How to Reduce Monthly Expenses: 7 Ways That Work

Every month I used to wonder where my money went. I’d check my bank account mid-month and feel genuinely confused. I wasn’t buying anything big. I wasn’t living lavishly. But the balance kept shrinking faster than it should, and the cost of living wasn’t getting any easier.

That feeling pushed me to dig deeper, and what I found surprised me. The problem wasn’t one large expense. It was dozens of small ones I’d never stopped to look at.

If you want to know how to reduce monthly expenses in a way that actually sticks, you don’t need extreme sacrifices. You need a clear picture of where your money is going and a set of proven changes that free up real cash. I’ve tested these strategies on my own budget and pulled insights from people who’ve done the same. That’s what this article covers.

The Step Most People Skip Before Cutting Anything

Before you cut a single expense, you need to know what you’re actually spending. Most people skip this entirely, and it’s why their budget never improves no matter how many tips they read.

I used to think I had a rough idea of my monthly spending. I was wrong. When I finally sat down and tracked every transaction for 60 days, I found money leaking out in places I hadn’t opened in months.

I wasn’t alone. One family tracked every dollar for two full months and discovered they were spending $400 more per month than they earned. Regular overtime had masked the gap completely. The moment they saw the real number, everything changed.

Expense tracking does one thing really well: it replaces a vague financial unease with specific numbers you can actually do something about.

Here is my actual process. I pull three months of bank and credit card statements and go through them line by line. I write everything into categories: housing, food, transportation, subscriptions, entertainment, and personal spending. When it’s all laid out together, the patterns jump out immediately. Expense tracking like this takes maybe an hour the first time and reveals months of financial planning decisions you never consciously made.

You don’t need a perfect monthly budget from day one. You just need to see where your money is actually going right now. You cannot cut what you cannot see, and most people have never actually looked.

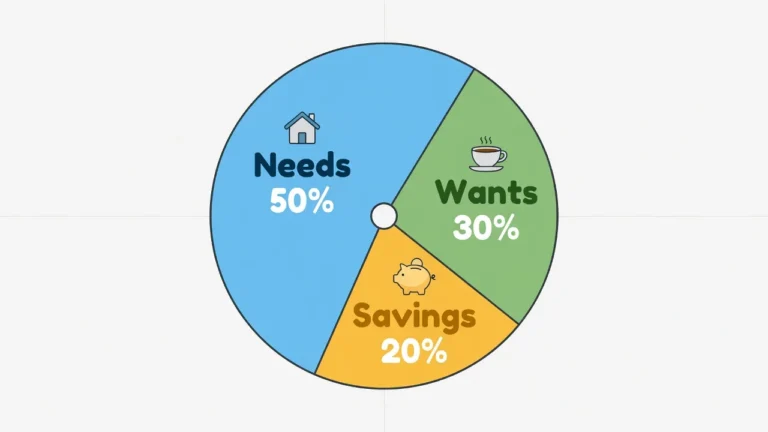

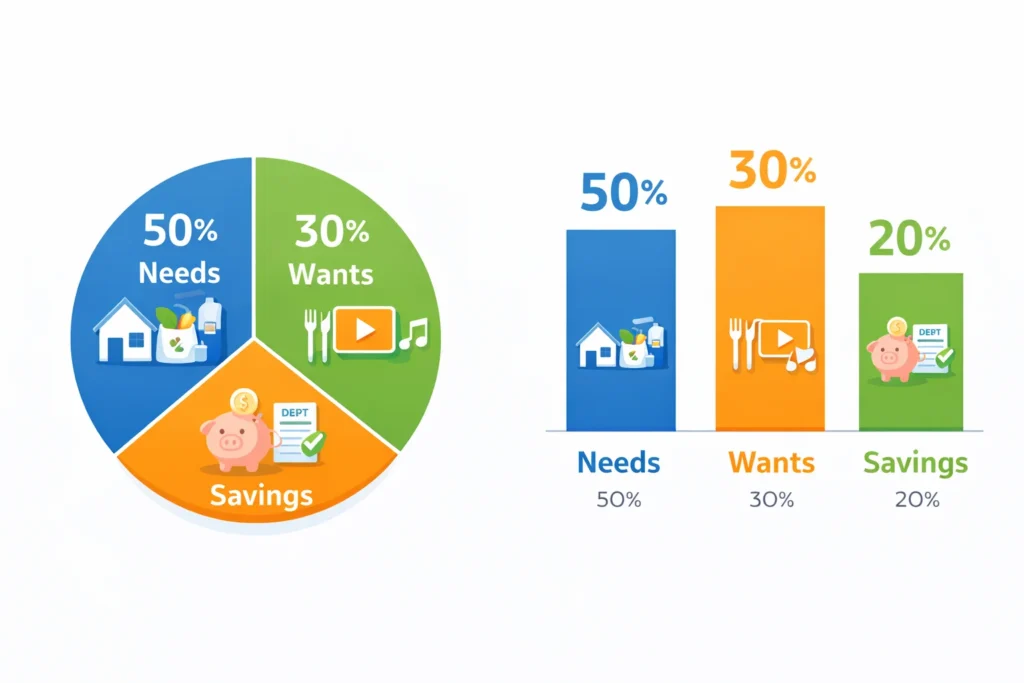

A budgeting method I found genuinely useful when I started was the 50/30/20 rule. It divides your net income, your actual take-home pay after taxes, into three categories. Fifty percent covers needs: rent, groceries, utilities, and insurance. Thirty percent is for wants: dining out, streaming services, and hobbies. The final twenty percent goes to savings and debt repayment.

When I first ran my numbers through this framework, my wants were sitting closer to 45 percent. That alone told me where the work needed to happen. Use it as a starting point, not a verdict on your spending.

Fixed vs. Variable Expenses: Which Ones You Can Actually Control

Once you’ve tracked your spending, you’ll notice two types of expenses.

Fixed expenses stay the same every month regardless of what you do: rent, mortgage payments, insurance premiums, and loan payments. You can reduce them, but it usually requires a bigger decision like refinancing, switching providers, or moving.

Variable expenses shift month to month. Food, entertainment, personal shopping, and subscriptions all fall here. This is where your fastest savings live, because you can adjust them starting this week.

When I started cutting expenses, I focused almost entirely on variable costs first. The wins came within days, and I didn’t have to upend anything major to find them.

How to Find and Reduce Recurring Monthly Expenses

Most people have recurring charges they’ve completely forgotten about. This is one of the fastest ways to reduce recurring monthly expenses without changing your lifestyle at all.

Go through your bank and credit card statements and highlight every charge that repeats monthly. Pay special attention to anything between four and twenty dollars. These are usually old app subscriptions, free trials that silently converted to paid plans, or auto-ship orders you set up once and never thought about again.

Also watch for auto-ship programs from supplement or household product companies. They advertise a ten or fifteen percent discount for subscribing, which seems reasonable. But if the product ships faster than you use it, you’re paying for inventory you don’t need and can’t return.

One pass through your statements can free up thirty to eighty dollars a month that’s currently doing nothing for you. That’s a real number from something that takes under an hour to fix.

Try the 10% Challenge Before Changing Anything Else

Here is the fastest way to cut monthly expenses without rebuilding your budget from scratch.

Sit down with someone you trust, a partner, a friend, or just yourself with a hot drink and twenty minutes. Look at your total monthly spending and ask one question: where can I trim ten percent of this?

That is the 10% Challenge. It is one of the most effective cost cutting strategies I have tried because it is small enough to feel achievable but broad enough to produce real results.

If you are spending two thousand dollars a month, you are looking for two hundred dollars in cuts. In my experience, that amount almost always exists somewhere. You just have not looked at it all together before.

When I tried this, I found three things quickly: a subscription I had been keeping just in case, a phone plan with data I never used, and a gym membership I visited twice in three months. Together they added up to almost ninety dollars a month. That was money I could redirect toward my actual financial goals.

The broader idea here is simple: try to live on as little of your income as you comfortably can. The mindset alone stops you from casually adding new expenses month after month.

The Real Reason You Keep Overspending (It’s Not Willpower)

I used to think people who overspent just lacked discipline. Then I realized I was one of them, and that forced me to look at the problem differently.

Overspending usually has nothing to do with willpower. It’s about exposure. The more you see things you want, the more frequently you buy them. Remove the exposure and the spending drops on its own.

Three things quietly drive most people’s consumer spending without them ever recognizing what’s happening.

The first is social media. Platforms are full of people sharing what they bought, what they’re wearing, where they’re traveling. Many of them are influencers whose entire job is to make you want something you didn’t want an hour ago. Seeing a product repeatedly creates familiarity, and familiarity quietly becomes desire before you recognize what happened.

The second is convenience spending. When you’re tired, delivery feels like a practical solution. When you’re bored, browsing an online store feels harmless. These aren’t character flaws. They’re predictable responses to your environment, and understanding that changes how you respond to them.

The third is what I think of as want creep. It’s the slow process where spending habits shift your wants into perceived needs over time. The streaming service you added as an occasional treat becomes a line item you never question. The daily coffee you started as a small ritual becomes something that feels non-negotiable. None of those were genuine needs when they started.

The fix for all three is awareness, not restriction. When you understand why you’re spending, you can make a deliberate choice instead of a reflexive one.

Something that has genuinely helped me is treating contentment as a budget tool. When I feel satisfied with what I already have, the pull toward new purchases weakens noticeably. That doesn’t mean never treating yourself. It means the treat feels like a real choice rather than something you fell into.

Why Unfollowing Certain Accounts Could Save You Hundreds a Month

I tried this myself after reading about it and honestly didn’t expect it to do much.

One well-known personal finance educator shared that she had to unfollow and mute certain social media accounts because clothing and lifestyle content kept making her want to buy things she hadn’t considered before seeing them. She didn’t judge herself for it. She removed the trigger and moved on.

I did the same thing. I unfollowed about a dozen accounts in one sitting. Within two weeks I noticed I was buying less without consciously trying to. The passive scroll had been doing real damage to my discretionary spending without me ever connecting the two.

Look at your own feed. Are there accounts that consistently make you feel like you’re missing something? Unfollowing them is not a dramatic act. It is a practical budget decision.

You can reinforce this by removing saved payment cards from your favorite shopping sites. No stored card means you have to actively enter your details before buying. That thirty-second friction is often enough to break the impulse.

You’re Probably Paying for 17 Subscriptions Right Now

The average millennial has around 17 active subscriptions. More striking is that most people pay approximately $133 more per month on subscriptions than they believe they do.

That gap isn’t a minor oversight. It’s a meaningful monthly drain hiding in plain sight, spread across charges small enough that none of them individually feel worth canceling.

Subscription services are designed to be forgettable. A charge for $6.99 doesn’t register as money leaving your account. But three of those, plus an auto-ship order you signed up for once, plus a music service you open twice a week, plus a premium app you upgraded eight months ago and have used twice since these small charges add up quickly to forty to eighty dollars a month that is delivering almost nothing.

The solution is a dedicated subscription audit. Block thirty minutes, go through three months of bank and credit card statements, and list every recurring charge. For each one, ask a single question: did I actually use this enough last month to justify the cost? If the answer is no, eliminate that unnecessary expense today, not eventually.

The Streaming Rotation Strategy That Saves $20 or More Per Month

Most people pay for three or four streaming services simultaneously and watch one or two of them.

One approach works much better. Subscribe to one service at a time, watch everything you want from it, and then cancel before the next billing cycle. Switch to a different service and repeat.

Couples and families who do this consistently report saving twenty dollars or more each month compared to keeping multiple services active. You watch more intentionally, waste less, and spend less.

A simple way to manage this is to keep a note on your phone with the show or series you want to watch next and which platform it’s on. When you finish your current service, you always know where to go next.

Where Families Quietly Waste $3,000 a Year on Food

Food costs are one of the largest variable expenses in most household budgets, and they’re also one of the most responsive to simple changes.

The average American family of four spends around $3,000 a year eating out. That works out to $250 a month on restaurants and takeout, usually not because anyone planned it that way, but because cooking felt like too much effort at the end of a long day.

Meal planning is the single most effective change I made to reduce food costs. Spending twenty minutes at the start of each week deciding what I’d actually cook removed the moment I’d stand in the kitchen at 6pm with no plan and reach for my phone to order delivery. That daily moment of indecision was costing me real money every week.

Prepare some food in advance when you have the time. Cut vegetables on Sunday. Cook a batch of protein that works across multiple meals. The more ready-to-eat food you have waiting, the less power hunger has over your grocery expenses and your delivery apps.

One more: never grocery shop while hungry. Every time I’ve done it I’ve spent more than I planned.

The Pantry-First Rule That Cuts Your Grocery Bill Before You Even Shop

Before you write your next grocery list, open your fridge, freezer, and pantry and actually look at what’s in there.

One family committed to reducing their grocery budget to $100 a month for four people by eating what they already owned first. Their pantry and freezer were so full that items were falling off the shelves. They realized they had been buying new food while older food sat quietly expiring in the back of the fridge.

Most households have more food available than they think. Eating through what you own before shopping again cuts waste, lowers your grocery bill, and often turns into a surprisingly fun meal challenge.

Does a Costco or Sam’s Club Membership Actually Save Money?For most households, yes, a club membership saves money, but the savings depend entirely on what you buy there.

Bulk buying makes financial sense for non-perishable staples you use regularly and predictably. Paper products, cleaning supplies, canned goods, and frozen proteins are categories where the per-unit price at a warehouse club is meaningfully lower than standard grocery pricing. Most households recover the annual membership fee within the first two or three months of regular shopping.

Gas is another genuine benefit if you drive frequently. Many clubs offer fuel at a consistent discount compared to nearby stations.

Where people lose money is buying perishables in bulk. I made this mistake early on. I bought a large pack of salad greens thinking I’d eat through them quickly. Half of it ended up in the trash. Stick to items with long shelf lives and bulk buying will reliably save you money month over month.

The Impulse Buy Problem and the Rule That Actually Fixes It

Impulse purchases are one of the quietest expense leaks in most budgets. The item feels completely reasonable in the moment. It’s only later, when you see it on your statement, that you wonder what you were thinking.

The most effective tool I’ve found is the waiting period rule. Before buying anything non-essential, I wait. For small items I hold off at least seven days. For mid-sized purchases I give it thirty days. For large purchases I wait up to ninety days.

What I’ve learned from that waiting period is revealing. About half the time, the desire simply evaporates. The item I was convinced I needed becomes something I’ve forgotten entirely. That tells me it was never a real need.

If the desire is still there after thirty or ninety days, I know it’s a considered decision worth making, not a reaction to a moment of excitement. I also use that waiting period to do some comparison shopping and find the best available price before I commit.

Why Paying With Cash Stops Overspending Faster Than Any App

When you physically hand over cash, your brain registers that exchange as a loss in a way that tapping a card simply does not trigger.

I noticed this the first month I tried the envelope method for my dining and personal spending categories. With a card, I’d spend without thinking. With cash in a physical envelope, I’d pause before every purchase and actually ask myself whether it was worth it. By the third week I still had money left, which had never happened before with those categories.

The process is simple. At the start of each month, put your budgeted amount for discretionary spending in a physical envelope for each category. When it’s empty, the spending stops for that month.

It requires no app, no tracking, and no willpower beyond the initial decision to set it up. The constraint is built into the system.

The Smartest Ways to Reduce Monthly Bills With One Phone Call

Most people have never tried to negotiate their bills. Those who do often give up at the first unhelpful response from a standard customer service representative and assume there is nothing more to be done.

There is. Negotiating your internet, cable, phone, and insurance bills is one of the most reliable paths to big savings because the effort is a single phone call and those savings repeat automatically every month after that.

Here is what most people do not realize: the first person you reach when you call has very limited authority to offer discounts. You are talking to the wrong department.

The Three-Step Negotiation Sequence That Works on Internet, Cable, and Phone Bills

Step one is to call during a weekday in the early afternoon. Weekday afternoons have shorter wait times and give you access to fully staffed teams. Call on a Monday morning and you’ll wait much longer.

Before you call, pull out your most recent bill. Know your account number. Note any specific fees listed on the bill, including things like equipment rental fees, network enhancement charges, or administrative fees. These are targets.

Also spend five minutes looking up what the same company is currently offering to new customers, or what a competitor is charging. This gives you specific numbers to reference.

Step two is to ask to be transferred to the Customer Retention Team. Say those words exactly. Standard customer service representatives often cannot offer meaningful discounts. The retention team exists specifically to prevent you from canceling, and they have access to deals that general support does not.

When you reach them, be friendly and direct. Mention that you’ve been a loyal customer, that the bill feels higher than expected, and that you’ve seen better offers available. Ask if they can match it or do better.

Step three is to lock in whatever they offer. Ask how long the rate is locked in, whether any new fees are being added, and request a confirmation email with the details. That email is your proof if the discount disappears on the next bill.

In one live demonstration, this process reduced an internet bill from $93 to $75 by removing a router rental fee, adding an autopay discount, and upgrading the plan speed at no additional cost. That single call saved over $200 in the first year.

This process doesn’t work every time with every provider. But in my experience attempting it across three different service accounts, two resulted in meaningful savings and one required the step below.

What to Do When They Say No (The Win-Back Strategy)

If the retention team doesn’t offer something workable, you still have two options.

The first is to hang up and call back another day. Different agents have different authority and different flexibility. I’ve had one call end with nothing and the next call three days later result in a significant reduction on the same account.

The second is to actually cancel. Canceling sometimes triggers an outbound call from a win-back team within a few days, and they typically have access to better offers than the retention team was offering. Several people I know have gotten their best pricing only after they walked away.

Your Utility Bills Are Higher Than They Need to Be

Most people treat their utility bills as a fixed cost and never look at them closely. That assumption is usually costing them ten to twenty percent more than necessary.

The first energy saving tip worth acting on immediately is switching to LED bulbs in your most-used fixtures. LED bulbs use roughly 80% less energy than incandescent ones. I swapped out the lights in my kitchen and main living areas and noticed a drop on my next bill without changing anything else.

Unplugging electronics when not in use stops what’s called phantom power draw. Televisions, gaming consoles, phone chargers, and kitchen appliances all pull electricity while plugged in even when turned off. A power strip with a switch makes it easy to cut the draw for a whole section of the room at once.

Turning down your heating or air conditioning a few degrees while you’re sleeping is one of the easiest changes you’ll never notice. You’re unconscious. Your energy bill is not.

One more worth five minutes of your time: call your utility provider and ask about paperless billing and autopay discounts. Many providers knock five to ten dollars off your monthly bill just for enrolling in both. The savings recur automatically without any additional effort.

Also worth doing is contacting your utility provider and asking about paperless billing and autopay discounts. Many providers offer between five and ten dollars off your monthly bill just for enrolling. It takes about five minutes and the savings repeat automatically every month.

Free Energy Fixes You Can Do in the Next 10 Minutes

Some energy savings require nothing: no purchases, no tools, no appointments.

Turn lights off when you leave a room. During the day, open the blinds and use natural sunlight before switching on overhead lights. Check the seals around your windows and doors by holding a piece of paper near the edge on a windy day. If the paper moves, you’re losing heated or cooled air through a gap that a few dollars of weatherstripping can seal.

Set your water heater to 120 degrees Fahrenheit if it’s currently higher. Most households have it set hotter than they ever actually need and pay for that heat every single month.

None of these changes are dramatic individually. Together, they typically reduce a household’s energy bill by ten to twenty percent, which adds up to real money across a full year.

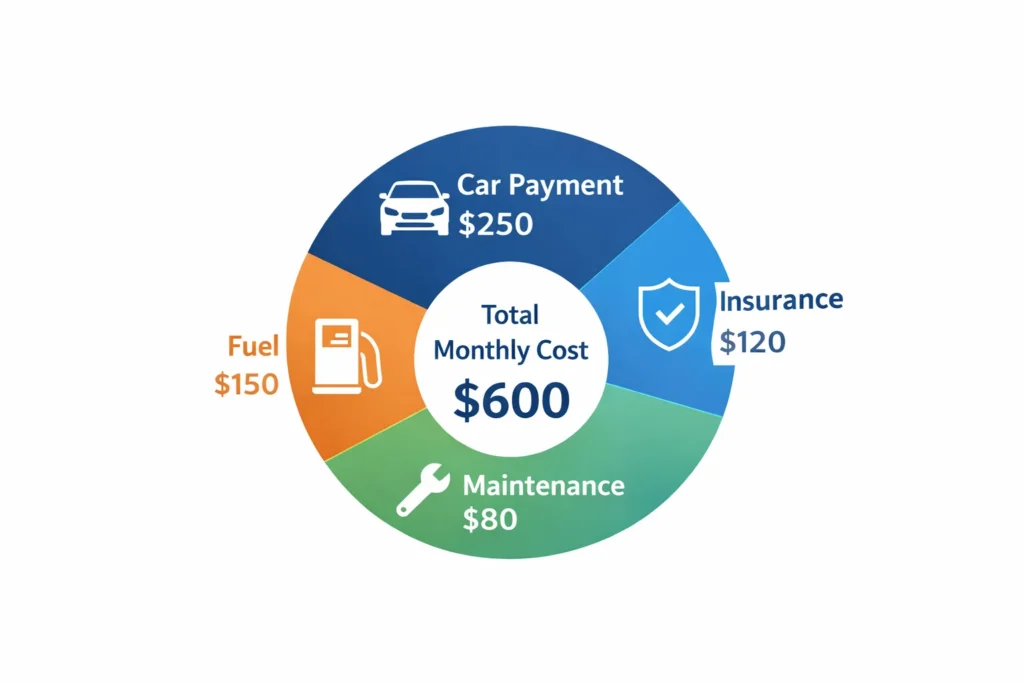

How Much Your Car Is Really Costing You Each Month

Most people look at their car payment and think that’s the main cost. But a car actually carries four expenses every month: the loan payment, insurance premiums, fuel, and maintenance. Add those up and most households are spending three hundred to six hundred dollars or more monthly on a single asset that sits parked the majority of the time.

Transportation costs are worth treating as a full category, not just a car payment. If you live in an area where public transportation is a realistic option, even replacing one or two car trips per week with a bus or train can meaningfully reduce your monthly fuel and parking costs.

The highest-impact move is comparing your insurance premiums annually. Providers vary significantly in price for identical coverage. I shopped my policy last year after ignoring it for three years and found a lower rate for the same coverage in about twenty minutes.

Using a free gas price app before you fill up is a small habit that compounds over the year, especially if prices vary by fifteen to twenty cents between nearby stations, which they often do.

Some insurers offer voluntary tracking devices that monitor your driving habits and lower your premiums if you drive carefully and cover fewer miles each month. I enrolled in one of these programs and my rate dropped after the first review period.

Checking your oil and coolant every couple of weeks is genuinely worth your time. Engine problems caused by low fluids can cost thousands. The check itself takes five minutes.

The Car Payoff Trick That Turns a Loan Into a Savings Account

When you finish paying off a car loan, do not change anything about your monthly behaviour.

Keep making the exact same payment, but send it to your own savings account instead of to the lender. Over time, you’ll earn interest on this growing balance you can see how the interest compounds over time to understand what your consistent deposits will be worth down the road.

You have spent months or years building the habit of setting aside that amount each month. The habit is already formed and the money is already accounted for in your mental budget. All you are doing is changing the destination.

People who do this save money monthly without ever feeling like they made a sacrifice, because the money was already leaving their spending budget. You just redirect it toward yourself instead.

How to Reduce Monthly Household Expenses Without Sacrifice

Housing costs are the largest fixed expense for most people, and there are more options to reduce what you pay than most people explore.

If you rent, the most direct move is getting a roommate to split the cost. House hacking, meaning renting out a spare room or a separate unit you own, can cover a meaningful portion of your mortgage and taxes. I know several people who effectively live for free this way.

If downsizing is something you’d consider, moving to a smaller space cuts both rent or mortgage and utility bills at the same time. The frugal living math here compounds in your favor from two directions simultaneously.

For day-to-day household products, simple DIY alternatives make a real difference. A mix of white vinegar and water handles most hard surface cleaning. I switched to this about two years ago and haven’t bought a single bottle of kitchen cleaner since. Reusable cloth replaces paper towels for the majority of tasks. Dryer balls replace fabric sheets and last for years.

For entertainment, your public library is one of the most genuinely underused resources available. Many libraries now provide free access to ebooks, audiobooks, streaming services, digital magazines, and local event passes in addition to physical books. Check your library’s digital offerings if you haven’t looked recently. The catalog has expanded considerably in the last few years and a library card costs nothing.

Generic vs. Name Brand: Where the Savings Are Real and Where They’re Not

Not every generic product is worth switching to, but many of them are.

For pantry staples like rice, flour, canned goods, pasta, cooking oil, and spices, store brands are often manufactured by the same producers as the name brands and packaged differently. In my experience the quality is indistinguishable, and the price difference is typically thirty to fifty percent.

For cleaning supplies, generic versions of dish soap, laundry detergent, and all-purpose cleaners typically perform just as well as premium brands at significantly lower prices.

Where I’m more cautious is with tools, electronics, and certain health products. A cheap version of something you depend on daily often costs more over time because it breaks faster and needs to be replaced. For items you’ll use frequently over many years, the cost per use of a quality product is usually lower than the cost per use of a cheap one. Frugality isn’t always about buying the least expensive option. Sometimes it’s about buying the one that lasts longest.

The Debt Payments Draining Your Budget Every Month

Debt payments are unique among monthly expenses because they deliver nothing today. You are paying for past decisions with present income, and if those balances carry high interest rates, the cost grows every single month you carry them.

Credit card debt is the most damaging because the interest compounds continuously. Paying only the minimum keeps the balance alive and growing. I carried a credit card balance for two years before I really understood how much interest I was paying. When I finally added it up, the number was genuinely shocking.

The most effective approach to paying it down faster is to focus every extra dollar on the balance with the highest interest rate first. Once that is cleared, move everything you were paying on it to the next highest rate. This is sometimes called the debt avalanche method and it minimizes the total interest you pay over time.

If you carry multiple types of debt, it may be worth looking into whether refinancing loans into a consolidation loan could reduce your overall monthly payment and interest rate simultaneously.

Also review the fees on your banking and credit accounts. Credit card fees, ATM fees, monthly maintenance fees, and foreign transaction fees are all avoidable. Most banks offer a no-fee checking option if you ask for it or look for one. Using your own bank’s ATM network eliminates withdrawal fees entirely at no cost.

Build an emergency fund alongside your debt payoff even though it feels counterintuitive to save while paying interest. Six to twelve months of essential expenses in savings means an unexpected car repair or medical bill does not send you back into high-interest debt and erase months of progress.

When You’ve Cut Everything: What to Do Next to Lower Monthly Living Costs

There comes a point where you’ve genuinely done the work. You’ve audited subscriptions, negotiated bills, reduced grocery spending, and built better habits. And somehow you’re still not reaching your financial goals.

What most personal finance content never acknowledges is that there is a floor to how low your expenses can go.

Food costs can only go so low before meals become unpleasant. Living space can only shrink so much. Some costs are simply real and unavoidable. Trying to reduce living expenses beyond that floor produces diminishing returns and increasing frustration.

When you have genuinely reached that point, the next move is not to squeeze harder. It is to earn more. Developing a skill, building a side income, or advancing in your current role can increase your monthly income by more than any remaining expense cuts could free up.

That shift in focus is the natural next step for someone who has already done the hard work to cut costs and bring their monthly expenses under control.

DIY Skills That Pay for Themselves in One Use

There is one more cost-reduction category worth exploring before you shift focus to income: basic skills that replace expensive service calls.

The first time I changed my own cabin air filter, it took eight minutes. I looked up my car model, watched a short video, popped out the glove compartment, slid the old filter out, and slid a new one in. No tools required. The dealership had quoted me ninety dollars for that same task. The replacement filter cost twelve dollars.

That experience changed how I thought about frugal living. I had been paying professionals to do things I could do myself in under ten minutes.

Rotating tires requires a floor jack and a torque wrench. Together those tools often cost less than a single shop visit, and they last for years. Changing your oil saves thirty to fifty dollars each time compared to a quick-change shop.

For home repairs, free video tutorials online walk you through fixing a running toilet, replacing a light switch, unclogging a drain, and dozens of other tasks. Most take under thirty minutes. Calling a professional for work you could learn in an afternoon is one of the most consistently expensive habits a homeowner can break.

Frequently Asked Questions

How do I find subscriptions I forgot I’m paying for?

Go through three months of bank and credit card statements and look for every recurring charge. Pay close attention to small amounts between four and fifteen dollars that appear monthly. These are often forgotten app subscriptions, free trials that became paid plans, or auto-ship orders. A budgeting app connected to your accounts will flag recurring charges automatically, which makes this process much faster. Once you have a complete list, go through each one and ask whether you used it enough last month to justify the cost.

What is the 7-day rule for expenses?

The 7-day rule means waiting at least seven full days before buying any non-essential item. The impulse to buy something typically fades within a week when you don’t act on it immediately. For mid-sized purchases you might extend this to thirty days, and for large purchases up to ninety days. Removing saved payment cards from shopping websites reinforces this naturally because the extra friction of entering your card details manually adds a decision point to every purchase.

What is the 50/30/20 rule of money?

The 50/30/20 rule divides your after-tax take-home income into three categories. Half goes to genuine needs: housing, groceries, utilities, insurance, and transportation. Thirty percent covers the things you want but could live without: dining out, streaming services, entertainment, clothes, and hobbies. The remaining twenty percent is for savings and paying down debt. The rule works best when you write it down and map your actual spending against it. Most people discover their wants category is running well above thirty percent, which is exactly the kind of clarity this framework is designed to provide.

How do I lower my monthly expenses when I’ve already cut the obvious things?

Start with the areas most people overlook. Call your internet and phone provider and ask specifically for the Customer Retention Team. Rotate streaming services instead of keeping multiple active at the same time. After paying off a car loan, redirect that payment into savings rather than spending it elsewhere. Learn a few basic DIY skills to replace costly service calls. And consider unfollowing social media accounts that consistently trigger spending. If you’ve genuinely optimized everything, the most effective next move may be increasing your income rather than cutting further.

Does negotiating your bills actually work?

Yes, and more reliably than most people expect. The key is asking to be transferred to the Customer Retention Team rather than speaking only with standard customer service. Retention agents have access to discounts and offers that general representatives cannot provide. Calling on a weekday afternoon, having your account number and a list of any itemized fees ready, and referencing competitor pricing all improve your outcome. In one documented example, a single phone call reduced an internet bill from $93 to $75 by removing a router rental fee, applying an autopay discount, and improving the plan. That’s over $200 saved in the first year from one call.

What are 7 ways to save money fast?

The seven fastest-impact actions are: audit your subscriptions and cancel the ones you don’t use actively; try the 10% Challenge with a partner in twenty minutes; call your internet or phone provider and ask for the Customer Retention Team; stop eating out for one full month and replace it with planned home cooking; switch to a more affordable phone plan if you’re on a premium carrier; unplug electronics when not in use and lower your thermostat a few degrees at night; and look through your home for ten items you no longer use and sell them.

How much money can you realistically save by reducing monthly expenses?

Savings depend on where you start, but real-world results from people who’ve done this work are encouraging. A thorough subscription audit often frees up $130 or more per month. A single bill negotiation call can save over $200 annually. Switching from frequent takeout to home cooking saves most households $200 to $300 per month. Moving to a more affordable phone plan saves around $30 per month. Basic DIY maintenance saves hundreds per year. Combined, most households that work through the strategies in this article can realistically free up $300 to $600 per month without making changes that feel like deprivation.

Learning how to reduce monthly expenses is less about sacrifice and more about attention. Most of the money that leaves your account unnecessarily does so quietly, in small amounts, through habits you set up once and never looked at again.

Most of those leaks are fixable in an afternoon. A subscription audit, a bill negotiation call, a meal plan for the week, a social media unfollow, and a decision to keep the paid-off car. None of these require hardship. They just require looking.

Start with the 10% Challenge this week. Find twenty minutes, sit with your last three months of spending, and ask where ten percent could be trimmed. Most people find the savings faster than they expected. And that first win, however small, is usually the start of something much bigger for your overall financial wellness and long-term financial freedom.