How Much Credit Card Debt Is Too Much? Your Personal Debt Diagnosis

I’m cutting straight to it because I know you’re anxious about this question I’ve been there myself, staring at my credit card statements at 2 AM wondering if I’d crossed the line.

So how much credit card debt is too much? You’ve hit that threshold when one of three things happens: your balances exceed 30% of your total credit limits, your monthly debt payments consume more than 36% to 43% of your gross monthly income, or you can’t cover minimum payments without skipping essentials like groceries or utilities.

After 15 years advising clients on debt recovery and analysing hundreds of personal finance cases, I’ve learned that “too much” isn’t just about numbers it’s deeply personal and depends entirely on your income, your expenses, and what’s actually happening in your life right now.

I learned this from Katie’s story a composite of several real clients I’ve worked with in my financial advisory practice. She makes $83,000 a year, which is solid income by most standards. But after paying rent, utilities, her son’s private school, and everything else, she has exactly $10 left when she gets paid.

That $10 is supposed to cover emergencies, unexpected expenses, and debt repayment. Unsurprisingly, it covers none of those things. Her $27,000 in credit card debt across six cards isn’t about making bad decisions with money. It’s about having no breathing room whatsoever.

The metrics I’m about to show you matter because they transform guessing into knowing. Instead of wondering whether your credit card debt is too much, you’ll calculate your exact position using two industry-standard measurements.

Katie’s DTI immediately revealed the real problem. she made decent money but had zero financial flexibility. The question you’re really asking isn’t “Am I normal?” It’s “Am I in trouble?” and we can answer that with two simple calculations.

Two Critical Metrics That Determine Your Debt Level (And How to Calculate Them)

Most people get stuck here: they know they have credit card debt, but they can’t tell if it’s manageable or dangerous. Nobody taught them the two measurements that financial advisors actually use to assess debt burden.

I’m walking you through both calculations right now. By the end of this section, you’ll know your exact numbers and understand precisely where you stand.

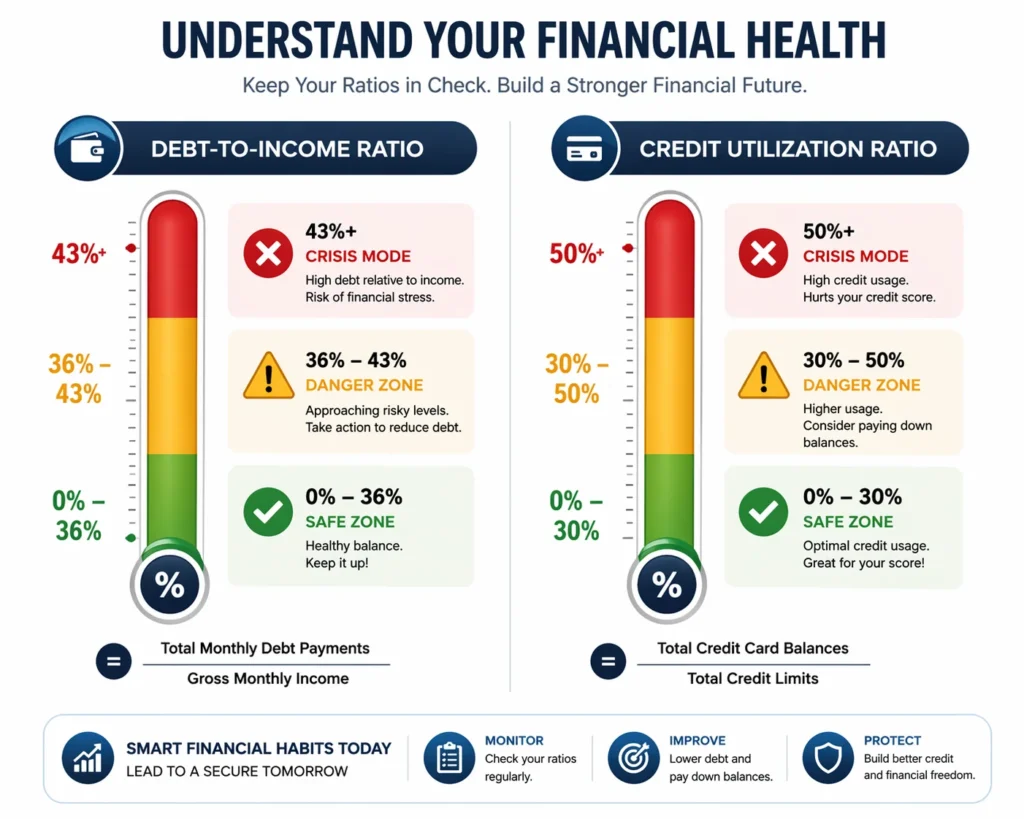

Metric #1: Your Debt-to-Income Ratio (DTI) : The 36-43% Danger Zone

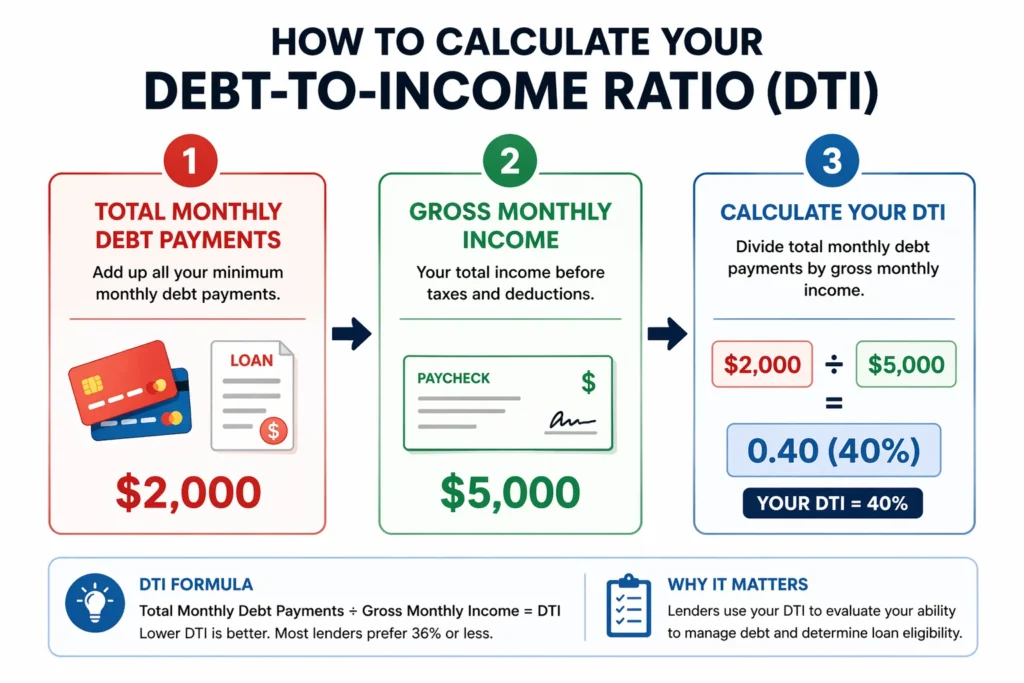

Your debt-to-income ratio (DTI) shows what percentage of your gross monthly income goes toward debt payments. Lenders examine this number when deciding whether to approve you for a loan or increase your credit limit. Unlike disposable income which shows what’s left after essentials—your DTI reveals how much of your earnings existing debt obligations already claim.

Here’s how to calculate it:

Step 1: Add up all your monthly debt payments credit card payments, car loans, student loans, mortgage or rent, and any other monthly obligations. Let’s say your total is $2,000 per month.

Step 2: Divide that number by your gross monthly income (before taxes). If you make $5,000 per month, then $2,000 ÷ $5,000 = 0.40, or 40%.

Step 3: That’s your DTI ratio. In this example, you’re at 40%.

Financial experts and mortgage lenders use these thresholds: anything under 36% is manageable, 36% to 43% means you’re stretching your budget dangerously thin, and above 43% signals serious trouble—debt payments are consuming nearly half your income before you even buy groceries.

These aren’t arbitrary numbers. The Consumer Financial Protection Bureau and most mortgage underwriters use the 43% threshold as a maximum debt-to-income ratio for qualified mortgages.

Greg’s situation illustrates this perfectly. He and his wife brought in $11,500 combined monthly income she made $7,500 and he made $4,000 after losing a better-paying job. But they carried over $300,000 in total debt between credit card balances, loans, and their mortgage.

When I calculated their monthly debt payments, they consumed well over 50% of their income. The numbers revealed an unsustainable situation. Greg was in genuine crisis mode, not because he was irresponsible, but because his debt burden mathematically couldn’t work with his current income.

Your DTI tells you whether you can actually afford your debt or if you’re just pretending you can while slowly drowning.

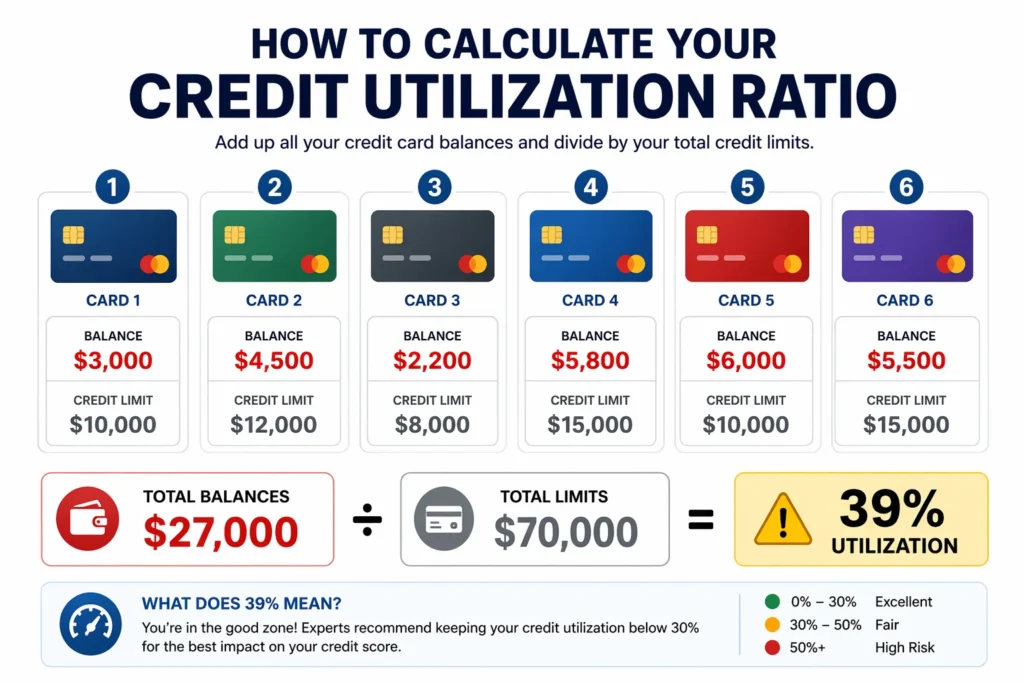

Metric #2: Your Credit Utilization Ratio : The 30% Safe Zone

Credit utilization is simpler but just as important for your financial health and credit score impact. It measures the percentage of your available credit that you’re actually using across all your credit cards.

Here’s how to calculate it:

Step 1: Add up all your credit card balances. If you have six cards carrying balances of $3,000, $4,500, $2,200, $5,800, $6,000, and $5,500, your total is $27,000.

Step 2: Add up all your credit limits across all cards. If your limits are $10,000, $12,000, $8,000, $15,000, $10,000, and $15,000, your total available credit is $70,000.

Step 3: Divide your total balances by your total limits. $27,000 ÷ $70,000 = 0.386, or about 39%.

If you’re at 39% utilization, you’re over the safe zone. Credit bureaus start penalizing your credit score once you hit 30% utilization a threshold built into most credit scoring models.

High credit utilization signals to lenders that you’re desperate for credit, can’t control your spending, and represent a risky borrower. This isn’t opinion it’s how the FICO algorithm mathematically weighs your credit risk.

Katie experienced this impact directly. She maxed out multiple cards, hitting 100% credit utilization the absolute worst position for your credit report. The credit bureaus immediately flagged her as someone who couldn’t manage credit card spending responsibly, and her FICO score dropped over 80 points in three months.

Credit utilization affects your credit score immediately that’s what makes it so dangerous. Unlike some financial metrics where consequences take months to appear, high utilization damages your creditworthiness the moment your credit card companies report your balances to the credit bureaus.

Quick Calculation Worksheet (Personalize Your Numbers)

Seriously, do this calculation right now don’t skip it. You’ll move from anxious guessing to actual clarity in about two minutes.

Your DTI Calculation:

Total monthly debt payments: $__________

Gross monthly income: $__________

DTI ratio (divide the first by the second): __________ %

If your DTI is under 36%, you’re in the safe zone. Between 36% and 43%, you need to act soon. Above 43%, you’re in crisis mode.

Your Credit Utilization Calculation:

Your Credit Utilization Calculation:

Total credit card balances: $__________

Total credit limits: $__________

Utilization ratio (divide the first by the second): __________ %

If you’re under 30%, you’re good. Between 30% and 50%, it’s impacting your FICO score. Above 50%, it’s severely damaging your score.

Write these numbers down and tape them somewhere visible your bathroom mirror, your computer monitor, your wallet. These percentages show your exact financial situation right now, not some vague sense of “being in debt.”

How Much Credit Card Debt Is Too Much? 7 Red Flags You’re in Trouble

Numbers tell one story, but your daily life tells another. Sometimes the real warning signs of excessive debt aren’t in spreadsheets they’re in how you feel at 3 AM and what you’re doing just to survive month to month.

I’m walking through seven red flags that signal you’ve crossed from “manageable debt” to “too much credit card debt.” Some come from calculations. Others come from behaviour. All of them matter.

Red Flag #1: You Can Only Make Minimum Payments

This is the most dangerous trap. When I say you can “only” make minimum payments, I don’t mean that’s the smallest amount on your statement. I mean that after paying minimums on everything, you have zero extra money to throw at debt.

The minimum payment trap works like this: minimum payments are designed to keep you in debt as long as possible through compound interest. At 18% interest on a $10,000 balance, a $200 minimum payment breaks down to roughly $150 in interest charges and only $50 toward your actual balance.

After five years of these payments, you’ve paid $12,000 total but still owe nearly $9,000. That’s the math working against you.

If you can’t afford to pay more than the minimum on any of your credit card bills, take this seriously. You’re not breaking even. You’re losing ground every single month.

Red Flag #2: You’re Using Credit Cards for Essential Expenses

Debt crosses from “I overspent” to “I can’t afford to live” the second you start charging rent, groceries, utilities, or medication because you don’t have enough cash. You’ve entered crisis territory.

Essentials aren’t optional—that’s what makes this different. You can skip restaurants or movies. You can’t skip rent or food. When you borrow just to survive, your monthly income isn’t covering basic needs anymore.

No budgeting tricks or payment strategies fix this problem. You need either more income or drastically lower expenses. You should also seriously consider contacting a credit counselor at this stage.

Red Flag #3: Your Credit Score Is Declining

Your FICO score is a real-time report card on your financial health. If it’s dropping, your debt is the most likely culprit. High credit utilization damages your score immediately. Missed or late payments damage it even more. Collections damage it worst of all.

If your FICO score has trended down over the past few months, your debt situation is getting worse, not better. Unfortunately, this red flag appears after the damage is already done by the time you notice the drop, the problem has been building for months.

Check your FICO score for free at MyFICO

This will show you your exact current score and how your credit utilization is impacting it right now.

Monitor your credit report regularly through Experian, Equifax, and TransUnion The three major credit bureaus Equifax, Experian, and TransUnion report. Most credit card companies and financial apps now show your score for free monthly.

Red Flag #4: You’re Juggling Payments or Paying Late

Juggling payments means paying one card with another, or paying credit card bills in a specific order because you can’t cover them all on time. Paying late means missing due dates regularly or barely making them.

Your monthly income doesn’t stretch far enough, forcing you to choose which bill to pay this week and which to push to next week. It’s stressful and completely unsustainable.

Late payments appear on your credit report immediately. After 30 days late, your FICO score starts dropping. After 90 days, creditors mark your account as delinquent or in default. At that point, you face collections calls, additional fees, and potential legal action.

Red Flag #5: You Have No Money Left at Month’s End

Katie’s situation illustrates this perfectly. She made $83,000 annually more than most Americans but after rent, utilities, childcare, her son’s private school, and minimum payments on her credit card debt, she had $10 left.

Ten dollars can’t cover an unexpected car repair, medical bill, or any real emergency. No emergency fund. No buffer. No safety net. One surprise expense would push her deeper into high credit card debt.

If you have very little or nothing left at the end of your paycheck, you’re living one emergency away from crisis. Building even a basic $1,000 emergency fund becomes impossible when debt payments consume nearly all your disposable income. The first step toward recovery is learning to reduce your monthly expenses so you can redirect funds toward both debt payoff and emergency savings.

Red Flag #6: You’re Stressed, Anxious, or Losing Sleep

This warning sign gets overlooked because it’s emotional rather than financial—but it matters enormously.

Constant worry about money, anxiety when you see notifications from credit card companies, sleepless nights replaying your debt situation these symptoms mean financial stress is destroying your quality of life. It’s neither normal nor sustainable.

Financial stress causes real health problems, damages relationships, and triggers depression. When the emotional toll reaches this level, you need to address the psychological impact alongside the numbers. Your mental health matters as much as your credit utilization ratio.

Red Flag #7: You’ve Maxed Out Multiple Cards

Maxed out means hitting your credit limit. If five cards exist in your wallet and three are maxed, you’ve completely lost control of credit card spending. You’re using credit cards as income replacement, not convenience tools.

Katie had six cards at 100% credit utilization—zero available credit remaining. She had nowhere to turn for emergency money. If her car broke down or her son got sick, she couldn’t even borrow because she’d already maxed out everything.

When you’ve maxed out multiple cards, you’re not just carrying high credit card debt. You’re completely out of options, and your credit score is tanking simultaneously.

What Actually Happens When You Have Too Much Credit Card Debt: Real Consequences (Not Theories)

Understanding you have too much credit card debt is step one. Understanding the real consequences if you don’t fix it that’s step two. And step two motivates action faster than anything else.

I’m not going to scare you with worst-case scenarios. I’m walking you through what actually happens, month by month, because reality provides enough motivation.

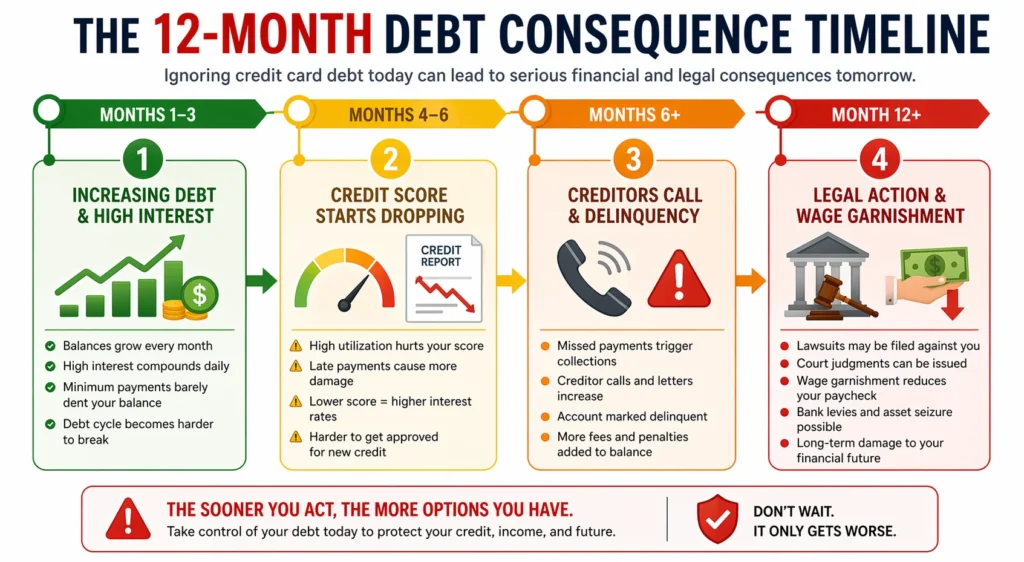

Month 1-3: Increasing Debt and High Interest

People often don’t realize how serious things are getting during this phase. Your credit card balance isn’t growing because you’re reckless it’s growing because of how credit card interest rates compound.

Take a $10,000 balance at 18% APR (standard for the credit card industry). Your monthly interest charge hits approximately $150. If your minimum payment is $200, only $50 actually reduces your outstanding balance the rest covers interest charges.

In months 1-3, life keeps happening. You use the cards for more expenses. The balance climbs instead of falling. You might pay $500 monthly in minimums across all cards, but your total debt grows faster than you can pay it down.

Compound interest works against you silently. You don’t see it as a separate line item on most statements it’s baked into your balance. But it’s accumulating constantly, making your debt burden harder to escape.

Month 4-6: Credit Score Starts Dropping

After four months of carrying high credit card balances, your credit utilization ratio locks in, and your FICO score starts dropping across all three credit bureaus—Experian, Equifax, and TransUnion. You might see a 30 to 100-point drop depending on your starting score.

If you were in the 700s, you might hit the 650s now. If you were at 650, you’re now in the 550s. Your credit score determines what interest rates you qualify for, meaning a lower score costs you more on everything. Need to refinance or get a loan? You’re paying a higher rate now because your FICO score tanked.

Many people don’t notice the drop because they don’t monitor their credit report. But Experian, Equifax, and TransUnion are watching and reporting constantly. Your score declines silently while you scramble to make next month’s credit card payments.

Month 6+: Creditors Call and Accounts Become Delinquent

After about six months of barely making minimum payments, something breaks. You miss a payment—not intentionally, but it happens. Or you pay late.

Once you’re 30 days late, the credit card company reports it to Experian, Equifax, and TransUnion. Your credit report now shows a late payment, and your FICO score drops again.

You’ll start getting calls from creditors at this point. These aren’t legal proceedings yet—they’re collection calls from your credit card companies themselves, not third-party collectors. They’re uncomfortable and sometimes aggressive.

Your account status changes to “delinquent,” a designation that appears on your credit report and signals serious financial trouble to any future lender.

Month 12+: Legal Action and Potential Wage Garnishment

After 12 months of non-payment, creditors gain legal options they didn’t have before. They can file a lawsuit against you. If they win (which they usually do), they get a judgment allowing them to pursue wage garnishment—your employer directly withholds money from your paycheck to pay the debt.

Wage garnishment is real, not theoretical. Money gets taken from your paycheck before you ever see it.

Some states allow creditors to garnish up to 25% of your disposable income. If you make $3,000 monthly and need $750 for survival, creditors can seize $562.50 per month directly from your pay.

You might also face bank account levies at this stage—creditors freeze your bank account and withdraw money directly from your savings. Some people file bankruptcy to stop wage garnishment, but that creates its own seven-year credit nightmare.

The 7-Year Myth (And Why It’s Wrong)

The “7-year myth” misleads thousands of people every year. It claims that debt disappears from your credit report after seven years, meaning creditors can’t touch you after that point.

Half true, completely dangerous.

Yes, debt falls off your credit report after seven years—that part is accurate. But your legal obligation to pay doesn’t disappear. Creditors can still sue you, obtain judgments, and garnish your wages. The statute of limitations varies by state—in many states, creditors have 10, 15, or even 20 years to pursue legal action.

I’ve worked with clients who waited for the “magic” seven-year mark, thinking they’d be free. Then a creditor sued them in year eight. The shock was devastating and completely avoidable.

The legal obligation to pay outlasts the credit report entry by years, sometimes decades. Don’t wait—act now to manage credit card debt properly.

“Normal” vs. “Too Much Credit Card Debt”: What’s Average in America?

One of the most common questions I hear: “Am I normal? Do other people have this much debt?” The answer is complicated because “normal” doesn’t mean “healthy.

Average American Credit Card Debt: $6,200–$7,000

According to recent data from the Federal Reserve and credit bureaus, Americans carry between $6,200 and $7,000 in average credit card debt. Fifty-six million Americans are carrying credit card balances right now an enormous number.

That average includes people with zero debt and people drowning in $50,000 of debt. It includes people who pay off their cards monthly and people who will never escape their revolving debt. The $6,200 average shows what the math works out to, not whether that level is normal or healthy for your specific situation.

The Real Story: What Matters More Than “Normal”

Here’s what I actually want you to understand: you shouldn’t care about normal. You should care about your situation.

Katie makes $83,000 per year with $27,000 in debt. That’s 32.5% of her annual income. That’s high, but not catastrophic.

Greg had $300,000 in debt on a combined household income of about $138,000. That’s 217% of their annual income. That’s a completely different level of crisis.

The same person with $10,000 in debt could be in great shape if they make $100,000 per year. But if they make $40,000 per year, $10,000 is dangerous.

Normal doesn’t matter. Your personal situation matters.

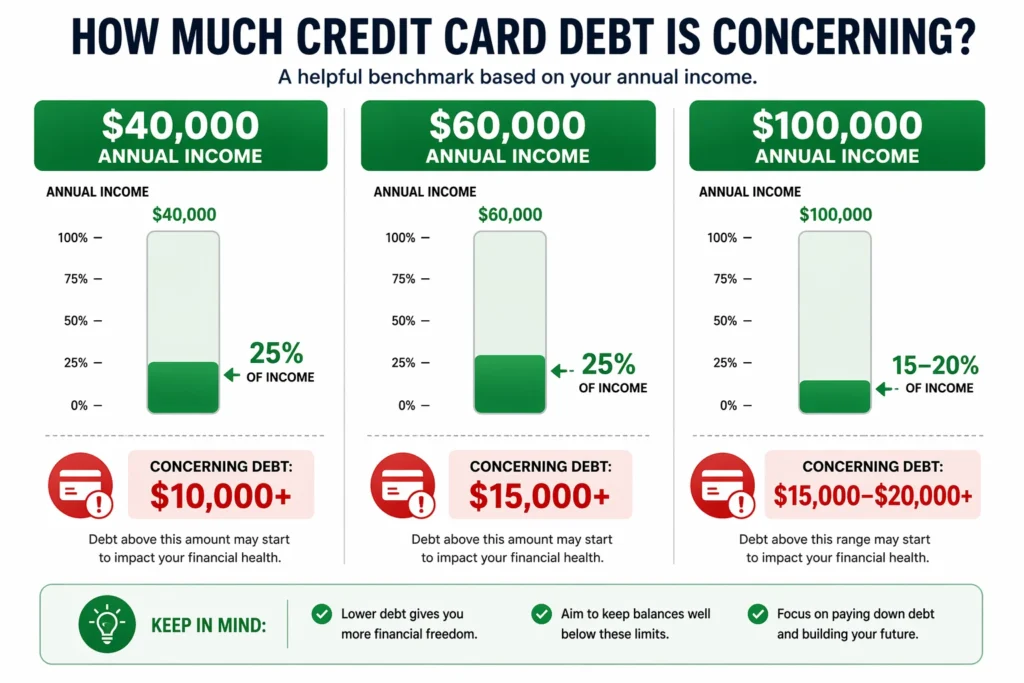

Credit Card Debt by Income Level: The Real Benchmark

Let me give you a better way to evaluate your situation using the 30% rule. Here’s what I consider concerning at different income levels:

$40,000 annual income: Anything over $10,000 in credit card debt is concerning (25% of income)

$60,000 annual income: Anything over $15,000 is concerning (25% of income)

$100,000 annual income: Anything over $15,000–$20,000 is concerning (15%–20% of income)

These aren’t hard rules they’re guidelines showing when debt outpaces your ability to manage it reasonably. However, these guidelines apply to credit card debt specifically. If you also have student loans, a car payment, and a mortgage, your total debt-to-income ratio becomes much more important than these numbers alone.

Why Comparing to Others Is a Trap (And What to Compare Instead)

I want to be blunt about this: comparing your situation to others is almost always a bad idea.

Yes, 56 million Americans have credit card debt. Yes, many of them have more than you do. But that doesn’t mean you’re okay. That doesn’t mean normal is healthy.

Normal in America right now is being broke and scared. Normal is living paycheck to paycheck. Normal is one emergency away from a crisis. That’s not a standard you should be shooting for.

Instead, compare your situation to your goals. Compare your debt to your income. Compare your interest payments to what you could be saving. Compare where you are now to where you want to be.

That comparison matters. That comparison motivates actual change.

The Behavior Problem: Why You Got Into Debt (And Why Metrics Alone Won’t Fix It)

This is where most financial advice falls short. People give you the numbers, tell you to cut your spending, and send you on your way. Then you don’t change anything because they haven’t addressed why you got into debt in the first place.

I learned something from watching how people actually fix their debt: 80% of the problem is behavior and 20% is knowledge. You probably know you should spend less. But knowing that isn’t making you spend less.

The 80/20 Truth: You Can’t Math Your Way Out of a Behavior Problem

Let me explain what I mean with an example. You can sit down, calculate your DTI ratio perfectly, understand your credit utilization, and still not change your behavior.

Why? Because understanding the metrics doesn’t change why you spend money the way you do.

Katie understood her debt was bad. She knew her credit cards were maxed out. She still kept using them. Not because she was stupid or reckless, but because her behavior—the way she related to money and spending—hadn’t changed.

You can hand someone a perfect budget and they’ll blow through it in two weeks. You can show someone their interest payments and they’ll still go out to eat instead of packing lunch. You can tell someone their debt is dangerous and they’ll nod and do nothing.

That’s not a knowledge problem. That’s a behavior problem. And you can’t solve a behavior problem with more information.

This is actually good news because it means the solution isn’t complicated. It means you need to change your habits, not learn harder.

Common Root Causes of “Too Much” Debt

Understanding how you got here isn’t about blame. It’s about breaking the pattern so you don’t get here again.

Katie’s debt started with a job transition. She went through a period where she didn’t have enough income, so she used credit cards to bridge the gap. That’s reasonable. That’s what credit cards are supposed to be for.

But then she kept using them even after she had income again. The behavior that started as survival spending became lifestyle spending. She kept charging things because she could, because the limit was there, because she wasn’t tracking where the money went.

Greg’s situation was different. He had a good job making $85,000 per year. But he bought a $42,000 truck to drive for Uber. That’s lifestyle inflation—spending at a level that looks good but doesn’t match your actual circumstances. When he lost his better job, that truck payment became an anchor dragging him down.

Many people go into debt because of unexpected expenses. Job loss, medical bills, car repairs. That’s real. But many people also go into debt because they never learned to say no to themselves. Because they use credit cards as permission to spend money they don’t have. Because the credit building myth taught them that being in debt was normal.

That credit building myth is particularly insidious. People convince themselves they need to carry a balance on credit cards to build their credit. They think rich people do this. They’ve heard that you “need to build credit” and somehow that translated to “need debt.”

It’s completely backwards. But once that belief is lodged in your brain, it justifies ongoing debt. You’re not being irresponsible. You’re building credit responsibly.

The Mindset Shift Required to Fix Debt

This is the hard part. Changing your behavior requires changing how you think about money itself.

Right now, your brain has likely accepted a story about money. Maybe it’s “I deserve nice things and should buy them now because I might not be able to later.” Maybe it’s “Everyone has debt, so it’s normal.” Maybe it’s “I’ll figure it out next year.”

None of those stories are true. But believing them feels comfortable because they justify your current behavior.

Breaking free requires a genuine shift: from “this is just how things are” to “this has to change and I’m going to make it change.

I watched Katie have that breakthrough moment. A financial expert told her directly: “Personal finance is 80% behavior and 20% knowledge. The behaviors that got you into this will keep you here if you don’t change them.”

It hit hard because it was true. All the knowledge in the world wouldn’t help if her behavior stayed the same. Knowing her DTI ratio didn’t matter if she kept spending like she had unlimited income.

Then came the perspective shift: “Use that fear as a driving force. Tell yourself: ‘I will never be here again. I will sacrifice anything to keep me and my child off the edge of financial terror.'”

That’s when real change becomes possible—when you decide being in debt is unacceptable, when you’re willing to make temporary sacrifices for permanent freedom.

That’s the mindset shift: from “I have to pay down my debt” to “I will not live like this anymore.”

4 Proven Methods to Reduce Credit Card Debt

Okay, you know you have too much debt. You understand the consequences. You’re ready to change your behavior. Now what?

I’m going to walk you through four methods people actually use to break free from credit card debt. One of them will fit your situation better than the others. The key is picking the right one and committing to it.

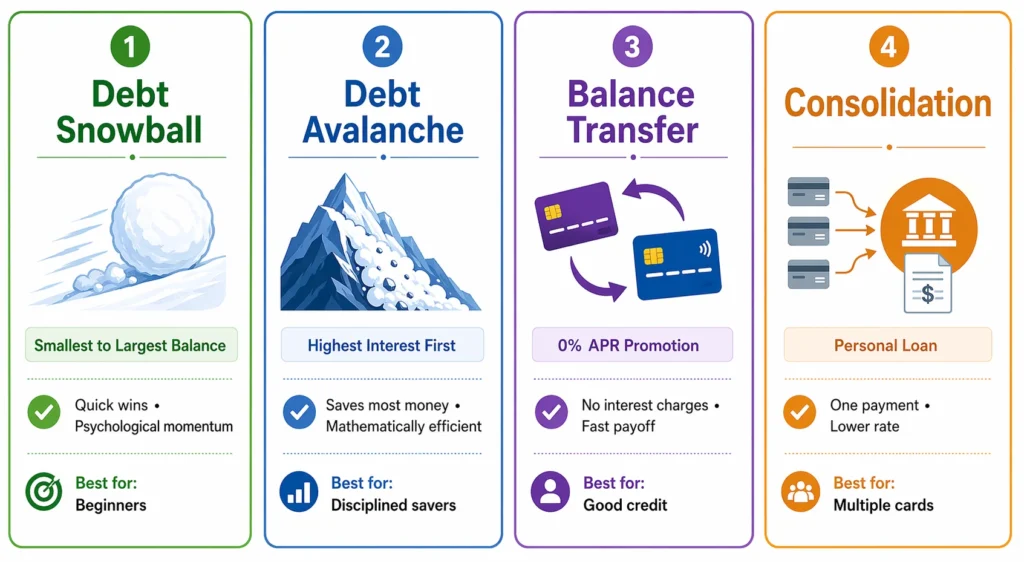

Method #1: The Debt Snowball (Smallest to Largest)

The debt snowball is simple: pay minimums on all your cards, then throw every extra dollar at the smallest balance.

Let’s say you have six cards:

Card 1: $2,500 balance

Card 2: $4,200 balance

Card 3: $6,800 balance

Card 4: $8,500 balance

Card 5: $3,900 balance

Card 6: $5,100 balance

You’d focus on Card 1 first. Pay your minimums on cards 2-6, but any extra money goes toward Card 1. Once Card 1 is paid off, you move to Card 5, then Card 2, then Card 6, and so on.

The advantage of this method is psychological. You get a win fast. That $2,500 card might be paid off in a few months if you throw extra money at it. Then you feel momentum. You’ve paid off a card. You can pay off the next one. That momentum keeps you going when the process gets hard.

The disadvantage is that you might pay more interest overall because you’re not prioritizing the highest-rate cards first.

This is the method I’d recommend if you’re new to debt payoff and you need to feel like you’re winning. You need that psychological momentum.

Method #2: The Debt Avalanche (Highest Interest First)

The debt avalanche is mathematically superior. You pay minimums on everything, then throw extra money at whichever card has the highest interest rate.

Using the same cards, if Card 1 has a 24% APR and Card 3 has an 18% APR, you’d attack Card 1 first even though the balance is smaller.

This method saves you the most money because you’re getting rid of the most expensive debt first. Interest charges accumulate slower. Your payoff timeline might be shorter overall.

The disadvantage is that you don’t get that quick win. If the highest-rate card has a big balance, it might take longer to pay off, which can feel discouraging.

I’d recommend this method if you’re disciplined, if you understand compound interest, and if you don’t need quick psychological wins to stay motivated.

Method #3: Balance Transfer (0% Offer Cards)

A balance transfer is when you move credit card debt from one card to another card that offers 0% APR for a promotional period, usually 6 to 12 months.

The advantage is obvious: no interest for that period means every dollar of your payment goes toward actually reducing the balance. You can make real progress if you have the discipline to pay aggressively during that window.

The disadvantage is that you need decent credit to qualify (usually 670 FICO or higher), and there’s often a transfer fee of 2% to 5% of the balance you’re moving. You’re also opening a new credit account, which slightly damages your credit score temporarily.

This method only works if you can pay off the entire balance before the promotional period ends. If you don’t, the interest rate shoots up to the regular rate (usually 18-25%) and you’re back where you started, but with an additional account.

I’d only recommend this if you have a realistic plan to pay the balance off within the promotional window. Otherwise, it’s just delaying the problem.

Method #4: Debt Consolidation (Personal Loan)

Debt consolidation means taking out a personal loan to pay off all your credit cards at once. You then have one payment instead of six.

The advantage is simplicity. One payment instead of multiple. Usually a lower interest rate (6-12% instead of 18-25%). It’s psychologically easier to manage one debt than six.

The disadvantage is that you’re often extending the timeline, which means more interest paid overall. You’re also borrowing money while you’re already in debt, which doesn’t address the underlying behavior problem. If your spending behavior doesn’t change, you could pay off the personal loan and run up the credit cards again.

I’d recommend consolidation only if the lower interest rate creates meaningful savings and if you’re committed to changing your spending behavior simultaneously. Otherwise, you’re just rearranging the furniture in a sinking ship.

Which Method Should YOU Use?

Here’s how to think about it:

If you want to feel like you’re making progress quickly and you respond well to momentum, use the snowball method. You’ll pay a bit more interest, but you’ll stay motivated.

If you’re confident in your discipline and you want to save the most money on interest, use the avalanche method. The math is better.

If you have decent credit and you can commit to aggressive payments over 6-12 months, and if your balances are high enough to make a 2-5% transfer fee worth it, consider balance transfer.

If you have many cards with very high interest rates and you want the simplicity of one payment, and if you’re genuinely committing to behavior change, consolidation might make sense.

But pick one. Don’t try all four. Pick the one that matches your situation and your personality, and commit to it completely.

The Action Plan: What to Do This Week (Not Someday)

You’re reading this article and probably feeling some combination of anxiety, clarity, and motivation. Don’t let that motivation fade into “I’ll start next week.”

This week, you’re going to take real action. Not big action necessarily. Just real action. Here’s your timeline:

Today: Cut Up Your Credit Cards

I mean this literally. Take your credit cards and cut them up. All of them. No exceptions.

This isn’t about being dramatic. It’s about removing the temptation immediately. You can’t use a card that’s been cut into pieces. The act of cutting them up is also psychological. You’re making a commitment. You’re saying “I’m done using credit to spend money I don’t have.”

If you have autopay set up on any of those cards, that’s fine. You’ll keep paying them. But they’re not going to be tempting you anymore.

Tomorrow: Calculate Your Numbers

Use the worksheet I provided earlier. Calculate your DTI ratio and your credit utilization ratio. Write the numbers down. Put them somewhere you see them every day.

These numbers are real. They’re not abstract concepts. They’re the current state of your finances.

Wednesday: List Your Debts Smallest to Largest

Get a piece of paper or open a spreadsheet. Write down every credit card debt, every personal loan, every debt you have. Write down the balance and the interest rate for each one.

Then sort them smallest to largest.

This is the moment you pick your payoff method. Are you doing snowball or avalanche? Look at your list and decide.

Thursday: Download a Budgeting App

Go to your phone’s app store and search for “budget app.” Download one that connects to your bank account. EveryDollar is popular. YNAB (You Need A Budget) is powerful. Rocket Money tracks expenses well.

Set it up and connect it to your bank account. Let it track your spending automatically. Don’t try to be perfect initially. Just let it show you what you’re actually spending money on.

Friday: Tell Your Budget Where Every Dollar Goes

This is the most important step. Open your budgeting app and create a budget for next month.

Don’t do this reactively by tracking where money went. Do this proactively by deciding where every dollar will go before the month starts.

Example budget:

- Food: $400

- Gas: $150

- Utilities: $120

- Debt payment: $500

- Entertainment: $50

When you allocate every dollar before the month begins, you’re not hoping money will be left over—you’re ensuring it.

This Week: Find Your First $500 to Attack Debt

Where can you cut? Where is money being wasted? These are the exact kinds of detailed strategies for cutting expenses that can free up $500 monthly:

No eating out: Save $200–$300/month

Cancel unused subscriptions: Save $30–$50/month

Reduce streaming services: Save $10–$20/month

Make coffee at home: Save $50–$100/month

Buy generic groceries: Save $50–$80/month

Find $500 per month to throw at debt. It’s a temporary sacrifice for permanent freedom.

Five hundred dollars monthly toward your smallest card means it’s paid off in 4–5 months. Then you move that $500 to the next card. And the next.

You’re not deprived forever. You’ll be free in 18–24 months instead of trapped for five years.

That’s worth the temporary sacrifice.

This Week: Identify Your First $500 to Throw at Debt

Where can you cut? Where is money being wasted?

No eating out. That might save $200-300 per month.

Cancel subscription services you don’t actually use. That might save $30-50.

Reduce your streaming services. That’s $10-20.

Stop buying coffee and make it at home. That’s $50-100 per month.

Buy generic groceries instead of name brands. That’s $50-80 per month.

These aren’t permanent. These are temporary sacrifices so you can throw an extra $500 per month at your debt and actually see progress.

Five hundred dollars per month toward your smallest credit card might mean that card is gone in 4-5 months. Then you take that $500 and throw it at the next card. Then the next. Then the next.

You’re not going to feel deprived forever. You’re going to feel free in 18-24 months instead of trapped for the next five years.

That’s worth the temporary sacrifice.

When to Seek Professional Help: Credit Counselling and Debt Options

I want to be clear about something: trying to fix your debt alone is smart. But asking for help when you need it is smarter.

Not everyone can DIY their way out of debt. Sometimes the situation is too complicated, or you need guidance from someone who understands your options.

When to Call a Credit Counselor (Signs You Need Help)

You should consider professional help if:

You’re being sued or threatened with legal action. At that point, you need someone who understands the legal side of debt, not just the financial side.

You’ve missed multiple payments and you’re not sure what to do. A counselor can help you understand your options and potentially negotiate with creditors.

You’re considering bankruptcy. Before you make that decision, talk to someone who can explain all your options.

You just can’t figure it out alone. You’ve tried budgeting and it’s not working. You’re too overwhelmed to organize your debts. You need someone to help you make a plan.

You’re in a situation where the numbers are too big. You have $100,000 in debt and you make $40,000 a year. The math doesn’t work without serious intervention.

A legitimate credit counselor won’t make you feel ashamed. They work with people in your exact situation constantly. They’ve seen worse. They can help.

Credit Counseling vs. Debt Settlement vs. Bankruptcy: What’s the Difference?

These are three different paths, and they have very different consequences.

Credit counseling is when a nonprofit counselor helps you understand your options, create a budget, and potentially negotiate with your creditors directly. This doesn’t damage your credit as much as the other options. The counselor acts as an intermediary between you and your creditors, often negotiating lower interest rates or adjusted payment plans.

Debt settlement is when a company helps you negotiate with creditors to pay less than you owe. For example, you might settle a $10,000 debt for $6,000. The advantage is that you owe less money. The disadvantage is that it damages your credit significantly. Settlement stays on your credit report for seven years.

Bankruptcy is a legal process where a court decides how much of your debt you actually have to pay. It’s the nuclear option. It eliminates most of your debt, but it destroys your credit for seven to ten years. It’s also expensive (lawyer fees, court fees) and complicated.

If you’re at the point where you’re considering settlement or bankruptcy, you need a professional. These aren’t decisions to make alone.

Resources: Finding a Legitimate Credit Counsellor

The National Foundation for Credit Counseling (NFCC) accredits legitimate non profit credit counsellors. Visit their website to find a counsellor in your area. NFCC counsellors are non profit, so their incentive is your success, not their profit.

Be cautious of for-profit debt relief companies. Since they make money from your situation, their incentive may not align with your best interests.

A legitimate credit counselor charges little to nothing for an initial consultation and explains all your options honestly—even when the best option doesn’t generate revenue for them.

Final Thought: Too Much Debt Doesn’t Mean You’re Broken

You’re reading this because you’re anxious about debt. That worry is valid. But I want you to understand something important: you’re not broken. You’re not uniquely bad at money. You’re not fundamentally flawed.

You’re human. Fifty-six million other Americans are in the exact same situation. Many of them feel exactly what you’re feeling right now.

The good news is that debt is fixable. It’s not quick. It’s not painless. But it’s fixable.

You now know the metrics that tell you if you’re in trouble. You know the red flags that indicate how serious your situation is. You know what happens if you don’t act. You know your options for getting out.

More importantly, you know that this is solvable. People solve it every single day. Some of them pay off their debt in 18 months. Some take several years. But they move from “I’m drowning” to “I’m breathing” to “I’m free.”

You can do this. Not because you’re special. But because it’s possible.

The hard part isn’t understanding what to do. You understand now. The hard part is actually doing it. Actually cutting up the cards. Actually refusing to use credit as a safety net. Actually making temporary sacrifices for a permanent solution.

But that hard part is also within your control. You have more power over this situation than you probably think you do.

This week, take the action steps I outlined. Calculate your numbers. Cut up your cards. List your debts. Download your app. Tell your budget where every dollar goes.

These aren’t dramatic, but they’re real and they’re the beginning of your escape.

You’ve got this. Now go do it.

FAQ: Your Questions About Credit Card Debt Answered

If I have $20,000 in credit card debt and make $60,000 per year, do I have too much?

Yes. That’s 33% of your annual income, which exceeds the 30% benchmark. If you have other debts on top of that, your DTI ratio is probably already over 36%. This is the danger zone. You need to calculate your DTI specifically, but yes, you’re carrying too much debt and you need to take action soon. The good news is that $20,000 is manageable for someone making $60,000. With aggressive payments, you could be free in 2-3 years.

Does credit card debt really disappear after 7 years?

This is the myth that misleads so many people. Here’s the truth: debt falls off your credit report after seven years. That part is accurate. But the legal obligation to pay remains. Creditors can sue you at any time, even years after the seven-year mark. The statute of limitations varies by state, but in many places, creditors have 10, 15, or even 20 years to pursue legal action. Don’t count on the seven-year mark. Work to pay or settle your debt instead.

What’s the fastest way to pay off credit card debt?

The fastest way is usually the debt avalanche (highest interest first) combined with aggressive expense cutting. Cut everything that’s not essential. Find every dollar you can and throw it at your highest-interest debt. Some people pay off significant debt in 18-24 months by dedicating 50% or more of their income to debt payoff. But “fastest” also requires discipline and the ability to live very frugally temporarily.

If I only make minimum payments, how long will it take to pay off my debt?

Much longer and much more expensive than you think. A $10,000 balance at 18% APR with a $200 minimum payment takes over five years to pay off. And you’ll pay over $3,000 in interest alone. The equation is simple: lower payment equals longer timeline equals more interest. Use an online calculator to see the real timeline for your specific balance and interest rate. It’s usually shocking enough to motivate a change.

Can I get a personal loan to pay off my credit card debt?

Maybe. If you have decent credit (650 FICO or higher), you can probably qualify for a consolidation loan at 6-12% APR instead of 18-25% for credit cards. The advantages are one payment instead of many, and a lower interest rate. The disadvantages are that you’re extending the timeline (longer payoff period) and you’re not addressing the spending behaviour that got you into debt. Consolidation only makes sense if the lower rate saves significant money and if you’re committed to behaviour change.

I’m stressed and embarrassed about my debt : is this normal?

Absolutely normal. Fifty-six million Americans are carrying credit card debt. You’re not alone. You’re not broken. You’re human. And the fact that you’re researching this and feeling concerned means you’re ready to change. That’s actually a good sign. If you’re struggling emotionally with this, consider reaching out to a credit counselor. Many organizations like the NFCC provide support that isn’t just financial advice, but emotional support too.

Should I use a balance transfer card to avoid paying interest?

Only if three conditions are true: (1) you have good credit to qualify, (2) you can pay off the entire balance before the promotional period ends (usually 6-12 months), and (3) you can avoid using the card again. Balance transfers aren’t a solution. They’re a tactic that works only if you commit to aggressive payoff during the interest-free window. Otherwise, you’re just delaying the problem.

What’s the difference between a credit counsellor and a debt settlement company?

Big difference. Credit counselors (like NFCC) are nonprofit and help you create budgets, negotiate with creditors directly, and find sustainable solutions. Debt settlement companies are for-profit and negotiate to pay less than you owe (which damages your credit significantly). Use a counselor first. Only consider settlement if you’re considering bankruptcy, because settlement is a last resort that comes with serious credit consequences.