Budgeting in Small Business: 7 Steps to Financial Control

If you run a small business and feel like money just disappears no matter how much you earn, you are not alone. I have seen this pattern repeat itself more times than I can count. A business owner works incredibly hard, brings in decent revenue, and still ends up stressed about making payroll or covering next month’s rent.

The problem is almost never the amount of money coming in. The problem is the absence of a plan for where it goes.

Budgeting in small business is not about restriction. It is about direction. When you give every dollar a job, your business stops running on hope and starts running on a system. This guide walks you through exactly how to build that financial management system, step by step, including the parts most articles never mention.

What a Small Business Budget Actually Is (And What It Is Not)

A budget is a forward-looking document. It is your best prediction of what you plan to earn and spend over a coming period, usually a month, a quarter, or a full year. You write it before the money moves. This is the foundation of your budget planning process, and creating your business budget systematically ensures you capture all necessary elements from the start. Your budget works alongside your business plan to translate strategic goals into specific financial targets.

A budget is not your bookkeeping. It is not your profit and loss statement. All three of these things sound similar, but they serve completely different purposes in your business finances, and mixing them up will cost you clarity when you need it most.

A budget is a forward-looking document. It is your best prediction of what you plan to earn and spend over a coming period, usually a month, a quarter, or a full year. You write it before the money moves. This is the foundation of your budget planning process, and creating your business budget systematically ensures you capture all necessary elements from the start.

Your profit and loss statement, on the other hand, looks backward. It shows exactly what happened after the money moved. A simple way to remember this: a budget is a guess, but your profit and loss statement is the truth. You need both documents working together, and comparing them monthly transforms your financial clarity.

Bookkeeping sits between the two. It is the act of recording every transaction as it happens. Think of bookkeeping as building the raw data that your P&L draws from. Without clean bookkeeping, your P&L means nothing, and your budget has nothing real to build on.

Understanding this distinction matters enormously for your business finances. Once you know that your budget is a planning document rather than an accounting record, the whole process becomes far less intimidating.

The Difference Between a Budget, a P&L, and Bookkeeping

Here is a simple way to think about all three:

Your budget is the plan. Your bookkeeping is the record. Your P&L is the verdict.

A bookkeeper records the data. An accountant interprets it. You need both to know whether your budget is actually working. If you are doing everything yourself at this stage, know that your budget tells you what you intended to happen, and your P&L tells you what actually did happen. The gap between those two documents is where the most valuable business lessons live.

Accounting software can help you manage all three in one place—your balance sheet, income statement, and budget—once your business grows to that point. For now, understanding how each document functions is the foundation of solid business budgeting.

The Four Core Components Every Budget Must Have

Every small business budget, regardless of industry or size, needs these four building blocks that form the operational budget foundation:

Revenue estimates. Your projected income from all sources for the period ahead.

Fixed costs. Expenses that stay the same every month no matter what your sales look like.

Variable costs. Expenses that rise and fall depending on your activity level or sales volume.

One-time expenses. Planned or anticipated costs that do not repeat regularly, like equipment purchases or a website overhaul.

Together, they form the operational budget that runs your business. Everything else fits inside them. I will walk through each of these in detail later in this guide. For now, these four categories form the skeleton of your budget.

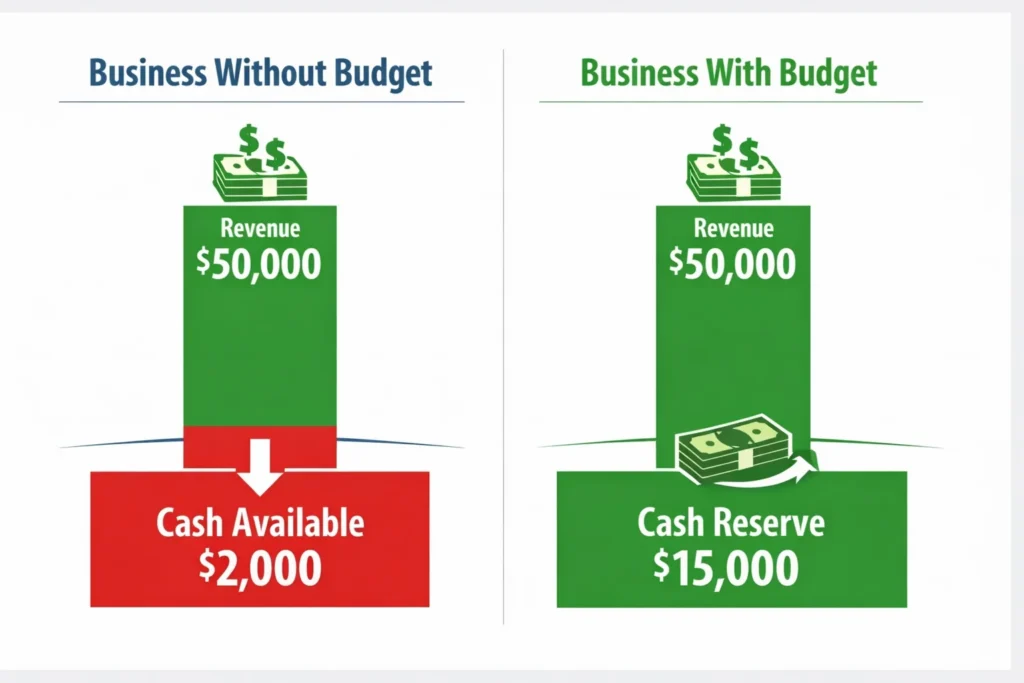

Why Most Small Businesses Struggle Without a Budget

Most small businesses that fail do not fail because they lacked customers. They fail because they lacked a financial plan. This reality demonstrates the importance of budgeting in small business more clearly than any theory could.

The importance of budgeting in small business becomes painfully obvious when you look at the patterns. A business brings in solid revenue. The owner feels confident. Money flows in and flows out. And then one month, something shifts. A big client pays late. An unexpected expense hits. Suddenly there is nothing left to cover the basics.

This is not bad luck. This is what happens when a business runs without financial management guardrails.

A critical observation that shaped my thinking: most small businesses fail not because they lack customers, but because they fail to track the leakage of small expenses. Not the big purchases. The small ones. The subscriptions nobody cancelled. The software renewals that slipped through. The minor fees that quietly add up to a significant monthly drain.

Business spending leakage is where most businesses lose money without realizing it, which is why implementing strategies to reduce recurring expenses becomes essential for protecting your margins. Consider this reality: if your business earns five thousand dollars a month but costs four thousand five hundred dollars to exist, you are one slow month away from a serious financial crisis.

That margin is not a cushion. That is a cliff edge.

Financial planning and financial stability are not luxuries for big businesses. They are survival tools for small ones.

The “High Sales, No Profit” Trap That Catches New Owners Off Guard

This is one of the most demoralizing situations a business owner can experience. Everything looks successful from the outside. Orders are coming in. The calendar is full. Revenue is growing.

But the bank account tells a completely different story.

This happens when there is no budget connecting revenue to expenses. Without a plan, costs quietly expand to fill whatever space the revenue creates. Marketing goes up because things are busy. Equipment gets upgraded. Staff hours increase. Before long, the profit margins shrink to almost nothing even though sales have never been better.

Businesses with high sales fail all the time because they lack an operating profit framework. Sales and profitability are not the same thing. A budget is the tool that connects them and keeps your cost control habits honest.

What Financial Stability Actually Looks Like in a Small Business

Financial stability does not mean having an overflowing bank account. For most small business owners, it simply means knowing what is coming, knowing what is going out, and having a plan that makes both work together. When you understand how to allocate your financial resources effectively, you gain the confidence to make decisions without constantly worrying about whether the money will be there.

When your budget is working properly, you are not anxious around payroll time. You are not surprised by tax season. You are not making financial decisions based on how your balance looks on a random Tuesday afternoon.

That kind of calm is achievable. And it starts with a written plan.

The Budget Mistake Most Owners Make Before They Even Start

Before I walk you through how to build a budget, I want to share one idea that completely changed how I think about business finances. It comes from the Profit First methodology, and I consider it one of the most practically useful financial concepts I have ever come across.

Most business owners think about money this way:

Sales minus expenses equals profit.

That formula seems logical. You earn money, you pay your costs, and whatever is left over is your profit. The problem is that in practice, whatever is left over is almost always nothing. Costs have a way of rising to meet available cash. Lifestyle creep happens in business the same way it happens in personal finances.

The Profit First approach flips the formula:

Sales minus profit equals expenses.

You decide your profit target first. You pull that money out before you pay anything else. Then you run your business on what remains.

This is not just a mental shift. It produces fundamentally different financial behavior. When you remove profit from the equation first, you are forced to run leaner. You question every cost more carefully. You find that a lot of the spending that felt necessary becomes optional when you are working with less.

If you cannot measure it, you cannot manage it. And if you never protect your profit before expenses consume it, you will never measure it accurately enough to manage it.

I am not saying this is the only way to budget. But it is worth understanding before you build your first budget, because it might change where you put the numbers.

The Four Budgeting Methods Small Businesses Actually Use

There is no single correct way to budget. The right method depends on your business type, your revenue patterns, and honestly, your personality. Here are the four approaches that actually work in practice, with an honest assessment of when each one makes sense.

Zero-Based Budgeting: Start From Scratch Every Period

Zero-based budgeting means you start every budget period from zero. Every expense must be justified from scratch. You do not carry forward last year’s numbers and assume they are still valid. You rebuild the entire budget with fresh eyes.

This approach connects to the principle that every dollar should have a destination before it gets spent. It is thorough, and it forces you to question whether every cost is still earning its place.

Zero-based budgeting is best for businesses going through a restructure, looking to cut costs aggressively, or simply wanting maximum control over where money goes. The drawback is that it takes time. If you are a solo operator running five projects at once, rebuilding your entire budget from scratch every month may not be realistic.

Incremental Budgeting: Build on What You Already Know

Incremental budgeting is the most common approach for established small businesses, and for good reason. You take your previous period’s budget as the starting point and adjust it up or down based on expected changes. This is a core part of the budgeting process in a small business that works well for predictable operations.

Using prior year growth rates to project sales is a practical and reliable approach. If your revenue grew by twelve percent last year, you project a similar growth rate and adjust your expenses accordingly. If you expect a five percent decline, you reduce your allocations by a similar percentage.

This method is fast, relatively accurate, and easy to maintain. The risk is that it can carry forward inefficiencies. If you budgeted too much for a certain expense last year and nobody noticed, that inflated number just rolls forward. A quick audit of your historical spending before building an incremental budget keeps this problem in check.

Activity-Based Budgeting: Budget Around What You Actually Do

Activity-based budgeting ties your financial projections to specific business activities rather than broad departments or general categories.

For example, instead of just listing a marketing expense, you break it down by campaign, by channel, or by client acquisition activity. Each activity gets its own budget line based on what it actually costs to run.

This method works particularly well for service businesses where your operating expenses are directly driven by the work you do. If you charge by project, this approach makes it much easier to see whether each activity is generating a positive return on investment.

Percentage-Based (Allocation) Budgeting: The Method Built for Beginners

This is the method I recommend most often to business owners just getting started, because it scales automatically and requires minimal maintenance once you set it up.

Instead of assigning fixed dollar amounts to expense categories, you assign percentages of your gross revenue. This budget allocation approach means when revenue goes up, your allocations increase proportionally. When revenue dips, your allocations shrink automatically. You are building flexibility directly into your financial framework.

Here is how it works in practice: you decide that marketing gets ten percent of revenue, salaries get thirty percent, rent gets eight percent, and software gets five percent. You then convert those percentages to actual dollar amounts based on your revenue for that month.

The beauty of this approach is that it forces discipline without complexity. Your budget categories stay balanced relative to your income, and you always have a clear picture of where your money is going across all your revenue streams.

How to Build Your Small Business Budget in 7 Steps

This is the section I wish had existed when I first started thinking seriously about business finances. The budgeting process in a small business does not need to be complicated, but it does need to be intentional. Here is a straightforward, practical approach that actually works.

Step 1: Set Your Financial Goals Before Touching Any Numbers

Most people start budgeting by opening a spreadsheet and typing numbers. That is the wrong place to start.

Before you write down a single dollar figure, you need to know what this budget is actually supposed to accomplish. Are you trying to grow revenue this year? Pay down a business loan? Save enough to hire your first employee? Reduce your personal financial stress?

Your financial goals determine everything that comes after. A budget built around growth looks completely different from a budget built around stability or debt reduction. Without a goal, budget planning becomes a guessing exercise with no meaningful destination.

Take fifteen minutes before you build your budget and write down your top two or three financial priorities for the year. Then build your numbers around those priorities.

Step 2: Estimate Revenue the Right Way (Use the Floor Method)

Here is one of the most important mindset shifts in budgeting: be pessimistic about income and realistic about costs.

Most business owners do the opposite. They project optimistic revenue and underestimate expenses, and then they wonder why the budget never works out. I have seen too many business owners crash financially because they budgeted on optimistic revenue. It is far better to be pleasantly surprised by higher-than-expected income than devastated by shortfalls.

The Floor and Ceiling method solves this problem simply. Your Floor is the minimum realistic amount you could earn in a month based on your actual history. Your Ceiling is your goal or your best month. You build your budget around the Floor, not the Ceiling.

When you estimate your revenue forecasting based on your worst realistic month, you build a budget that works even when things are slow. Any revenue above your Floor goes toward savings, profit, or reinvestment rather than covering expenses you already committed to.

For the gross revenue estimate, pull at least 6 to 12 months of historical data for your financial projections if you have it. If you are brand new and have no history, be conservative. It is far better to be pleasantly surprised than financially overwhelmed.

Step 3: List Every Fixed Cost You Pay No Matter What

Fixed costs are your non-negotiables. These are the bills that arrive regardless of whether you made a single sale this month.

Common fixed costs include:

• Rent or office space

• Insurance premiums

• Loan repayments

• Software subscriptions that run monthly

• Minimum payroll for permanent staff

• Recurring professional service fees (accounting or legal retainers)

List every single one of these. Then total them up. That number is the absolute minimum your business must earn every month just to keep the lights on. If your revenue floor does not cover your fixed costs, that is your first and most urgent financial problem to solve.

Your annual budget should account for the full year of these overhead costs, including any that are paid quarterly or annually. Divide those into monthly equivalents so your monthly budget picture is accurate.

Step 4: Estimate Your Variable Costs Honestly

Variable costs are the expenses that change based on what your business does. When you sell more, some of these go up. When things slow down, they can come down too.

Common variable costs include:

• Marketing and advertising spend

• Raw materials or product inventory

• Shipping costs

• Contractor or freelance labor

• Utilities that fluctuate with usage

• Travel for client visits or events

The critical task here is to go through your expense tracking records and look for what I call leakage. These are small recurring charges that have piled up quietly over time. A tool you signed up for eighteen months ago and barely use. A subscription that auto-renews each year. Small platform fees that show up every month.

Business spending leakage is where most businesses lose money without realizing it. I recommend doing a full subscription and recurring charge audit every quarter. Cancel anything that does not have a clear purpose and a measurable return.

Step 5: Plan for One-Time and Unexpected Costs

This is the step most budget guides skip, and skipping it is the reason so many carefully built budgets fall apart.

One-time costs are not actually surprising if you plan ahead. At some point this year, you will probably need to replace a piece of equipment, pay for a professional development course, redesign something on your website, cover an unexpected repair, or invest in a tool that will save you significant time.

None of these are emergencies in isolation. But if they all hit your monthly budget as surprises, they create real financial disruption.

The solution is simple: create a capital expenditure line in your budget, even if it is small. Set aside a specific amount each month for planned future purchases. And separately, always include a miscellaneous buffer of around five to ten percent of your total monthly budget. Something will always come up. Build the buffer in before it happens, not after.

Step 6: Calculate Your Bottom Line and Know What It Means

Subtract your total estimated expenses from your total estimated revenue. What you get is either a surplus or a deficit.

If you have a surplus, the financial decisions you face are good ones. You can allocate that surplus toward a profit account, an emergency fund, future investments, or growth spending. But make those decisions intentionally and in advance, not in the moment.

If you have a deficit, do not panic. First, check whether your revenue estimate was realistic or overly pessimistic. Second, look at your variable costs. These are always the first place to trim because they are more flexible. Do not touch your marketing budget first, even though it feels like an easy cut. Reducing your ability to earn new business usually makes the deficit worse over time.

Understanding your net income and budget variance is what separates reactive financial management from proactive financial control.

Step 7: Choose Your Tool and Set Up Your Budget Document

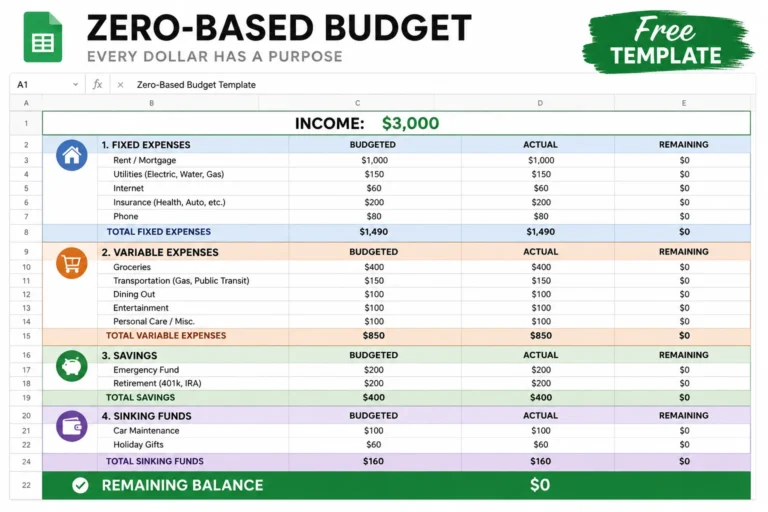

You do not need expensive software to build an effective budget. For most small businesses just starting out, Google Sheets or Excel is genuinely all you need.

Set up your budget spreadsheet with your expense and revenue categories in rows and the twelve months of the year in columns. This gives you a full-year view at a glance and makes it easy to track your actual numbers against your projections each month.

A solid business budget template should include:

• Rows for each income source

• Rows for each fixed cost category

• Rows for variable cost categories

• A row for one-time expenses

• A summary row showing your net position for each month

Start simple. You can always add complexity later. Getting something real and usable in front of you this week is far more valuable than waiting until you find the perfect tool.

How to Organize Your Budget Categories in Small Business (So Nothing Gets Lost)

Most beginner budget guides tell you to split your expenses into fixed and variable costs and call it done. That is a reasonable starting point, but professional bookkeepers and accountants organize expense categories in a more structured way that gives you much cleaner data for decision making.

Understanding how income and expenses flow through three main buckets will immediately improve both your expense tracking and your overall financial clarity.

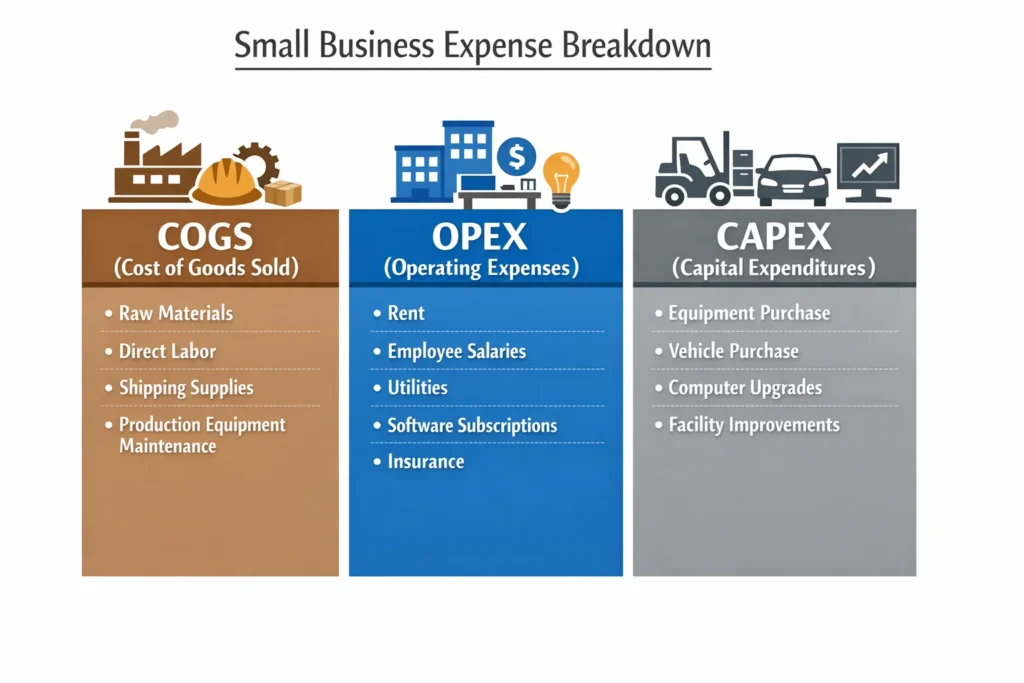

COGS vs. OPEX vs. CAPEX: The Three Buckets Your Budget Needs

COGS (Cost of Goods Sold) is the direct cost of producing or delivering whatever you sell. If you make a physical product, COGS includes materials and production labor. If you provide a service, COGS includes the direct labor or contractor cost tied specifically to delivering that service. It does not include your general overhead.

OPEX (Operating Expenses) is your general overhead. These are the costs of running the business that are not directly tied to producing a specific product or service. Rent, marketing, administrative salaries, software, and utilities all live here.

CAPEX (Capital Expenditures) covers large investments in long-term assets. New equipment, vehicles, major technology upgrades, or significant infrastructure improvements count as capital expenditures rather than regular operating expenses.

Here is why this distinction matters in practice: if you sell physical products and your COGS is very high, you need to subtract those costs from your gross revenue before you apply any percentage-based allocations to the rest of your budget. Otherwise, you will consistently over-allocate your operating expenses and find yourself underfunded for the actual cost of running the business.

The 5-10% Miscellaneous Buffer That Saves Budgets Every Month

I covered one-time expenses in the step-by-step section, but this point deserves its own dedicated mention because it is one of the most practical budget categories that most business owners leave out completely.

Always include a miscellaneous line item in your budget. A reasonable amount is five to ten percent of your total monthly budget.

This is not sloppy financial planning. It is honest financial planning. The moment you decide that your budget is perfectly accounted for with zero room left over, something will appear and prove you wrong. A client tool breaks and needs replacing. A short-notice professional service is required. A software price increases without warning.

The miscellaneous buffer is not automatically spent each month. What it does is prevent every unexpected cost from forcing you to immediately reallocate money from another category and throw your entire budget into chaos.

Good cost control does not mean eliminating every financial cushion. It means being strategic about where you put them.

What Percentage of Revenue Should Go Where?

This is one of the questions I get asked most often by small business owners who are building a budget for the first time. They want a starting framework. Something real to work from.

The honest answer is that exact percentages vary depending on your industry, your cost structure, and your business model. But several experienced financial coaches and accounting professionals have shared frameworks that work well as starting points for most small businesses.

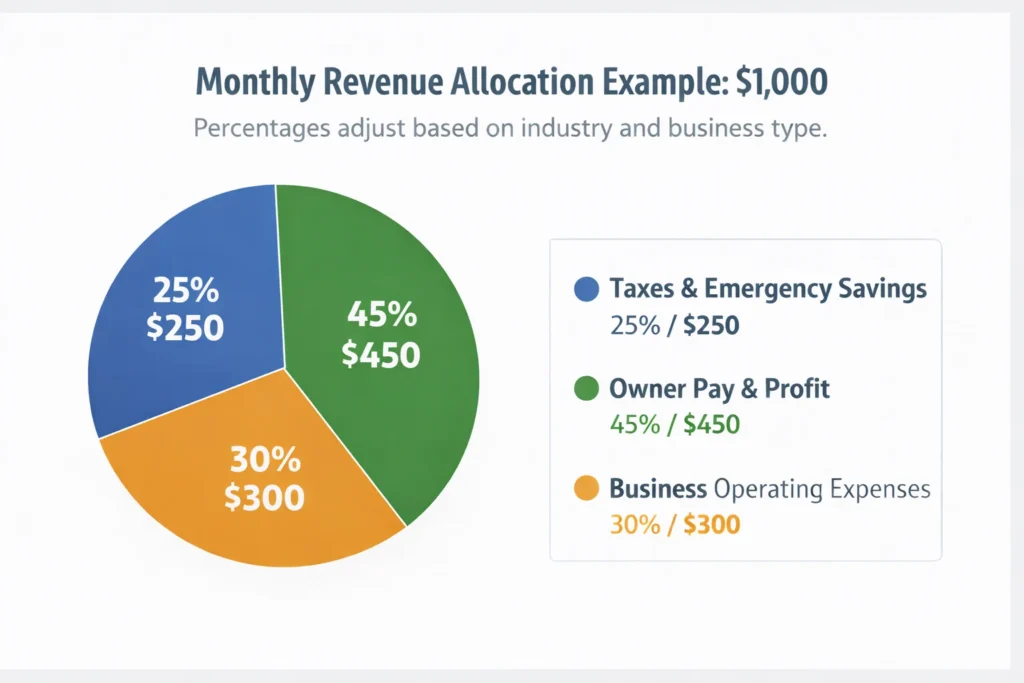

Here is a general budget allocation framework worth considering:

Taxes and emergency savings: 20-30% of gross revenue. This money goes into a separate account the moment it arrives and does not get touched for regular expenses. Tax season should never be a crisis. Setting aside this percentage every month means it never will be. The Small Business Administration (SBA) recommends this reserve approach for small business stability.

Owner pay and profit: 40-50% of gross revenue. This includes what you pay yourself and the profit your business keeps. Treating this as a priority allocation rather than an afterthought is one of the most important financial decisions a small business owner can make. More on this in the next section.

Business operating expenses: 30-40% of gross revenue. This covers everything else: marketing, tools, rent, staff, contractors, insurance, and every other cost of running the business day to day.

For revenue streams that involve high material or production costs, subtract those COGS from your gross revenue first before applying the percentages. Otherwise, your operating expense budget will not stretch to cover everything it needs to.

These percentages are starting points, not rules set in stone. Your financial planning goals, industry norms, and growth stage will all influence where you land. But if your current expenses are consuming ninety percent of your gross revenue with nothing left for tax reserves or profit, you need a break-even analysis to understand your minimum revenue requirement and a clear framework to work toward profitability.

The return on investment of getting your revenue allocation right is significant. Businesses that run with intentional percentage-based budget allocation, often called the Profit First methodology developed by Mike Michalowicz, tend to have far more financial stability than those that allocate expenses first and hope for profit afterward.

The One Number Every Small Business Owner Must Know: Your Burn Rate

There is one number in your budget that tells you more about your financial health than almost any other single figure. Most small business owners either do not know it or have never calculated it.

That number is your burn rate.

Your burn rate is the total amount your business spends every single month regardless of what revenue comes in. It is the cost of your business existing for thirty days. It covers every fixed obligation, every recurring expense, and every predictable operational cost.

Knowing your burn rate is not just useful for budgeting. It is essential for survival planning. When you know exactly how much your business costs to run, you can calculate your runway: the number of months your business can continue operating if revenue stopped completely today.

Runway equals your current cash reserves divided by your monthly burn rate.

If you have four thousand dollars in your business account and your burn rate is two thousand dollars per month, your runway is two months. That is a vulnerable position. Knowing that number is not frightening. Not knowing it is.

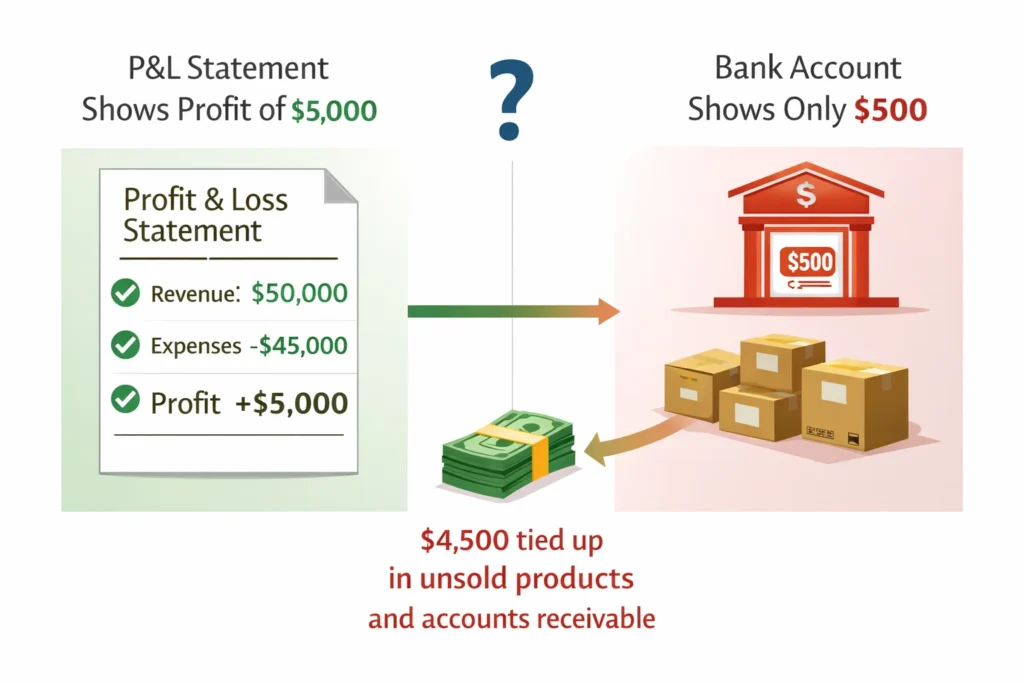

Cash Flow vs. Profit: Why You Can Be Making Money and Still Go Broke

This distinction between cash flow and profit is genuinely one of the most important concepts in small business budgeting and cash flow management, and it surprises a lot of business owners when they encounter it for the first time.

Profit is a calculation on paper. It is the difference between what you earned and what you spent during a period. But profit does not always reflect actual cash availability.

Consider a product-based business. You purchase inventory using cash, but you will not receive payment from customers until the inventory sells and invoices get paid. During that gap, your working capital is tied up in physical stock. Your income statement might show a profit for the month while your bank account sits near zero because all your cash is sitting on shelves or in transit.

You can be profitable on paper and still find yourself unable to make payroll because the cash is not there yet.

Cash flow management is the discipline of making sure money arrives when you need it, not just at some point during the month. Your profit margins tell you whether the business model works. Your cash flow tells you whether you can survive while it does.

Understanding both is essential. Tracking only one will eventually catch you off guard.

How to Calculate Your Burn Rate and Runway in 5 Minutes

Here is the quickest way to get these numbers right now.

Add up every fixed monthly cost your business pays: rent, insurance, minimum payroll, loan payments, recurring software, and any other non-negotiable monthly expenses. That total is your monthly burn rate.

Now look at your current business cash balance. Divide that balance by your monthly burn rate. The result is your runway in months.

If your burn rate is three thousand dollars and you have nine thousand dollars in your business account, your runway is three months. That is the window you have to generate new revenue before you face a genuine cash crisis.

Once you know this number, your budget monitoring takes on a completely different level of meaning. Every decision about spending becomes a decision about runway. Does this expense shorten my runway unnecessarily? Does this investment generate returns fast enough to justify the risk?

Financial health for a small business starts with knowing your burn rate and protecting your runway.

The Part Nobody Budgets For: Paying Yourself Properly

I am going to say something that a lot of small business owners have never heard clearly stated: your salary is a business expense.

It is not the money left over after everything else gets paid. It is not a bonus for months when things go well. It is a line item in your budget that gets allocated before you calculate profit, not after.

This is one of the most common and most painful financial decisions small business owners make incorrectly. When your income as the owner is treated as whatever remains after all business costs are covered, two things happen reliably. First, you chronically underpay yourself. Second, you never have an accurate picture of your true profit margins because your own labor is not priced into the budget.

A business that appears profitable because the owner is effectively paying themselves nothing is not a profitable business. It is an unpaid job with overhead.

How to Structure Owner Pay in Your Budget

The structure of how you pay yourself depends on your business entity type. If you operate as a sole proprietor or a single-member LLC, you typically take an owner’s draw rather than a formal salary. If you have elected S-Corporation tax status, you are required to pay yourself a reasonable salary and document it properly.

Regardless of entity structure, the budgeting principle is the same: decide what you need to live on and what fair compensation for your role would look like in the open market. Build that number into your budget as a fixed cost and protect it the same way you protect rent.

Most practitioners working in this area suggest that owner compensation and business profit together should represent around forty to fifty percent of gross revenue. That combined allocation is your return for building and running the business.

For a small business owner just starting out, this number might be lower in the early months while you establish the business. But it should be planned for explicitly, not treated as an afterthought.

The moment you start treating your own salary as a real budget allocation, your financial goals become much clearer and your overall budget accuracy improves dramatically.

The Bank Account System That Makes Budget Discipline Automatic

I want to share something that dramatically simplifies budget management for almost everyone who tries it. It does not require any special software. It does not require an accounting background. It requires about five minutes of setup time and a small amount of bank paperwork.

The system is this: use multiple business bank accounts to physically separate your money by purpose.

This sounds almost too simple to matter. But the reason most budgets fail is not because the math is wrong. It is because when all your money lives in one account, it all looks available. The budget categories exist only in your spreadsheet. In real life, that account balance is what your brain responds to.

When you physically separate your money into purpose-specific accounts, the discipline becomes structural rather than willpower-based. You cannot accidentally spend your tax reserve because it is in a different account you do not touch for expenses. This system might seem overly simple, but I have recommended it to dozens of small business owners over the years. Every single one who actually implemented it reported better financial discipline within the first month.

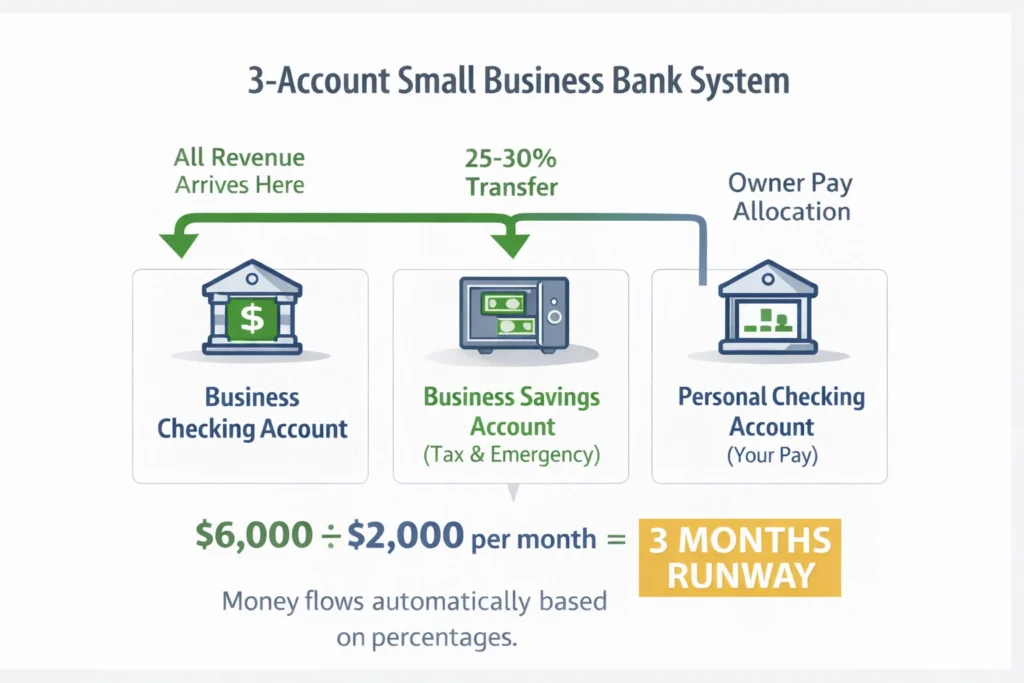

The 3-Account Beginner Setup (Start Here This Week)

If you currently have all your business and personal money in one place, this is the minimum viable account structure you should set up as soon as possible.

Business Checking Account: Every dollar your business earns goes here first. All client payments, sales revenue, and any other business income lands in this account. Give clients only this account number for payments.

Business Savings Account (Tax and Emergency Fund): Transfer a percentage to this account every time revenue arrives (typically 25-30% for taxes, plus additional for emergency reserves). This covers your tax obligations throughout the year and serves as your emergency buffer. It does not get touched for regular business expenses.

Personal Checking Account (Your Pay): On a regular schedule (weekly or monthly), you transfer your owner pay allocation from your Business Checking to your personal account. This is your income. It is separate from business finances and managed completely independently.

That is it for the beginner setup. Three accounts, one simple financial management habit, and your money has structure it did not have before.

The 5-Account Advanced System (When You Are Ready to Scale)

Once you are comfortable with the three-account structure and your business is generating consistent revenue, you can evolve to the five-account system used by the Profit First methodology.

The five accounts are:

• Income Account: All revenue deposits land here.

• Profit Account: A protected percentage (typically 10%) of every deposit goes here immediately. This account represents your business profitability and is not used for expenses.

• Owner Compensation Account: Your personal pay allocation (typically 40-50% of revenue).

• Tax Account: Your ongoing tax reserve (typically 25-30% of revenue).

• Operating Expenses Account: What remains after profit, owner pay, and tax allocations are transferred. This is the only account you pay business expenses from.

The key discipline within this system is the transfer rhythm: move money between accounts twice a month on the tenth and the twenty-fifth. This creates a predictable budget cycle that removes the impulse decisions that drain most business finances.

Treating your tax and profit transfers like automatic bills that get paid immediately every time revenue arrives is what makes this system work without relying on willpower or daily tracking.

10 Budgeting Mistakes That Quietly Drain Small Business Cash

I want to walk you through the ten budgeting mistakes I see most often, because most of them are completely preventable once you know what to look for. Each one has a clear consequence and a straightforward correction.

Mistake 1: Treating Your Salary as Whatever Is Left Over

You work a full year in your business and pay yourself based on whatever happens to remain after every other expense is covered. This means your income is unpredictable, often inadequate, and invisible to your actual profit calculation.

Fix it: Set your owner pay as a fixed budget allocation. Pay yourself first, on a schedule, as a line item.

Mistake 2: Overestimating Income to Make Numbers Look Good

You project your best-case revenue because it makes the budget feel more comfortable. Then reality does not match the plan and you spend the rest of the year chasing a shortfall.

Fix it: Use the Floor method. Project based on your minimum realistic month. Build your expenses around that number.

Mistake 3: No Plan for One-Time or Emergency Costs

A piece of equipment breaks. A website needs updating. A professional service is required on short notice. None of these are genuinely unexpected when you look at the pattern over time. But without a budget category for them, they break your financial decisions every time.

Fix it: Create a capital expenditure line item and a miscellaneous buffer in every budget period.

Mistake 4: Missing the Leakage of Small Subscriptions

You signed up for twelve different tools over the past two years. Some you use daily. Some you barely remember. All of them are billing you monthly. The total adds up to a significant monthly expense that nobody audited.

Fix it: Set a calendar reminder for a quarterly subscription audit. Review every recurring charge and cancel what is not earning its place. This is expense tracking at its most practical.

Mistake 5: Mixing Personal and Business Finances

Everything goes through one account. Your groceries share a bank statement with your supplier payments. Come tax time, separating them is a nightmare. And your business spending numbers are meaningless because personal costs contaminate them.

Fix it: Open a dedicated business account immediately. Keep every personal transaction completely separate from the first day.

Mistake 6: Creating a Budget Once and Forgetting It

You spend an afternoon building a budget in January. You look at it in November and discover it bore no resemblance to the year you actually had. Nothing was updated. No adjustments were made. The document was useless the moment it stopped being reviewed.

Fix it: Budget monitoring is not optional. Schedule a short review weekly and a deeper review monthly. More on this in the next section.

Mistake 7: Cutting Marketing Budget When Cash Gets Tight

Revenue dips. Anxiety rises. You immediately cut the marketing budget because it is a large and visible number. Six weeks later, your lead flow has collapsed and revenue is even lower than before.

Fix it: Marketing is how you generate the revenue that pays every other expense. Before cutting it, look for ways to make it more efficient or find creative low-cost alternatives. Return on investment should drive these financial decisions, not panic.

Mistake 8: No Miscellaneous Buffer in the Budget

You build a budget where every dollar is perfectly allocated with nothing left over. You feel organized and thorough. Then something unexpected happens and it breaks the entire structure.

Fix it: Add a miscellaneous line for five to ten percent of your total budget. This is not waste. It is reality-testing built into the plan.

Mistake 9: Confusing Profit With Cash Flow

Your income statement shows a profit this month. You feel comfortable about spending. But the cash that created that profit is still sitting in unpaid invoices or tied up in inventory. Your actual bank account is near empty.

Fix it: Track both profit and cash flow as separate metrics. A positive P&L does not mean cash is available today. Understand where your working capital actually is at any given time.

Mistake 10: Never Comparing Budget to Actual P&L

You built a budget. Your bookkeeper maintains records. But you never sit down to compare what you planned to what actually happened. The budget exists in isolation from reality, and neither document teaches you anything useful.

Fix it: Every month, sit down with your budget and your actual profit and loss statement side by side. The gap between them is your most valuable financial education. Understanding your budget variance over time is how your forecasting gets more accurate each year.

How to Keep Your Budget Working Every Month

Building a budget is an accomplishment. But a budget that sits in a drawer or a forgotten spreadsheet tab does nothing for your financial health. The ongoing practice of budget monitoring is what turns a planning document into a management tool.

Weekly check-in (5 minutes). Once a week, open your bank accounts and your budget side by side. Check your current balances against where your budget says you should be. This is not a deep analysis. It is a quick pulse check to catch obvious problems before they compound and help you stay on track with your spending targets. You are looking for red flags, not conducting a full audit.

Most budget guides tell you to review your numbers monthly. That is good advice as far as it goes, but it is not quite specific enough to be actionable. Here is the review system I think works best.

The Three-Level Review Rhythm That Takes 30 Minutes a Month

Weekly check-in (5 minutes). Once a week, open your bank accounts and your budget side by side. Check your current balances against where your budget says you should be. This is not a deep analysis. It is a quick pulse check to catch obvious problems before they compound. You are looking for red flags, not conducting a full audit.

Monthly P&L comparison (20 minutes). At the end of every month, compare your budget projections to your actual profit and loss statement. For every category, note whether you came in above or below your budget. Do not just note the gap. Ask why it happened. Understanding the cause of your budget variance is how you build better projections over time.

Quarterly strategic adjustment (30 to 45 minutes). Every three months, step back and look at the bigger picture. Are your financial goals still the same? Has anything in your business changed significantly enough to require adjusting your annual budget? This is where you make mid-year corrections rather than forcing a budget that no longer fits your actual situation.

Budgeting is not a once a year event. It is an ongoing financial discipline that takes less than an hour a month when you approach it systematically.

Reading Your Budget Variance: What the Numbers Are Telling You

Budget variance is the difference between what you planned and what actually happened. A positive variance means you spent less or earned more than projected. A negative variance means the opposite.

Small variances are normal. Markets shift. Timing changes. A payment expected on the twenty-eighth might arrive on the third of the following month. Large or consistent variances warrant attention. If your actual expenses are consistently running fifteen to twenty percent above budget projections, your estimates need adjustment.

The key insight: a budget is a guess, and your profit and loss statement is the truth. The monthly habit of comparing these two documents closes the gap between prediction and reality over time.

When Your Budget Tells You It Is Time to Hire

Your budget is not just a record of expenses. It is a decision-making tool. And one of the most valuable decisions it can help you make is whether you are financially ready to bring someone onto your team.

The signal you are looking for is consistent. If your revenue has been running above your projections for several months in a row, and your expenses are staying consistently below your budget allocations, the gap between those two trends represents your real capacity to support a new hire.

Before hiring, run the numbers. Add the full cost of the new position, including salary, benefits, payroll taxes, and any additional tools or equipment they will need, to your existing expense budget. Then check whether your current revenue floor still covers that expanded cost base comfortably.

If it does, your business growth is signaling financial readiness. If it does not, you know exactly what revenue milestone you need to hit before the decision makes financial sense. That is what a working budget gives you: the ability to make big financial decisions with clarity rather than guesswork.

Tools and Templates to Build Your Budget Without Starting From Scratch

One question I hear constantly from small business owners is this: what tool should I use for my budget? My answer might surprise you.

The best tool is the one you will actually open and use regularly. Sophistication is far less important than consistency.

Free Budget Tools That Are Good Enough to Start With

For most small businesses, especially those in the early stages, Google Sheets or Microsoft Excel is completely sufficient. Both are free or low-cost, widely understood, and flexible enough to build a functional business budget template with a few hours of setup.

A good business budget template in either tool should have your revenue sources listed by category in one section, your fixed and variable costs organized clearly below, a capital expenditure or one-time expense line, a miscellaneous buffer row, and a summary section that shows your net position by month.

If building from scratch feels intimidating, there are solid startup budget templates available through platforms like Google Workspace or Microsoft Office that you can adapt to your specific business structure without starting from zero.

The advantage of spreadsheet-based budgeting for beginners is full transparency. You can see every formula, understand every calculation, and customize anything without being locked into a predetermined structure.

When to Upgrade to Paid Accounting Software

There are clear signs that your business has outgrown a manual spreadsheet budget:

• You are managing invoices from multiple clients with different payment terms

• You have employees or contractors whose hours and payments need tracking separately

• You are managing product inventory with regular reordering cycles

• Your tax situation has become complex enough that your bookkeeper spends hours monthly reconciling accounts

When you reach that stage, accounting software designed for small businesses becomes worth the investment. QuickBooks is the most widely used option and integrates with most bookkeeping practices. FreshBooks works particularly well for service-based businesses and solo operators who need invoicing built into the same platform as their financial management tools.

The right accounting software does not replace a budget. It gives you cleaner, faster data to inform your budget decisions and makes your bookkeeping records far easier to maintain.

When Your Budget Needs a Professional Eye

There comes a point in many small businesses where doing your own financial management is costing you more than hiring someone to do it properly.

Bookkeeping is recording the financial data. Accounting is interpreting it. If you are doing neither particularly well, both your budget accuracy and your tax position are likely suffering.

Signs that you need professional help include:

• Spending more than a few hours weekly on financial administration

• Consistently finding that budget projections are far from actual results

• Feeling uncertain about tax obligations or deductions

• Making major business decisions without a clear financial picture

A bookkeeper handles the day-to-day recording and keeps your records clean. An accountant interprets those records and helps you plan. A fractional CFO, which is an experienced finance professional you hire part-time rather than full-time, can provide strategic budget oversight and financial planning for growing businesses that are not yet large enough for a full-time finance hire.

The benefits of hiring a CFO for budgeting at the right stage of growth include better financial projections, cleaner cash flow management, and the ability to make growth decisions based on real data rather than gut feeling. It is worth understanding what level of professional support your business genuinely needs, and building the cost of that support into your budget.

Start Small, Stay Consistent, and Let the Numbers Guide You

I want to close this guide with something that I believe is more important than any specific technique or formula covered above.

The biggest financial mistake a small business owner makes is not a math error. It is avoiding the numbers altogether because they feel overwhelming or scary.

Every expert perspective I have encountered on this topic agrees on one point: even an imperfect budget is infinitely more useful than no budget at all. A rough plan that you actually review and follow is worth more than a perfect spreadsheet that gets opened twice a year.

If you have been reading this guide and feeling the weight of everything there is to do, let me give you a starting point that is genuinely achievable this week.

Open three bank accounts. Put a simple spreadsheet together with your basic income and expense categories. Look at your numbers for five minutes this Friday. That is it.

Financial planning for a small business owner is not a one-time event you complete and never revisit. It is a habit you build slowly, improve consistently, and benefit from for as long as you run your business.

Budgeting in small business is how you stop wondering where the money went and start deciding where it goes. Your financial health does not improve by earning more. It improves by managing what you earn with intention and clarity.

Start where you are. Start today. Your numbers will show you the way forward.

Frequently Asked Questions

How much of my revenue should I set aside for business expenses?

Most financial practitioners recommend keeping your operating expenses below forty percent of gross revenue. A practical starting framework is this: allocate twenty to thirty percent for taxes and emergency savings, forty to fifty percent for owner pay and profit, and thirty to forty percent for all business operating costs. If your business has significant cost of goods sold, subtract those production costs from your gross revenue first before applying these percentages to the remainder.

Do I need separate bank accounts for my small business budget?

Yes, and treating this as optional is one of the most expensive mistakes you can make. At minimum, maintain three separate accounts: a business checking account where all revenue arrives, a savings account strictly for tax reserves and emergency funds, and a personal account for your owner pay. Keeping all your money in one account makes real budgeting nearly impossible and creates serious problems when tax time arrives. The five-account system used in the Profit First methodology is the advanced version of this structure and works extremely well for growing businesses.

What is the difference between a budget and a profit and loss statement?

A budget is a forward-looking document. You create it before the money moves and it represents what you plan to earn and spend. A profit and loss statement is a backward-looking document. It shows what actually happened after the money moved. Both are essential. The budget is your plan. The P&L is your reality check. Comparing the two every thirty days is how you learn what your estimates are getting right and where they consistently miss.

What should I do if my budget shows I am spending more than I earn?

Start by checking your income estimate. Most owners overestimate revenue, and an inflated income projection makes the deficit look smaller than it actually is. Next, look carefully at your variable costs. These are more flexible than fixed costs and are where you should trim first. Audit every subscription and recurring charge to find leakage. Avoid cutting your marketing budget as a first response. Reduced marketing leads to reduced revenue, which makes the original problem worse. If the deficit is structural rather than temporary, you likely need to either reduce your fixed overhead or find ways to increase your revenue floor.

How often should I review my small business budget?

Three levels of review work well together. Do a quick five-minute check weekly where you compare your bank balances to your budget position. Do a twenty to thirty minute comparison monthly where you sit down with both your budget and your actual profit and loss statement and understand the variance between them. Do a thirty to forty-five minute strategic review quarterly where you assess whether your annual budget still reflects your business reality and make any significant adjustments needed for the months ahead.

How do I pay myself as a small business owner in my budget?

Your pay should be a planned budget allocation, not whatever happens to remain after all other expenses are settled. The exact structure depends on your business entity. Sole proprietors and single-member LLC owners typically take an owner’s draw. S-Corporation owners pay themselves a documented salary. Regardless of structure, the financial planning principle is the same: decide what fair compensation looks like for your role, build that amount into your budget as a fixed cost, and protect it with the same priority you give to rent or insurance. Most practitioners suggest that owner pay and business profit together should represent approximately forty to fifty percent of your gross revenue.

What is a burn rate and why does my small business need to know it?

Your burn rate is the total amount your business spends every month to continue existing, regardless of whether any revenue comes in. It includes every fixed cost and recurring operational expense. Your runway is calculated by dividing your current cash reserves by your monthly burn rate, giving you the number of months your business could survive with zero new income. Knowing both numbers transforms your financial health awareness. It tells you exactly how vulnerable your business is at any given moment and helps you make smarter decisions about spending, saving, and growth investments.

Final Thoughts

Building a budget is the foundation of financial management for your small business. The systems and strategies covered in this guide—from the basic three-account setup to the advanced Profit First methodology—provide you with multiple pathways to take control of your business finances.

The most important insight is this: you do not need perfection. You need consistency. The budget you build today, even if it is rough and imperfect, is infinitely more valuable than waiting for the perfect time to start.

Your financial stability depends not on how much money comes in, but on how intentionally you direct where it goes. Start small, review regularly, and let the numbers guide your business decisions.

The path to financial control in your small business begins with a single step: opening your first budget spreadsheet or setting up your first bank account. Everything else follows from that commitment to clarity.

Your numbers are waiting. Start today.