How to Calculate Gross Monthly Income: 4 Methods With Real Examples

When my mortgage lender first asked for my “gross monthly income,” I handed over my take-home pay figure. Wrong number entirely. That small mistake almost derailed my application and it taught me why knowing how to calculate gross monthly income matters far more than most people realize.

Gross monthly income is everything you earn in a month before taxes and deductions reduce it federal income tax, health insurance, retirement contributions, student loan garnishments. All of that comes out afterward. Your gross is the raw starting number.

Lenders, landlords, and financial institutions all use this number to evaluate your earning capacity. When a bank reviews your mortgage income requirements, they work exclusively from your gross not your take-home pay because it gives them a standardized, comparable view of what you actually earn, not what your specific tax situation leaves behind.

In this guide, I’ll walk you through four methods to calculate gross monthly income accurately whether you’re salaried, paid hourly, receive a biweekly paycheck, or earn from multiple income sources.

What Does Gross Monthly Income Mean? (And How It Differs From Net)

In financial terms, “gross” has a precise meaning: it’s your income before deductions the full amount your employer agreed to pay you before the government, insurance providers, and retirement accounts take their share.

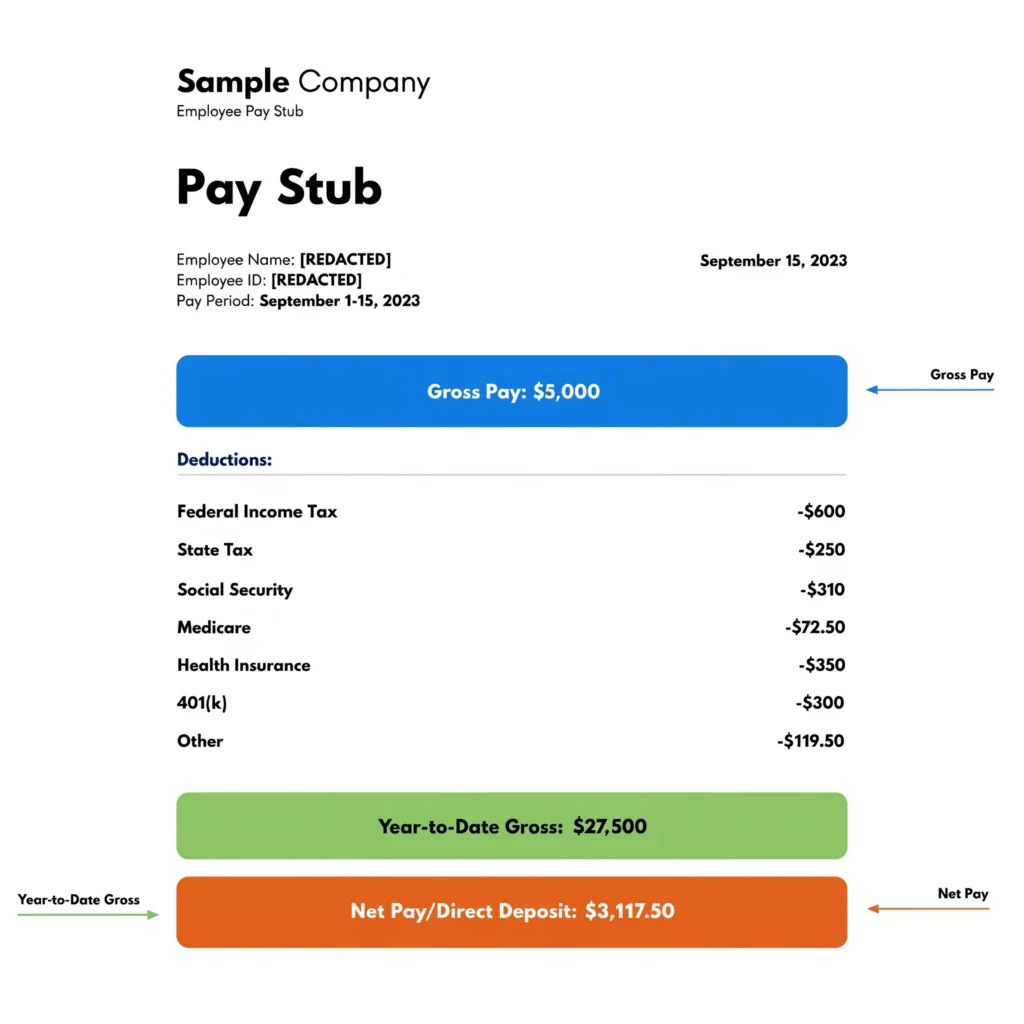

Your pay stub makes this visible. At the top you’ll see your Gross Pay. Below that are line items: federal income tax, Social Security, Medicare, health insurance premiums, 401(k) contributions. Each one chips away at that gross figure. What remains at the bottom your Net Pay is what actually deposits into your bank account.

Simply put: gross is what your employer committed to paying you. Net is what you actually keep.

Depending on your tax bracket, state, and benefit elections, the gap between those two numbers is typically 25–35% of your gross. A $5,000 gross paycheck might leave you with $3,250–$3,750 in hand after everything comes out. This net figure is what you’ll have available for managing your monthly expenses and financial planning.

Why Do Lenders Ask for Gross Monthly Income Instead of Net?

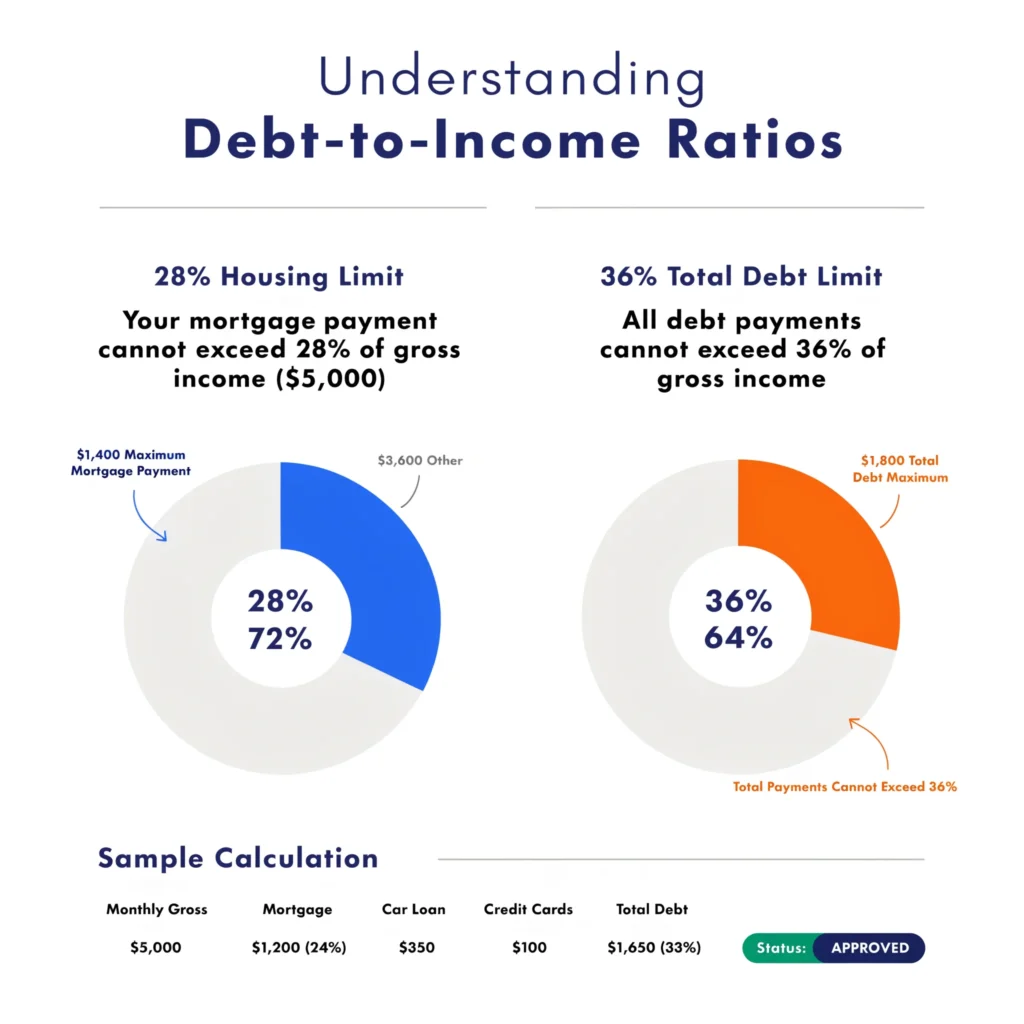

Lenders ask for gross income not net because they need a standardized number to calculate your debt-to-income ratio (DTI): the percentage of your monthly gross income that goes toward debt payments.

Here’s how this plays out on a real mortgage application. The lender takes your gross monthly income and applies two thresholds:

- Your mortgage payment alone shouldn’t exceed 28–30% of your gross monthly income

- Your total debt load mortgage, car loans, credit cards, student loans shouldn’t exceed 36%

The Consumer Financial Protection Bureau (CFPB) and Fannie Mae both use these 28/36 DTI thresholds as benchmarks, supported by decades of mortgage default data showing borrowers outside these ranges default at significantly higher rates.

Why gross? Because two people earning the same salary could have wildly different net incomes depending on their state tax rates, health plan choices, and retirement contributions. A borrower in Texas and a borrower in California both earning $80,000 gross take home different amounts but their earning capacity is identical. Gross income levels the playing field.

This is actually a fairer system than it first appears. It evaluates what you earn, not what your personal financial decisions leave behind.

How to Calculate Gross Monthly Income: Choosing the Right Method

Your correct income calculation method depends on how you get paid. Below are four methods covering every common pay structure.

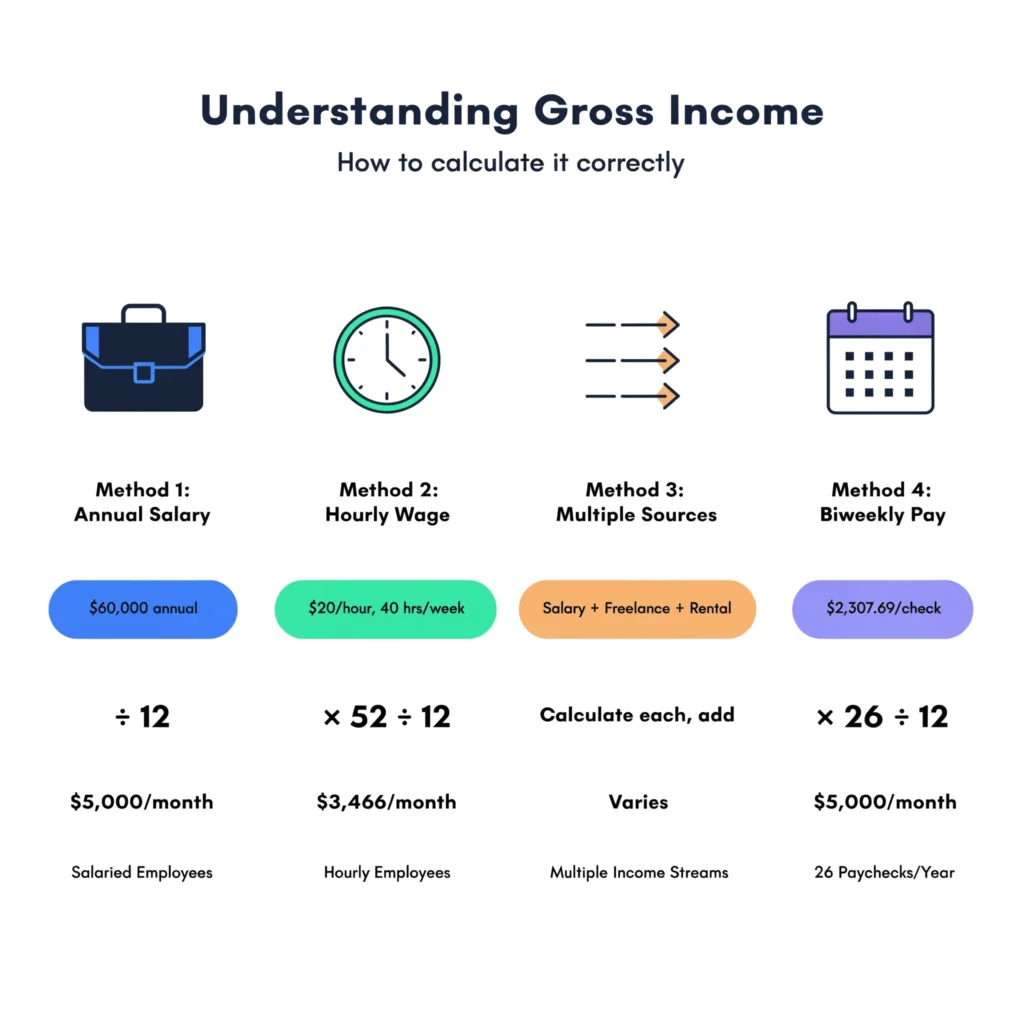

Method 1: Calculate Gross Monthly Income From Your Annual Salary

For salaried employees, this income calculation is the most straightforward of all four methods no guesswork, just basic division.

Your annual salary is the number in your employment contract or offer letter. Whether it’s $40,000 or $140,000, the process is identical: divide by 12.

The Gross Monthly Income Formula for Salaried Employees

This salary conversion formula is the same regardless of your pay level:

Annual Salary ÷ 12 = Gross Monthly Income

Because your salary is fixed for the year, dividing by 12 gives you a consistent monthly figure every time.

If you’d rather verify your figure per paycheck first, multiply your per-paycheck gross by the number of pay periods in a year, then divide by 12.

Real Examples: Annual Salary to Monthly Gross

Here are three concrete examples at different salary levels:

- $40,000 ÷ 12 = $3,333.33 gross monthly income

- $60,000 ÷ 12 = $5,000 gross monthly income

- $90,000 ÷ 12 = $7,500 gross monthly income

In every case, the gross is what you earn before deductions. Your actual paycheck will be lower — for a $5,000 gross, you might see $3,200–$3,700 deposited, depending on taxes and benefit elections.

What If Your Salary Includes Bonuses or Commissions?

Many jobs include variable compensation on top of base salary bonuses, commissions, and performance pay all count toward your gross. Here’s how to handle each situation:

Method A : Include everything: Add your total expected annual compensation (base + average bonus) before dividing by 12. Use this for personal budgeting.

Method B : Separate base from variable: Calculate base salary monthly gross, then add a documented monthly average of your variable pay (based on 12–24 months of history). For loan applications, Method B is generally preferred because it clearly separates guaranteed income from variable income lenders appreciate the transparency, and underwriters can verify each component independently.

Method 2: Calculate Gross Monthly Income From Hourly Wage

Not everyone receives a weekly paycheck from a salaried position. For hourly workers, your paycheck frequency weekly, biweekly, or semi-monthly and your actual hours worked both affect the calculation.

The Formula for Hourly Employees

Hourly Rate × Hours Per Week × 52 Weeks ÷ 12 Months = Gross Monthly Income

This income formula annualizes your earnings first, then converts to monthly which is more accurate than simply multiplying by 4 weeks.

Converting hourly wages to monthly income trips people up for one reason: multiplying by 4 weeks per month is wrong. The math doesn’t hold. There are 52 weeks in a year not 48 so using 4 weeks/month undercounts your earnings by about 8%.

Real Examples: Hourly Wage to Monthly Gross

Example 1 : Standard 40-hour week at $20/hr: $20 × 40 × 52 ÷ 12 = $3,466.67 gross monthly income

Example 2 : Overtime at $20/hr, averaging 45 hrs/week: $20 × 40 × 52 ÷ 12 = $3,466.67 (regular) $30 × 5 × 52 ÷ 12 = $650 (overtime at 1.5x) Total: $4,116.67 gross monthly income

The Key Variable: Average Monthly Hours

For hourly workers, the key variable is your average monthly hours and that number matters more than most people realize.

If you typically work 40 hours per week but sometimes pick up overtime, use your realistic average not your best-case scenario. The most reliable approach: add up your total hours for the last three months, divide by three to get a monthly average, then apply that to your formula.

This is the most common payroll calculation error hourly workers make assuming 52 full working weeks when they should account for unpaid time off, slow seasons, or reduced hours.

What About Overtime and Seasonal Work?

Overtime is additional pay for hours beyond 40 per week (or your jurisdiction’s standard). Include it in your gross calculation if it’s consistent and documented over at least 12 months. A one-month overtime spike doesn’t count as regular income for loan purposes.

Seasonal work requires an annualized approach: add your total income across all working months, then divide by 12 not just by the months you worked. A holiday retail worker earning $18,000 across October–January has a gross monthly income of $1,500/month ($18,000 ÷ 12), not $4,500/month ($18,000 ÷ 4).

Method 3: Calculate Gross Monthly Income From Multiple Income Sources

Many people don’t draw from a single source. You might receive a weekly paycheck from a primary job, freelance income on the side, rental revenue, or investment returns and all of it counts toward your gross monthly income.

Here’s how to combine income sources step by step:

Step 1: Calculate your primary job’s gross monthly income using Method 1 or Method 2 above.

Step 2: Calculate each additional income source separately (see below).

Step 3: Add all monthly figures together.

Calculating Income From Freelance Work and Gig Economy Jobs

Self-employment income takes more work to calculate accurately, but the process is straightforward once you know it.

Use your total annual income from self-employment found on your Schedule C (net profit) or your total 1099 earnings and divide by 12. For loan applications, lenders typically use your net profit (after business expenses), not gross revenue.

If you freelanced and earned $24,000 net last year, your average monthly freelance gross income is $2,000/month.

For newer freelancers without a full year of history: use your documented monthly average for however many months you’ve operated, with a minimum of 12 months of history preferred by most lenders. Once you understand your income, creating a business budget helps you allocate that income effectively across business expenses and personal use.

Rental Income and Investment Returns

Rental income has an important nuance worth flagging. For your own budgeting, you’d subtract expenses mortgage payments, property taxes, insurance, maintenance to find your true net. But for loan qualification, lenders often count your gross rental income before those expenses. Check with your specific lender, because policies vary.

Investment income (dividends, capital gains) is included in gross monthly income only if it’s consistent over two or more years. A one-time capital gain doesn’t qualify as regular monthly income for most lenders.

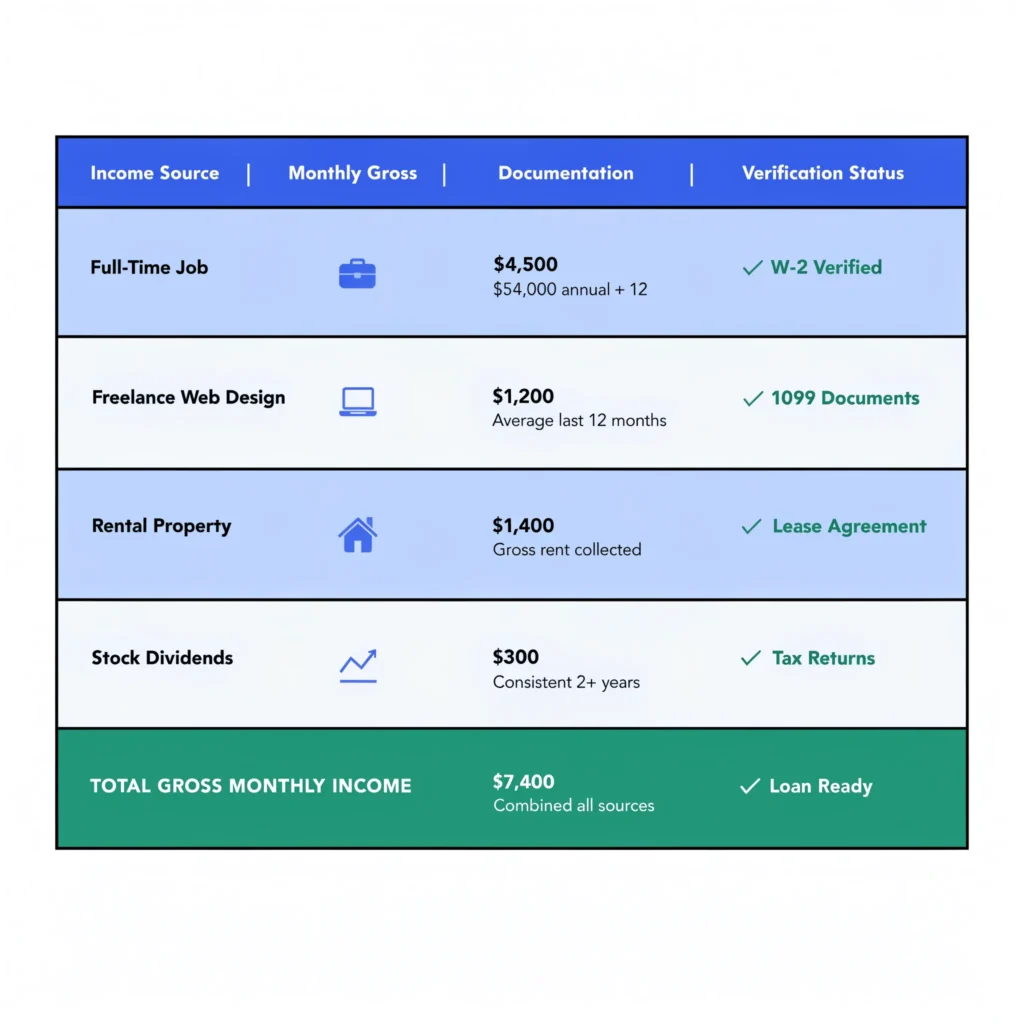

Real Example: Multiple Income Sources Combined (Sarah)

Sarah’s gross monthly income calculation:

| Income Source | Monthly Gross |

|---|---|

| Full-time job ($54,000/yr ÷ 12) | $4,500 |

| Freelance web design (avg. last 12 mo.) | $1,200 |

| Rental property (gross rent) | $1,400 |

| Stock dividends (consistent 2+ yrs) | $300 |

| Total Gross Monthly Income | $7,400 |

Documenting Multiple Income Sources for Verification

Here’s something I learned through my own loan application: calculating gross monthly income from multiple sources is easy. Proving it to a lender is a different challenge entirely. When I applied with rental income and freelance work alongside my salary, I needed three separate sets of documents something I wasn’t prepared for.

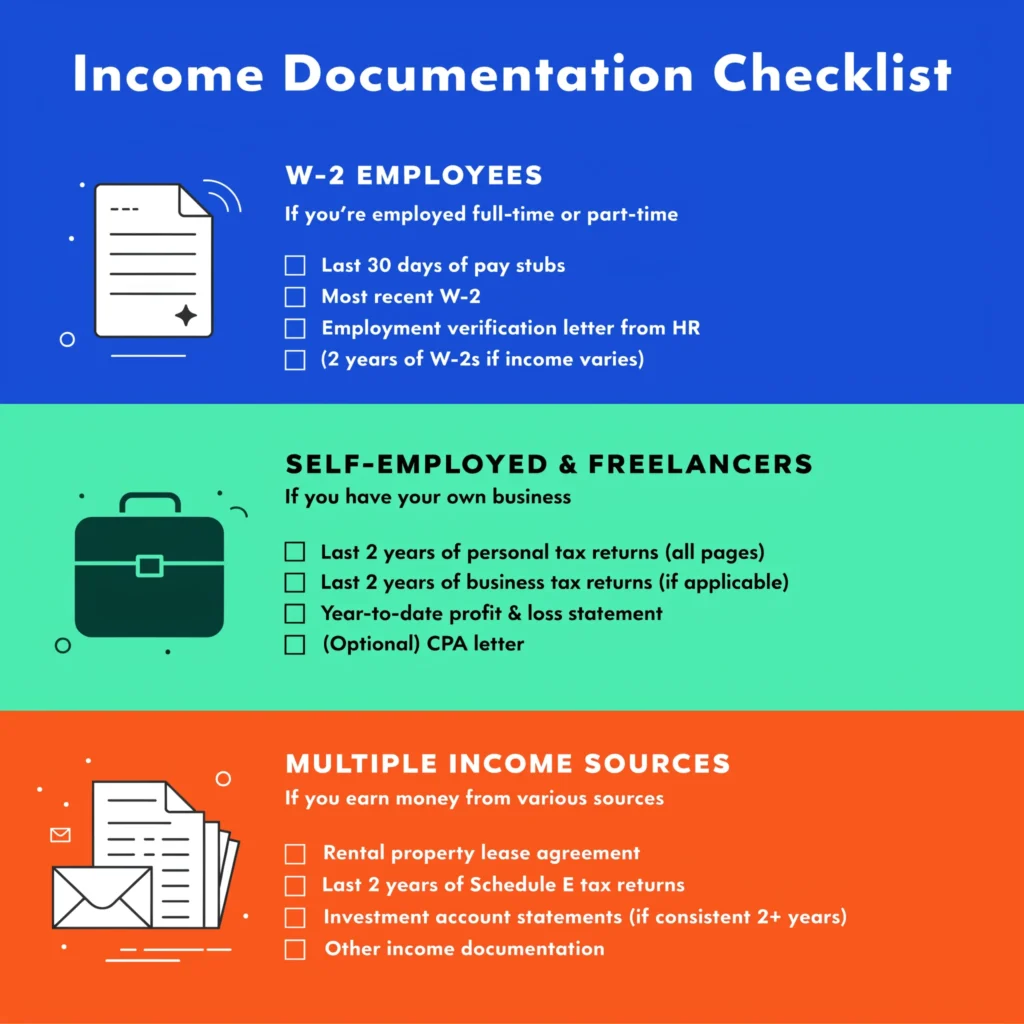

Income documentation pay stubs, tax returns, lease agreements is what separates a successful multi-source loan application from a declined one. Lenders want financial statements and documentation for every income stream you declare:

- Primary job: Last 30 days of pay stubs + most recent W-2 + employment verification letter

- Freelance/self-employment: Last 2 years of tax returns (Schedule C) + year-to-date profit/loss statement

- Rental income: Current signed lease + last 2 years of tax returns (Schedule E)

- Investment income: Last 2 years of tax returns showing consistent dividend/interest income

I always recommend requesting your employment verification letter from HR before you apply it speeds up the process significantly.

Method 4: Calculate Gross Monthly Income From a Biweekly Paycheck

Paycheck frequency matters more than most people realize. Biweekly—also written as bi weekly—means you get paid every 14 days, resulting in 26 paychecks per year not 24. Understanding whether you receive biweekly or bi weekly pay (the terms are interchangeable) affects your gross monthly income calculation. This is the most common biweekly calculation error: multiplying by 2 instead of using 26.

The Biweekly Formula

Biweekly Gross Paycheck × 26 ÷ 12 = Gross Monthly Income

Real Example: Biweekly to Monthly Gross

If your biweekly gross paycheck is $2,307.69:

$2,307.69 × 26 = $60,000 annual gross $60,000 ÷ 12 = $5,000 gross monthly income

Biweekly vs. Semi-Monthly: What’s the Difference?

- Bi weekly: 26 paychecks/year (every 2 weeks) → multiply by 26, divide by 12

- Semi-monthly: 24 paychecks/year (1st and 15th) → multiply by 24, divide by 12

These look similar but produce different results. Confirm your pay frequency with HR if you’re unsure which applies to you.

The Difference Between Gross and Net Monthly Income

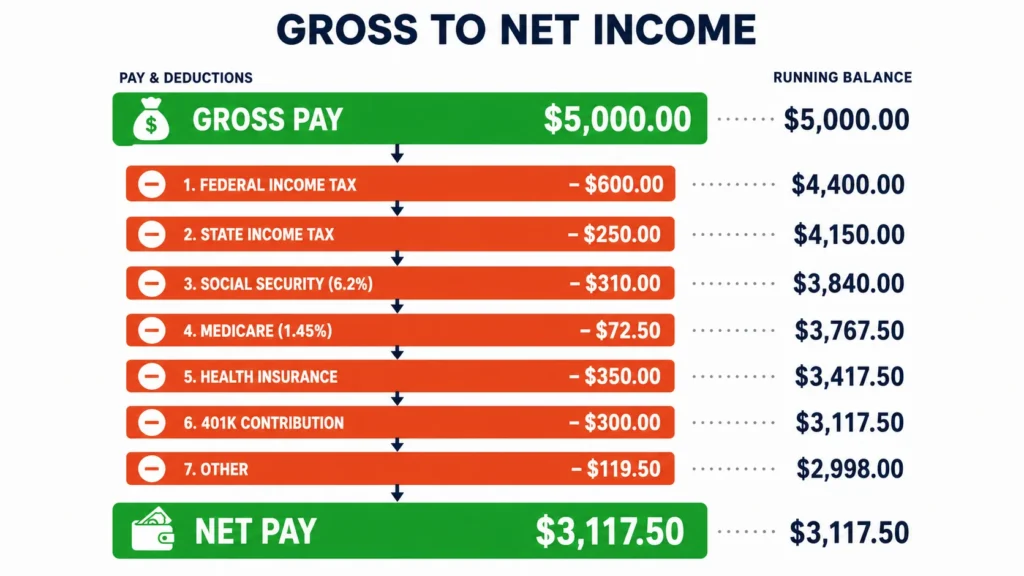

The gross vs. net distinction is the most important concept in this guide. Gross is what you earn before deductions. Net your take-home pay is what arrives in your bank account.

Here’s where the difference goes. Starting from a total amount of $5,000 gross monthly: That’s roughly 62–65% of your gross total amount reaching your bank account.

| Deduction | Amount |

|---|---|

| Federal income tax (~12% mid-range) | −$600.00 |

| State income tax (~5%, varies by state) | −$250.00 |

| Social Security FICA (6.2%) | −$310.00 |

| Medicare FICA (1.45%) | −$72.50 |

| Health insurance premium (employer plan) | −$350.00 |

| 401(k) contribution (6%) | −$300.00 |

| Total Deductions | −$1,882.50 |

| Net Take-Home Pay | $3,117.50 |

The gap varies someone in Texas with no state income tax takes home more; someone in California maxing their retirement plan takes home less.

FICA taxes Social Security (6.2%) and Medicare (1.45%) are mandatory federal deductions that come out of every paycheck regardless of income level or employer size.

For budgeting, always use your net understanding how to reduce monthly expenses with your net figure ensures you’re living within what you actually earn. For loan applications, always use your gross.

How Lenders Verify Gross Monthly Income

Knowing how to calculate your gross monthly income is only half the equation. Lenders don’t take your word for it they verify every number through documentation. If you have student debt, that also becomes part of your verification process since lenders evaluate all debt obligations. Here’s exactly what they look for.

Verification for W-2 Employees

If you’re a traditional W-2 employee, lenders typically request:

- Recent pay stubs (last 30 days minimum)

- Most recent W-2 (or last 2 years for variable income)

- Employer verification of employment letter

Lenders cross-check your stated income against year-to-date earnings shown on your pay stubs and what you reported to the IRS on your tax returns. If those numbers don’t align, expect delays.

Lenders follow Fannie Mae’s B3-3.1 income documentation guidelines for conventional loans these specify exactly what documentation is required for each income type, from W-2 employment to self-employment to rental income.

Verification for Self-Employed and Freelance Income

Self-employed borrowers face a higher documentation bar:

- Last 2 years of personal tax returns (with all schedules)

- Last 2 years of business tax returns (if applicable)

- Year-to-date profit and loss statement

- CPA letter (some lenders require this)

When I gathered documentation for my own multi-income loan application, I brought two years of tax returns, three months of pay stubs, and a signed lease for my rental property and the lender still asked for a CPA letter. Prepare for more than you think you’ll need.

Income Verification Standards: Why They’re So Strict

Income verification standards tightened significantly after the 2008 financial crisis. Lenders moved away from “stated income” loans where borrowers could report income without documentation because those loans contributed heavily to the mortgage collapse. Today, most lenders require full documentation regardless of your credit score or down payment size. Having your pay stubs, tax returns, and employment letter organized before you apply will noticeably speed up the process.

Verify Your Calculation: Using Your Pay Stub as a Double-Check

Your pay stub is the fastest way to verify your gross monthly income calculation without doing any extra math.

Look for these fields:

- Current Period Gross: Your gross for this single pay period

- Year-to-Date (YTD) Gross: Your total gross earnings since January 1

To verify your monthly gross using YTD: divide your YTD gross by the number of months completed so far this year. If your YTD gross shows $27,500 at the end of May, your monthly gross averages $5,500/month ($27,500 ÷ 5).

This method is especially useful for hourly workers with variable hours it automatically accounts for weeks where you worked more or fewer hours than usual.

Common Mistakes When Calculating Gross Monthly Income

These are the most common calculation errors I’ve seen and they’re easy to avoid once you know what to watch for.

Mistake 1: Using Net Pay Instead of Gross The single most common error. When a form asks for your gross monthly income, they want the number before deductions not your bank deposit. Your pay stub’s “Gross Pay” field is what you report.

Mistake 2: Including One-Time or Non-Recurring Payments as Regular Income Some companies issue one-time bonuses, retention payments, or end-of-year payouts that fall outside your normal pay cycle. A $3,000 year-end bonus divided by 12 adds $250/month to your stated gross but lenders will strip it out if it’s not consistent and documented over 12–24 months. Only include income you can prove is recurring.

Mistake 3: Assuming 52 Working Weeks for Hourly Calculations According to the Bureau of Labor Statistics, the average U.S. private-sector employee receives approximately 10 vacation days annually — meaning a realistic work year is closer to 48 weeks than 52 for most hourly calculations. If you get two weeks of vacation plus five personal days, you’re working approximately 47 weeks per year. Use actual hours worked, not theoretical maximum hours.

Mistake 4: Using Gross Revenue Instead of Net Profit for Self-Employment If you’re self-employed and invoiced $8,000 last month but spent $3,000 on business expenses, your gross monthly income for loan purposes is $5,000 not $8,000. Lenders use net profit from your Schedule C, not top-line revenue.

Why Gross Monthly Income Matters Beyond Loans

I’ve focused on loans because that’s where this number comes up most often. But gross monthly income drives several other financial calculations worth knowing.

Personal Budgeting: The 50/30/20 budget rule (50% needs, 30% wants, 20% savings) is designed to run off your net income but knowing your gross lets you set accurate savings targets and understand your total earning capacity.

Child Support and Alimony: Family law courts use gross monthly income to calculate child support and alimony in most U.S. jurisdictions. For example, if a parent earns $6,000 gross monthly, a court may apply the state’s percentage-of-income formula to that figure not to their take-home pay. Knowing your gross before entering any legal proceeding involving family finances is critical.

Benefit Eligibility: Many federal and state assistance programs (Medicaid, CHIP, ACA subsidies, SNAP) use gross household income thresholds to determine eligibility. Reporting net income when gross is required can disqualify you from benefits you may be entitled to or create compliance issues later.

Debt-to-Income Ratio (DTI): Beyond mortgage applications, your DTI ratio matters for auto loans, personal loans, and credit card applications. Most lenders want to see total debt payments below 36% of gross monthly income. Knowing your gross lets you calculate exactly how much new debt you can take on before hitting that ceiling.

Tools and Resources for Calculating Gross Monthly Income

Several resources can simplify gross monthly income calculations:

Your HR or payroll department is the most accurate source they have your exact compensation data. A quick call or email gets you the number directly, along with documentation that satisfies most lenders.

Your pay stub’s Year-to-Date Gross field does the calculation for you: divide the YTD number by the number of months completed in the year. No formulas required.

For freelancers and self-employed individuals, accounting platforms like QuickBooks Self-Employed or FreshBooks track income by month automatically, making 12-month averages straightforward to pull for loan applications.

IRS W-2 and 1099 forms, which you receive annually, serve as authoritative gross income documentation for both personal verification and lender submission. Box 1 on your W-2 is your gross wages for the year.

I’ve personally found that tracking monthly income in a simple spreadsheet for six months before any major loan application makes the documentation process dramatically easier you already have the averages calculated before anyone asks.

Frequently Asked Questions

Q1: What counts as gross monthly income?

Gross monthly income includes wages and salary, hourly pay, tips, bonuses, commissions, freelance/self-employment income, rental income, investment dividends, alimony or child support received, Social Security benefits, and pension or retirement distributions. It’s the total of all income streams before any deductions.

Q2: How do I calculate gross monthly income if I’m self-employed?

Use your net profit from the last 12 months (found on Schedule C of your tax return) and divide by 12. If you have two years of tax returns, lenders typically average the two years’ net profits. Avoid using gross revenue business expenses come out before lenders count your income.

Q3: Should I include bonuses in my gross monthly income?

Yes, include them, as long as they’re regular and documented. A bonus you’ve received for two or more consecutive years, documented on your W-2, qualifies. A first-time or discretionary bonus typically doesn’t count until there’s a history.

Q4: How do I calculate household gross monthly income if I’m married or partnered?

Calculate each person’s gross monthly income separately using the methods above, then add them together. On joint loan applications, lenders combine household income and apply the DTI test to the combined figure against all combined debts.

Q5: What’s the difference between gross monthly income and net monthly income?

Gross is before all deductions. Net is after federal and state income tax, FICA (Social Security + Medicare), health insurance premiums, retirement contributions, and any other payroll deductions. For a $5,000 gross paycheck, you might net $3,100–$3,700 depending on your state, tax elections, and benefits.

Q6: Why do lenders use gross income instead of net income?

Gross income is consistent and comparable across all borrowers. Two people with identical gross incomes may have very different net incomes based on state of residence, retirement contributions, and health plan elections none of which reflect their actual earning capacity. Gross removes those variables.

Q7: How often should I recalculate my gross monthly income?

Recalculate any time your compensation structure changes raise, new job, new freelance client, changed hours, or added income source. For loan applications, lenders want income documentation from the last 30–60 days, so your current figure matters more than last year’s.

The Bottom Line

Knowing how to calculate gross monthly income puts you in control of your financial situation. You understand your true earning capacity, you can run the key financial ratios yourself, and you can walk into any lender conversation with confidence rather than guesswork.

Gross monthly income your total monthly earnings before any deductions is the number the financial world runs on. Lenders use it to approve loans. Courts use it to calculate support payments. Benefits programs use it to set eligibility. Getting this number right, and knowing how to document it, is a foundational financial skill.

The four methods in this guide cover every common pay structure:

- Method 1: Annual salary ÷ 12

- Method 2: Hourly rate × hours × 52 ÷ 12

- Method 3: Multiple sources added together

- Method 4: Biweekly paycheck × 26 ÷ 12

Pick the method that fits your pay structure, verify it against your pay stub’s year-to-date gross, and you’ll have a reliable, lender-ready number.

Note: Tax rates, DTI thresholds, and lender requirements can change. For loan-specific decisions, always verify current guidelines with your lender or a licensed financial advisor.