $460 over the same period.

The difference between $1 and $460 from the exact same balance, sitting in different deposit accounts, is not a rounding error. It’s the entire point of switching.

Most people I know myself included for years park their money in traditional banks without questioning whether they’re being paid fairly for it. The reasons are understandable: we trust the institutions we grew up using, we like having a branch down the street, and frankly, nobody tells you that dramatically better options exist.

By the end of this guide, you’ll know exactly how these accounts work, which ones are worth your time in 2026, and whether one belongs in your financial setup.

How Do High Yield Savings Accounts Work?

Before I moved any real money, I wanted to understand the mechanics not just take the rate on faith. The gap between 0.01% and 4.5% seemed too large to not have a straightforward explanation somewhere.

The mechanics are simpler than most people expect. You deposit money, and the bank calculates interest on your balance every single day a process called daily compounding, which is one reason these accounts grow faster than they initially appear to.

What makes this powerful is that the interest doesn’t just get tracked on paper it actually gets added to your balance each day. Tomorrow’s calculation runs on a slightly higher number. That’s compound interest working in your favour, and the effect becomes more meaningful the longer your money stays in the account.

Interest is paid monthly into your account balance though it’s calculated and credited to you daily.

One term tripped me up early on: APY, or annual percentage yield. Unlike a simple interest rate, APY already factors in the effect of compounding. When a bank advertises 4.6% APY, that’s the actual amount you’ll earn over a full year assuming your balance stays put.

Compounding frequency matters here. Rather than calculating and applying interest once a year, these accounts compound daily meaning your balance grows incrementally every single day.

The math gets striking when you run it across five years. Put $5,000 in a traditional account at 0.1%, and you’d walk away with about $25 in total interest. That same $5,000 in a high-yield account at 4.3% APY returns roughly $1,171 over those same five years a difference that funds several months of groceries, not just a cup of coffee.

APY vs. Interest Rate: What the Numbers Actually Mean for Your Balance

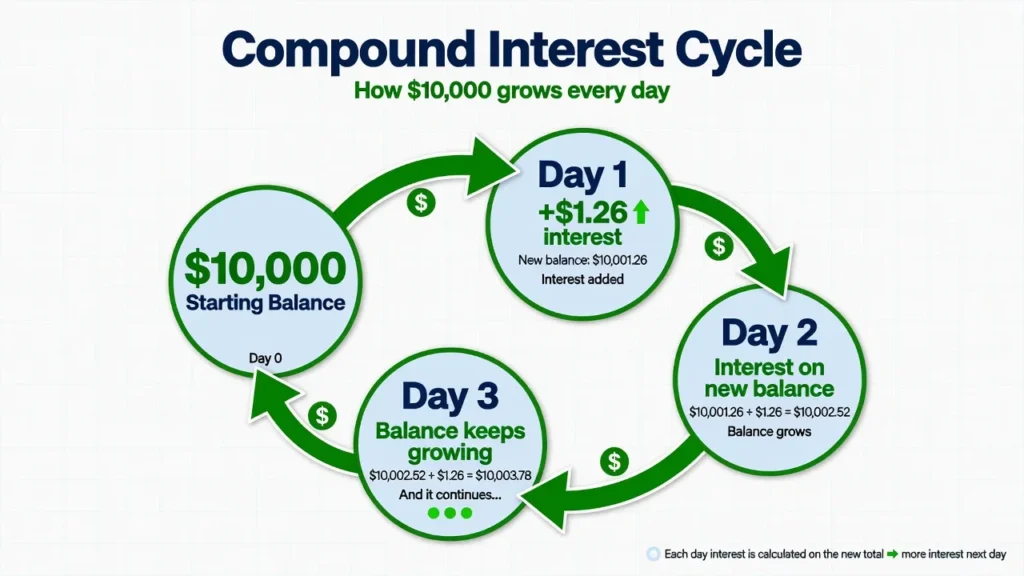

Daily compounding in practice looks like this. Take $10,000 in an account with 4.6% APY. The bank doesn’t hold your interest until year-end. Instead, every single day, it calculates that day’s portion based on your current running balance.

On day one, you earn about $1.26 in interest. That gets added to your balance. On day two, the bank calculates interest on $10,001.26, not just the original $10,000. On day three, it’s even higher. This process repeats every single day.

By the end of the month, you might have earned around $38. That $38 gets paid into your account, and now your new starting balance is $10,038. The next month’s interest calculation starts from this higher number.

Over a full year, you don’t earn exactly 4.6% of your starting $10,000. You earn slightly more because each month’s interest rolls into the next month’s calculation. The longer the money sits, the more meaningful that gap becomes.

Watching my own account balance move each day was unexpectedly motivating. It’s easy to dismiss a $1.26 daily gain until you notice, three months in, that the account is generating more per day than it was when you started without you adding a single dollar. If you want to calculate your own potential interest earnings based on your specific balance and time frame, running the numbers yourself can be equally eye-opening.

so tomorrow’s interest is calculated on a slightly higher amount.

Compounding a 0.01% rate is mathematically real but practically irrelevant you’re multiplying almost nothing. Compounding 4.6% is where it actually matters, and the gap between the two accounts widens not just each year but each month.

How Banks Can Afford to Pay You 50x More

If traditional banks could afford to pay more, they would so what are online banks doing differently? The answer isn’t complicated once you look at where the money actually goes.

Traditional brick-and-mortar banks carry enormous fixed costs: branch leases, utilities, maintenance, security, teller staff, ATM networks, and vaulting. When a bank is spending millions annually on physical infrastructure and payroll, there’s simply less left to pass along to depositors as interest.

Online banks operate without any of that physical overhead. No branches, no tellers, no downtown real estate. Their entire operation runs through a website and an app, which cuts costs to a fraction of what traditional banks carry. Those savings don’t disappear they get passed directly to customers through higher interest rates. That’s not a gimmick. It’s a more efficient business model.

There’s also the lending side of this. Banks profit from the spread between what they pay on savings deposits and what they charge on loans. Your deposit funds mortgages, car loans, and credit cards at interest rates far higher than what they pay you.

High-yield banks use attractive interest rates as a customer acquisition strategy. More deposits allow them to make more loans, which generates more profit. The cycle benefits them and you simultaneously which is why the model is sustainable rather than promotional.

Some online banks go further with features like same-day interest crediting you on the day you initiate a transfer, even before it clears. This kind of customer-focused feature is possible because online banks compete entirely on the quality of their product rather than the proximity of their branches.

High-yield banks can afford to pay more because they spend less and because competitive rates help them grow. The internet made this model possible, and depositors are the direct beneficiaries. There’s nothing complicated or risky about it it’s just a more efficient version of the same banking you’ve always done.

High Yield Savings vs Traditional Savings: The Real Numbers

Claims about 20x or 50x more interest sound impressive but abstract until you put specific dollar amounts against them. So I ran the numbers with balances most people actually hold in savings.

I compared both account types using three realistic balances: $5,000, $10,000, and $20,000.

What $10,000 actually earns in a traditional account at 0.01%:

- After 1 year: $1

- After 3 years: $3

- After 5 years: $5

Five dollars total over five years on ten thousand dollars.

In a high-yield account at 4.6% APY:

- After 1 year: ~$460

- After 3 years: ~$1,430

- After 5 years: ~$2,540

The numbers looked wrong to me the first time, so I recalculated. They weren’t wrong that gap is real, and it widens every year because compound interest amplifies the rate difference, not just the balance difference.

Scale that across different starting balances: $5,000 earns $0.50 versus $230 per year. $20,000 earns $2 versus $920. The pattern holds regardless of your starting balance the rate is always the dominant factor.

I showed these numbers to a friend with $15,000 sitting in a traditional savings account, earning roughly $1.50 per year. After she moved it to a high-yield account, she now earns close to $700 annually. That’s the difference between a number that doesn’t register and one that covers a car payment.

Comparison Table: High Yield Savings vs Traditional Savings

Here’s a direct comparison of what you’re actually choosing between when you evaluate these two account types, based on current figures from major banks.

| Feature | Traditional Savings | High-Yield Savings |

|---|---|---|

| Typical APY | 0.01% – 0.10% | 4.00% – 5.00%+ |

| Annual Earnings on $10,000 | $1 – $10 | $400 – $500+ |

| Monthly Maintenance Fees | $5 – $12 (unless min. balance met) | $0 |

| Minimum Balance | $500 – $1,500 (to avoid fees) | $0 – $500 (many require $0) |

| Account Access | Branch, ATM, online, mobile | Online and mobile (some offer ATM/debit) |

| Transfer Time | Instant at branch/ATM | 1–2 business days |

| FDIC / NCUA Insurance | Yes — up to $250,000 | Yes — up to $250,000 |

The table makes the trade-off clear: traditional banks offer physical convenience; high-yield banks offer better returns and lower costs. For most people with meaningful savings balances, the math heavily favours the latter.

$460 per year in a high-yield savings account.

What $10,000 Earns Over 5 Years: Compound Interest Year by Year

Traditional Account at 0.01% APY

| Year | Starting Balance | Interest Earned | Ending Balance |

|---|---|---|---|

| 1 | $10,000.00 | $1.00 | $10,001.00 |

| 2 | $10,001.00 | $1.00 | $10,002.00 |

| 3 | $10,002.00 | $1.00 | $10,003.00 |

| 4 | $10,003.00 | $1.00 | $10,004.00 |

| 5 | $10,004.00 | $1.00 | $10,005.00 |

High-Yield Account at 4.6% APY (daily compounding)

| Year | Starting Balance | Interest Earned | Ending Balance |

|---|---|---|---|

| 1 | $10,000.00 | $470.00 | $10,470.00 |

| 2 | $10,470.00 | $492.09 | $10,962.09 |

| 3 | $10,962.09 | $515.22 | $11,477.31 |

| 4 | $11,477.31 | $539.43 | $12,016.74 |

| 5 | $12,016.74 | $564.79 | $12,581.53 |

What makes the high-yield numbers compelling is the year-over-year growth in interest earnings themselves. Year one generates ~$470. By year five, that annual figure has climbed to ~$565 without a single additional deposit. The balance is doing the work, growing the base from which each year’s interest is calculated.

That realization was genuinely frustrating not at the bank, but at myself for not looking into it sooner. The money wasn’t stolen. I just didn’t know to ask. Which is why I’m laying all of this out as plainly as I can.

The longer your money stays in a high-yield account, the more the difference compounds. A meaningful interest rate is what activates that growth without it, time doesn’t work in your favour.

7 Major Benefits of a High Yield Savings Account

Based on my own research and first hand use, here are the seven benefits that matter most and why each one actually shows up in your account.

bank savings including dramatically higher interest and zero monthly fees.

Benefit 1: Earn Dramatically More Interest

The rate difference isn’t incremental it’s categorical. Moving from 0.01% to 4.6% isn’t a small upgrade; it’s a fundamentally different financial outcome from the same starting amount.

My old bank paid 0.01%. My high-yield account pays 4.6%. That’s 460 times more interest. Even using the national average traditional rate as the baseline, a 4.6% high-yield rate still delivers 10 times more.

For me, this translated from roughly $5 per year to over $400 per year. Same money, same safety, different bank. That’s not a marginal improvement it’s a different category of outcome.

Benefit 2: FDIC Insurance : Identical Safety to Traditional Banks

The natural assumption is that higher returns require accepting higher risk. With FDIC-insured savings accounts, that assumption doesn’t hold.

Both traditional banks and high-yield accounts offer the exact same protection. The Federal Deposit Insurance Corporation insures your deposits up to $250,000 per depositor, per bank. If the bank fails, you get your money back, guaranteed by the federal government. For credit unions, look for NCUA insurance the National Credit Union Administration provides the same $250,000 per depositor, per account-holder coverage that FDIC provides for banks. Both are federal government-backed protections.

Knowing the protection is identical made the decision straightforward. More interest, same safety floor. The only thing that changed was the rate.

Benefit 3: Full Liquidity : Access Your Money When You Need It

A common point of confusion is between high-yield savings accounts and CDs. They’re not the same. CDs lock your money in for a fixed term, with early withdrawal penalties. High-yield savings accounts offer full liquidity no penalties, no lock-in periods, no barriers to accessing your money when you need it.

When I had an unexpected expense, I logged into my high-yield account, initiated a transfer, and had the money in my checking account two business days later. Not instant, but definitely accessible when I needed it.

Benefit 4: Compound Interest That Builds on Itself

Compound interest is worth its own mention here because it’s the mechanism that separates a 4.6% account from a savings account that technically also compounds but at 0.01%. The rate is what matters. Compounding amplifies whatever rate you’re working with, for better or worse.

Watching month two generate slightly more than month one without adding money is when the mechanics stop being theoretical. The account is quietly building on itself.

Benefit 5: Zero Monthly Fees

One thing I genuinely didn’t expect: most high-yield savings accounts charge zero monthly maintenance fees. My traditional bank charged $12 per month unless I maintained a $1,500 minimum balance.

Run the numbers: $12 per month is $144 per year paid to the bank, while they paid me $5 in interest. Net result: I was $139 in the hole annually just for having a savings account.

Years of paying those fees without questioning them is money I can’t recover, but it’s also the clearest example I have of why financial inertia has a real cost one that’s easy to calculate and even easier to avoid going forward.

Benefit 6: The Ideal Home for Your Emergency Fund

My emergency fund lives in a high-yield savings account, and the logic is simple: an emergency fund needs to be safe, accessible, and ideally earning something while it waits. High-yield accounts satisfy all three requirements without compromise. FDIC insurance handles safety. The one-to-two-day transfer timeline handles access. And unlike leaving the money in checking, it’s earning 4% to 5% in the meantime which on a $15,000 fund adds up to meaningful money each year.

Consider someone with $20,000 in an emergency fund. At a traditional bank’s 0.01% rate, that earns $9 per year. At 4.6%, the same balance generates $920. That difference covers two months of utility bills from money that was going to sit untouched regardless.

The principle scales to any balance. Money that’s meant to sit untouched might as well earn while it does.

Benefit 7: Zero Market Risk

The natural assumption is that higher returns require accepting higher risk. High-yield savings accounts provide risk-free savings in the truest sense. The balance only moves when I move it. Rates can fluctuate, but principal and accumulated interest are protected that’s a guarantee no market investment can offer for short-term money.

I use both savings and investments now. Long-term retirement money goes into index funds. Short-to-medium-term savings goes into my high-yield account. Each tool serves its purpose.

Why Most People Still Use Traditional Banks and When It Actually Makes Sense

If high-yield savings accounts consistently outperform traditional accounts on every financial metric that matters for most savers, why hasn’t the majority of the country switched? That’s not a rhetorical question the reasons are specific and worth understanding.

According to Bankrate research, the majority of Americans have stayed with the same bank for more than a decade. We default to what’s familiar, even when better options are available and easy to access.

Banks understand this inertia and invest heavily in it. Maintaining branch networks, running brand advertising, sponsoring sports arenas none of that is accidental. It’s a calculated bet that most customers won’t bother to look for alternatives.

Some people genuinely value physical access over returns. It’s a valid trade-off. If having a branch nearby reduces financial anxiety or makes banking easier for your lifestyle, that preference deserves respect as long as it’s a conscious choice, not a default.

The Real Cost of Convenience

Someone keeping $12,000 at a traditional bank earning 0.01% takes home $1.20 per year in interest. Just over a dollar annually on twelve thousand dollars.

At 4.5% in a high-yield account, that same $12,000 generates $540 per year. Same money, same safety, different bank. The gap between what you’re earning and what you could be earning: $538 per year.

I calculated my own cost of convenience. I had kept about $15,000 in my traditional bank for six years. At the rate I was earning, I made less than $10 total over those six years. If I had moved that money to a high-yield account earning 4.6%, I would have earned over $4,000 in that same period.

Four thousand dollars. A vacation. A car repair. Several months of groceries. All of it sitting uncollected, simply because I never asked whether a better option existed.

I’m not saying that was the bank’s fault. They didn’t steal from me. I chose to keep my money there. But banks do benefit enormously from customers not understanding or not caring about the difference. They pay you almost nothing, lend your deposits at much higher rates, and profit from that spread. Meanwhile, you’re earning less in a year than you’d spend on lunch.

When a Traditional Bank Is Actually the Right Choice

There are legitimate situations where a traditional bank is the better fit:

If you regularly deposit cash. High-yield accounts are almost all online-only. You can’t walk into a branch and hand them cash. If you run a cash-based business or frequently receive cash, you’ll need a traditional bank for deposits. You can then transfer money to your high-yield account once it’s in the banking system.

If you need immediate access to large amounts of cash. While high-yield accounts can get you money in one to two days, that’s not instant. If your car breaks down and you need $2,000 today, having some money at a traditional bank with immediate access can be valuable.

If you’re not comfortable with online banking. If you genuinely prefer or need in-person assistance, a traditional bank may be your only realistic option for day-to-day management.

I do this myself. One month of expenses stays in my traditional checking account for immediate needs. The rest of my emergency fund sits in my high-yield account earning real interest giving me both instant access when I need it and growth when I don’t.

Know what the convenience costs before deciding it’s worth it. For most people with meaningful savings balances, the math will point clearly toward a high-yield account. But the exceptions are real, and they should inform your decision.

Disadvantages of High Yield Savings Accounts (What to Know Before Opening One)

High-yield savings accounts are genuinely better than traditional accounts for most people in most situations. But every financial product has trade-offs, and these are worth understanding before you move your money.

Drawback 1: Variable Interest Rates

The rate you see advertised today is not guaranteed forever. High-yield savings accounts have variable interest rates that go up and down based on broader economic conditions and decisions by the Federal Reserve.

Current rates sit in the 4% to 5% range, but that won’t always be the case. During the low-rate environment of 2020 to 2022, even the best high-yield accounts paid under 1%. The rate you see today reflects the current Federal Reserve policy environment, not a permanent baseline.

The rate you’re earning today will eventually change. That’s the nature of variable-rate accounts tied to Federal Reserve policy. What matters is whether the account continues to pay competitively relative to other options and that’s something worth monitoring.

How Rates Connect to Federal Reserve Policy

Savings account rates are closely tied to what the Federal Reserve does. When the Federal Reserve raises its benchmark interest rate to fight inflation, banks can afford to pay higher rates on deposits. When the Fed lowers rates to stimulate the economy, deposit rates fall.

During the Fed’s aggressive 2022–2023 rate increases, my high-yield account rate climbed from around 2% to over 4% in under twelve months. Those same rates moved the other direction when the Fed began cutting.

What I do have control over is choosing an account that pays competitively whatever the overall rate environment is. Some banks adjust their rates quickly to stay competitive. Others let their rates lag. I pay attention to this and am willing to switch banks if my current rate falls significantly behind what others are offering.

Drawback 2: No Physical Branches

Almost all high-yield savings accounts come from online-only banks no branches, no tellers, no walk-in access. Everything is handled through a website or mobile app.

Transfer Times and Withdrawal Limits

When I need money from my high-yield savings account, I have to initiate a transfer to my checking account and wait. Typically, this takes one to two business days. If I need money on a Monday, I’ll usually have it by Wednesday. That’s fast enough for most situations, but it’s not immediate.

Some high-yield accounts still limit withdrawals or transfers to six per month a holdover from Regulation D, the federal rule that historically restricted savings account transactions. While the Federal Reserve suspended mandatory enforcement of this rule in 2020, many banks keep the six-transaction limit in place as an internal policy. If you exceed the limit, some banks charge a per-transaction fee or convert your account to a checking account. For most savers, this limit is never an issue but it’s worth knowing if you tend to move money frequently.

What You Give Up Without Branch Access

You can’t walk in and withdraw cash. Some high-yield accounts offer debit cards and ATM access, but many don’t and those that don’t require you to transfer money to another account before spending or withdrawing.

For many people, these limitations don’t matter. I almost never use cash anymore. But for others especially older customers or people who prefer in-person service these are real disadvantages that might outweigh the higher interest rate.

Can You Lose Money in a High Yield Savings Account?

The question that holds most people back: can you actually lose money in these accounts? It’s a reasonable concern given the higher rates. The short version is no.

You cannot lose your principal in a properly insured high-yield savings account. Your principal is protected. The interest you earn is locked in. The account balance only goes down if you withdraw money yourself.

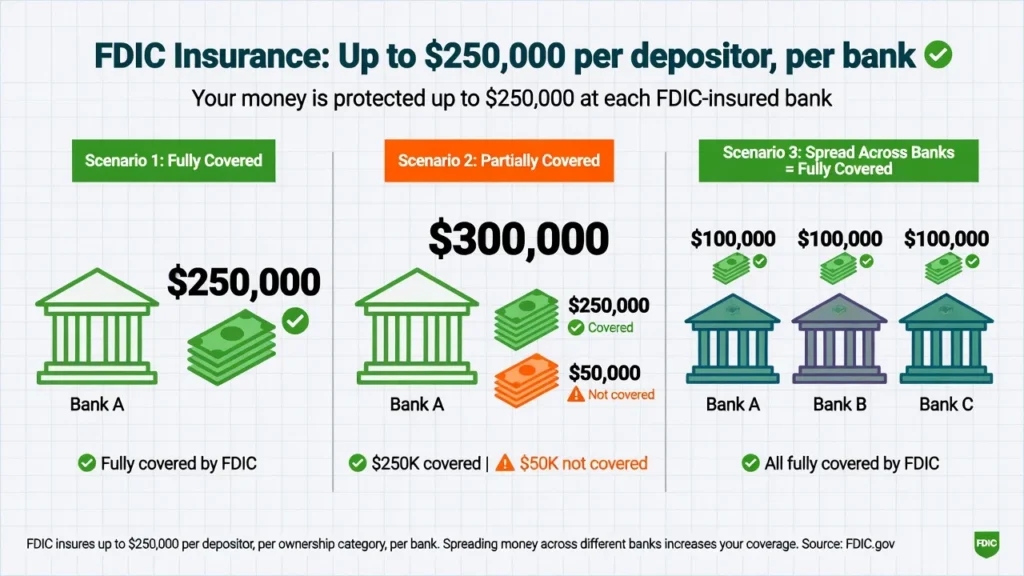

High-yield savings accounts at legitimate banks are covered by FDIC insurance the same insurance that protects deposits at traditional banks. The Federal Deposit Insurance Corporation, backed by the federal government, guarantees your deposits up to $250,000 per depositor, per bank, per account ownership category.

I verified that my high-yield account was FDIC insured before I deposited money. This information is clearly stated on the bank’s website and in the account documentation. If you’re looking at a high-yield account, make absolutely sure it has FDIC insurance or, if it’s a credit union, NCUA insurance, which provides equivalent protection.

FDIC and NCUA Insurance Explained

FDIC insurance covers $250,000 per depositor, per insured bank, per account ownership category. Breaking that down: “per depositor” meaning per account holder means the limit applies to you individually. You and your spouse each get $250,000 in individual accounts at the same bank. A joint account between you would get another $250,000 of separate coverage.

“Per insured bank” means the limit is per financial institution, not per account. If you have three savings accounts at the same bank with $100,000 in each, you have $300,000 total at that one bank, and only $250,000 is insured. But if you have $100,000 at three different banks, all of it is insured because it’s spread across different institutions.

exceeding this limit at a single institution are not insured.

Some high-yield accounts offer extended FDIC coverage beyond the standard $250,000 limit a feature most people don’t know exists. SoFi and Wealthfront, for example, advertise coverage up to $2 million and $5 million respectively through partner bank networks.

[Editor note: Verify current extended coverage limits for both banks as of 2026.]

These companies partner with multiple banks. When you deposit money, they automatically spread it across several partner banks in amounts that keep each portion under the $250,000 limit at any single institution. Your entire balance is insured even if it exceeds the usual limit.

The Inflation Risk Nobody Talks About

There’s one risk these accounts carry that most people don’t discuss: inflation. While your principal is safe, inflation can erode your purchasing power the actual value of what your money can buy.

If inflation runs at 3% per year, something that costs $100 today will cost $103 next year. Your money buys less as time goes on.

If your high-yield account pays 4.3% interest but inflation is running at 2.5%, your real return is only 1.8%. You’re earning 4.3%, but prices are rising 2.5%, so your actual purchasing power only increases by the difference.

This becomes a problem if inflation exceeds your interest rate. If inflation hits 5% while your account pays 4%, you’re technically earning interest, but your money is buying less each year. You haven’t lost dollars, but you’ve lost purchasing power.

This played out clearly during the 2021–2023 inflation surge. Even with my account earning 4%, inflation peaked above 8% at its worst point meaning my savings were losing purchasing power despite the interest income.

Compare this to traditional savings accounts paying 0.01% when inflation is 2.5%. You’re losing 2.49% of purchasing power every year. Your balance stays the same in dollars, but those dollars buy less and less. It’s like your money is slowly evaporating.

High-yield accounts help protect against inflation by earning rates that are at least close to or above inflation. They won’t make you rich, but they prevent your savings from losing value as badly as they would in a traditional account.

The key is understanding what these accounts are for. They’re not wealth-building tools. They’re safe places to park short-to-medium-term savings while earning a reasonable return that helps offset inflation. Within that purpose, they work extremely well.

The opportunity cost of keeping long-term money in savings instead of investments is one of the most expensive silent mistakes in personal finance especially when it spans years or decades.

When to Use a High Yield Savings Account: The Best Use Cases for Your Money

High-yield savings accounts aren’t right for every dollar you own. There are specific categories of money they’re nearly perfect for and understanding which categories those are changed how I organize my entire financial approach.

Use Case 1: Emergency Fund

An emergency fund needs three things: it must be safe from market losses, accessible within a few days, and earning something while it waits. High-yield accounts satisfy all three. FDIC insurance handles safety. The one-to-two-day transfer timeline handles access. And unlike leaving the money in checking, it’s earning 4% to 5% in the meantime.

I keep three to six months of living expenses in my high-yield savings account as my emergency fund. For me, that’s about $15,000. At 4.6%, that earns me roughly $690 per year just sitting there, available if I need it. Compare that to the $1.50 it would earn in my old traditional account.

When I had unexpected medical expenses, I logged into my high-yield account, initiated a transfer, and had the money in my checking account two business days later. The bill was paid on time. And because the account had been compounding in the months before I needed it, I withdrew slightly more than I had originally deposited.

Use Case 2: Short-Term Goals (House, Car, Wedding)

Any goal that’s one to five years away is well-suited for a high-yield savings account things like saving for a house down payment, a car purchase, a wedding, or a major vacation.

If I need the money within five years, I don’t want it in the stock market where it could lose value right before I need to use it. But I also don’t want it earning nothing while I save up.

I watched a friend make this mistake. He was saving for a down payment and put the money in stocks because he wanted it to grow faster. The market dropped 20% the year before he wanted to buy. His down payment fund shrank by thousands of dollars. He either had to wait longer for the market to recover or buy with a smaller down payment than planned.

I saved for a vacation this way instead. I knew I wanted to travel in 18 months. I set up automatic monthly transfers from my checking to my high-yield savings account. By the time I was ready to book flights and hotels, I had more than I originally planned because of the accumulated interest. If finding money to save feels challenging, strategies to save money faster can help you identify areas to cut back and build your savings more quickly.

Use Case 3: Parking Money Before Investing

Sometimes I have money that I know I’ll invest eventually, but I’m not ready to invest it right now. Maybe I’m saving up to reach a certain amount before investing. Maybe I’m waiting for a better market opportunity. Maybe I just need time to research where to invest. A high-yield savings account keeps that money productive in the meantime.

Use Case 4: Sinking Funds

Sinking funds are money you set aside for expenses you know are coming but that don’t happen monthly annual insurance premiums, property taxes, holiday shopping, or home maintenance.

For example, my car insurance costs $1,200 per year. Instead of scrambling to find $1,200 when the bill arrives, I set aside $100 per month. That money sits in my high-yield account earning interest until I need it.

Building Your Emergency Fund (3 to 6 Months)

Financial experts recommend keeping three to six months of expenses in an emergency fund. If you have stable employment and good insurance, three months might be enough. If your income is variable or you’re self-employed, six months is smarter. Beyond the basic rule, how much you should have saved at different life stages can help you set more specific targets based on where you are in your financial journey.

The Savings Buckets Strategy

Some banks make goal-based saving straightforward. Ally Bank, for example, has a feature called Savings Buckets. Within one account, you can create separate buckets for different savings goals emergency fund, house down payment, vacation fund each with its own labeled balance.

Other people use completely separate accounts at different banks for each major goal. This works especially well if you’re trying to maximize interest rates, since different banks sometimes offer different rates.

The key is organization. When money is categorized by purpose, you’re less likely to dip into savings for non-emergencies.

Naming accounts with specificity matters more than most people expect. “Six Month Emergency Fund” creates a different psychological barrier than “Savings.” “House Down Payment 2027” makes it harder to redirect that money casually than a generic account label ever would.

When NOT to Use a High Yield Savings Account

High-yield savings accounts are not the right vehicle for every dollar you own. There are specific situations where using them is actually a mistake and those situations cost people more money than keeping too much at a traditional bank.

Wrong Use 1: Long-Term Retirement Money

The biggest mistake I see people make is using high-yield savings accounts for retirement or other long-term goals that are 10, 20, or 30 years away. This feels safe, but it’s actually costing you enormous amounts of money over time.

The numbers tell the story clearly. A high-yield savings account at 4% to 5% and an S&P 500 index fund historically averaging 8% to 10% look similar in the short term. Over 30 years, they produce completely different outcomes.

At 4% in a savings account, $10,000 becomes about $32,400 over 30 years. At 8% in stock market index funds, that same $10,000 becomes about $100,600. The difference is over $68,000 from the same starting amount.

I watched a coworker keep his entire retirement savings in a high-yield account, earning 4% safely and feeling confident about it. Over 30 years, the difference between 4% and 9% turns $50,000 into either $162,000 or $663,000. That gap $501,000 is retirement security versus financial stress in your later years.

Wrong Use 2: Money You Need Instantly

High-yield accounts have that one-to-two-day transfer delay. For most purposes, this is fine. But if you need money instantly, regularly, these accounts don’t work well for that purpose.

Wrong Use 3: Balances Exceeding FDIC Coverage

FDIC insurance covers up to $250,000 per depositor, per bank. If you have more than that at a single institution, the excess is not insured. For balances that exceed FDIC coverage limits, Treasury Bills are worth investigating as an alternative. T-Bills are direct U.S. government debt instruments, considered among the safest investments available.

Wrong Use 4: Regular Cash Withdrawals

Most high-yield accounts are online-only. If you genuinely need physical branch access regularly, or make frequent cash withdrawals, these accounts may not work for your day-to-day needs.

The Long-Term Investing Mistake

Years ago, I kept over $20,000 in savings convinced I was being financially responsible. I wasn’t scared of investing, exactly I just kept finding reasons to wait. The comfort of seeing a stable balance felt like prudence.

Then I learned about inflation and opportunity cost. Even though my savings was earning interest, inflation was eating away at the purchasing power. And by not investing for the long term, I was missing out on compound growth that would have made my money grow much faster.

HYSA vs Other Savings Options: Quick Comparison

| Vehicle | Best For | Rate Range | Risk | Access |

|---|---|---|---|---|

| High-Yield Savings Account | Emergency funds, 1–5 year goals | 4%–5%+ APY | None (FDIC insured) | 1–2 business days |

| Money Market Account | Similar to HYSA but with check-writing/debit access | Comparable to HYSA | None (FDIC insured) | 1–2 days or instant with debit |

| Certificate of Deposit (CD) | Known fixed-date goals; slightly higher guaranteed rate | Slightly above HYSA | None if held to term | Locked until maturity |

| Index Funds (S&P 500) | Long-term goals (5+ years), retirement | ~8%–10% historically | Market risk | Days (sell + settle) |

A money market account is similar to a high-yield savings account in rate and safety, but it typically includes check-writing privileges and a debit card for more direct access to your funds. Use one if you want comparable interest rates with slightly more spending flexibility.

CDs lock your money in for a fixed term but often pay a slightly higher guaranteed rate. Consider a CD laddering strategy spreading money across CDs with staggered maturity dates if you have predictable, periodic cash needs and want to maximize guaranteed rates.

Top High Yield Savings Accounts Compared (2026)

After researching and personally using several of these accounts, I can say there’s no single best option for everyone. The right account depends on what you’re optimizing for: highest rate, ATM access, extended insurance, or organizational features.

My Banking Direct Frequently offers one of the highest APYs among online banks. No monthly fees, no minimum balance. Best for rate-seekers who want maximum yield and don’t need ATM access.

Wealthfront Cash Account Offers extended FDIC coverage up to $5 million through its partner bank network. Competitive APY. Best for savers with large balances who need coverage above the standard $250,000 FDIC limit.

SoFi High-Yield Savings Competitive APY available with qualifying direct deposit setup. Without direct deposit, the rate drops significantly so read the account requirements carefully before opening. Also offers extended FDIC coverage through partner banks.

Ally Bank Strong reputation for customer service and usability. Features include Savings Buckets for goal-based saving and a competitive base APY with no minimum balance. Best for savers who want organizational tools alongside a solid rate.

American Express High Yield Savings Backed by a major financial institution. No debit card or ATM access transfers to an external account are required to access funds. Best for people who want a large, established brand with competitive rates and don’t need debit access.

Marcus by Goldman Sachs Verify Marcus product availability for 2026. Goldman Sachs announced significant changes to the Marcus consumer banking line in 2024. Confirm whether this savings account is still actively offered before including it.

My honest advice: don’t agonize over 0.25% rate differences. Getting your money out of a traditional account earning near-zero and into any competitive high-yield account is the move that matters. The difference between first and second place is minor; the difference between any of these and a traditional bank is enormous.

The biggest mistake is analysis paralysis researching endlessly while your money sits earning almost nothing. Pick one from this list that meets your basic requirements and open it. Perfection is the enemy of meaningful action here.

How to Open a High Yield Savings Account (Step by Step)

Step 1: Choose Your Bank

Pick a bank from the comparison above that fits your priorities. If you want the highest rate, sort by APY. If you want extended insurance, look at Wealthfront or SoFi. If you want organizational features, consider Ally.

Step 2: Gather Your Information

You’ll need your Social Security number, a government-issued ID (driver’s license or passport), your current address, and your existing bank account and routing numbers for the initial transfer.

Step 3: Complete the Application

Most applications take 10 to 15 minutes online or through the bank’s mobile app. You’ll fill in your personal details and answer identity verification questions.

Review the account disclosures. They cover fees, withdrawal limits, and rate change policies — worth at least reviewing the key terms before agreeing.

Step 4: Verify Your Existing Bank Account

The bank needs to confirm you own the account you’re transferring from. Some banks use instant verification through third-party services like Plaid, which let you log in to your existing bank through a secure portal to verify ownership instantly no test deposits needed. Others use micro-deposits (two small amounts sent to your account, which you confirm).

Step 5: Fund Your Account

Transfer money from your existing account. I started with a smaller test deposit the first time — maybe $100 or so just to make sure everything worked correctly. Once I confirmed the money arrived and I could access the account, I transferred the rest of my savings.

Step 6: Set Up Automatic Transfers

Set up recurring automatic transfers from your checking account to make saving consistent. Even $100 per month compounds meaningfully over time in a high-yield account.

Tax Implications: What You Need to Know

One thing nobody mentioned before I opened my first account: the interest you earn is fully taxable. Every dollar of interest gets added to your income for the year, and you owe taxes on it at your ordinary income tax rate.

Banks report the interest they pay you to the Internal Revenue Service. If you earn more than $10 in interest during the year, the bank sends you a form called a 1099-INT. They also send a copy of this form to the IRS, so the government already knows how much interest you earned before you even file your taxes.

The actual tax you owe depends on your tax bracket. If you’re in the 22% federal tax bracket and you earned $500 in interest, you’ll owe $110 in federal taxes on that interest. The $500 doesn’t increase your tax bracket. It just gets taxed at whatever bracket you’re already in.

Understanding Your 1099-INT Form

The 1099-INT is a simple form that shows how much interest you earned. The bank sends it to you by mail, though some banks make it available electronically if you’ve opted for paperless statements.

Keep the form for at least three years in case the IRS ever questions your tax return. Store it with your other tax records from that year.

The important thing to remember is that even if you somehow don’t receive the form, you’re still required to report the interest. The IRS has a copy, so they know you earned it. Failing to report it can lead to penalties and interest charges that cost more than the taxes you were trying to avoid.

How Much Tax Will You Actually Owe?

Federal income tax brackets for 2026 follow the same basic tiers established in recent years: 10%, 12%, 22%, 24%, 32%, 35%, and 37% depending on your total income.

[Editor note: Verify current 2026 bracket income thresholds at IRS.gov, as inflation adjustments change these figures annually.]

A real example: I earned $680 in interest in a given tax year. In the 22% federal bracket with a 5% state income tax:

- Federal tax: $680 × 22% = $149.60

- State tax: $680 × 5% = $34.00

- Total tax owed: $183.60

- Amount kept after tax: $496.40

Out of $680 earned, I kept $496.40. Compare that to my old traditional account where I earned maybe $6 in interest for the year. Even after paying taxes on the higher interest, I came out over $490 ahead.

The taxes are real and you need to plan for them, but they don’t negate the benefit. I set aside about 25% of my interest earnings throughout the year so I’m not caught off guard at tax time. If you’re looking for ways to reduce your tax liability, there are strategies to minimize your tax burden on savings interest that are worth understanding.

7 Common Mistakes to Avoid

Mistake 1: Falling for Promotional Rates

Some banks advertise incredibly high rates to attract new customers, but these rates drop after a few months. I almost fell for this with an account offering 5.5% APY. When I read the fine print, that rate only lasted three months before dropping to 2%.

Another version is accounts that require specific conditions to earn the advertised rate. Some banks require qualifying direct deposits for their highest rate without that setup, the rate drops significantly. Always read the account requirements carefully before opening.

Mistake 2: Keeping Long-Term Retirement Money in Savings

This deserves emphasis because the financial cost is enormous and the mistake is common.

I watched a coworker keep his entire retirement savings in a high-yield account, earning 4% safely and feeling confident about it. Over 30 years, the difference between 4% and 9% turns $50,000 into either $162,000 or $663,000. That gap $501,000 is the difference between retirement security and financial stress in your later years.

High-yield savings accounts are excellent for short-to-medium-term money. They are the wrong tool for long-term wealth building.

Mistake 3: Not Checking Minimum Balance Requirements

Some accounts advertise great rates but require you to maintain a certain minimum balance to actually earn that rate. If your balance drops below the threshold, you may earn a much lower rate or pay fees. Read the account requirements before transferring money.

Mistake 4: Moving All Your Money at Once

I made this mistake myself when I first opened my account. I was so excited about earning interest that I moved every dollar I had into my high-yield account. Then I needed to pay an unexpected bill quickly and realized I couldn’t access the money for two days. Keep at least one month of expenses in a traditional checking account for immediate access.

Mistake 5: Exceeding Monthly Withdrawal Limits

Some high-yield accounts limit you to six withdrawals or transfers per month. I didn’t know this when I first started and came close to hitting the limit one month when I was moving money around frequently. Check your account’s transaction limits before opening.

Mistake 6: Not Comparing Rates Regularly

Interest rates change constantly. The rate that was competitive when you opened your account might fall behind over time. Set a calendar reminder every six months to check whether your current rate is still competitive with what other banks are offering. Switching banks is easier than most people think.

Mistake 7: Staying Put Out of Inertia

Inertia is the most expensive mistake in personal finance not bad decisions, but non-decisions. The decision to keep money at a traditional bank because switching feels like a hassle, while losing hundreds of dollars a year to the status quo.

Final Verdict: Should You Get a High Yield Savings Account?

Yes get a high-yield savings account if you have liquid savings you want to keep safe and accessible. The conditions that make it the right choice are straightforward.

Get a high-yield savings account if you:

- Have an emergency fund sitting in a traditional account earning near-zero

- Are saving toward a goal that’s one to five years away

- Want FDIC-insured safety with no market risk

- Can tolerate a one-to-two-day transfer window for access

- Don’t need to make frequent cash deposits at a branch

You may want to reconsider if you:

- Regularly deposit cash and need branch access

- Need immediate access to funds on a daily basis

- Have balances significantly above $250,000 at a single institution (though extended coverage options solve this)

Action Steps If You’ve Decided to Move Forward

- Choose a high-yield savings account from the comparison section above based on your priorities (rate, access, features, insurance coverage)

- Gather your Social Security number, government ID, and current bank account details

- Complete the 10–15 minute online application

- Verify your existing bank account through Plaid or micro-deposits

- Start with a small test transfer ($100–$500) to confirm the process works

- Move the bulk of your short-term savings once you’ve confirmed access

- Set up automatic monthly transfers to build the savings habit. If you’re struggling to find money to save regularly, reducing your monthly expenses can free up funds for consistent transfers without feeling financially stretched.

One final question worth asking about any financial arrangement: who benefits more from it you or the institution?

This isn’t about getting rich from savings interest. Even at 5%, savings accounts don’t build wealth on their own. It’s about getting fairly compensated for money you’ve already worked to earn, rather than handing the bank a free loan.

Reading this without acting is the most common outcome. The information is clear. The math is not ambiguous. The only variable is whether you spend 10 minutes opening an account this week or continue doing what you’ve been doing.

One choice generates hundreds or thousands of dollars per year. The other costs nothing upfront and nothing ongoing except the interest you’re not collecting.

Frequently Asked Questions

How do banks afford to pay 20x to 50x higher interest rates than traditional banks?

Online banks eliminate the overhead costs of physical branches rent, utilities, tellers, ATM networks. Those savings get passed to customers as higher interest rates. It’s not a promotional trick. It’s a structural cost difference made possible by internet-only banking.

Are high-yield savings accounts safe?

Yes. Deposits at FDIC-insured banks are protected up to $250,000 per depositor, per bank the same protection offered by traditional banks. Credit unions offer equivalent protection through NCUA insurance. Your principal cannot decrease in a properly insured high-yield savings account.

How much does $10,000 earn in a high-yield savings account?

At 4.6% APY with daily compounding, $10,000 earns approximately $460 to $470 in the first year. The same balance in a traditional account at 0.01% earns $1. The gap widens each year as compound interest builds on the growing balance.

Can you lose money in a high-yield savings account?

No, not your principal. Your balance only decreases if you withdraw money yourself. Rates can fluctuate, but your deposited money and previously earned interest are always protected under FDIC or NCUA insurance.

What is the difference between APY and interest rate?

APY (annual percentage yield) already includes the effect of compounding. A simple interest rate does not. When a bank advertises 4.6% APY, that is the actual amount you’ll earn over a full year on a stable balance, including the benefit of daily compounding.

How do I choose between a high-yield savings account and a CD?

Use a high-yield savings account for money you might need access to emergency funds, short-term goals, sinking funds. Use a CD if you know exactly when you’ll need the money, can commit to not touching it, and want a slightly higher guaranteed fixed rate.

Which bank has the best high-yield savings account?

The best account depends on your priorities. For the highest rate, compare current APYs at My Banking Direct and similar online banks. For organizational tools, Ally’s Savings Buckets feature is useful. For extended FDIC coverage above $250,000, Wealthfront and SoFi offer partner bank networks. Rates change frequently always verify current APY directly with the bank.

This article is for informational purposes only and does not constitute financial advice. Interest rates, FDIC coverage structures, and bank product offerings change frequently. Verify all figures directly with financial institutions and the FDIC (fdic.gov) before making financial decisions.