How to Save Money Fast on a Low Income: 15 Proven Strategies With a 90-Day Action Plan

How Saving Money Fast on a Low Income Actually Happens: Two Real Stories

I want to start with two real stories before sharing a single tip on how to save money fast on a low income because if you’re in the paycheck-to-paycheck cycle, you don’t need more generic advice. You need proof that this is actually doable.

Gabe Bult was cleaning office buildings at night. Not a glamorous job. No weekends off. No high salary. He hadn’t even finished high school. Yet by the time he turned 22, he had saved $25,000 while earning well under the median income. He wasn’t born into money. He didn’t get a windfall. He used a specific set of strategies the same ones we’re going to walk through together.

Then there’s the story of a waiter in Chicago who was barely making rent with zero savings. He started moving $20 into a separate account every single time he got paid manually, by hand, every time. That amount felt almost laughably small at first. But that account eventually grew to over $2,000. He used that money to buy recording equipment without going into debt, which launched a YouTube channel that changed his entire financial trajectory.

These weren’t people with advantages you don’t have. They were low-income earners under real financial pressure and what changed things wasn’t luck, or a raise, or a perfect moment. It was doing something small, consistently, for long enough that it compounded into something real.

If you’re in the paycheck-to-paycheck cycle right now, that’s exactly where they started too.

Why Saving Money Fast on a Low Income Feels Impossible (But Isn’t)

Let me be honest about something most financial articles won’t say. When you’re earning a low income or living on a fixed income, standard money advice is largely useless for your situation.

“Save 20% of your income.” Great. But what if 55% of your income already goes to rent? What exactly are you saving 20% from?

“Cut your morning coffee.” Sure $5 a day is roughly $150 a month. But if your housing costs are eating half your paycheck, no amount of coffee skipping will solve the real problem.

The advice isn’t wrong for people earning comfortable incomes. It just doesn’t apply to your reality. That’s not a personal failure. It’s a gap in the advice itself.

The 3 Psychological Barriers to Saving on Low Income

Financial literacy gaps are the first barrier. Not knowing where to start, which account to use, or what budgeting method fits a tight budget creates paralysis. Most pbudgeting on low incomeeople end up doing nothing because the options feel overwhelming.

Immediate gratification is the second barrier. When you’re constantly stressed about money, your brain craves relief right now. Saving for a future goal feels abstract when today’s problem is immediate. This isn’t weakness. It’s a natural psychological response to ongoing financial pressure.

Social pressure is the third and the least talked about. Watching people around you spend freely, travel, or buy things you can’t afford creates a quiet “keep up with everyone else” pull that slowly destroys savings habits. Even small purchases that feel social can add up to hundreds of dollars a month.

Understanding these three barriers matters because saving on a low income is not just a math problem. It’s a behavioral challenge. If you only try to fix the math without addressing the behavior, you’ll set a budget and abandon it in two weeks. Work on both at the same time.

And here’s the practical truth: you can watch every video, read every article, have every tool installed and still do nothing. One small action today beats a hundred plans that stay in your head.

What “Fast” Really Means (30–90 Day Expectations)

Let me reframe what “fast” actually looks like in your situation.

Fast does not mean saving $10,000 in a month. Fast means meaningful, measurable progress within 30 to 90 days.

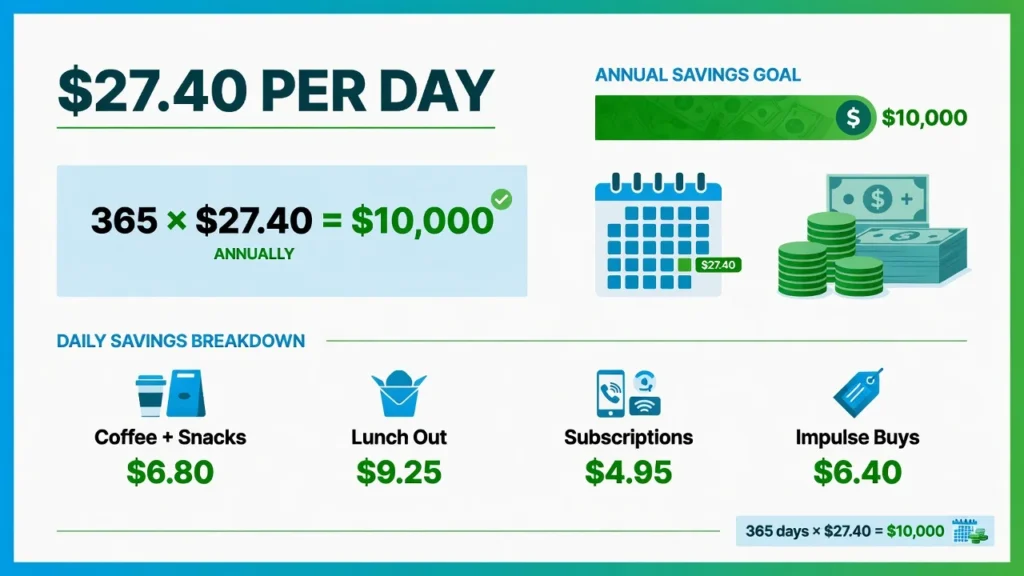

If you save $500 in 30 days starting from nothing, that is fast. If you reach $1,000 in 90 days, that is a genuine win. Here’s a number worth writing down: saving $10,000 in a year means setting aside just $27.40 per day through reduced spending, added income, or both. When you translate a big annual goal into a daily number, it shifts from feeling impossible to feeling like something you can actually aim for.

Set your financial goals in daily or weekly numbers. The specificity makes the difference.

Start Here: Your 7-Day Money Audit (Track Every Dollar Before You Save)

Here’s the most important step before you try any savings strategy: you cannot fix what you haven’t measured and the fastest way to start is to track expenses for just one week.

Most people have a rough sense of what they spend. But a rough sense is not the same as actual numbers. There’s almost always a gap between what you think you spend and what you actually spend and that gap is usually exactly where your savings are hiding.

A 7-day money audit closes that gap. Every dollar you spend for one week gets written down. Every coffee. Every snack. Every app charge. Every gas stop. You don’t need a special tool. A notebook works. Your phone notes app works. A Google Sheet works.

The goal is not to feel bad about what you find. The goal is information. You’re doing detective work on your own finances, not passing judgment on yourself.

At the end of 7 days, total everything up by category. What usually surprises people most are the food and takeout numbers, the subscriptions they forgot about, and the small convenience purchases — things that can quietly add up to $100 or more in a single week.

Free Tools to Track Every Dollar

You don’t need a paid app for this. A basic pen and paper works well because the physical act of writing makes spending feel more real. Google Sheets with a simple three-column layout date, category, amount works for anyone comfortable with a phone or laptop.

Free apps like YNAB (You Need A Budget) or Monarch Money offer automatic transaction tracking if you connect your bank account and prefer a digital approach. Note: Mint discontinued its service in 2024, so avoid any recommendations pointing you there.

The important thing is not which tool you pick. The important thing is that you actually use it every single day for 7 days without skipping.

Build your money management habit here. Everything else builds on top of it.

What to Look For in Your Spending Patterns

Once you have your 7 days tracked, look for four specific things.

Forgotten subscriptions are the biggest low-hanging fruit for most people. Streaming services, gym memberships, app subscriptions, trial periods that auto-renewed these often run $8 to $50 a month each and can add up to $100 to $200 in monthly waste you don’t even notice.

Impulse food spending is the second area. This includes not just restaurants but the snack at the gas station, the drive-through because you didn’t plan lunch, and groceries you bought without checking what was already at home. A useful mental shift: calculate how many hours of work it takes to pay for a single takeout meal. That number changes your relationship with the spending.

Transportation costs often surprise people. Not just gas, but parking fees, ride-share apps, and out-of-the-way detours to cheaper stations that end up costing more than they save. Add these up across a week and the total is often shocking.

Recurring expenses that don’t actively improve your life. These are the automatic spending habits you probably don’t consciously notice the $12 app subscription you haven’t opened in four months, the premium plan on a service you use on the free tier anyway.

Your 30-60-90 Day Plan to Save Money Fast on Low Income

Now that you’ve completed your audit, here’s a realistic roadmap. These aren’t aspirational numbers pulled from someone earning a comfortable salary they’re based on strategies that real low-income earners have used to build savings from nothing.

Month 1 target: $300 to $500 This month is about fast, visible action. Cancel the subscriptions you found in your audit. Sell 5 to 10 items you don’t use. Start one micro-savings method this week any one of the three you’ll find in the automation section below. These steps alone, done consistently, typically produce your first $300 to $500.

Month 2 target: $500 to $700 By month 2, your budget system is written down and working. Your food costs have dropped through meal planning. You’ve seriously looked at whether your housing or transportation costs can be reduced. Your savings habit is beginning to feel like a normal part of your week rather than a sacrifice.

Month 3 target: $700 to $1,000 By month 3, savings should be either automated or deeply routine. A side income source even a small one has started contributing. Your emergency fund is real and growing. The financial pattern that once felt out of reach is now your actual day-to-day reality.

Total at 90 days: $1,500 to $2,200 saved from scratch.

Keep this daily number somewhere visible: $27.40. That’s how much you need to save or earn each day to reach $10,000 in one year. Breaking a big goal into a daily number makes the path forward concrete instead of overwhelming.

Month 1 Goal: Save $300–$500 (The Quick Wins)

The first month is purely about fast, visible wins actions you can take this week that show immediate results in your bank account.

Step 1: Cancel every subscription you haven’t actively used in the past 30 days. For most people, this alone frees up $50 to $150 in month one.

Step 2: Sell 5 to 10 items you no longer need. Old electronics, unworn clothes, furniture in storage. Facebook Marketplace and OfferUp are free and reach local buyers quickly.

Step 3: Start one savings method this week not next month, this week. The three options that work best for beginners are covered in detail in the automation section below. Pick the one that sounds easiest and start it with your next paycheck.

Any one of these builds the savings habit. The goal in month one is not the amount it’s proving to yourself that saving is something you actually do.

Month 2 Goal: Save $500–$700 (Systems in Place)

Month 2 is about replacing impulsive spending with deliberate systems. By now you have some savings momentum. The work in month two is locking in the habits that make those savings automatic.

Your budget plan is written down and you’re working it. Your food costs are dropping through meal planning and smarter grocery shopping. You’ve looked seriously at whether housing or transportation costs the two biggest expense categories can be reduced.

If you’re renting alone and spending more than 40% of your take-home pay on housing, this is the month to act. Research taking on a roommate, moving to a smaller unit, or negotiating with your landlord. Even reducing housing cost by $100 to $150 a month adds $1,200 to $1,800 to your annual savings without any other changes.

Month 2 is also when your grocery and food systems should start producing consistent savings. If you’re not yet using a weekly meal plan with a cash-only grocery envelope, start both this month.

Month 3 Goal: Save $700–$1,000 (Habit Solidified)

By month 3, the focus shifts from building the habit to making it automatic and sustainable.

Set up an automatic transfer from your checking to a dedicated savings account that executes on the same day your paycheck arrives before you have time to spend it. Even $30 to $50 automating out on payday adds up to $360 to $600 a year without any conscious effort. If your side hustle has started producing income, direct that money straight into savings before it touches your regular spending account.

Most importantly: protect what you’ve built. Your emergency fund now exists. Guard it. Do not touch it for anything that isn’t a genuine financial emergency a car repair you can’t defer, an unexpected medical bill, a gap in income. Everything else can be managed another way.

At the end of month 3, review your numbers. You’ve likely saved $1,500 to $2,200 and built habits that if you keep them will produce dramatically different financial outcomes over the next 12 months.

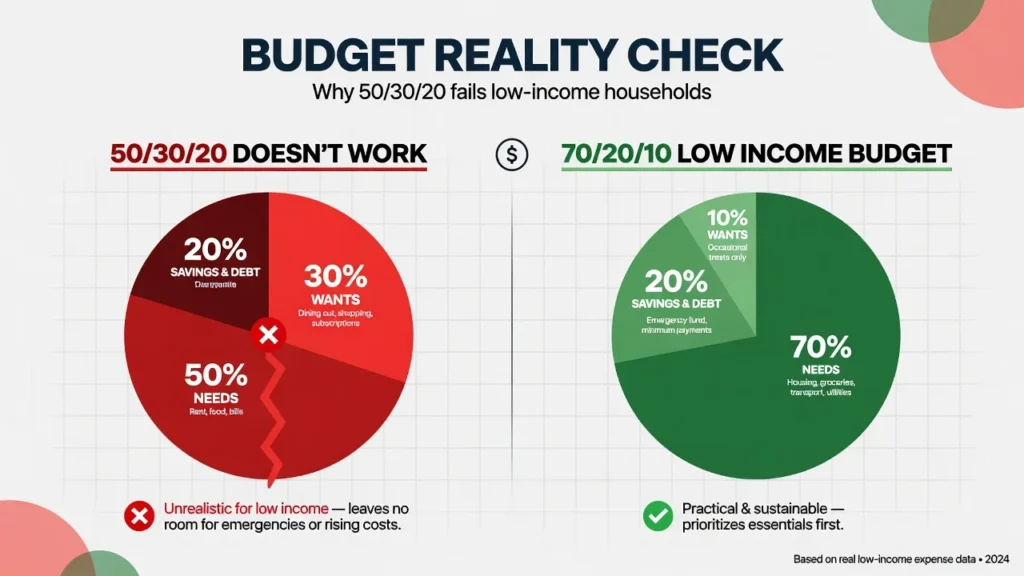

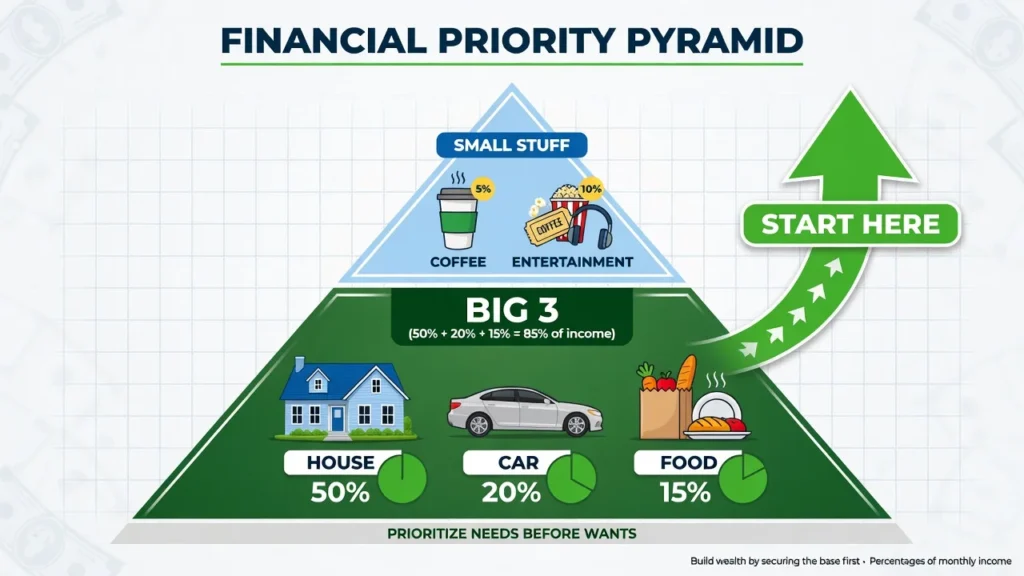

Budgeting on Low Income: Why 50/30/20 Doesn’t Apply to You (Try 70/20/10 Instead)

The 50/30/20 budget rule is one of the most widely shared personal finance frameworks online. It allocates 50% of your income to needs, 30% to wants, and 20% to savings. It’s clean, it’s simple, and if your rent alone already takes up 55% of your take-home pay, it simply doesn’t apply to your situation.

I’m not criticizing the framework it works well for people with comfortable incomes and lower housing burdens. The problem is that most of the personal finance content you find online was written for that audience, not yours. Following advice that doesn’t fit your situation doesn’t produce savings. It produces guilt and frustration.

What you need is a money management framework that starts with your actual numbers. Here’s one built specifically for low-income budgeting reality.

The 70/20/10 Budget Rule for Low Income

70% : Essential living expenses (monthly expenses): This covers rent, utilities, basic groceries, transportation to work, and any minimum debt payments. If your rent alone pushes past 70%, you’re in a situation where the Big 3 expenses (housing, transportation, food) need to be addressed before the rest of the budget can work.

20% : Savings and debt repayment: When you’re just starting out, split this as roughly 15% toward a small emergency fund and 5% toward debt above minimums. As your emergency fund grows, shift more of this 20% toward debt payoff, then eventually toward longer-term savings.

10% : Everything else: Small wants, entertainment, personal care, and any non-essential spending lives here. When the envelope is empty, non-essential spending stops for that period.

If even 70% for essentials isn’t realistic right now, use an 80/15/5 split temporarily: 80% to essentials, 15% to savings, 5% to everything else. This is a short-term survival budget, not a permanent plan. Use it while you work on reducing your biggest expenses.

Zero-based budgeting applies this logic in practice: every dollar you earn gets assigned to a specific category the moment income arrives. Rent gets its portion. Groceries get theirs. Savings gets its allocation. Nothing goes unassigned. This eliminates the trap of “I’ll save whatever’s left” because with zero-based budgeting, there is no “whatever’s left.”

Envelope Budgeting: Cash Control for Variable Expenses

The envelope method works best for the categories where you tend to overspend typically food, entertainment, and personal care.

At the start of the month or week, withdraw cash for each variable spending category and place it in a labeled envelope. Groceries. Dining out. Gas. Personal spending. When the envelope is empty, that category’s spending stops for the period.

This works because physical cash feels real in a way that card swipes don’t. Seeing the bills actually decrease makes your spending behavior adjust naturally. Many people who have tried every app and spreadsheet report that this straightforward method is the one that genuinely changes how they spend.

If you rarely carry cash, a digital envelope app like Goodbudget works on the same principle you allocate virtual envelopes by category and track manually as you spend. The key is the same: when the category is empty, you stop.

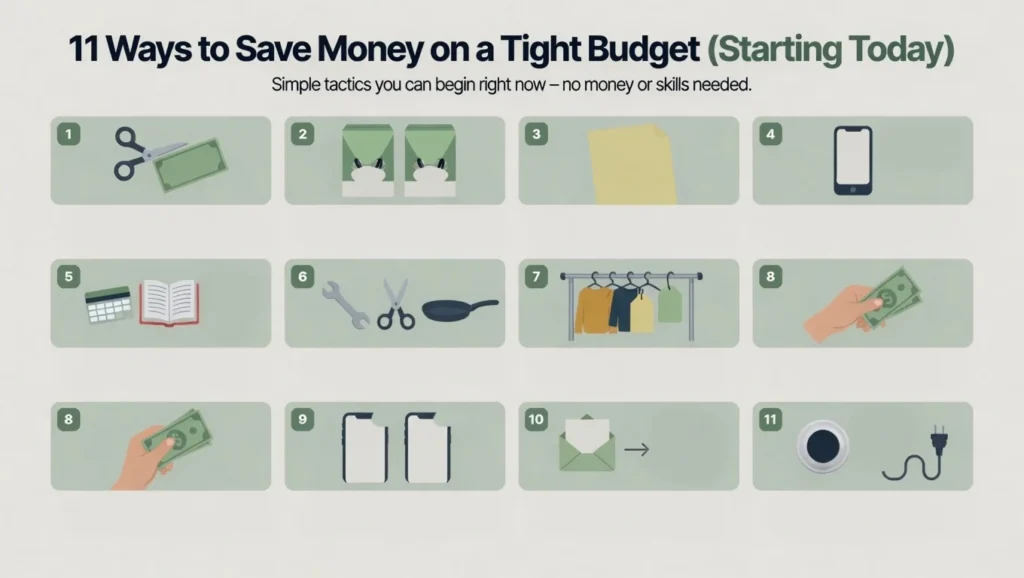

11 Ways to Save Money on a Tight Budget (Starting Today)

These are specific, actionable tactics each one can be started today with no special equipment, skills, or upfront money.

1. Cancel unused subscriptions. Go through your last two bank statements and highlight every recurring charge. Cancel anything you haven’t actively used in the past 30 days. Average savings: $50 to $150 per month.

2. Switch to generic brands. Store-brand products are often manufactured in the same facilities as name brands. The quality difference on most staples is minimal. The price difference is typically 20 to 40%.

3. Use the 30-day rule for impulse purchases. For any non-essential purchase over $20 that wasn’t planned, wait 30 days before buying. Write it on a list. If you still want it after 30 days and can afford it, buy it. Most of the time the urge fades.

4. Negotiate your recurring bills. One of the fastest ways to reduce bills call your internet, phone, and insurance providers and ask directly for a lower rate. Mention competitor pricing. Most providers have retention discounts they don’t advertise. This takes 20 minutes and can save $20 to $50 per provider monthly.

5. Use free entertainment. Libraries offer books, audiobooks, movies, and sometimes museum passes all free. Community events, parks, and local festivals replace expensive weekend habits.

6. Do things yourself. Basic car maintenance, haircuts, home repairs, and cooking at home more often all have free tutorial videos online. The hourly value of learning these skills is high and the savings are ongoing.

7. Thrift shop strategically. Clothes, kitchen items, furniture, and books at thrift stores often cost 5 to 20% of retail price. Focus your thrift shopping on the categories where you spend the most.

8. Use cash for your problem spending categories. If you consistently overspend on groceries or dining out, switch to cash-only for those categories for 30 days.

9. Use cash-back and round-up savings tools. Cash-back apps like Ibotta and Rakuten return real money on purchases you’re already making. Round-up apps like Acorns save the change from every card transaction automatically. Neither requires changing your spending only adding one step to what you already do. Note: Acorns charges $3 per month, so make sure your round-ups consistently exceed that before committing to a paid tier. Combined, these tools typically add $20 to $60 a month to your savings with no extra effort.

10. Leverage any windfall immediately. Tax refunds, bonuses, gift money, or any unexpected income goes directly into savings the day it arrives not toward a celebration purchase. Savings first, always.

11. Reduce utility bills with small changes. Adjust your thermostat by 2 to 3 degrees. Switch to LED bulbs. Unplug devices not in use. These changes save $20 to $60 a month depending on your current habits and utility rates.

Cutting Expenses on Low Income: The Big 3 vs The Small Stuff

There’s a specific order to cutting expenses that most personal finance advice gets completely backwards.

Most articles start with the small stuff: skip your coffee, pack your lunch, cancel Netflix. If you’re disciplined, those changes save you $100 to $150 a month.

But if your housing is already taking 50% of your income, and your car payments plus insurance plus gas are taking another 20%, you have a 70% problem that no amount of latte-skipping will fix.

When you need to cut spending fast, the most impactful approach starts with the Big 3: housing, transportation, and food. Everything else is secondary until those three are optimized.

Housing: Rent Hacking and Geo-Arbitrage Explained

Housing typically takes the largest share of any low-income budget. The most aggressive and effective way to reduce it is rent hacking.

Rent hacking means renting a place slightly larger than you need, living in one section, and renting out the remaining rooms to one or more roommates. Done well, the rental income from your roommates covers most or all of your own housing cost taking you from spending 40 to 50% of your income on housing down to 5 to 10%. The financial impact is equivalent to gaining a second income.

This requires living with other people, which isn’t right for everyone. But if you’re in the early stages of building savings, it’s worth seriously considering.

If renting out space isn’t possible, the next option is what financial writers call geo-arbitrage moving to a cheaper neighborhood, a smaller unit, or even a lower cost-of-living city where your income stretches further. The short-term discomfort of a less desirable space creates real breathing room to build savings quickly.

A third option and the most accessible is negotiating directly with your current landlord. If you’re a reliable, long-term tenant with a good payment history, some landlords will agree to a small rent reduction in exchange for minor property maintenance tasks. It costs you nothing to ask, and even $50 to $75 off monthly rent adds $600 to $900 to your annual savings.

Transportation: The True Cost of Your Car

Transportation is the second biggest expense category for most low-income households — and the one most underestimated because the costs are spread across multiple line items.

The full cost of owning a car includes the loan payment, insurance, gas, maintenance, annual registration, and depreciation. According to AAA’s annual driving cost analysis, a single vehicle costs between $10,000 and $12,000 per year on average when all ownership costs are included. If you’re currently making car payments, that number alone may be one of the biggest drains in your budget.

If public transit, biking, or carpooling with a coworker can realistically replace a vehicle even part-time the savings are substantial. Two-car households that drop to one often free up the equivalent of a part-time income in monthly expenses.

If you need a car and are considering your options, choose an older model purchased outright or with a small loan over financing a new vehicle. A reliable $5,000 used car with modest insurance costs significantly outperforms a $25,000 car requiring a $450 monthly payment both on your monthly budget and your long-term net worth.

Why the “Latte Factor” Is a Distraction

The latte factor concept isn’t wrong it’s just in the wrong order.

Yes, cutting small daily habits saves money. Yes, $5 a day is $1,800 a year. But if your housing and transportation together are eating 70% of your income, eliminating your morning coffee saves you 1 to 2% of total spending. It’s a rounding error compared to addressing the Big 3.

The right order: optimize housing first. Reduce transportation costs second. Cut food costs third. Then, and only then, do the small daily habits become meaningful accelerators instead of the primary strategy.

Save $200+ Monthly on Food Without Eating Ramen Every Night

Food is the most flexible expense in most budgets which makes it one of the most powerful levers for low-income savers. Unlike rent, you have real control over what you spend here. And unlike entertainment, you can’t skip it entirely.

Cooking at home more often isn’t about deprivation it’s intentional spending that gets you better value from every food dollar.

According to the USDA, Americans waste roughly one pound of food per person per day. That waste represents real dollars going directly from your paycheck into the trash. Reducing food waste alone without changing what you eat can save a meaningful amount each month.

The second biggest food cost for most low-income households is unplanned eating. When you don’t know what you’re having for dinner, you’re vulnerable to takeout, fast food, or expensive convenience items. A weekly plan removes that vulnerability before it costs you.

Meal Planning and Batch Cooking (Cut Your Grocery Bill by $150+)

Meal planning doesn’t need to be elaborate. At its simplest, it means deciding what you’ll eat for the next week before you go grocery shopping.

Once you know your meals, you build a specific list. You shop the list and nothing else no browsing, no impulse additions. You buy what’s on the list, pay, and leave.

Batch cooking takes this further by preparing multiple meals in a single cooking session. A large pot of beans, rice, or soup on Sunday takes roughly the same time as one normal meal but provides lunches and dinners for multiple days. Freezer meals extend this even further, letting you cook in large quantities and freeze portions for weeks ahead.

For a single person, combining meal planning with batch cooking typically reduces grocery spending by $150 to $200 per month. For families, the savings are often higher. It also eliminates the “what do I make for dinner tonight” problem that sends people to fast food or takeout which is where most food budgets quietly collapse.

One of the fastest ways to cut grocery costs without reducing nutrition: replace meat in 3 to 4 meals per week with beans, lentils, or eggs. Meat is consistently the most expensive item in any grocery cart. A bean-based dinner costs a fraction of one built around chicken or beef and the protein content is comparable.

Strategic Grocery Shopping (The Cash-Only Method)

Shop the store perimeter first. That’s where produce, proteins, and dairy live. The center aisles are where processed and convenience foods are shelved and those are almost always more expensive per serving than their whole-food equivalents.

Buy generic and store-brand versions of staple items. For pasta, canned goods, rice, flour, and similar basics, the quality difference from name brands is negligible while the price difference is meaningful.

Consider discount grocery chains. Aldi consistently offers prices 20 to 30% lower than standard supermarkets on most staple categories.

Use the cash envelope method specifically for groceries. Set your weekly grocery budget, withdraw that exact amount in cash, and shop only with that cash. When it’s gone, shopping stops for the week and you work with what you have. This single habit eliminates the “I’ll just grab a couple extra things” creep that destroys most grocery budgets.

Automate Your Savings (But Build the Habit First)

Almost every money advice article will tell you to automate your savings immediately. And they’re right that automation works long-term. But something important gets lost when you automate before you’ve consciously built the habit.

When you manually move $20 to savings every payday, you experience the action. You watch the account grow. You feel the small decision. That experience is what builds the psychological foundation that makes saving sustainable over time.

When you automate from day one, you never experience the decision. The money just disappears. For people who already have strong saving habits, this is efficient. But for someone building from scratch, it can feel like the money was always just gone and the connection to the behaviour never really forms.

Why Manual Saving Works Better at First

Start with one manual method for your first 30 to 60 days. The $20 rule is the simplest: every time any income arrives, move $20 to a separate savings account before spending anything else. It sounds almost too small to matter. But it works for two specific reasons.

First, it carries zero risk. The money is still accessible if you genuinely need it. This removes the fear barrier that stops many low-income earners from saving anything at all.

Second, watching a savings account grow from $0 to $20 to $40 to $100 to $200 creates a concrete kind of motivation. You’re watching a number rise that directly represents your effort and decisions. That progress loop seeing your own actions produce visible results is what keeps the habit alive.

The key insight: when you subtract $20 from your available balance, you naturally adjust your spending to the remaining number. Most people who try this report barely noticing the difference in day-to-day spending after the first few weeks.

When and How to Automate (Month 3+)

After 60 to 90 days of manual saving, the habit is established. Now automation makes it effortless and removes willpower from the equation entirely.

Set up automatic savings by scheduling recurring transfers automate transfers from checking to a dedicated savings account on the same day each paycheck arrives, before you have a chance to spend it. Even $25 to $50 per paycheck adds up to $650 to $1,300 a year without a single conscious decision after setup. If your side hustle is producing income, direct that automatically as well.

This is the pay-yourself-first approach: you treat savings as a non-negotiable expense the same way you treat rent. It leaves before anything discretionary touches it. No willpower required. No end-of-month hoping there’s something left.

Where to Keep Your Savings (High-Yield Accounts and Apps)

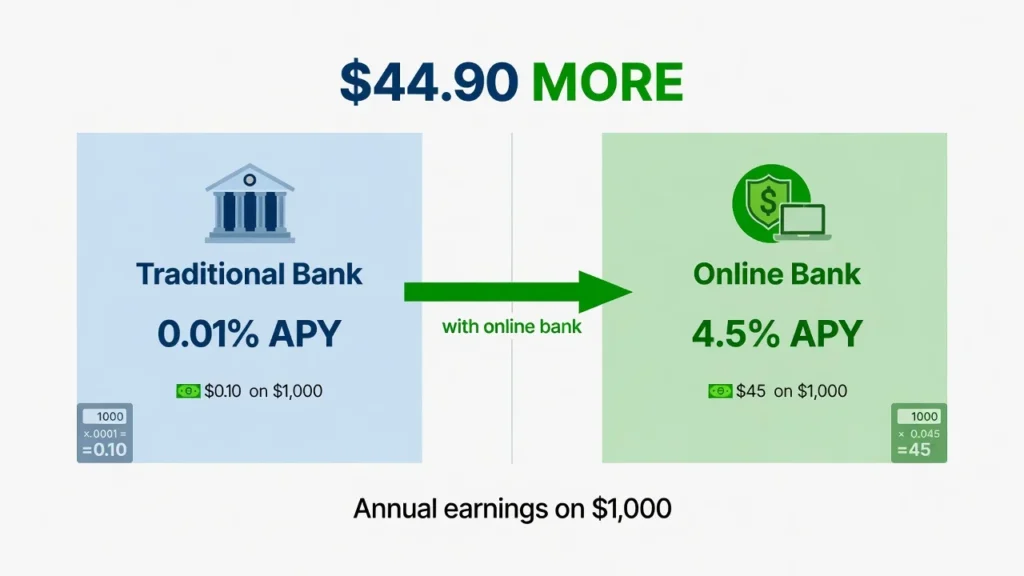

Where you keep your savings matters more than most people realize. Leaving savings in the same checking account as your spending money is the fastest way to accidentally spend it. And keeping it in a traditional bank savings account earning 0.01% interest means your money is losing purchasing power to inflation every month it sits there.

High-Yield Savings Accounts

Online banks like Ally, SoFi, and CIT Bank offer high-yield savings accounts that pay significantly more than traditional brick-and-mortar banks. Rates vary and change with the market, but high-yield accounts have recently offered between 4% and 5% APY compared to the standard 0.01%. The practical difference: on $1,000, that’s roughly $45 a year versus $0.10. On $5,000, it’s approximately $225 a year in interest with no extra effort.

Opening a high-yield savings account is free and takes about 10 minutes online. Most have no minimum balance requirement. The minor inconvenience of a transfer taking 1 to 2 business days is a feature for an emergency fund it creates just enough friction to prevent impulse withdrawals.

Keep your emergency fund and any specific savings goals in a high-yield account, fully separate from your everyday checking. Check current rates at the time you open your account, as they change with Federal Reserve policy.

Savings Apps and Round-Up Tools

Cash-back apps like Ibotta and Rakuten return real money on grocery and online purchases you’re already making. Ibotta gives cash back on specific grocery items when you scan receipts. Rakuten provides cash back from online retailers. Neither requires changing your spending only adding one step to what you already do.

Round-up apps like Acorns link to your debit card and automatically round each purchase to the nearest dollar, saving or investing the difference. Buying something for $4.37 triggers a $0.63 automatic save. These small amounts add up to $20 to $50 a month for average spenders with no conscious effort. Note: Acorns charges $3 per month, so make sure your round-ups consistently exceed that before committing to a paid tier.

These tools supplement your main savings strategy. They’re not replacements for a real budget and savings habit, but they’re genuinely useful additions especially in the early months when every dollar counts.

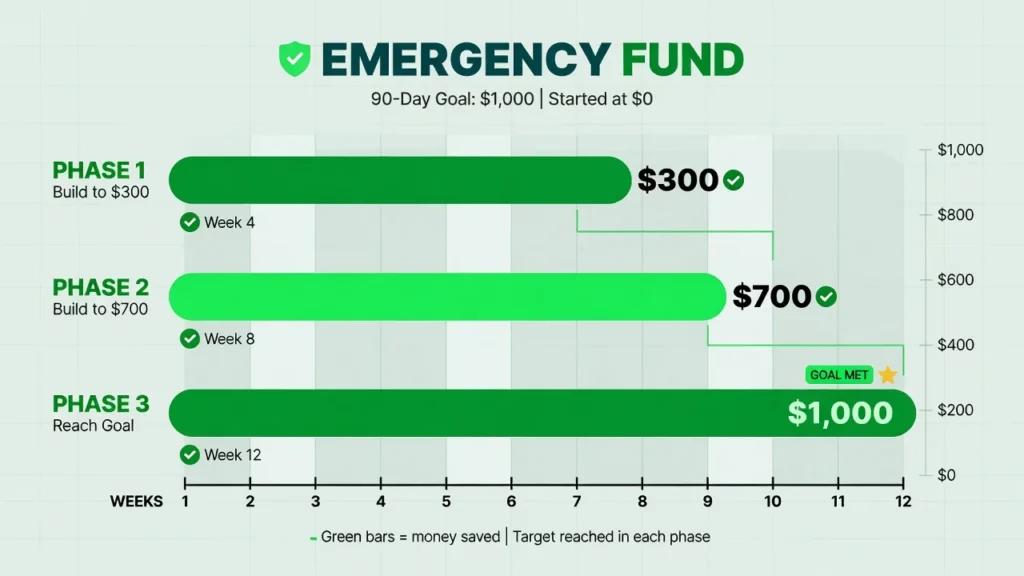

Build Your $500–$1,000 Emergency Fund in 90 Days (Action Plan)

Before you invest, before you pay extra on debt, before you do anything else with saved money you need to save for emergencies first a starter fund of $1,000. This is not optional.

Without a cash cushion, any unexpected expense (a car repair, a medical bill, a broken appliance) goes straight onto a credit card. That creates new high-interest debt that wipes out the progress you’ve made. The emergency fund is your protection against that cycle.

Dave Ramsey’s Baby Step One targets a $1,000 starter emergency fund as fast as possible. That number is the minimum, not the goal but it’s the right first target because it covers the most common financial emergencies most people face.

Here’s something that often surprises people who save their first $500 to $1,000: even that small cushion changes how you feel about money. You go from being completely vulnerable to every unexpected cost to having a buffer. The psychological shift is almost as significant as the financial one. Financial research consistently shows that the psychological impact of a small emergency fund is as significant as the financial impact.

Week-by-Week Savings Goals to Hit $1,000

Weeks 1 to 4: Target $300. This comes from subscription cancellations you found in your audit, selling a few unused items, and starting your first micro-savings method.

Weeks 5 to 8: Target $400. Your food costs are dropping through meal planning. Your budget system is working. Any side income earned this month goes directly into the fund.

Weeks 9 to 12: Target $300. The quick wins of month one are behind you month three’s target is slightly lower because the easy gains are already captured. Your savings habit is established, and automation may have started. Any windfall this period (a tax refund, extra work hours, a small gig job) goes directly here.

Result: $1,000 in 90 days, starting from zero.

When to Use Your Emergency Fund (And When Not To)

An emergency fund is for genuine emergencies only. Car breaks down and you need it for work: emergency. Medical bill you can’t defer: emergency. Job loss with no backup income: emergency.

A sale on something you want, a social event that costs money, or a “good deal” you don’t want to miss: none of these qualify.

When you use your emergency fund for a real emergency, your very next financial priority is replenishing it before debt payoff, before extra savings, before anything else. Keep this fund in a high-yield savings account that’s separate from your everyday checking account. Even at the same bank, a dedicated account creates enough distance to prevent casual dipping.

When Cutting Isn’t Enough: Boosting Income on Low Wages

There’s a ceiling to how much you can save by cutting expenses. At some point, your essential costs are at their minimum and there’s nothing left to cut. When you hit that wall, the only path forward is increasing income.

This doesn’t mean you need a better job immediately. It means using what’s available to you right now to generate additional cash even temporarily, even imperfectly.

Quick Cash: Sell What You Don’t Use

Most households have $200 to $1,000 worth of unused items sitting in closets, garages, and storage clothes that don’t fit, old electronics, furniture you’ve been meaning to get rid of, books, sports equipment, kitchen appliances.

Facebook Marketplace and OfferUp make selling locally easy and free. Electronics sell quickly at any price point. Clothes sell well when photographed in natural light against a plain background. Furniture moves fastest when priced 70 to 80% below retail.

A serious weekend of decluttering and photographing can generate several hundred dollars within a week. Every dollar goes directly to your emergency fund or savings target not back into spending.

Gig Economy and Side Hustles Worth Your Time

The gig economy offers income options that fit almost any schedule. Door Dash, Instacart, and Uber provide flexible hours evenings, weekends, or any gap in your week. TaskRabbit connects people with local work for practical skills: assembling furniture, moving help, or basic repairs.

The key is treating this income as temporary and purposeful. Working an extra 10 to 15 hours per week for 3 to 6 months to reach a specific savings target is a fundamentally different commitment from taking on a permanent second job. You’re not changing your life forever. You’re sprinting toward a number.

Some people in aggressive savings phases run two or three income sources simultaneously for a defined period a primary job plus one or two gig sources on evenings or weekends. This level of intensity isn’t sustainable long-term, but for 6 to 12 months with a clear target in view, it can accelerate savings dramatically. The difference is that you know it’s temporary.

Invest in Your Earning Power (Free Education)

This is the most underutilized strategy for low-income earners and the one with the highest long-term return.

The time you spend commuting, doing repetitive work, or waiting between tasks can be invested in higher earning power. Free audiobooks on financial skills, YouTube tutorials on in-demand topics, and platforms like Coursera or Khan Academy cost nothing but attention. Even 30 minutes a day of focused learning compounds significantly over 6 to 12 months.

Skills worth prioritizing: basic coding, digital marketing, spreadsheet proficiency, trade certifications, or any skill your current employer pays a premium for. Learning a skill that earns you $3 to $5 more per hour permanently changes your financial baseline.

The long-term truth: financial freedom comes from increasing your income floor, not just reducing your spending ceiling. Cutting expenses is necessary. Raising your earning capacity is what changes the trajectory.

Government and Community Resources You’re Leaving on the Table

I want to address something directly: many low-income people qualify for financial assistance programs that would meaningfully free up money for savings but don’t use them because of stigma, confusion about eligibility, or simply not knowing they exist.

Using programs you qualify for is not a character failure. It’s smart. Programs like SNAP, Medicaid, and LIHEAP exist specifically for situations like yours, and using them gives you the financial breathing room to build stability which is exactly what reduces dependence on assistance over time.

Food Assistance (SNAP, WIC) and How to Apply

SNAP (Supplemental Nutrition Assistance Program) provides monthly benefits for grocery purchases. Eligibility is based on household size and gross income a single adult earning at or near minimum wage often qualifies in most states, though limits vary. Average monthly benefits range from $150 to $300 for individuals (amounts adjust annually; check your state’s current limits).

Apply through your state’s social services department most states now allow online applications. If you qualify, SNAP directly reduces your grocery spending, which frees up those dollars for savings.

WIC (Women, Infants, and Children) provides nutritional support for pregnant women and young children in qualifying households.

Food banks and community food pantries provide free groceries in most communities with no eligibility requirements. Using these resources even temporarily can meaningfully reduce monthly food costs while your savings build.

Utility and Housing Help (LIHEAP, Section 8)

LIHEAP (Low Income Home Energy Assistance Program) provides financial assistance with heating and cooling costs for qualifying households. Given that utility bills can run $100 to $200 or more per month, qualifying for LIHEAP directly frees up money for savings.

Section 8 housing vouchers subsidize rent for qualifying low-income households. Waiting lists can be long which is exactly why applying now matters. Earlier application means earlier access.

Many utility companies also offer low-income rate programs and budget billing (a flat monthly payment calculated from your average usage, which prevents large seasonal spikes). Call your utility provider directly and ask specifically about assistance programs and low-income rates these aren’t always advertised.

Tax Credits That Put Money Back (EITC, CTC)

The Earned Income Tax Credit (EITC) is one of the most valuable and underused financial tools available to low-income workers. Depending on your income and family size, the EITC can put $500 to over $6,000 directly back in your pocket at tax time.

The Child Tax Credit (CTC) provides additional savings for qualifying parents.

If you’re not claiming these credits, you’re leaving real money on the table. Free tax preparation through VITA (Volunteer Income Tax Assistance) ensures you claim every credit you qualify for at no cost. VITA operates primarily during tax season typically February through April so plan ahead.

Free Financial Counseling and Community Support

Non-profit credit counselling agencies offer free or low-cost financial counselling, debt management plans, and budgeting help. The National Foundation for Credit Counselling (NFCC) can connect you with accredited agencies in your area visit nfcc.org to find local options.

Community organizations, libraries, and faith-based organizations also frequently offer free financial literacy workshops, emergency assistance funds, and referrals to additional local resources. A call to your local library or United Way chapter is often the fastest way to find what’s available in your specific area.

Should You Save or Pay Off Debt First? (The Real Answer)

This is one of the most common questions in personal finance, and the answer is more nuanced than the typical “pay debt first” or “save first” advice admits.

Here’s the framework that works for most low-income earners when balancing savings and debt repayment: start with a small emergency fund, then attack high-interest debt, then build savings. In that specific order.

The $1,000 First Rule (Why Emergency Fund Beats Debt)

Save $1,000 before aggressively paying any debt beyond minimum payments.

This seems counterintuitive when you’re carrying debt at 20%+ interest. But consider this: without a cash cushion, the next car repair or unexpected medical bill goes straight onto a credit card. You’re not just failing to make progress you’re actively moving backward. The $1,000 emergency fund breaks that cycle before it continues.

While you’re building that $1,000, keep paying the minimum on every debt. Don’t skip payments. Just don’t make extra payments yet.

Debt Snowball: Smallest to Largest (Ignore Interest Rates)

Once your $1,000 emergency fund is saved, list all your debts from smallest total balance to largest.

Pay the minimum on every debt except the smallest. Put every extra dollar toward that smallest debt until it’s gone. Then move to the next smallest with the same intensity.

This is the debt snowball method. It’s not mathematically optimal the debt avalanche method (targeting highest interest rate first) saves more money over time but for most people, the psychological momentum of eliminating actual debts produces better real-world results. Each eliminated debt gives you a visible win that makes the next one feel achievable.

If you’re disciplined and motivated by numbers rather than milestones, the avalanche method is worth considering. For most people starting from scratch, the snowball produces better follow-through.

The One Exception: High-Interest Debt Is an Emergency

If you’re carrying credit card debt at 20 to 25% APR while keeping money in a 4% savings account, you’re effectively losing 16 to 21% annually on every dollar held in savings instead of applied to debt. The numbers don’t lie.

Once your $1,000 emergency fund is secure, any high-interest debt above 10% APR becomes your highest financial priority. The interest you’re paying costs more than any savings rate you’re realistically going to earn.

5 “Money-Saving” Tricks That Actually Make You Poorer

Not every frugal living tactic actually saves money. Some create the feeling of being careful with money while quietly costing more. Here are five worth knowing including one that almost everyone does.

1. Buying in bulk when you can’t use it all. Bulk pricing only saves money if you use everything before it expires or spoils. Buying a giant bag of produce you throw half of away costs more than buying what you need weekly.

2. Using credit card rewards to justify spending. Earning 2% back on a purchase you wouldn’t have made otherwise is not a saving it’s a spending rationalization.

3. Shopping sales on things you didn’t need. “It was 50% off” is not savings unless you would have bought it at full price. A $40 item at 50% off that you didn’t need costs $20, not saves $20.

4. Driving across town for cheaper gas. If you drive 10 miles out of your way to save $0.05 per gallon on a 12-gallon fill-up, you spent $0.60 in fuel savings and burned more in the detour. The math rarely works.

5. Canceling all insurance to cut costs. Dropping health, renters, or car insurance to save $50 to $100 a month creates catastrophic financial risk. One accident or medical event can cost more than years of premiums. Insurance is a non-negotiable budget item for low-income earners specifically because one bad event without it can destroy years of progress.

Stay Motivated: Reframe Your Terrible Job and Celebrate Small Wins

Here’s something I’ve noticed from real accounts of people who saved their way out of low-income situations: the job they hated became one of their most powerful financial motivators.

When your work is genuinely miserable working nights and weekends, dealing with difficult conditions for wages that feel disrespectful that dissatisfaction is information. It’s telling you exactly what you’re building toward. Every dollar saved is buying you closer to a future where that specific job is optional.

People who made the most dramatic financial turnarounds often describe their worst work periods as their most financially productive. Being uncomfortable in a job they wanted to leave created urgency. Urgency created discipline. And six months of real discipline produced financial changes they hadn’t thought were possible.

Your Terrible Job Is Actually Motivation (If You Use It Right)

Most of us carry a mental image of what financial freedom looks like personally a different career, working for yourself, cutting back to part-time, or just not having to panic every time the car makes a strange noise.

That image is your why. Your terrible job is the thing that makes that why feel urgent instead of theoretical.

Write down what you’re working toward. Put it somewhere you’ll actually see it. On a bad Tuesday night at a job you resent, that written goal is what keeps the savings habit alive. It turns misery into motivation on purpose.

Track Progress and Celebrate Every $100

Invisible progress is demotivating. Make yours visible.

A savings tracker on paper, a hand-coloured chart on your wall, or a savings balance you check every week any of these transforms an abstract number into real, visible evidence of your effort. Every $100 milestone deserves a small acknowledgment: not a spending celebration, but a genuine moment of recognition that you did something hard and it worked.

The motivation to keep going comes from seeing that your actions are producing results. Build that feedback loop early, and saving starts to feel like something you’re winning at not just something you’re enduring.

Find Your Money Community (You’re Not Alone)

The online personal finance community for low-income earners is large, active, and genuinely supportive. The r/povertyfinance subreddit specifically offers real-world advice, shared experiences, and accountability from people navigating exactly the same challenges you’re facing.

Local community organizations, faith-based organizations, and libraries sometimes host financial support groups or budgeting workshops. Having even one accountability partner who shares your savings goals changes this work from lonely and difficult to shared and sustainable.

The same social pressure that makes saving hard can work in your favor. When the people around you are building financial stability rather than competing for visible spending, the pull to overspend weakens considerably. Community is one of the most underrated financial tools available.

Your First $1,000 Starts Today: Take These 3 Actions Right Now

You’ve read through 15 real strategies. The only thing that separates making real progress from returning to this article in 6 months having changed nothing is whether you take one action today.

Not tomorrow. Not when things calm down. Today.

Gabe started saving $25,000 while cleaning office buildings at night without a high school diploma. He started with the exact question you have right now: how do I actually begin?

The answer is always the same: one small action, not the perfect action.

Action 1: Start your 7-day money audit today. Open a notes app, grab a notebook, or pull up a spreadsheet. Write down every dollar you spend for the next 7 days. No judgment just measurement.

Action 2: Choose one savings method and start it this week. The $20 rule: move $20 to a separate savings account the next time any income arrives. The zeroing out method: look at your balance tonight and move the last digit to savings. A round-up app: download one and connect your debit card in the next 10 minutes. Pick one. Do it.

Action 3: Write down your daily savings target. To save $10,000 in a year, you need $27.40 per day through earning, spending reduction, or both. Write that number somewhere you’ll see it not as pressure, but as a daily reminder that the target is specific and reachable.

Saving money fast on a low income is hard. I won’t pretend otherwise. The cost of living is real. The wages are real. The bills are real. But so are the people who have done this from exactly where you are now.

The path to financial freedom doesn’t start with a windfall or a raise or a perfect moment. It starts with $20. Or $27.40. Or even $5.

It starts today.

Start now.

This article is for educational purposes. For personalized financial advice, consult a certified financial counsellor or financial planner. Program eligibility, benefit amounts, and interest rates referenced in this article are subject to change always verify current figures directly with the relevant agency or institution.

Frequently Asked Questions: How to Save Money Fast on a Low Income

Q1: Can I really save money when I’m barely making enough to pay bills?

Yes but only if you attack the Big 3 expenses first: housing, transportation, and food. Small cuts like skipping coffee won’t move the needle when rent alone takes 50% of your income.

The fastest move: take on a roommate (rent hacking) to drop housing costs from 40–50% of income to under 10%. Add one temporary side hustle DoorDash, Instacart, or TaskRabbit for 3–6 months.

Gabe Bult saved $25,000 by age 22 on a below-median income using exactly this approach. A broke waiter started with $20 per paycheck and grew it to over $2,000. Start with whatever you can. $20 is enough to begin.

Q2: Should I save money or pay off debt first?

Follow this order:

Save $1,000 emergency fund first : without it, the next car repair creates new credit card debt and kills your progress

Pay off high-interest debt above 10% APR : carrying 22% APR debt while saving at 4% means you’re losing 18% annually

Use the debt snowball : smallest balance first, minimum payments on everything else, every extra dollar at the smallest until it’s gone

Build a full 3–6 month emergency fund, then invest

One line: $1K emergency fund → high-interest debt → full emergency fund → investing.

Q3: How much can I realistically save in 3 months on a low income?

$1,500 to $2,200 in 90 days is realistic from zero:

Month 1: $300–$500 : cancel subscriptions, sell unused items, start $20/paycheck savings habit

Month 2: $500–$700 : meal planning cuts grocery budget $150–$200, budget plan is working

Month 3: $700–$1,000 : savings automated, side hustle contributing, emergency fund growing

Daily target to keep visible: $27.40/day = $10,000/year. Break the big number down and it stops feeling impossible.

Q4: Is it better to automate savings or do it manually?

Manual first for 30–60 days, then automate.

Manual saving builds the habit you watch the account grow, your brain adjusts spending to the lower balance, and the behavior becomes real. Automating too early means the money disappears without you ever engaging with the decision.

The $20 rule: Move $20 to a separate savings account every time income arrives before spending anything. After 60–90 days, automate. Even $25–$50 per paycheck automated adds $650–$1,300 a year with zero effort after setup.

Q5: Should I always buy the cheapest option to save money?

No. Use this formula instead:

(Total Price) ÷ (Number of Uses) = Cost Per Use

$20 shoes replaced 5 times a year = $100 annually. $100 shoes lasting 3 years = $33 annually. The “expensive” option saves $67 a year.

Buy quality for daily-use items: work shoes, appliances, reliable used car. Buy cheap or second hand for rarely used items thrift stores offer 5–20% of retail on clothes, furniture, and kitchen goods.

The real frugal living mistake: obsessing over a $3 saving while ignoring a $400/month car payment.

Q6: What’s the fastest way to save $1,000 for an emergency fund?

Combine all five at once : 30–60 days is achievable:

Zeroing out method (tonight): Move the last digit of your checking balance to savings daily. $347 balance → move $7. Small amounts add up fast.

Cancel subscriptions (this week): Two bank statements, highlight every recurring charge, cancel anything unused in 30 days. Saves $50–$150 immediately.

Sell unused items (this weekend): Facebook Marketplace and Offer Up are free. Electronics, clothes, furniture most households have $200–$1,000 sitting unused. Photograph in natural light; items sell faster.

Pick up 5–10 gig shifts: DoorDash or Instacart evenings. Ten shifts at $50 net = $500 straight to your fund.

Direct your tax refund to savings the day it arrives not toward anything else, savings first.

Keep this fund in a high-yield savings account (Ally or SoFi, currently 4–5% APY) separate from checking.

Q7: How can I save money on groceries when I’m already buying the cheapest food?

The problem usually isn’t what you’re buying it’s the system around it:

Meal plan before every trip : the USDA reports Americans waste roughly 1 lb of food per person per day. A weekly plan eliminates that waste and prevents emergency takeout.

Replace meat 3–4 meals per week with beans, lentils, or eggs meat is the most expensive grocery item and the protein swap is comparable.

Cash envelope for groceries : withdraw your weekly budget in cash, shop only with that, stop when it’s gone.

Shop Aldi : consistently 20–30% cheaper than standard supermarkets on staple categories.

Batch cook weekends : one session covers lunches and dinners for 4–5 days, removing the daily takeout temptation.

Result: $150–$200/month saved for a single person without cutting nutrition.

Q8: Is couponing worth my time on a low income?

Only if it takes under 10 minutes and covers items already on your list.

The math: 3 hours clipping coupons to save $15 = $5/hour below minimum wage. That same 3 hours on DoorDash earns $30–$50.

Worth it: 5–10 minutes on Ibotta or Rakuten before a grocery run you were already making. Both return real cash on purchases you’re making anyway.

Not worth it: buying things you didn’t need because they were “on sale,” or spending hours for minimal return.

Your time is your most valuable asset on a low income. Strategic coupon use adds $20–$60/month. Developing one marketable skill that earns $3–$5 more per hour adds $6,000–$10,000/year.