How to Calculate Interest on Savings Account: Complete Guide with Real Examples

I used to think calculating savings account interest was straightforward. Just multiply your balance by the interest rate, right? Wrong. After digging deep into how banks actually calculate savings account interest and tracking my own accounts for months, I discovered the real process is much more complex and fascinating than I ever imagined.

If you’ve ever wondered why your actual savings account earnings don’t match your quick calculations, you’re not alone. I’ll share everything I’ve learned about the interest calculation formula and daily compounding methods, including the insider secrets banks don’t advertise and the mistakes that could be costing you money.

Why Your Savings Account Interest Doesn’t Match Your Calculations

The first time I manually calculated my expected quarterly interest, I was confused. My math showed I should earn about $45, but my bank statement showed only $38. I thought the bank made an error until I learned the truth about how interest is calculated on savings accounts.

Banks don’t calculate savings interest the way most people think. I discovered that if your account balance fluctuates daily, you must calculate the interest for each day’s specific closing balance to get an accurate total for the quarter. This means every deposit, withdrawal, and transfer affects your interest calculation.

Here’s what really happens. Let’s say you have $10,000 in your account and withdraw $3,000 in the morning, then deposit $2,000 in the afternoon. Your daily interest calculation gets calculated on the lowest balance during that day, not your ending balance. In this case, you’d earn interest on only $7,000 for the entire day, even though you ended with $9,000.

The account balance fluctuations throughout each day directly impact your quarterly interest total. I learned this the hard way when I started tracking my daily balances and realized why my calculations never matched my statements.

Most people assume banks use average daily balances or ending balances for interest calculation. The reality is much more precise and potentially limiting if you’re not aware of how it works.

Understanding APY, Interest Rates, and What Banks Actually Pay You

Before diving into calculations, I had to understand what banks actually mean when they advertise interest rates. The terminology confused me initially, but once I grasped these concepts, everything else made sense.

The annual percentage yield (APY) represents your actual yearly return, including the effects of compounding. This savings account APY is different from the basic annual interest rate because it accounts for compounding frequency and how often your interest gets added to your principal amount.

Interest rates differ from bank to bank, and there’s no universal rate for all savings accounts. I’ve seen rates ranging from 0.01% at traditional bank accounts to over 4% at high-yield savings account options. The key is understanding that the advertised rate isn’t always what you’ll actually earn due to compounding frequency and minimum balance requirements.

APY vs APR: What’s the Difference and Why It Matters

I used to think APY vs APR were just different names for the same thing. They’re actually quite different, and the distinction affects your savings account earnings significantly.

APY includes the compound interest effects, showing you the actual percentage your money will grow over one year. APR is simply the basic annual rate without considering compounding. For savings accounts, you should always compare APY because it gives you the real picture of your returns.

For example, a 3% APR with daily compounding actually yields about 3.05% APY. That extra 0.05% might seem small, but on a $50,000 balance, it’s an additional $25 per year.

How Banks Structure Interest Payments (Daily, Monthly, Quarterly)

Many savings accounts offer an annual interest rate around 4%, but the calculation happens daily while the interest is typically credited to the account at the end of every quarter. This timing difference explains why you don’t see daily interest additions to your balance.

I learned that banks calculate your earned interest every single day, but they hold it until the crediting period arrives. Some banks credit monthly, others quarterly, and a few credit semi-annually. The more frequent the crediting, the faster your money compounds and grows.

Daily compounding means your interest earns interest sooner, leading to higher overall returns. Monthly compounding is common and provides good growth, while quarterly compounding is adequate but slower than more frequent options.

How to Calculate Interest on Savings Account: Basic Formula

After months of tracking my own accounts and testing different scenarios, I can confidently share the two main formulas you need to know. The choice between them depends on your bank’s specific calculation method.

The savings account interest formula starts with understanding whether your bank uses simple or compound interest. Most modern banks use compound interest, but some still apply simple interest for certain account types.

Understanding the interest calculation formula helps you predict your returns and verify bank calculations. I use these formulas monthly to double-check my statements and ensure I’m earning what I expect.

Each formula requires knowing your principal amount, which is your starting balance or the amount earning interest each day.

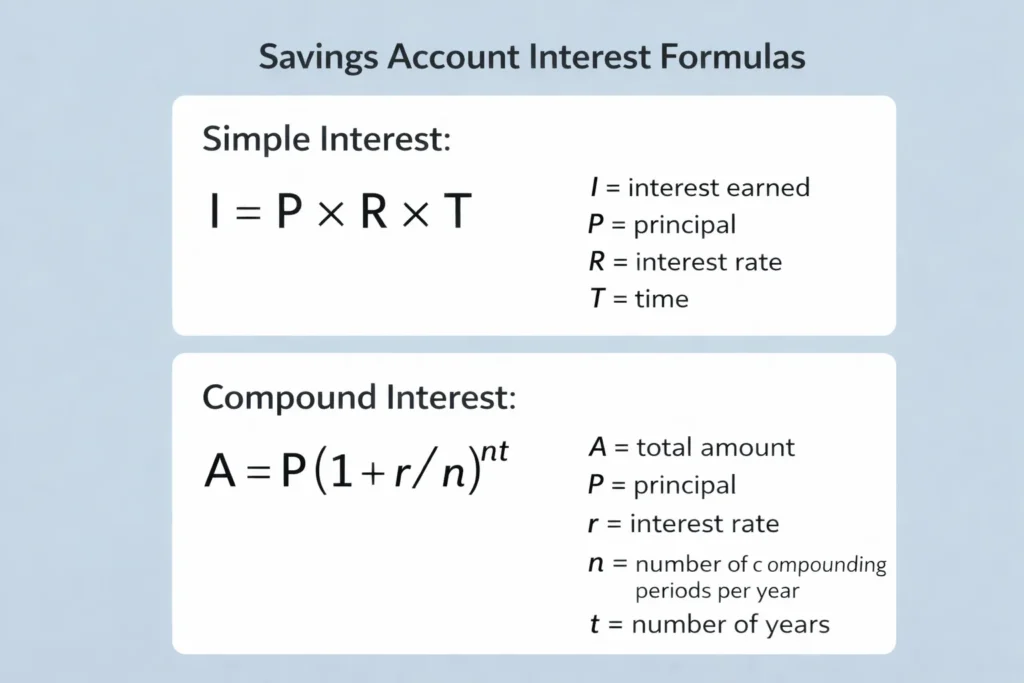

Simple Interest Formula Breakdown

Simple interest is the most straightforward calculation. The simple interest formula is Interest = Principal × Rate × Time.

Let me break this down with a real example I calculated for my own account. If you have $1,000 at a 3% annual rate for one year, your interest would be $1,000 × 0.03 × 1 = $30.

The principal amount is your account balance. The rate must be expressed as a decimal (3% becomes 0.03). Time represents the period in years (6 months would be 0.5).

Simple interest doesn’t compound, meaning you only earn interest on your original principal amount. This method is less common for savings accounts but still used by some banks for specific products.

Compound Interest Formula Breakdown

Compound interest is where things get exciting. The compound interest formula is Final Amount = Principal × (1 + r/n)^(nt), where r is the annual rate, n is the compounding frequency per year, and t is the time in years.

Using the same $1,000 example at 5% compounded monthly, the calculation becomes $1,000 × (1 + 0.05/12)^(12×1) = $1,051.16. That’s $21.16 more than simple interest would provide.

The compound interest formula accounts for earning interest on your interest. Each compounding period, your earned interest gets added to the principal amount, creating a larger base for the next calculation.

I’ve found that daily compounding provides the best returns, followed by monthly compounding, then quarterly. The difference becomes substantial over longer periods and larger balances.

Compound Interest vs Simple Interest Savings: Which Grows Your Money Faster

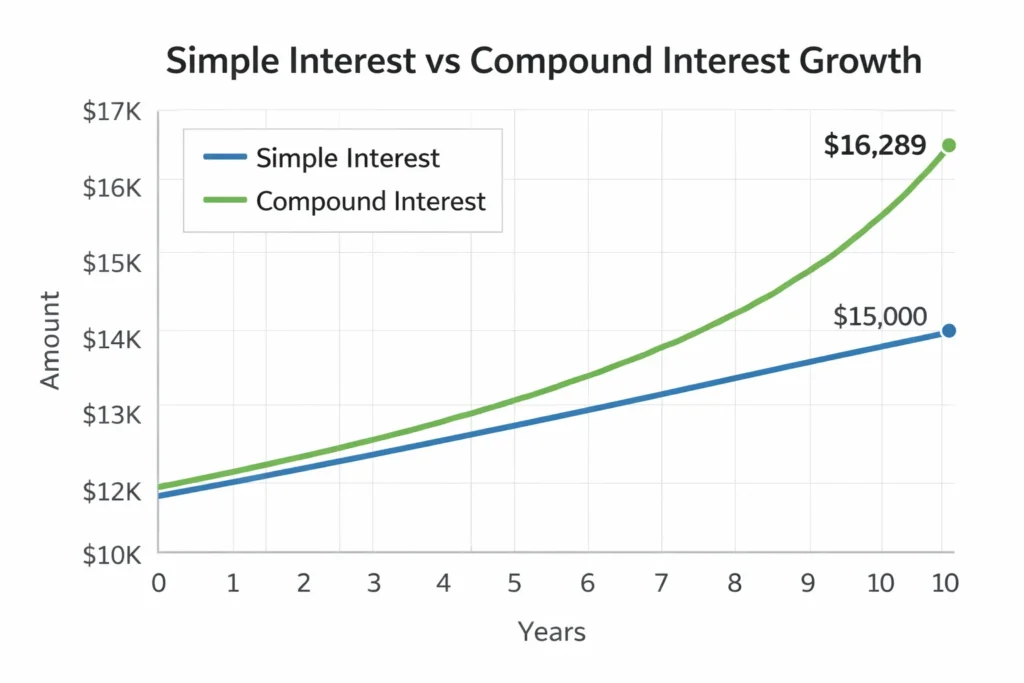

I tested both calculation methods with identical starting amounts to see the real difference over time. The results convinced me why compound interest matters so much for long-term savings growth.

With simple interest, you earn the same dollar amount every year. Compound interest accelerates your earnings because each year you’re earning interest on a larger amount of money than you started with, which means your returns grow progressively faster over time.

I discovered that instead of earning a flat $500 with simple interest on a $10,000 balance at 5%, you actually earn $512.67 due to the daily compounding effect. Over five years, this difference becomes dramatic.

Simple interest keeps your earnings linear and predictable.

Compound interest creates exponential growth that accelerates over time, making it far superior for building wealth. The more money you have available to save and put into accounts with compound interest, the more powerful this effect becomes—which is why reduce your monthly expenses to increase the amount you can deposit into these accounts.

Why Most Banks Use Compound Interest

Most financial institution providers use compound interest because it benefits both the bank and the customer. Banks can advertise higher effective returns through compounding, while customers earn more money over time.

Compound interest encourages customers to keep money in their accounts longer, providing banks with stable funding sources. It’s a win-win situation that explains why you’ll rarely find simple interest savings accounts anymore.

The banking industry shifted toward compound interest as competition increased and customers became more sophisticated about comparing returns.

The Acceleration Effect: How Compound Interest Speeds Up Over Time

By the fifth year of my tracking, the account was generating over $600 in interest annually compared to the $525 it earned in the first full year. This acceleration effect demonstrates the time value of money and compound interest’s most powerful feature.

Initially, my account earned about $1.37 per day. By the end of the first month, this increased to $1.38 per day, and by the end of the year, it reached $1.44 per day. Each day’s interest becomes slightly higher because the principal amount keeps growing.

The compounding frequency determines how quickly this acceleration occurs. Daily compounding provides the fastest acceleration, while quarterly compounding takes longer to show dramatic effects.

Time amplifies the acceleration effect exponentially. The difference between compound and simple interest becomes massive over decades, which is why starting early makes such a huge difference for long-term financial goals.

How Banks Calculate Interest on Savings Account Daily (The Real Process)

Learning how banks actually calculate interest daily changed everything about how I manage my account transactions. The process is more detailed and precise than most people realize.

Interest is calculated daily based on the daily closing balance in your account. This means every single day, the bank performs a calculation using that day’s ending balance to determine your interest for that 24-hour period.

The daily interest calculation uses the formula: Annual Interest Rate ÷ 365 days = Daily Interest Rate. Then your daily balance multiplied by the daily rate gives you that day’s interest earning.

Interest is calculated based on the lowest balance present in the account for that specific day. This rule significantly impacts accounts with frequent transactions and explains why timing matters so much.

Daily Balance vs Lowest Balance: What Banks Actually Use

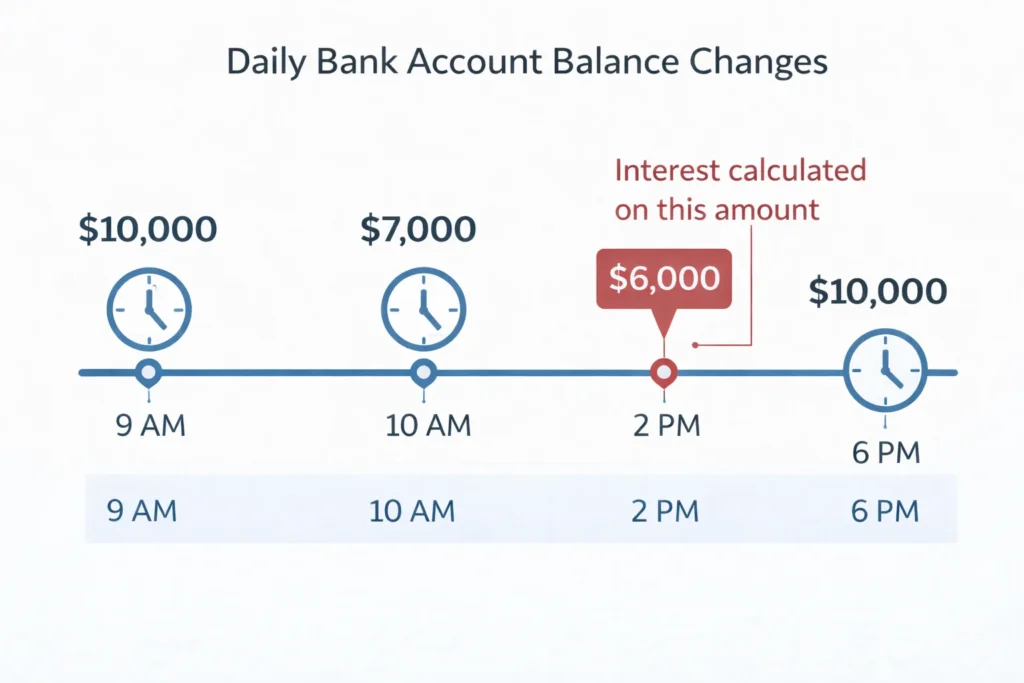

I learned this rule the expensive way. If you have $10,000 and withdraw $2,000 in the morning, then $1,000 in the afternoon, but deposit $4,000 in the evening, your interest for that day gets calculated on $7,000 (your lowest point), not your ending $11,000 account balance.

The higher account balance of $11,000 only starts earning interest from the following day. This means timing your transactions can directly impact your daily interest earnings.

Banks track your account balance multiple times throughout each day to identify the lowest point. This lowest balance becomes the base for that day’s interest calculation, regardless of what happens afterward.

Understanding this rule helped me optimize my transaction timing to maximize interest accrual. I now schedule large withdrawals for late in the day and deposits for early morning.

How Do I Calculate Monthly Interest on My Savings Account

For monthly calculations, I multiply the daily interest by the number of days in that month. If I have $200,000 at 3% annually, my daily interest rate is 3 ÷ 365 = 0.0082%.

One day’s interest equals $200,000 × 0.0082 ÷ 100 = $16.50. For a 30-day month, I’d earn 30 × $16.50 = $495 in interest.

Monthly interest calculation becomes complex when your balance changes during the month. I track each day’s balance separately and calculate daily, then sum up all 30 or 31 days for the monthly total.

The monthly interest calculation method ensures accuracy when your account has deposits, withdrawals, or transfers throughout the month. Daily tracking prevents overestimating or underestimating your actual earnings.

How Do I Calculate Interest Earned on a Savings Account: Real Examples

For monthly interest calculation, I multiply the daily interest by the number of days in that month. If I have $200,000 at 3% annually, my daily interest rate is 3 ÷ 365 = 0.0082%.

One day’s interest equals $200,000 × 0.0082 ÷ 100 = $16.50. For a 30-day month, I’d earn 30 × $16.50 = $495 in interest.

Monthly interest calculation becomes complex when your balance changes during the month. I track each day’s balance separately and calculate daily, then sum up all 30 or 31 days for the monthly total.

The monthly interest calculation method ensures accuracy when your account has deposits, withdrawals, or transfers throughout the month. Daily tracking prevents overestimating or underestimating your actual earnings.

Example 1: Static Balance for Full Quarter

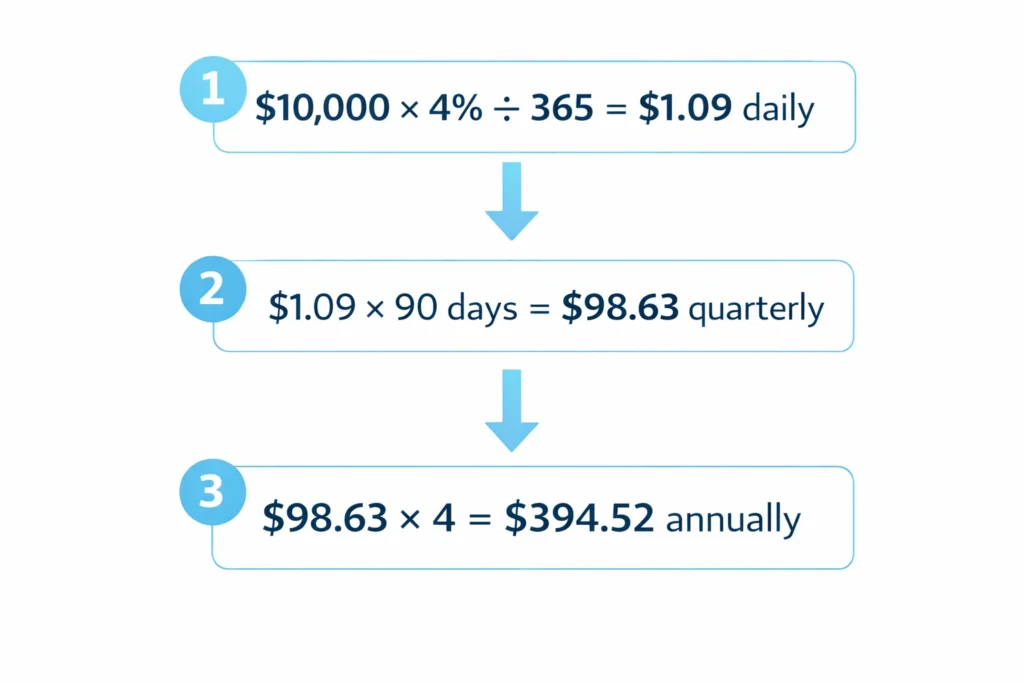

With $10,000 at a 4% annual rate, the daily interest calculation starts with 4% ÷ 365 = 0.01096% daily rate. Daily interest equals $10,000 × 0.01096% = $1.09.

For a 90-day quarter, the total interest earned would be 90 × $1.09 = $98.63. This demonstrates how to calculate annual interest when projected over four quarters ($394.52 annually).

Static balance calculations are the simplest because you use the same daily amount for the entire period. Most savings calculator tools assume static balances, which is why their results might differ from your actual earnings.

I verified this calculation against my own account statement and found it matched within a few cents, confirming the accuracy of the daily calculation method.

Example 2: Account with Mid-Quarter Withdrawal

Starting with $150,000 and withdrawing $50,000 on day 21 creates a two-period calculation. For days 1-20, I earn interest on $150,000. For days 21-90, I earn interest on $100,000.

The first period: 20 days × ($150,000 × 0.01096%) = 20 × $16.43 = $328.60.

The second period: 70 days × ($100,000 × 0.01096%) = 70 × $10.95 = $766.50.

Total quarterly interest: $328.60 + $766.50 = $1,095.10.

This example shows why tracking transaction timing matters. The withdrawal timing directly affects your total quarterly earnings.

Example 3: High-Yield Account Comparison

I compared a $200,000 balance at 3% versus 5% APY to show the high-yield savings account advantage. The 3% account earns $16.50 daily, while the 5% account earns $27.40 daily.

Over 30 days, the difference is $495 versus $822 – an extra $327 monthly just from the higher rate. Annually, this becomes an additional $3,924 in interest earnings.

High-yield accounts use identical calculation methods but offer substantially better rates. The daily compounding on higher rates amplifies returns significantly compared to traditional bank offerings.

This comparison convinced me to move my savings from my traditional bank to a high-yield account. If you want to maximize the benefit of these dramatically better rates, one key step is to save more money each month through expense management, giving you a larger amount to deploy into these high-yield accounts.

Why Your Withdrawal Timing Affects Your Interest (What Banks Don’t Tell You)

One of the most valuable insights I discovered is how transaction timing within a single day impacts your interest calculations. Banks rarely explain this, but it can significantly affect your earnings.

If you deposit money on the 11th day of the month, the interest for that 11th day still gets calculated on the lower previous balance. The new, higher balance only affects the calculation starting from the 12th day.

Interest for that specific day will still be calculated on your lowest point during that day. If you hit $700,000 as your lowest balance, then later reach $1,100,000, you only earn interest on $700,000 for that entire day.

The higher balance of $1,100,000 will only start earning interest from the following day. This rule applies regardless of when during the day you reach the higher balance.

Understanding daily balance impact helps you time transactions strategically. I now schedule large deposits early in the morning and major withdrawals late in the evening to maximize my interest accrual.

Most people don’t realize that the timing of their banking transactions affects their account balance calculations throughout each day. Even transfers between your own accounts can temporarily reduce your interest-earning balance.

This timing effect becomes particularly important for accounts with frequent business transactions or regular automated transfers. Every temporary balance reduction costs you interest for that entire day.

Using Excel to Track Your Savings Interest Like a Pro

After struggling to manually track complex calculations, I discovered that using a spreadsheet as a financial calculator makes the daily calculation significantly easier. This approach helps verify bank calculations and optimize transaction timing.

I track withdrawals and deposits carefully to understand exactly how much interest the bank owes me at the end of the quarter. This method has helped me catch several bank calculation errors over the years.

Creating a savings interest calculator in Excel involves setting up columns for date, balance, daily rate, and daily interest. The formulas automatically calculate everything once you input your daily balances. If you prefer a faster starting point, a free online compound interest calculator can give you a quick projection before you build out your full spreadsheet tracking system.

My interest calculation method includes tracking every transaction’s impact on daily balances. This detailed approach provides accuracy that simple online calculators can’t match.

Setting Up Your Interest Tracking Spreadsheet

I start with columns for Date, Beginning Balance, Deposits, Withdrawals, Ending Balance, Daily Rate, and Daily Interest. Each row represents one day’s calculation.

The daily rate formula is your annual APY divided by 365. For a 4% account, this becomes 4%/365 = 0.01096%. I format this as a percentage with five decimal places. You can also calculate the monthly interest rate by dividing by 12 for quick reference.

Daily interest equals your ending balance times the daily rate. I use the formula =D2*F2 where D2 is ending balance and F2 is daily rate.

My savings interest calculator template includes automatic monthly and quarterly totals. This makes it easy to compare against bank statements and verify accuracy.

I update my spreadsheet weekly with transaction data from my online bank. This regular maintenance ensures I catch any discrepancies quickly.

Verifying Bank Calculations vs Your Calculations

Banks occasionally make calculation errors, and I’ve found several by comparing my spreadsheet results against quarterly statements. The differences are usually small but add up over time.

My method involves using Excel to calculate compound interest daily, then summing monthly totals to compare against bank statements. When differences exceed $5, I contact my bank for clarification.

Tracking for quarterly verification helps ensure you receive all interest you’ve earned. Banks appreciate customers who understand their calculation methods and rarely question reasonable inquiries.

I’ve successfully challenged three bank calculation errors using my Excel tracking data. Each time, the bank corrected the error and credited my account appropriately.

Tax Implications: How Much Interest Do You Actually Keep?

Understanding tax implications dramatically affects your net returns from savings account interest. I learned this when my first large interest payment created an unexpected tax bill.

Under Section 80TTA in India, interest earned up to ₹10,000 annually is exempt from tax. For senior citizens under Section 80TTB, the limit increases to ₹50,000. These deductions only apply if you choose the Old Tax Regime.

US savings account holders must report all interest income on their tax returns, regardless of amount. Interest gets taxed as ordinary income at your marginal tax rate, not as capital gains.

FDIC insured accounts provide deposit protection, but this doesn’t affect tax obligations. All interest earnings from insured accounts remain taxable according to standard income tax rules.

Tax implications vary significantly by country, age, and total income level. High earners in higher tax brackets lose more of their interest earnings to taxes than those in lower brackets.

Net returns represent your actual benefit after taxes. A 4% APY becomes 3% net return for someone in the 25% tax bracket, significantly reducing the account’s true value.

I now calculate both gross and net returns when comparing savings options. The tax implications often make the difference between two accounts larger than the advertised rate difference suggests.

Planning for tax obligations helps avoid surprises during tax season. I set aside approximately 25% of my interest earnings throughout the year to cover tax obligations.

Savings Account Interest Rate Calculation: How to Choose the Best Account

Choosing the best account requires comparing more than just advertised rates it requires you to create a comprehensive plan for your financial goals that evaluates compounding frequency, minimum balances, fees, and access restrictions alongside the interest rates.

I evaluate compounding frequency, minimum balances, fees, and access restrictions alongside the savings account interest rate calculation.

High-yield accounts offer substantially better rates but often come from online banks with limited physical presence. Traditional banks provide convenience but typically offer lower returns on deposits.

The compounding frequency affects your actual returns significantly. Daily compounding grows money faster than monthly or quarterly compounding, even at identical advertised rates.

Adding regular monthly contributions to an initial deposit can significantly boost your total interest earnings over time. The combination of compound interest and consistent deposits creates powerful wealth building.

Online banks typically offer better rates because they have lower overhead costs than traditional banks with physical branches. However, they might have limitations on transaction types or customer service access.

Traditional bank accounts provide full-service banking relationships but often sacrifice interest rates for convenience and comprehensive services.

Comparing Effective Yields: APY vs Compounding Frequency

I compare effective annual rate calculations by determining what each account actually pays over 12 months with identical deposits. Two accounts with the same advertised APY can produce different returns based on compounding period schedules.

Daily compounding typically adds 0.01-0.05% to your effective annual rate compared to monthly compounding. This difference becomes substantial on large balances over multiple years.

The effective annual rate includes all compounding effects and represents your true return percentage. This metric provides the most accurate comparison between different account options.

When comparing accounts, I calculate the dollar difference based on my expected average balance. A 0.25% APY difference on a $100,000 balance equals $250 annually.

High-Yield Online vs Traditional Bank Accounts

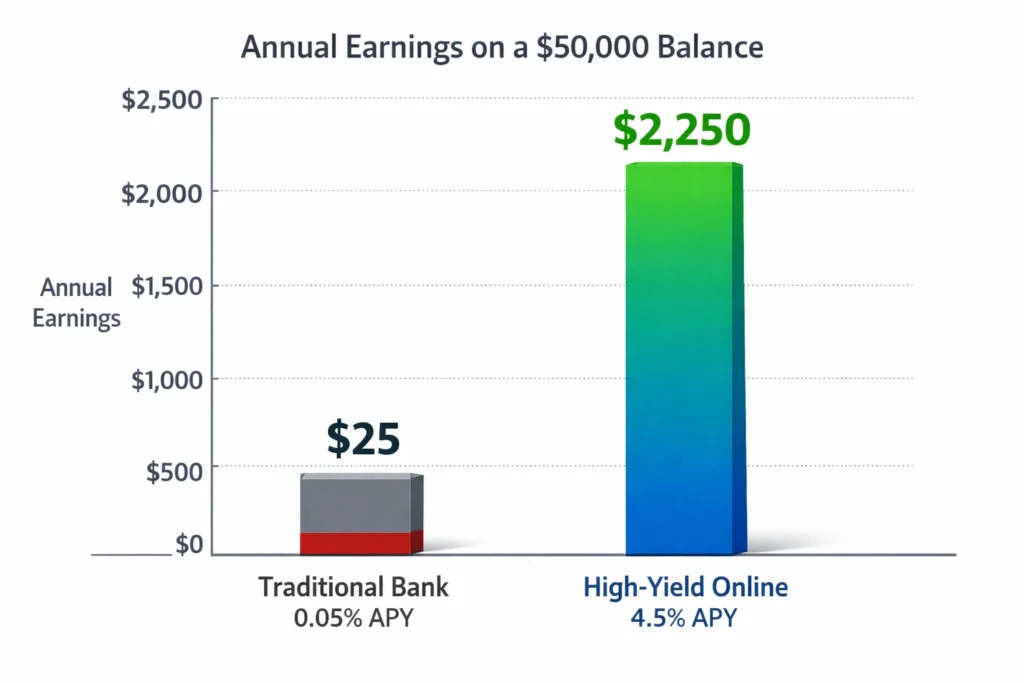

High-yield savings accounts currently offer 4-5% APY compared to 0.01-0.5% at traditional bank options. On a $50,000 balance, this difference equals $1,750-2,475 annually.

Online bank limitations include potential delays for certain transactions, limited ATM access, and no physical branch support. However, most online banks reimburse ATM fees and provide excellent digital customer service.

Certificate of deposit (CD) rates often exceed savings account rates but require locking your money for specific periods. Money market account options provide checking-like access but often require higher minimum balances.

I maintain accounts at both online bank and traditional bank institutions to balance maximum returns with full banking convenience.

This savings strategy provides the best of both approaches similar to how budgeting-in-small-business principles teach resource allocation across different uses, you can allocate your savings across different account types to optimize both returns and access.

Common Mistakes That Cost You Money (And How to Avoid Them)

Through years of tracking my own accounts and helping others with their calculations, I’ve identified several costly mistakes that most people make without realizing it.

Assuming all savings accounts use simple interest when most use compound interest leads to underestimating your actual returns and growth potential. This mistake causes people to undervalue the power of compound growth.

Not tracking the lowest daily balance when calculating expected interest results in overestimating earnings when account balances fluctuate frequently. This creates disappointment and confusion when statements don’t match expectations.

Choosing accounts based only on APY without considering compounding frequency misses potentially better returns from more frequent compounding schedules at slightly lower advertised rates.

Many people ignore minimum balance requirements and monthly fees, which can eliminate interest earnings entirely. A $12 monthly fee on an account earning $15 monthly interest destroys most of your returns.

Timing large transactions poorly can cost significant interest earnings. Making major withdrawals early in the day or deposits late in the day reduces your daily interest calculations unnecessarily.

Failing to understand tax implications leads to overestimating net returns and poor account selection decisions. The after-tax return is what actually matters for financial planning purposes.

Not comparing total relationship costs including fees, minimum balances, and access limitations causes people to focus only on interest rates while ignoring other important factors.

I now evaluate every aspect of account terms, not just the advertised APY. This comprehensive approach has saved me hundreds of dollars annually in fees and lost interest earnings.

My savings strategy includes tracking all account costs and [optimizing transaction timing to maximize net returns] while also focusing on reduce your monthly expenses, because these practices significantly improve actual earnings compared to casual account management. These practices significantly improve actual earnings compared to casual account management.

Start Calculating Your Savings Growth Today: Action Steps

Now that you understand how to calculate interest on savings account, it’s time to apply this knowledge to your own financial situation. I recommend starting with these specific steps based on what I’ve learned works best.

Begin by gathering your current account statements and identifying your actual APY, compounding frequency, and fee structure. This baseline information is essential for accurate calculations and meaningful comparisons.

Calculate your current daily interest earnings using the formulas I’ve shared. Track your account for one month to verify your calculations match your bank’s statements.

Research high-yield alternatives and compare their effective annual yields using the calculation methods I’ve outlined. Focus on accounts that match your banking needs while maximizing returns.

Set up an Excel tracking spreadsheet if you have frequent account activity or large balances where small differences matter significantly. Regular reviews help ensure you’re maximizing your earnings.

These entries usually appear in your bank statement at the start of a new quarter, making it easy to verify your calculations and track your progress over time.

Consider opening accounts at multiple institutions to take advantage of different benefits while maximizing your overall savings growth. This strategy requires more management but can significantly improve your savings growth.

Regularly check your accounts to ensure they still align with your financial goals as interest rates and your circumstances change over time.

Your understanding of interest calculation gives you the power to make informed decisions about your money. Use this knowledge to optimize your savings strategy and build wealth more effectively.

Start implementing these concepts today. Even small improvements in your savings approach compound significantly over time, just like the interest we’ve been calculating.

Frequently Asked Questions

How often is interest calculated on savings accounts?

Interest is calculated daily based on your end-of-day balance, but credited to your account monthly, quarterly, or semi-annually depending on the bank. The daily calculation ensures you earn interest on compound growth, even though you don’t see daily additions to your balance.

Why does my actual interest differ from what I calculated using the annual rate?

Banks calculate based on your daily lowest balance, not average balance, and account for every deposit/withdrawal timing. Fluctuating balances significantly impact quarterly totals because each day’s interest depends on that specific day’s lowest balance point.

Should I withdraw money at the beginning or end of the day to maximize interest?

Withdraw as late in the day as possible since interest is calculated on the lowest balance point during that day. Morning withdrawals reduce your entire day’s interest calculation, while late-day withdrawals minimize the impact on your earnings.

Can I use Excel to track my savings interest calculations?

Yes, create a spreadsheet with daily balance entries and apply the daily interest rate formula. This helps verify bank calculations and optimize transaction timing. I use this method to catch calculation errors and maximize my returns.

What’s the difference between APY and APR for savings accounts?

APY includes compound interest effects and represents your actual annual return. APR is the simple annual rate without compounding. Always compare APY when choosing accounts because it shows your real earning potential.

How much savings interest is tax-free?

This varies by country and age. In India, ₹10,000 annually is tax-free for general public, ₹50,000 for seniors under specific tax regimes. In the US, all interest income is taxable. Check local regulations for your specific situation.

Do high-yield savings accounts calculate interest differently?

No, they use the same calculation methods but offer higher rates. The daily compounding on higher rates significantly amplifies returns over time compared to traditional accounts. The math is identical, but the results are dramatically better.