How to Pay No Taxes on Rental Income: 9 Legal Strategies for 2026

The one issue I’ve been working on for years is the rental property tax strategy issue and the overwhelming question I hear is always some version of this: can you collect the rent every month and pay nothing in the end of the year to the IRS? Yes. You can. The idea of not paying taxes on rental income legally is not some form of cheating.

It is about applying existing provisions in the tax code that Congress has already established to motivate the investment in housing. Landlords are the ones who are getting the short straw. Most just don’t know how.

One of the few types of passive income where the tax code is actually on your side is rental property investing. Learning how to pay no taxes on rental income through deductions, depreciation, and strategic planning can completely change the way investors build wealth. And these benefits can apply whether you own a single rental property or a portfolio of one hundred.

The Landlord’s Paradox: How You Can Make Money While Paying Zero Taxes

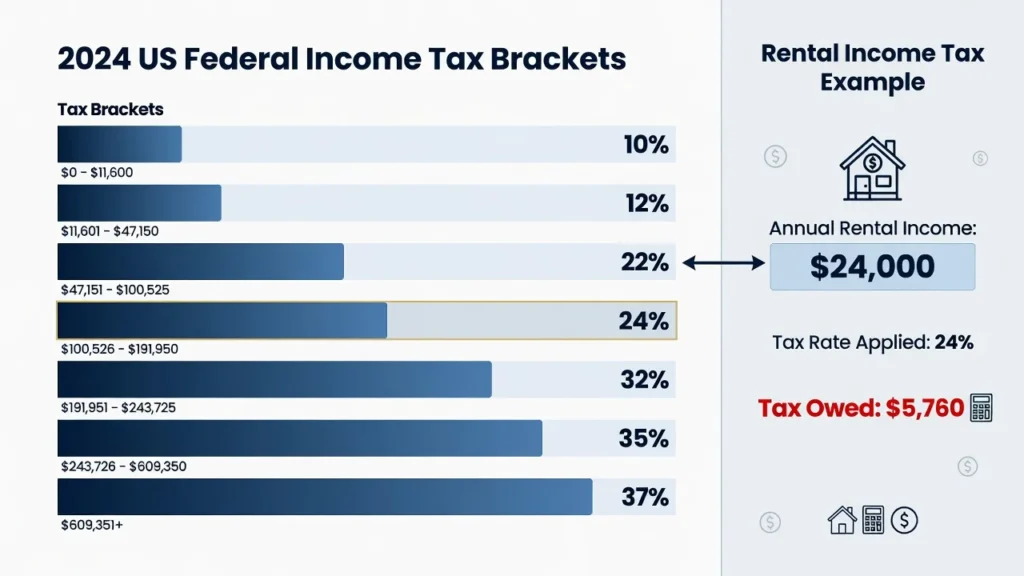

Rental income falls under the category of taxable rental income, and is taxed at ordinary income tax rates, which include the rates of your paycheck. For the majority of landlords, that’s the federal rate of 22 percent to 37 percent.

If the property is earning $2,000 a month, then that’s $24,000 in gross rent that may be subject to the tax. When you calculate your gross monthly income from all sources including rental properties, this additional revenue pushes you into higher tax brackets. The federal tax bill by itself is $5,760 at 24% before deductions, strategies, and planning.

According to a report by HMRC (His Majesty’s Revenue and Customs) in 2023, UK landlords made a total of £1.8 billion in tax errors that year, highlighting the prevalence of tax errors among owners of rental properties. The US pattern is virtually assured to be similar. Landlords are leaving real money behind, or even worse, paying taxes that they didn’t even have to pay.

Is It Legal to Pay Zero Taxes on Rental Income?

Yes, absolutely. All strategies in this article are based on the tax code in the USA. The answer to how to avoid paying taxes on rental income is, as it turns out, easier than most people think:

Congress intentionally created these provisions to help stimulate investment in rental properties. But when private investors provide housing, there are communities to benefit from and there are tax advantages for the government. There is no hidden, no obscure. It is only underutilised.

Understanding Your Rental Income Tax Rate (And Why Most Landlords Overpay)

Unlike qualified dividends, there is no special low tax rate for rental income. The IRS considers it ordinary income tax, which is the same kind of income as on your paycheck.

It is an addition to all your earnings and your combined adjusted gross income is what determines the bracket you will fall into. When you are a teacher making $60,000 and your rental gross is $12,000, that additional income will take you from the 22% into the 24% bracket – which is more than you may think!

The positive thing about it was that Congress didn’t end there. It added deductions, depreciation provisions, and loss provisions that were particularly tailored to minimize that taxable rental income, even to extinction.

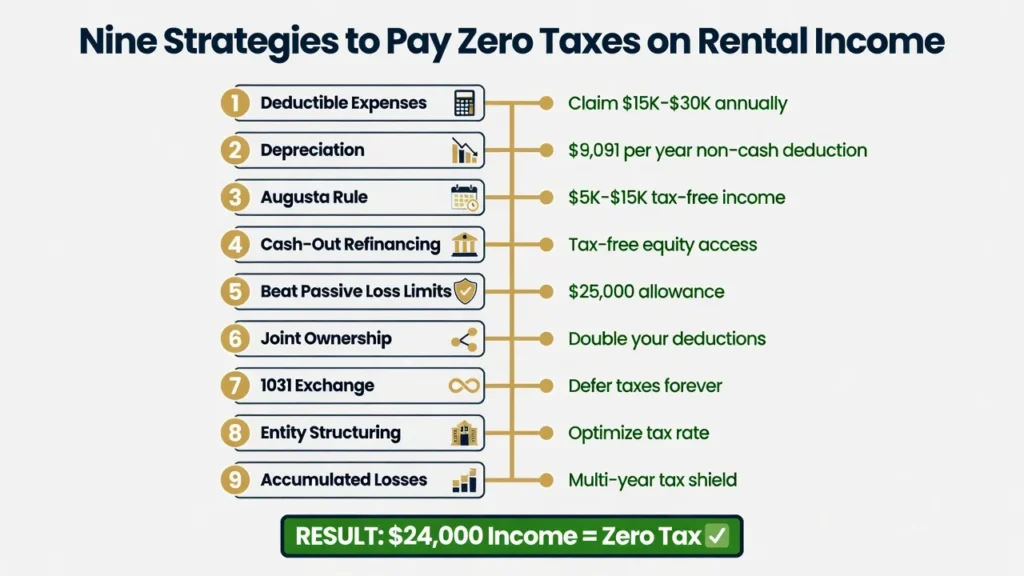

Strategy 1: Claim Every Deductible Expense (Most Landlords Miss Half of These)

My first tip for advanced strategies is to begin with the basic ones first. Landlords can claim a wider tax deduction on their rental income than is widely thought, especially when treating your rental property as a business with systematic expense tracking. Every dollar in costs associated with owning a rental property will offset your taxable income.

Many landlords are claiming the obvious rental property write-offs and not getting hundreds or thousands in other write-offs annually. This is the first and foremost step when it comes to getting it right.

The Big Three: Mortgage Interest, Taxes, and Insurance

Most landlords will have the mortgage interest deduction as their largest single deduction. On a $300,000 loan at 7%, your first-year interest is approximately $20,700. With a 22% tax rate, that single deduction can save you about $4,550 in federal income taxes. At 24%, it saves $4,968. The figures are important and build up over time in the property.

100% of the rental property tax is deductible. The cost varies from location to location, from about $3,000 to $8,000 or higher per year. There are also full tax deductions for insurance premiums, such as landlord liability insurance and property insurance. Each of these three categories can be a significant portion of the deductions on a mid-range rental property, and can contribute $25,000 or more in annual deductions.

Operating Expenses Most Landlords Forget

All renter tax deductions are considered landlord expenses and can be deducted on your tax return. If the manager receives 8% to 10% of your rents, then every dollar that you pay to the manager is a dollar that is deducted from your taxable income.

Here are some landlord tax deductions that many investors overlook:

Vacancy fees, Zillow fees, signage.

Professional attorney fees for preparing the lease, CPA fees for preparing taxes.

Landlord software subscriptions like Stessa, Buildium, and AppFolio are essential tools for tracking every monthly expense systematically throughout the year. Even the fees you pay on your dedicated rental account are deductible.

Travel costs flights and hotel when managing out of state properties

Education – books, courses, and seminars which are directly related to your rental business.

One of the least used of all these deductions, it is one of the most straightforward business expenses to claim for a rental property with little effort by using the right rental property tracking app. IRS business trip standard rate for 2024 is 67 cents per mile (inspections, meetings with tenants, supply runs). If he takes 20 trips a year that are 15 miles long, then he spends $201 per year.

When you put it in the context of a 10-year portfolio with a number of properties, it really begins to mean something. Consider using a simple spreadsheet log or MileIQ. Write the date, destination and purpose for each journey. This is the only documentation you’ll need.

Repairs vs. Improvements: The Critical Tax Difference

One of the most useful and applicable tax rules that landlords should know is the difference between repair and improvement. A repair will keep the property in the same state, and you will deduct the entire amount in the year that the payment is made.

Repairs include a broken boiler, leaking roof patch, repainting between tenants. An improvement adds value or extends useful life, therefore is capitalized and depreciated over time. It’s important to note that the IRS Tangible Property Regulations offer specific guidance on this issue and your CPA should make sure that any major project is explored before categorization is considered.

Replacement of Furnishings and Appliances

A lot of landlords either deduct the costs of furniture when it’s first furnished (not permitted) or forget to claim the replacement deduction when the furnishings get used up and need to be replaced (a real money-lender).

The rule is you don’t get to do any of the deductions on year one of a rental property. So, if you replace an old refrigerator in the 5th year, the replacement cost is an allowable expense. Save receipts for all appliances and furniture items replaced. Deductions have value if they are held for multiple years.

Home Office Deduction for Landlords

If rentals are managed from a separate work space within the home, you might be eligible for the home office deduction. The simplified method lets you deduct $5 for each square foot of the home, up to a total deduction of 300 square feet, or $1,500 annually. The true actual cost that is incurred

Strategy 2: Depreciation The Non-Cash Expense That Wipes Out Rental Income

There is one type of real estate investing strategy that truly makes a seasoned investor stand out against everyone else, and that’s depreciation for rental property. This one non-cash expense can literally make a roaring property a paper loss on your tax return without legally losing anything! and it’s no cost to you whatsoever.

There isn’t any other deduction that has a more regular effect, year after year. I have seen landlords lose thousands of dollars in depreciation because they forgot that depreciation was not possible for land. This is the logic the IRS wants to use.

How Depreciation Works: The IRS Logic

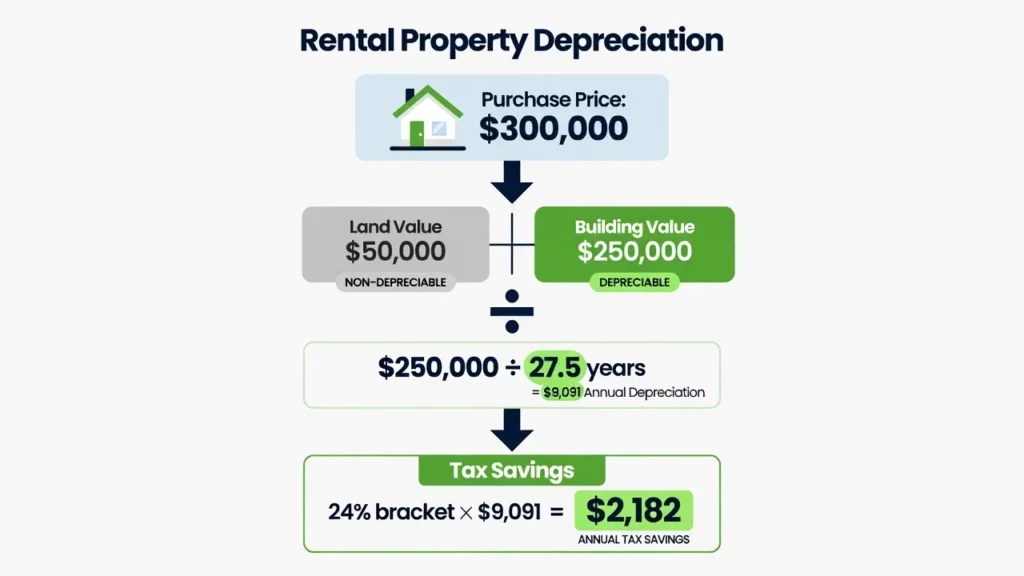

The IRS has the common sense that a residence rental property gets worn down and needs to be replaced. Instead of overlooking this fact, the tax code allows for a systematic deduction over 27.5 years. All landlords need to bookmark Publication 527 (Residential Rental Property) that is published by the IRS.

The rule is to only depreciate the building, not the land. If you buy a $300,000 house, you have to consider the dollar value put into the property, and the dollar value put into the land under it. Typical amounts could be $250,000 for the structure and $50,000 for the site. The $250,000 is the only amount that is depreciable.

The Real Numbers: How Much Depreciation Saves You Each Year

Annual depreciation on that $250,000 building: $250,000 ÷ 27.5 = $9,091 per year.

That one non-cash deduction will save you $2,000 in federal taxes each year at the 22% Federal tax rate. At 24%, it saves $2,182. In the 10 years that it took to save that much, the federal tax savings totaled $20,000 to $21,820, all on a no-cost basis.

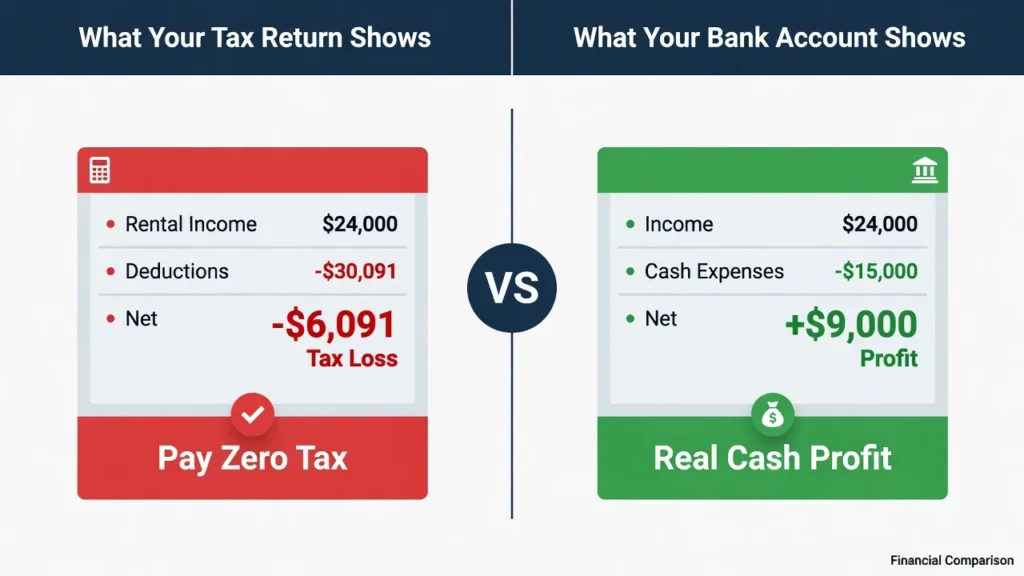

The secret is how you add depreciation to your operating expense deductions. Even if you cash flow positive, a property that brings in $28,800 in annual rent could indicate that you have a tax loss of $6,000 and even more after all deductions. This is what paper loss rental property owners do and that is completely legal.

Cost Segregation: Accelerate Depreciation by Five to Seven Years

Standard depreciation is calculated over a 27.5 year period. Cost segregation expedites it significantly by shifting the recovery periods of its components to shorter periods.

Cost segregation studies are conducted under the IRS’ MACRS system, which determines the recovery periods for various types of property. A qualified engineer will determine which components can be recovered in 5, 7 or 15 years instead of the 27.5 years. Typically, flooring, fixtures, landscaping and some electrical items qualify.

The cost of a cost segregation study generally ranges from $5,000 to $15,000, but will quickly recoup its cost on properties valued at more than $200,000. The tax break in the first year can be extraordinary when bonus depreciation is added to the reclassified parts (see next section).

Bonus Depreciation: Act Fast Because It Is Phasing Out

Bonus depreciation lets you claim 100% of the cost of qualifying property in the year the property is acquired, instead of over the recovery period. When the first-year deduction is added to a well-structured acquisition, the total can be massive.

It matters when and it’s chipping away. Congress originally scheduled to start the phase-down of bonus depreciation in 2023, but enacted the Tax Cuts and Jobs Act of 2017 which establishes an accelerated phase-down for bonus depreciation, bringing it down to 40% in 2018 and 20% in 2019 before the 100% threshold is reached in 2022. The schedule as originally written dropped to 60% for 2024, 40% for 2025, 20% for 2026, and 0% from 2027.

Congress has, however, indicated it would like to change or extend these phase-outs before final decisions are made based on the bonus depreciation percentages. The optimum time for maximum benefit could be opened, closing or re-opening depending on when you read this.

What Happens When You Sell: Depreciation Recapture Explained

Depreciation cannot be given without any cost. The IRS gets back the depreciation deduction taken at 25% of the maximum, in addition to the capital gains rate when you sell. The recapture tax on $90,000 in accumulated depreciation over 10 years could be $22,500.

That is why the more successful real estate investors seldom sell their investment real estate directly. There is no doubt that the tax price of a direct sale is nearly always higher than the alternatives. In the following pages, Strategy 7 (the 1031 exchange) is devoted to the details of how to indefinitely postpone capital gains tax and depreciation recapture.

The Cash Flow Paradox: Make Money and Show a Loss

You left with actual cash in your hands, no tax bill due to the IRS. That’s a paper loss rental property owners come up with without hiding anything, without playing the system. This is tax code in action, as designed, and it is within the reach of all landlords who know how to use it.

Strategy 3: The Augusta Rule Rent Your Home Tax-Free for 14 Days

This is a real lost opportunity as few landlords have heard of it. The Augusta Rule rental property provision (Section 280A(g) of the tax code) lets you rent out your primary home or vacation home for up to 14 days of the calendar year and avoid paying any taxes on the income. It’s not reported. It is not taxable. It just isn’t there in the eyes of the IRS.

How the 14-Day Rule Works

The IRS rental day vs personal use day rule is a hard and fast rule. If you rent a day, it’s a “rental day.Every day that rent is charged is a “rental day. Each day that you or a family member use the property (even for short periods) is a personal day. The 14-day rental window is valid for the number of days of the rental, only. If you remain in it, you will not incur any additional tax on this income.

An important consideration to keep in mind: Rental-related expenses cannot be deducted while the property is being rented out since they are being deducted as one of the homeowners (as mortgage interest, property taxes). The Augusta Rule is not a policy to “stack” deductions.

Real-World Examples and Income Potential

The Augusta Rule is named after Masters golf tournament week, held in the town of Augusta, Georgia, where residents in the region had traditionally been able to rent out their homes to golf fans at high prices.

A home near a major sports venue can rent for $5,000 to $15,000 for this championship game weekend a fair market rent for a three night stay over a championship game weekend and all of the rent is tax-free under the 14-day rule.

Other high-value opportunities:

By a large university: Rental charges for graduation weekend may be $3,000 – $6,000.

Near a conference center: weeks of trade shows are steady demand.

Beach or ski properties: peak holiday weeks can see prices go from 3x to 5x the normal rate for vacation rentals.

City properties at major events: concerts, political conventions or marathons

Documentation Requirements and Audit Protection

The IRS rarely audits Augusta Rule claims but, when it does, having documentation is key. To protect yourself:

Sign a rental agreement – even a one-page document – for each trip

Take payment in a traceable manner: check, bank transfer, or Venmo/Zelle including a memo

Charge fair rental value: based on the fair market rent, similar to other verified short term rentals in the area, on comparable dates and conditions. The safest way to record this is to use the data from Airbnb or VRBO service for your market.

Maintain records of renters, dates of rent, and renter fees

No more than 14 days per calendar year.

Augusta Rule for Business Owners: An Advanced Application

Owners of businesses have a specific application of this rule. You may be able to rent your own home for meetings, retreats, or team events and get paid a maximum of 14 days of rent per year on your business entity’s books, without having to pay taxes on this income to you personally, and you can deduct the rent expenses from your business taxable income.

This means that there is a “clean” income change that includes a business expense deduction on one hand and income that is not subject to tax on the other. Talk with a CPA before putting this plan into place to make sure that the rental agreement and business purpose paperwork are airtight.

Strategy 4: Cash-Out Refinancing Pull Equity Tax-Free and Increase Your Deductions

This strategy involves cashing out of a home to use for other purposes, but simultaneously getting more tax deductions. This strategy involves cashing out of a home for another use, but simultaneously generating more tax deductions.

This is one thing I have seen that most real estate investors don’t associate with their taxes. If the investment property appreciates in value or its value is increased following renovation (adding value), it is possible to refinance the investment property to remove some of the value ( Equity ) without it being classed as a taxable event.

Why Debt Is Better Than Sale for Tax Purposes

If you sell, you will incur 15% – 20% capital gains tax on the profit on the sale of the property plus 25% depreciation recapture on the depreciation you claimed. If you pull out equity from your home it is considered cash in hand and you don’t owe any taxes. None.

The downside is that they will be saddled with greater debt and interest payments on a larger amount. That interest is tax-deductible, however. The sum of the capital gains taxes and capital gains depreciation recapture taxes owing on a direct sale is usually significantly higher than the interest expense on borrowing against the same equity.

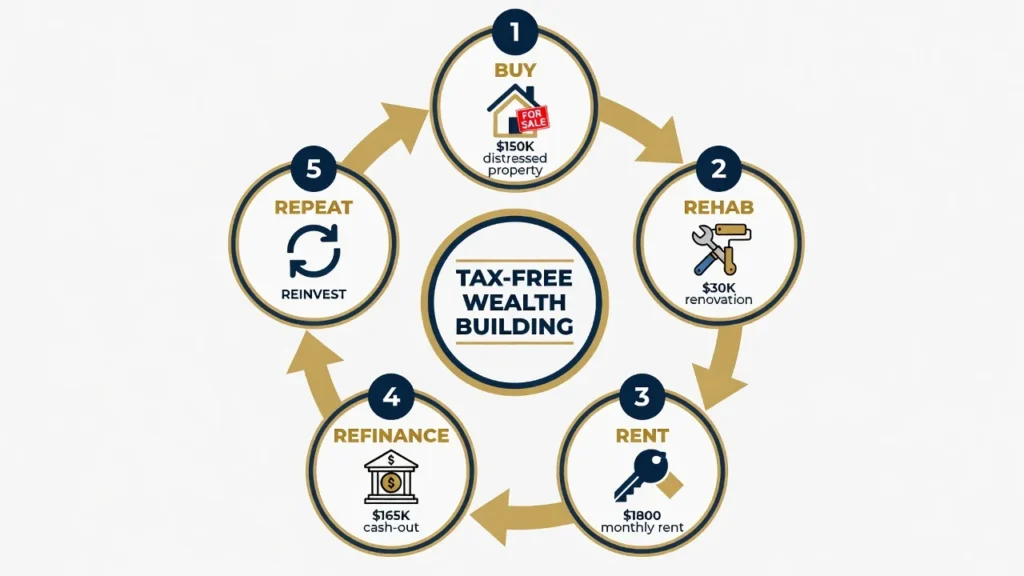

The BRRRR Strategy: Building Wealth Without Selling

Cash-out refinancing in real estate investing is the structured application of the BRRRR strategy – Buy, Rehab, Rent, Refinance, Repeat.

In practice, the answer is as follows:

Purchase the distressed property at a discount price.

Rehabilitate it to rentable condition Rent it out and make it an income.

Refinance on new, higher appraised value

Get the equity and apply the same steps to the next house.

A home that was bought for $150k and upgraded to the appraised value of $220k enables the cash-out refinance for $165,000, avoiding any tax implications. With the rental, you pay off the new debt until you can get it paid back.

Banks vs the IRS: Two Different Scorecards

Your tax return is based on the logic of a different nature than your mortgage application. You can have a loss on your tax return, but a profit in your bank account. Banks are interested in your rental income less actual cash expenses. It doesn’t take depreciation into account. Tax losses are good for you – they reduce taxes, and cash flow is good for bank approval. Knowing both provides you with a huge strategic edge.

The most successful investors do the opposite of what is simple: they borrow against their assets as opposed to selling them. Each sale involves a capital gains tax and depreciation recapture. Each refinance provides cash and doesn’t result in any tax savings, but does result in greater deductible interest payments in the future.

This isn’t limited for the very rich. A cash-out refinance is a strategy that any landlord with an appreciating real estate investment can use to access the equity of the property without tax consequences, then use that capital to invest in another property. The math functions behave the same at $200,000 as they do at $20 million.

Strategy 5: Passive Activity Loss Rental Property Rules And How to Beat Them

Many landlords with a W-2 earning job find themselves hitting a roadblock when it comes to passive activity loss rental property rules. IRS regulations define rental losses as passive losses and thus allow them to only offset passive income, not wages or active business income. If you have a $15,000 loss on your rental property and earn a $120,000 income from your job, the $15,000 loss will not offset the income taxes on your $120,000.

That’s where I’ve seen the most frustration with landlords who have W-2 jobs. They discover that their rents are to be withheld, and question the value of the strategies. Yes, they are but you must learn the rules first. The difference between a passive income versus an active income and the exceptions make all the difference.

Why Your Rental Losses Might Not Reduce Your Tax Bill

The passive activity rules of the IRS (Section 469) deem rental activities to be passive income, no matter how much time you invest in them, unless you meet certain requirements. Passive losses are only tax deductible against passive income.

If your rental properties are your only passive income, and you have a combined loss on them, the loss is suspended and will be carried forward to later years. The losses are suspended and do not go to waste. They are added to your tax return, offsetting future passive income or released in full at the time of sale. Imagine them as a tax savings account that is growing over time.

The $25,000 Special Allowance and Its Income Limits

The $25,000 exception provides a practical tax-saving benefit for the active landlords who have rental losses. The full allowance applies to your modified adjusted gross income (MAGI) being below $100,000. The allowance decreases by 50 cents on every $100,000 MAGI above $100,000 and ends at $150,000 MAGI unless you are a real estate professional.

You have to be actively involved in managing the property to be eligible for the $25,000 exception, which includes making decisions about it, like approving tenants, establishing rents and authorizing repairs. It is not necessary to do the work physically. As long as you still have the ability to make decisions on the property, it is okay to use a property manager.

Real Estate Professional Status: The Ultimate Strategy for High Earners

There are two requirements that must be satisfied to be a real estate professional:

There are two requirements for a real estate professional: First: 750 hours or more of activities in real property trades/businesses in which you materially participate per year. Second: The real estate activities must constitute over 50% of your total working time for the year.

The 50% test is the one that is tough to pass for those who have full-time jobs. You would have to work over 2000 hours for your boss the equivalent of more than 2000 hours in real estate, which is difficult to imagine when you’re on a 40-hour work week. The most attainable form of real estate professional status is for individuals who have retired from, or are part-time employees in, traditional jobs, as well as for individuals whose spouses are real estate professionals while filing jointly.

In addition to these qualifying tests, you must also show that you have participated materially in each individual rental unit a separate, but related requirement addressed in the next section.

Material Participation Requirements

The term material participation means you are involved in the activity on a regular, persistent and significant basis. The IRS has seven tests and if you pass any one of them you qualify. The most commonly used:

Self Test: You conducted at least 500 hours of services in the activity during the tax year.

No one else did more: You worked 100 hours and possibly more hours than anyone else

There was a high level of your participation in the activity: Substantially all

There is also an election to group together all rents as one activity for material participation. This results in a much easier hour threshold in a portfolio.

Who Should Pursue Real Estate Professional Status?

Real estate professional status is an important designation that has real consequences. The most appropriate people for:

If passive income is suspended entirely for you (with high income), you can adjust your withholding taxes accordingly.

Anyone who has big cost segregation losses, meaning that they have big depreciation losses on paper, Spouses of high income earners that can qualify on their own hours during a joint filing

Those who are already spending the time necessary as a full-time real estate developer or investor

When your rental losses are relatively small and your income is less than $150,000, you may be better off claiming the $25,000 special allowance and it is easier to do.

Strategy 6: Joint Ownership Double Your Deductions, Split Your Income

Married individuals who own rental property may be missing out on large tax savings by being the sole owner of the property. When you add a co-owner, rent income and deductions are divided differently on your tax return, and in many situations will keep both you and your co-owner in lower tax brackets and provide double the opportunity for some deductions.

Note: The international examples below in the subsections show the common sense of income-splitting. Each country has different amounts of deduction. For the United States, you just need to verify what the deduction amounts are with a certified public accountant (CPA).

How Joint Ownership Changes Your Tax Picture

In the U.S., each co-owner would own the income and expenses on Schedule E based on their percentage of the business. Adjusting the effective tax rate on rental income can be significantly reduced when the income is shared between two taxpayers with varying or staggered income levels.

A landlord with an income of $180,000 from his or her job would place all of the rental income ($24,000) in the 32% tax bracket, and would owe $7,680 in federal tax on the rental income alone. Their spouse earns $45,000. If the property is jointly owned and the $24,000 is divided equally then each reports $12,000. The higher earner pays 32% and the lower earner pays 22%. Federal tax on rental income: $6,000.Income tax on rental income at the Federal level: $6000. That’s a one-time annual savings of $1200 just because of the way they’re owned.

Doubling Your Deductions

Each co-owner in the US reports their share of the income, and can apply their own deduction thresholds. In other tax systems, it works in reverse – for instance, in India and UK, each co-owner takes each’s own standard deduction and home loan interest allowance, thus significantly reducing the total tax liability. The basic idea is so simple:

If the two taxpayers have different tax brackets, they will have a lower effective tax rate.

The Bracket Arbitrage Strategy

If one spouse falls into the 22% bracket and the other spouse falls into the 12% bracket, then the income from the rental property is taxed at the lower rate of 12%. This is legal it simply shows the legal ownership of the property. The income is declared in accordance with the ownership, and both spouses report on the income truthfully.

Rental income that is directed to the lower earner (parental leave, sabbatical, etc.) is taxed at a lower rate in that year than it would be in any other year. Discuss allocations of ownership with your CPA each year.

How to Re-Title Property and When It Makes Sense

The cost of adding a spouse is $500-$2000 and is done with a quitclaim deed (which requires an attorney). It pays off right away if the first year tax savings are greater than that, which many times they are. Compile and run the numbers in conjunction with your CPA.

Before re-titling, contact your mortgage company if there is a mortgage on the property. Some lenders are “owner-sensitive” and will require the refinance when the ownership changes, increasing costs and complexity that can alter the equations.

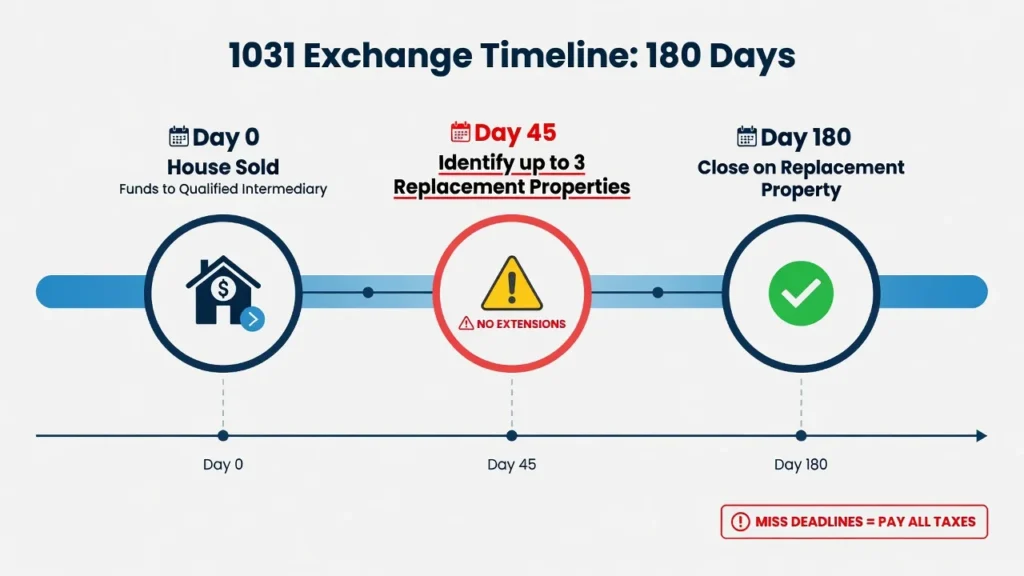

Strategy 7: The 1031 Exchange Defer Taxes Indefinitely When You Sell

As a general rule, you’ll be subject to a 15% to 20% federal capital gains tax rate plus an additional 25% capital gains tax for any depreciation that you claimed in prior tax years. But with a 1031 exchange, you can package up that entire capital gains tax bill (plus depreciation recapture) to go into a new like-kind property. This can be repeated ad infinitum if done properly.

How 1031 Exchanges Work

The rules are clear and the time limits are rigid:

Immediately sell your home and leave the funds in a qualified intermediary (the funds cannot be touched by you).

Identify replacement property within 45 days of closing of the sale you can identify up to three properties.

Complete the closing of the replacement property within 180 days of the original closing.

All the taxes are deferred until the property is replaced with a property of equal or greater value.

Properties must be like-kind: investment property exchanged for investment property residential for residential, commercial for commercial, or residential for commercial.

The qualified intermediary cannot be negotiated. The exchange fails if the proceeds of the sale are received in your bank account at any time, and the sale’s tax bill is now due.

The Tax You Are Deferring

The figures on this common exchange accurately narrate it.

Property purchased for $200,000, sold for $400,000 after 10 years.

Accumulated depreciation: $72,727.

Without a 1031 exchange: Capital gain of $200,000 at 20% federally = $40,000

Depreciation recapture of $72,727 at 25% = $18,182

Total tax due: $58,182 With a 1031 exchange: $0 due at sale. This $400,000 is in full use on the next home.

The Infinite Deferral Strategy

There is no limit to the number of times you can use the 1031 exchange; hence its name “infinite deferral. Buy a property. Appreciate it. Move up to a bigger home. Repeat for 30 years. Under current law, the appreciated value of the property is passed on to your heirs at death with a stepped up basis so that they do not owe any tax on the value of the property at the time of your death.

One investor of experience said to me: “I have never paid capital gains taxes. All I am ever realizing is being reinvested in my portfolio.

Common 1031 Mistakes to Avoid

There are no extensions for the 45 day identification period, no matter what the situation is.

Conditions where the proceeds are touched prior to the exchange finishing.

To exchange for another property of lower value (you will have to pay tax on the difference or “boot”)

Using a disqualified intermediary the QI cannot be your attorney, CPA, real estate agent, or anyone who has worked for you in the past two years

Not reinvesting all proceeds including any equity generated through debt pay down.

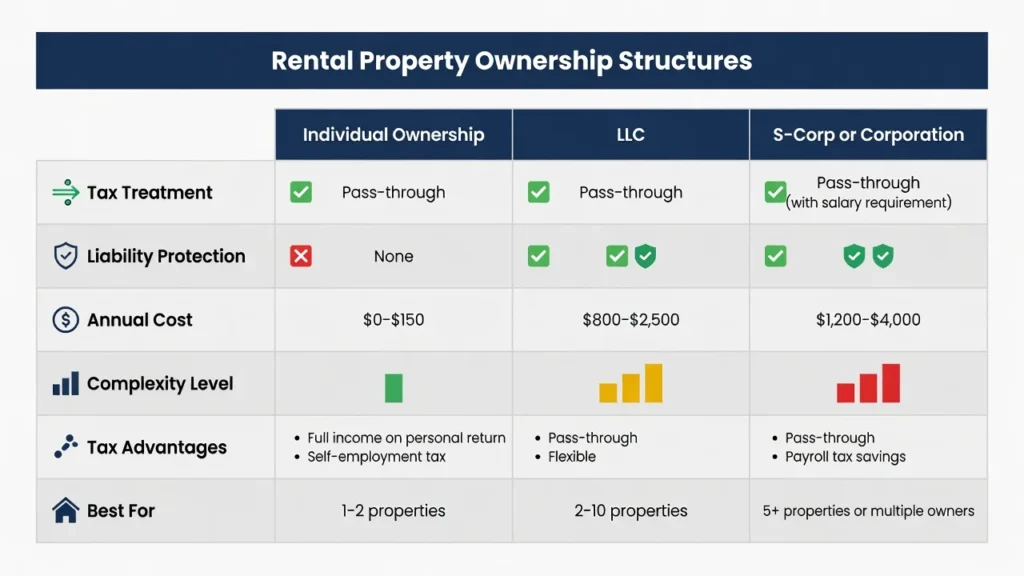

Strategy 8: Entity Structuring LLC vs. Individual Ownership

Every serious real estate investor will eventually have to choose between personally owning their rental properties, owning them in an LLC or a corporation. The entity structure you select affects not only your tax treatment but also requires creating a formal budget for your rental business with separate accounting systems and financial tracking.

This structure is also a factor when determining eligibility for the qualified business income deduction under Section 199A, making it worthwhile to consult with a CPA about your real estate business.

Individual Ownership: Pros and Cons

Most landlords start here. Individual ownership will involve the property being registered in your name and declared on Schedule E and taxed at your personal income tax rate. Cons: No formation costs, no mortgage interest deduction, easiest financing, simplest set up. Cons: no separation between personal and business finances, all income taxed at your marginal rate, and personal liability exposure in case a tenant sues you.

LLC Ownership: Liability Protection Without Tax Change

A single-member LLC is not a separate entity for federal tax purposes – it does not alter how rental income is taxed in any way. Just like with individual ownership, the LLC distributes income to you. It offers you certain liability protection between your home and your rental property.

Every state has its own set of LLC maintenance fees for the year. California franchise fees for LLCs cost California landlords more than other states, at $800 per year. If you and your spouse, partner or investor form a multi-member LLC, the LLC is taxed as a partnership, and you will need a separate tax return (Form 1065), which costs an additional $500 to $1,500 per year.

S-Corp or Corporation: Lower Rates but Greater Complexity

On paper, having property in a limited company can be very tax attractive for a higher-rate individual taxpayer. However, if these profits are withdrawn as dividends or salaries, they’ll again be taxable as personal income. The net rate (corporate tax plus dividend tax) is frequently not all that different from the individual rate anyway, and you’ve incurred an extra $2,000 to $5,000 in annual accounting expenses. Don’t assume that the corporate structure will save you money – run it with your CPA.

When to Use Each Structure

Individual: 1-3 properties, moderate income, simple tax situation

LLC: Any landlord that is worried about potential liability which should be every landlord.

If you have multiple real estate properties, high income, and a CPA that has a specialization in real estate entity structuring, then you should consider an S-Corp or corporation.

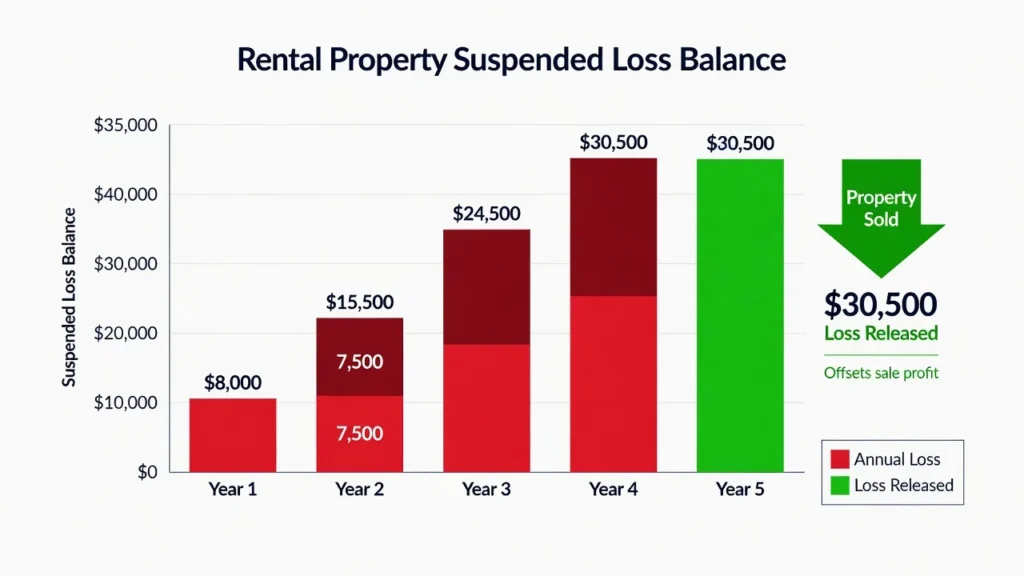

Strategy 9: Accumulated Losses : Your Multi-Year Tax Shield

It doesn’t happen all at once when you file a single tax return, but takes years to occur, and it’s one of the least recognized aspects of the passive activity loss rental property rules. Rental losses that you can’t use today won’t disappear. They slowly but surely decrease the tax bill you’ll owe in the future, one year at a time, until they’re all gone.

How Loss Carryforwards Work

The income from a rental property is considered passive income and is only subject to the tax loss rules in the year it is earned. Any tax loss in any year less than the amount you can deduct in that year will be suspended and carried over to the next tax year.

Example of carryforward accumulation:

| Tax Year | Rental Loss | Allowable Deduction | Carryforward Balance |

|---|---|---|---|

| Year 1 | $8,000 | $0 | $8,000 |

| Year 2 | $7,500 | $0 | $15,500 |

| Year 3 | $9,000 | $0 | $24,500 |

| Year 4 | $6,000 | $0 | $30,500 |

If you sell the property in the year, or in a year when your income falls below this threshold, the full $30,500 is released, and offsets your income in full for that year.

Why New Landlords Often Show Losses for Years

There are several factors in the early years of a rental property that will result in tax losses despite a positive cash flow. Interest rate will be the highest in the initial years (front-loaded amortization). The depreciation is also 100% from day one, at $9,091 per year. The first year’s repairs, furnishings, advertising, and legal costs are most severe.

Any losses accumulate annually with a growing carry forward balance if they were not incurred by the real estate professional and your income is over $150,000. This is not a shortcoming of the strategy. It is the approach to develop value that can be used in the future.

Strategic Loss Timing

If you have a high income tax year, such as a bonus, or closing a business deal, or having other higher income, consider accelerating your rental costs in order to reduce your income tax liability in that year. Prepay insurance. Complete pending repairs. Have a cost segregation study performed. One of the obvious illustrations of proactive tax planning is to focus deductions on the year in which they will benefit you most.

On the other hand, if your income falls in a low year, ask yourself if it’s worth letting carry forward losses go down the drain with a property sale. The rate of those released losses is dependent on the timing of the sale. You’ll need to make this kind of planning a year ahead of time, as it is with your CPA.

Seven Tax Mistakes That Trigger IRS Audits (And How to Avoid Them)

Aggressive tax planning, when not executed properly, is the source of genuine tax audit risk. The majority of these errors are a result of one thing – renter income reporting. I’ve seen these seven mistakes and their solutions time and time again.

Mistake 1: No Documentation for Mileage and Expenses

The IRS isn’t going to accept your word for your deductions. A contemporaneous log should accompany every mileage claim (date, destination, purpose and mileage). Each and every expenditure must have a receipt or bank statement.

The simplest solution is to use a dedicated app, which automatically logs all trips and allows you to categorize business vs. personal travel from one swipe. Understanding the key components of successful expense tracking including categorization, consistent documentation, and systematic record-keeping—makes the entire process manageable. Use Stessa or accountant’s software to manage expenses. Set these systems up in week one and documentation becomes simple.

Mistake 2: Claiming Initial Furnishing Instead of Replacements Only

The expenses for the initial furnishing of a rental property cannot be deducted. Replacements are allowed as a deduction. If a landlord acquires a refrigerator in the first year of a new rental, he or she does not receive any immediate deduction. After 5 years, a landlord who gets a new refrigerator replaces it with his full cost. Know the difference. Your receipts and property’s history tell the tale.

Mistake 3: Claiming 100% Business Use

If you ever do use your rental property personally, even once, then the amount of time the house was available for rent should be taken into account and applied to your deductions. Any personal use on a property, with 100% business use is an audit flag. Track actual available percentage of rentals and use it uniformly for all deductions for that property.

Mistake 4: Using Round Numbers on Your Tax Return

$1,200 in repairs, $800 in insurance, $500 in supplies. In the case of round numbers, indications mean estimates and not records. The IRS is looking for this pattern. Real expenses produce figures like $487.32 and $1,047.89. If your schedule E is a lot of zeros, you haven’t documented enough.If your schedule E is a lot of zeros, you haven’t documented enough — an auditor will notice

Mistake 5: Not Retaining Records Long Enough

The three-year window for standard IRS audits is from the IRS filing date. However, the window is extended to six years if the IRS suspects that you underreported income by 25% or more. Depreciation records: Documentation should be retained for the entire deposit period and 6 years post-sale period. Records must be maintained for 15 years, for a 2030 property sold after 15 years, that means a 15-year potential exposure period. Cloud-based backup and digital storage is the only viable option.

Mistake 6: Mixing Personal and Rental Expenses

Create a separate bank account for your rental properties—this is a basic budgeting principle that becomes critical for rental property owners. Make all payments for rent from that account and deposit all rents in that account.

Personal and rental funds that are placed in a single account make it difficult to clearly distinguish the deductible expenses from the non-deductible expenses—and make audit red flags more likely. Commingling of personal and rental funds creates audit red flags that wouldn’t exist if the funds were separated and makes it difficult to clearly distinguish personal from rental expenses.

Mistake 7: Forgetting Depreciation Recapture at Sale

There is a misconception among many landlords that depreciation recapture will not be treated if they do not take the depreciation. The IRS taxes you on the depreciation amount that you could have taken, not what you actually took. Prior to signing listing agreement, determine the total accumulated depreciation and recapture tax. This number does have a direct impact on your net proceeds and your choice of selling or exchanging.

Filing and Reporting: How to Actually Implement These Strategies

Understanding the strategies is one thing, but having them written down is another. Most guides don’t explain the nuts and bolts of reporting rental income, how to do it, how to stay compliant, and how to set things up to be done properly and efficiently for years to come. The mechanics are covered, and Schedule E, the fundamental tax form for every landlord, is the first one covered.

How to Report Rental Income on Schedule E

The rental property income and expenses are reported on Schedule E (Supplemental Income and Loss). A new column is created for each property. You report gross rents received, and then itemize each of the categories of deductible expenses. The net gain (or loss) goes to your Form 1040 and is included in your adjusted gross income.

The depreciation amount is based on the depreciation amount on Form 4562 where you record all the depreciable assets and the remaining recovery periods. Form 4562 can get complicated with multiple properties purchased at various times, cost allocations, and depreciation schedules. Many self-filing landlords make expensive mistakes here.

Net profit or loss incurred on each property for the tax year are added to Form 1040. If passive losses were incurred in the previous years but have been suspended, they are reported on Form 8582 and are released based on the rules outlined in Strategy 5.

When You Need to Make Estimated Tax Payments

Rental property owners are normally expected to make quarterly estimated tax payments if their net income from their rental property is more than $1,000 and they anticipate owing more than $1,000 in federal tax for the year. The deadlines are usually April 15th, June 15th, September 15th and January 15th of the next year. If you don’t make the required estimated payments, you will be charged an underpayment penalty, which is a small percentage, but can be avoided with a bit of planning.

If your rents aren’t regular (rental units are not fully occupied, repairs may not be done on a regular basis), consult with a CPA and be conservative with your estimates, not aggressive.

DIY vs. Hiring a CPA: What to Choose

If you own one rental property that has simple income and typical deductions, decent tax software (TurboTax or H&R Block) will do a good job of filing your tax return. If you’re a landlord with more than one property, cost segregation, 1031 exchanges, passive loss carryforwards or real estate professional status claims come into play, and a real estate CPA isn’t a luxury; it’s a necessity.

A house real estate CPA’s return is normally 3 times to 10 times the amount of money they save you on taxes. An experienced landlord who has switched said, “Get an accountant; I discovered $11,000 in deductions that I had overlooked for three years.

CPA fees for rental property returns vary from $500 to $2,000 per year, depending on the complexity of the returns. Think of it as a business expense – and it is!

State and Local Tax Considerations

Federal strategies are not standalone. The tax treatment of rental income varies by state. States that don’t tax income, such as Texas and Florida, have no state income tax, so federal optimization is it. However, rental income is subject to taxes in some states that can make it more complex and costly, such as California (up to 13.3%) and New York (up to 10.9%).

There are states that have their own depreciation rules that don’t match the federal rules. California, in particular, doesn’t offer the same bonus depreciation percentages as the federal code. Check treatment in each state with a state certified CPA.

Record-Keeping Best Practices

Your rental property bookkeeping system should be built by following a systematic budgeting process that ensures nothing falls through the cracks. The system should include: income received by property and by month—all income received; all costs covered and grouped by cost category (repair, insurance, management, etc.).

Dated and documented for purpose mileage logs,

Cost basis documentation for each asset (purchase price, closing costs, improvements, etc.)

Accumulated depreciation by asset and depreciation schedules:

Stessa is the most popular free rental property accounting software. It is linked to your bank account, automatically classifies transactions, and produces tax-time, Schedule E-ready reports. Buildium or AppFolio offer more comprehensive property management capabilities and accounting for larger portfolios.

Use a separate “basis tracking” document for each property. It will be useful at the time of your sale, possibly decades later, as it records everything that’s going to impact your cost basis purchase price, capitalized improvements, and depreciation taken.

Putting It All Together: How to Pay No Taxes on Rental Income Full Blueprint

Let’s take a realistic example and walk through how these strategies all come together. Here’s how the rental property owner can turn a paper loss rental into a real cash flowing rental property and how he can pay no taxes on the income.

Property details: $300,000 purchase, $60,000 down, $240,000 mortgage at 7% Monthly rent: $2,400 | Annual gross rent: $28,800

| Expense | Annual Amount |

|---|---|

| Mortgage interest | $16,800 |

| Property taxes | $3,600 |

| Landlord insurance | $1,200 |

| Repairs and maintenance | $2,400 |

| Property management (8%) | $2,304 |

| Total cash expenses | $26,304 |

| Depreciation (non-cash) | $9,091 |

| Total deductions | $35,395 |

Taxable income: $28,800 − $35,395 = −$6,595 (tax loss)

Actual cash flow: $28,800 − $26,304 = +$2,496 (profit)

You made $2,496 in real cash. Your tax return shows a $6,595 loss. Federal tax owed on this property: zero.

Years Two Through Seven

Years two – seven: This is the period in which the principal amount of the mortgage is being paid down, and the interest amount decreases at a gradual pace. The depreciation remains constant at $9,091 per year. You have more cash flow as rents increase (3%/year) and the tax situation looks good. At the fifth year, one might be making $2,700 a month and still be in a small tax loss or break-even situation.

If income is over $150,000 and the passive loss rules prevent the losses from being taken as a deduction this year, they will be added to the carryforward account, a future tax shield that will help offset income when you sell or refinance or when income falls below the threshold.

Year Fifteen: Refinance and Reset

At the end of year 15, the house could sell for $425,000.The value of the house after fifteen years is $425,000. Your equity is $180,000 and your mortgage is about $185,000. A cash-out refinance at 75% LTV will generate a new loan for $318,750, and leave you with approximately $130,000 cash in hand, which will be tax-free.

The new loan will add to your interest expense, and thus to your annual deductions. Your depreciation remains the same. You earn more money from your rent. The refinance resets your deduction profile for another 15 years.

Year Twenty-Seven: Sale or 1031 Exchange

At the end of the depreciation schedule, you have 2 choices.

Path A Direct sale: Property worth $600,000. Capital gain of $400,000. Rental income has been already subject to depreciation rates, which amounted to $90,909, the full value of the building depreciated over 27.5 years. Total tax bill before state: potentially $90,000 to $120,000.

Path B 1031 exchange: $0 tax due. The entire $600,000 is invested in a replacement property. Under current law, heirs inherit with a stepped-up basis and all the accumulated tax liability is lost forever at death. The difference between these two ways is a distinction between good investment and generational wealth.

Final Thoughts: Wealth First, Taxes Second

The tax code is the only one that outright favors the investor in real estate. These are tools that Congress intended to include in the statute and are part of the depreciation rules, 1031 exchanges, passive loss rules and the Augusta Rule. It’s not like they’re out of your reach. They are. But is it worth taking the time to use them?

There are no easy ways to avoid paying taxes on rental income, but there are good ways: ensure they have good properties, keep good records, and utilize a CPA or qualified tax professional with a real estate background. The property investor who handles this seriously and takes it day by day will always do better compared to the one who doesn’t use these investing strategies.

The strategies contained in this article are valid for 2026 and tax legislation may change. Be sure to always check current rates and rules with a CPA or visit IRS.gov before putting any strategy into action.

You can never go wrong with the foundation which is always the property itself. Locate a solid market, control it properly, and the tax methods in this article will compound each dollar you make. Rental property investing is one of the most powerful vehicles for building long-term wealth, but only when it’s part of a comprehensive financial plan with clear milestones and goals.

No good investment will compensate for bad fundamentals, and no tax optimization will make up for that.

Your Next Steps

Take your previous tax return and find each rental deduction you took

Now check your list with the operating costs included in Strategy 1 see if there are any gaps

Make sure that you are claiming the right depreciation amount (building value / 27.5).

If your property is worth more than $200K, have a cost segregation feasibility analysis done.

Figure out if you’re eligible for the $25,000 special allowance or real estate professional.

Have a planning meeting with a CPA familiar with real estate before year-end.

This week, create a separate bank account with a separate accounting software (Stessa) for your rental property.

The Long Game

Not all landlords that make good money in real estate are necessarily the ones who made the best landlords deals. They’re the ones who retain a lot of the fruits of what their homes produce every year, every decade. Tax strategy is not a process you do at the end of the year after you talk to your CPA. Tax strategy is not a thing that you do at the end of the year after you speak to your CPA. It is something you think about in January, do throughout the year and continually improve as the tax code evolves.

Start now. All the strategies can be found here.

Frequently Asked Questions

How is it that I can have rental income of $2,000 a month (or more) and still pay no taxes?

Yes, and, it’s more common than people think. This is why a property that makes $24,000 a year in rent can have a tax loss after all expenses are factored in, including mortgage interest, property taxes, insurance, repairs, management fees and depreciation. Depreciation alone can generate $8,000 to $10,000 in non-cash deductions each year that lower income taxes by itself, without any spending. That comes to an advantage that this puts the taxable income at zero or negative when a property is cash-flowing.

Can I claim depreciation even if I didn’t know about it?

Yes, it is 100% legal. The depreciation is a deduction that is approved by the IRS that recognizes how much buildings deteriorate over time. An amended return (Form 1040-X) may also be filed to claim depreciation for up to three of the prior tax years. This process can be managed by a CPA.

If the property is sold, what will happen to my suspended passive losses?

All suspended passive losses are released in full in the year you sell the property in a fully taxable transaction. If you have $40,000 of suspended losses and sell the property, all $40,000 will be deducted against ordinary income in the year of the sale, which can result in lots of money being sheltered from your taxable income when you sell the property.

Is there an Augusta Rule for rental to family members?

The IRS considers a “fair rental value” the amount you must rent to a tenant, including family members. In cases where the rent is less than the market rent, the IRS could classify it as a disguised sale and the tax-exempt status could be denied. Charge the market rate, and list it correctly on Airbnb or VRBO using comparable, and always have a rental agreement on hand.

Are the tax treatment of vacation rentals different from the tax treatment of long-term rentals?

Some of the rules governing vacation rentals vary based on the number of days you rent a year and the number of days you actually use the property. The Augusta Rule applies if the property is rented for four or fewer nights.The Augusta Rule applies for rentals of 4 or fewer nights. Mixed-use rules apply when renting for over 14 days and you personally use it for over 14 days or 10% of the rental days (whichever is higher) and you must prorate between deductible and non-deductible use. An error is possible, so ask a CPA for help if you are dealing with a mixed-use property.

What are the requirements for becoming a real estate professional?

You must be materially involved in more than 750 hours per year in a real property trades or business, and the hours must be more than 50% of the total hours you worked for the year in all your trades or businesses. Both tests need to be satisfied concurrently. Maintain a comprehensive contemporaneous record of all time spent on real estate activities – good record keeping has been the life blood of many court controversies. An expert real estate CPA can evaluate your particular case before filing the claim.

To put your rental property in an LLC or not?

A single-member LLC offers landlords some liability protection without altering the tax consequences of owning rental income. You need to take into account the annual LLC filing fees in your state (which in California equals $800), your lender’s guidelines, and the transfer of title cost. If the equity is large enough, it makes sense to have the liability protection at the expense of the annual maintenance fee almost every time. Explain the details to your real estate lawyer and/or your CPA.

Where should I keep my rental property reserves and tax savings?

Keep 3-6 months of expenses in a high-yield savings account dedicated to your rental properties. This ensures you have immediate access to funds for emergency repairs, vacancy periods, or quarterly tax payments while earning competitive interest on money that would otherwise sit idle. Never commingle these reserves with personal funds maintain separate accounts for clean record-keeping and audit protection.