How to Avoid Tax on Savings Account Interest Legally

When I first discovered how to avoid tax on savings account interest legally, it completely changed how I managed my money. But before I share those strategies, you need to understand something that surprised me: your bank is already reporting every penny of your savings account interest to the tax authority.

Whether you’re in the UK or the US, this happens automatically without your knowledge.

In the UK, banks report everything to HMRC. In the US, your financial institution sends you and the IRS a Form 1099-INT showing all your reportable interest income. You don’t get to choose whether to report it. The system already knows.

What shocked me most was the scale of this. According to official HMRC data, they collected £1.4 billion from savings interest in the 2021/22 tax year.

By 2024/25, that figure is expected to jump to £10.2 billion. That’s a massive increase, and it tells me people are earning more interest but also paying far more tax than they realize.

If you’re employed and paid through PAYE in the UK, the process is even more automated. HMRC doesn’t send you a separate bill for taxable interest income. Instead, they quietly adjust your tax code so the money comes straight out of your salary. You might notice your monthly pay slip shrinking without understanding why.

In the US, things work a bit differently, but the outcome is the same. Come tax filing time, you’re responsible for reporting that interest as ordinary income and paying federal income tax on it, often at your marginal tax rate.

The key point I want you to understand is this: thinking you can quietly earn interest without the tax authority knowing is not realistic anymore. The reporting happens behind the scenes, every single tax year.

What Changed in 2016 That Most Savers Don’t Know About

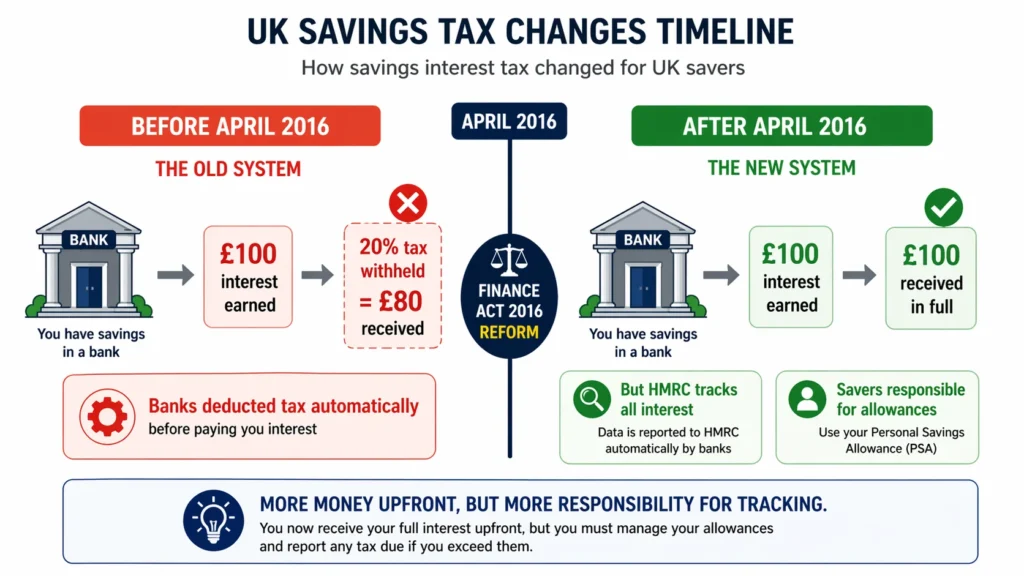

Before 2016, banks in the UK used to deduct tax from your interest automatically before paying you. If you earned £100 in interest, you might only see £80 hit your account because the bank took the tax at source.

That system changed in April 2016 when HMRC implemented the Personal Savings Allowance under the Finance Act 2016. Now, banks pay you gross interest. You get the full amount upfront. But many people miss this critical detail: banks still report every penny you earn directly to HMRC.

I think a lot of savers assume the old system is still in place, or they believe that because they’re receiving the full amount, no one is tracking it. That’s not true. The tracking actually got more comprehensive after the change, not less.

This shift in savings account tax treatment means you’re responsible for staying aware of your allowances. The interest is paid gross, but it’s still treated as ordinary income for tax purposes. If you go over your limits, HMRC will come looking for what’s owed, usually by adjusting your tax code or including it in your self-assessment if you file one.

How Much Savings Interest Can You Actually Earn Tax-Free?

The good news is that even though your bank reports everything, you can still earn a significant amount of interest without paying a penny in tax if you know how the allowances work.

Let me show you the three main allowances available in the UK. Most people only know about one of them, and that’s a real shame because combining all three can shelter a surprising amount of interest earned on savings accounts. Understanding these interest income thresholds is the key to keeping more of your money.

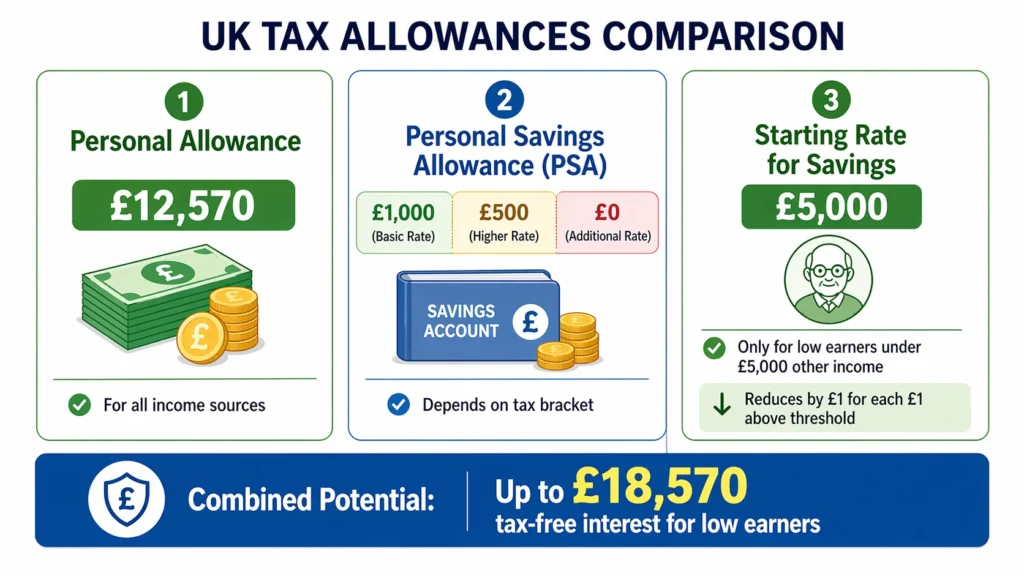

The first is your Personal Allowance. That’s the £12,570 you can earn each year before paying any income tax at all. If your only income is savings interest and it’s below that threshold, you pay nothing.

The second is the Starting Rate for Savings, which I’ll cover in detail below. It’s a hidden gem that low earners and retirees often miss.

The third is the Personal Savings Allowance, or PSA, which is what most people have heard of. It gives you an additional tax-free buffer depending on your tax bracket.

In the US, the structure differs. There’s no blanket threshold like the PSA. Instead, tax-free treatment depends on account type, your tax filing status, and whether it offers tax-deferred growth or tax-free withdrawals.

Let me break down each UK allowance and show you exactly how much you can earn tax-free.

The Personal Savings Allowance: What You Get by Default

The Personal Savings Allowance is the most well-known one, and it’s pretty straightforward. If you’re a basic-rate taxpayer, you can earn up to £1,000 in savings interest each year completely tax-free. If you’re a higher-rate taxpayer, that drops to £500. If you’re an additional-rate taxpayer, you get nothing. You can verify these figures and check your specific situation directly on the HMRC savings interest guidance page.

Let me put this in perspective: at a 5% interest rate, you’d need around £20,000 in savings to generate £1,000 in interest earned on a savings account. If you want to calculate your interest earned on your own savings to see where you stand, you can use a calculator to verify this quickly. So if you’re a basic-rate taxpayer and you have less than £20,000 saved, you’re almost certainly not paying any tax on your interest right now.

The mistake I see people make is thinking that once they cross the £1,000 mark, all their interest suddenly becomes taxable. That’s not how it works. Only the amount above £1,000 gets taxed. If you earn £1,050 in interest, you only pay tax on the extra £50.

Your tax bracket determines how much PSA you get, but it also determines the rate you’ll pay on any excess. A basic-rate taxpayer pays 20% on the overage. A higher-rate taxpayer pays 40%.

This is where understanding your marginal tax rate really matters. The tax you owe is calculated on the slice of interest that exceeds your allowance, not on your total savings.

The Hidden Allowance Retirees and Low Earners Often Miss

This one is rarely talked about, but it can make a huge difference if you qualify. It’s called the Starting Rate for Savings, and it gives you an extra £5,000 of tax-free interest if your total income is low enough.

The mechanics are simple. If your total income from all sources, excluding your Personal Allowance, is £5,000 or less, you can earn up to £5,000 in savings interest completely tax-free.

But there’s a taper. For every £1 you earn above £12,570 from other sources like work or pensions, you lose £1 of this £5,000 allowance. So if you earn £14,570 in total income, you’ve used up £2,000 of the allowance and only have £3,000 left for tax-free interest.

This is incredibly valuable for retirees or people with low earned income. If you’re earning less than £12,570 from work and you have savings generating interest, this allowance can shelter a lot more than the PSA alone. If you’re managing a retirement savings account, this is one of those tax-free savings options that flies completely under the radar.

But there’s a taper. For every £1 you earn above £12,570 from other sources like work or pensions, you lose £1 of this £5,000 allowance. So if you earn £14,570 in total income, you’ve used up £2,000 of the allowance and only have £3,000 left for tax-free interest.

This is incredibly valuable for retirees or people with low earned income. If you’re earning less than £12,570 from work and you have savings generating interest, this allowance can shelter a lot more than the PSA alone.

When you combine the Personal Allowance, the Starting Rate for Savings, and the PSA, someone with very low other income could theoretically earn up to £18,570 per year in interest without paying any tax at all. That’s a significant amount that’s rarely mentioned in standard savings advice.

If you’re managing a retirement savings account or you’re semi-retired with mixed income sources, this is worth exploring. It’s one of those tax-free savings options that flies completely under the radar.

In the US, there’s no equivalent to this. Tax treatment of interest depends entirely on the type of account, not on your income level, unless you’re talking about credits and deductions that phase out at higher incomes.

The Tax Bracket Mistake That Makes People Fear Their Savings

I need to address something that causes a lot of unnecessary worry. I’ve talked to people who are genuinely afraid to earn more interest because they think it will push them into a higher tax bracket and cost them a fortune.

This fear is based on a misunderstanding of how progressive taxation actually works. Once you understand the reality, the fear disappears.

The truth is simple: when you move into a higher tax bracket, only the income that falls into that bracket is taxed at the higher rate. The rest of your income is still taxed at the lower rates.

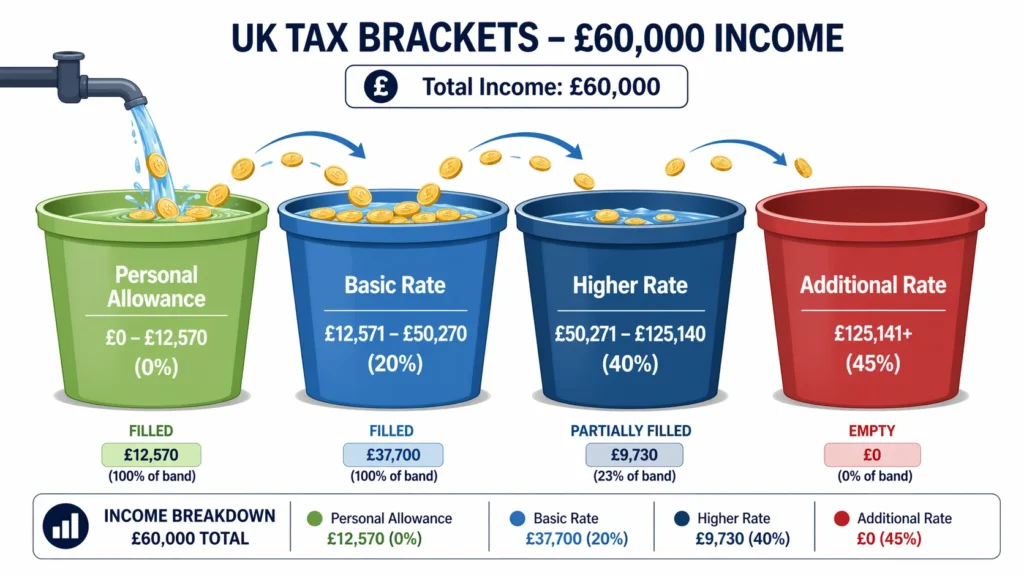

Think of it like filling buckets. The first bucket is your Personal Allowance, taxed at 0%. The next bucket is your basic-rate band, taxed at 20%. The third bucket is your higher-rate band, taxed at 40%. You only pay the higher rate on the money that spills into that specific bucket.

Think of it like filling buckets. The first bucket is your Personal Allowance, taxed at 0%. The next bucket is your basic-rate band, taxed at 20%. The third bucket is your higher-rate band, taxed at 40%. You only pay the higher rate on the money that spills into that specific bucket.

Let me give you a concrete example. Say you earn £60,000 in salary. You pay 0% on the first £12,570, then 20% on the next £37,700, and finally 40% only on the remaining £9,730. You don’t pay 40% on the entire £60,000.

The same logic applies to your savings interest. If your interest earned on savings account pushes you slightly into a higher bracket, you only pay the higher rate on that small excess, not on all your income or all your interest.

This is your marginal tax rate at work. It’s the rate you pay on the next pound you earn, not the rate you pay on everything.

This misunderstanding stops people from maximizing their savings. They cap themselves artificially, scared of crossing an invisible line.

In the US, the principle is exactly the same. Ordinary income, including savings interest, is taxed progressively. If you move from the 12% bracket to the 22% bracket, only the dollars above that threshold are taxed at 22%. The rest are still taxed at 12% or lower.

Your adjusted gross income determines which bracket you’re in, but again, it’s only the slice of income in each bracket that gets taxed at that rate. Investment income follows the same progressive structure.

Understanding this removes one of the biggest psychological barriers to smart saving. You’re not penalized for earning more. You’re only taxed fairly on the increment.

The Mistake That Makes People Lose Money While Avoiding Tax

This might be the most important thing I tell you in this entire article. Sometimes, trying too hard to avoid tax actually costs you more money than just paying the tax would have.

I learned this from financial advisors who see it happen constantly. People make decisions based purely on minimizing taxes on interest, without looking at the actual after-tax returns.

A real-world example: someone spends $10,000 on something just to get a $10,000 tax deduction. They think they’re saving $10,000 in taxes. But a $10,000 deduction only reduces your tax bill by your marginal rate, whether it’s the standard deduction or an itemized one, maybe $4,000 if you’re in a 40% bracket. So they spent $10,000 to save $4,000. That’s a net loss of $6,000.

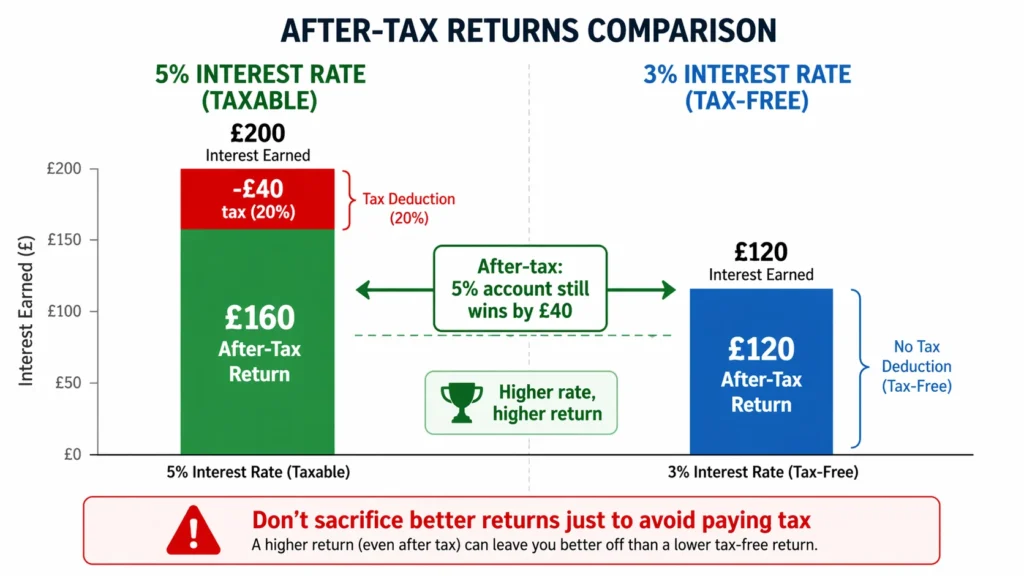

If you’re a basic-rate taxpayer, you’d pay 20% tax on that £200 excess, which is £40. But the extra interest you earned by choosing the higher rate far outweighs that £40 tax bill. You come out ahead even after tax.

This is why I always say: don’t chase lower rates just to avoid tax. The goal is to maximize your after-tax returns, not to minimize your tax bill at any cost.

Another thing worth knowing is that tax-free savings options like ISAs are now very competitive. The assumption that tax-free automatically means lower interest used to be true, but it’s often not the case anymore. I’ve seen Cash ISAs offering rates that match or beat standard savings accounts.

So before you accept a lower annual percentage yield just to stay under a threshold, compare the actual numbers. Calculate what you’d keep after tax in both scenarios.

The point is simple: tax-efficient savings means keeping more money in your pocket overall, not just avoiding tax on paper.

Cash ISAs: Still the Simplest Way to Shelter Savings From Tax

If I had to recommend one strategy to avoid paying tax on savings account interest, it would be this: use a Cash ISA.

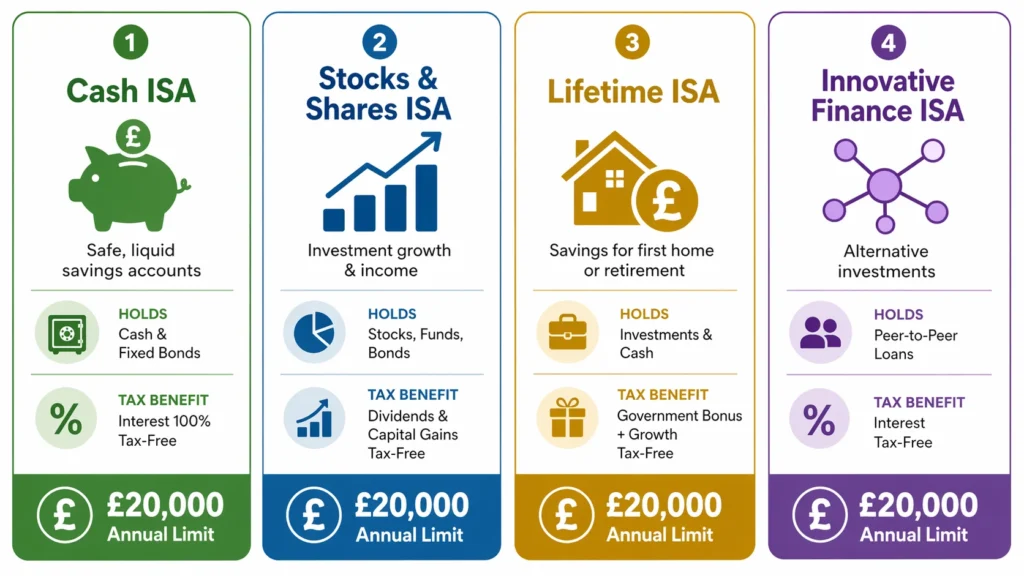

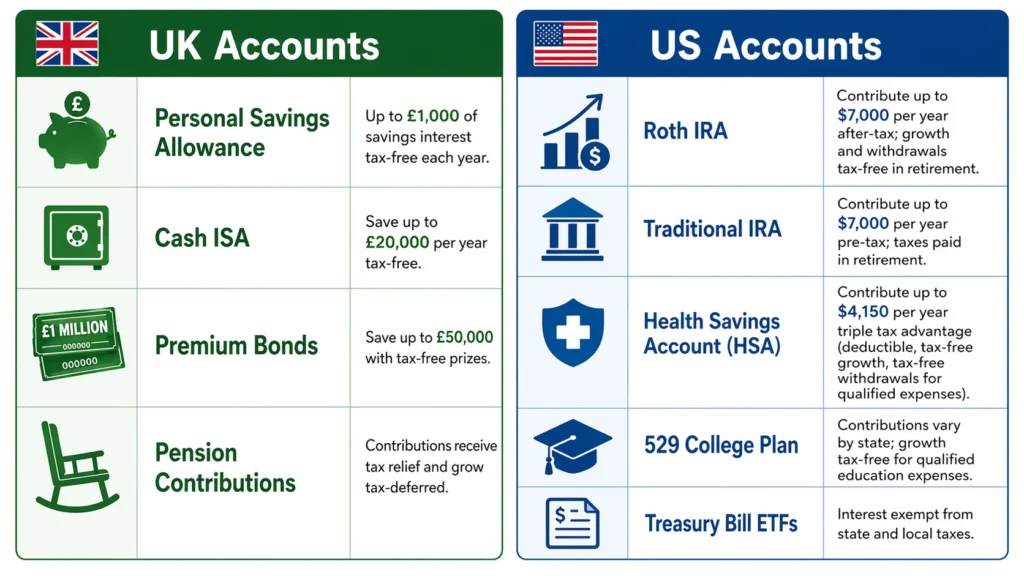

A Cash ISA is a tax-advantaged savings account available in the UK. You can put up to £20,000 into it each tax year, and all the interest you earn inside it is completely tax-free. It doesn’t count toward your Personal Savings Allowance, and you never pay a penny of tax on it.

The beauty of a Cash ISA is its simplicity. You don’t need to calculate allowances, track interest thresholds, or worry about your tax bracket. The interest is tax-free, period.” OR “The interest is completely tax-free.

ISAs come in different forms. Cash ISAs work like regular savings accounts. Stocks and Shares ISAs let you invest in funds, shares, or bonds, and any growth or dividends are also tax-free. There are also Lifetime ISAs and Innovative Finance ISAs, but for straightforward savings, a Cash ISA is usually the best starting point.

One thing that’s changed in recent years is the quality of ISA rates. It used to be that ISAs paid noticeably less interest than standard accounts. That’s no longer true. Current best-buy Cash ISA rates on MoneySavingExpert show easy-access and fixed-term ISAs now rivalling or even exceeding taxable high-yield savings accounts.

This makes the decision much easier. If you can get the same or better rate inside an ISA, there’s no reason not to use one.

The £20,000 annual limit is per person, per tax year. If you don’t use it, you lose it. You can’t carry unused allowance forward. But any money you put in stays tax-free forever, including all the compound interest it earns over time.

For most savers, this is the simplest and most effective way to shelter interest from tax.

What “Flexible ISA” Means and Why It Matters

Not all ISAs are created equal, and this is a detail that most articles miss. Some ISAs are flexible, and some aren’t.

Here’s the difference. With a standard ISA, if you deposit £10,000 and then withdraw £3,000 later in the same tax year, you’ve used up £10,000 of your annual allowance. You can’t put that £3,000 back without it counting as a new contribution.

With a flexible ISA, you can withdraw that £3,000 and put it back in the same tax year without losing any of your allowance. The withdrawal doesn’t permanently use up your limit.

This is incredibly useful if you’re building an emergency fund or if you dip into your savings occasionally and then top them back up. It gives you much more control without sacrificing the tax-free benefit.

Not all financial institutions offer flexible ISAs, so it’s worth checking when you open one. It’s a small feature that makes a big practical difference, especially if your savings aren’t static.

This distinction comes directly from advisors who work with real savers, and I think it’s one of the most underappreciated features of ISAs.

How to Avoid Tax on a High-Yield Savings Account Using an ISA Wrapper

If you’re currently paying taxes on high yield savings because your money isn’t in an ISA, you might be leaving hundreds or thousands on the table.

The solution is straightforward: move that money into a Cash ISA with a comparable rate. You get the same high annual percentage yield, but now the interest is completely tax-free.

I used to assume that high-yield accounts couldn’t be ISAs, or that ISA rates were always lower. That’s not the case anymore. Many of the best-buy savings accounts are available as ISA versions with identical or near-identical rates.

This is one of the easiest wins for tax-efficient savings. You’re not sacrificing returns. You’re just wrapping the same account in a tax-free structure.

The Best Tax-Advantaged Savings Accounts Beyond a Standard ISA

Once you’ve maxed out your ISA allowance or you’re looking for additional options, there are several other tax-advantaged savings accounts and structures worth knowing about.

I’m going to cover both UK and US options here because the principles overlap, even though the specific accounts differ by country.

The goal with all of these is the same: legally shelter your interest or investment returns from tax using tax-advantaged investments and accounts designed specifically for that purpose

Premium Bonds: Tax-Free Prizes, But Read This First

Premium Bonds are a UK government-backed savings product. Instead of earning interest, your money is entered into a monthly prize draw. Prizes range from £25 to £1 million, and every prize is 100% tax-free.

You can hold up to £50,000 in Premium Bonds, and your capital is completely safe because it’s backed by the government. You can withdraw your money anytime without penalty.

Here’s the honest assessment: Premium Bonds are useful, especially if you’re an additional-rate taxpayer with no Personal Savings Allowance left, or if you’ve already maxed your ISA and you want another tax-free option.

But on average, the prize rate is lower than what a top Cash ISA currently pays. The prize fund rate fluctuates, but it’s often around 4% to 4.5% annually, and that’s an average. Some people win more, many win less, and some win nothing at all.

If you want certainty and the best possible return, a top Cash ISA usually wins. If you like the idea of a tax-free lottery and you’ve already used your ISA, Premium Bonds are a solid complement.

I wouldn’t use them as a replacement for an ISA, but as an addition, they make sense for the right person.

Roth IRA and Traditional IRA: Tax-Free vs Tax-Deferred

In the US, IRAs are one of the most powerful tax-advantaged savings accounts available, especially for retirement. I’ve seen countless people transform their retirement savings by understanding the difference between these two.

A traditional IRA lets you contribute up to $7,000 per year, or $8,000 if you’re over 50. These contribution limits increase periodically, so check current IRS guidance. Contributions may be tax-deductible, and the money grows tax-deferred. You pay tax when you withdraw in retirement.

A Roth IRA uses after-tax dollars, but all the growth and all your withdrawals in retirement are completely tax-free. There are no required minimum distributions, and you can pass it on to heirs tax-free.

The trade-off is simple: traditional IRA saves you tax now, Roth IRA saves you tax later. If you expect to be in a higher tax bracket in retirement, Roth usually wins. If you need the deduction now and expect lower income later, traditional makes sense.

Both offer tax-deferred growth or tax-free withdrawals, which makes them far superior to holding cash in a taxable savings account if you’re saving for retirement.

The contribution limits are modest compared to ISAs, but the tax benefits are significant. If you’re in the US and not using an IRA, you’re leaving money on the table.

Health Savings Account (HSA): Triple Tax Advantage

The HSA is one of the best-kept secrets in US tax planning. It’s the only account with a triple tax advantage.

You contribute pre-tax,which reduces your taxable income by up to $4,150 for individuals or $8,300 for families (2024 IRS limits) or $8,300 for families. The money grows tax-free inside the account. And when you withdraw it for qualified medical expenses, it’s tax-free again.

No other account offers all three. Not even a Roth IRA.

If you have a high-deductible health plan, you’re eligible. I recommend treating your HSA like a retirement account. Pay your medical expenses out of pocket if you can, let the HSA grow, and use it later in life when medical costs are higher.

The investment options inside an HSA are often similar to a 401(k), so you’re not limited to cash. You can invest in funds and let it grow for decades.

This is one of the most tax-efficient savings strategies available in the US, and it’s significantly underused.

529 College Savings Plan: If Education Is in the Plan

If you’re saving for a child’s education, a 529 college savings plan offers tax-deferred growth and tax-free withdrawals for qualified education expenses. I’ve recommended this to friends with young children, and the state tax benefits alone make it worthwhile.

Many states offer a state income tax deduction on contributions, which makes it even more attractive.

The money grows without being taxed, and as long as you use it for tuition, books, room and board, or other qualified expenses, you never pay federal tax on the gains.

How to Reduce Taxable Income From Savings Using Pension Contributions

This is a strategy most people don’t connect to savings tax, but it’s incredibly powerful. Increasing your pension contributions can actually reduce the tax you pay on your savings account interest.

Here’s how it works. Pension contributions reduce your taxable income. If you earn £60,000 and contribute £6,000 to your pension, your taxable income drops to £54,000.

That might not sound like a big deal, but here’s the bonus: if that £6,000 reduction moves you from the higher-rate tax band back into the basic-rate band, your Personal Savings Allowance doubles from £500 to £1,000.

Suddenly, you’re sheltering an extra £500 in interest from tax, just by making a pension contribution that was already saving you tax on your salary.

If you’re right on the edge of a tax bracket, this is a huge win. You get tax relief on the pension contribution, you reduce your adjusted gross income, and you unlock a bigger tax-free savings buffer.

Your employer may also match your contributions, which is essentially free money. Combined with the tax relief, pension contributions are one of the most tax-efficient moves you can make.

In the UK, you get automatic tax relief on pension contributions. Basic-rate taxpayers get 20% added automatically. Higher-rate taxpayers can claim an additional 20% through their tax return.

In the US, contributing to a traditional 401(k) or IRA works the same way. It’s a pre-tax contribution that lowers your taxable income and can shift your tax bracket, indirectly helping with how much tax you pay on other income, including interest.

There’s one more advanced trick worth mentioning. If you’re a high saver and you’ve already maxed your ISA, you can hold money market funds inside a pension wrapper. They act like cash, earning a steady return, but they grow completely tax-free inside the pension.

This is a more sophisticated strategy, but for people with significant savings, it’s a way to keep earning on cash-like assets without paying tax every year.

The trade-off is that pensions are locked until retirement, and there’s an early withdrawal penalty if you access them too soon. But if the money is genuinely long-term savings, pensions and other tax-sheltered accounts can be powerful tools for more than just salary.

If You’ve Maxed Your ISA: 3 Strategies Most Articles Don’t Cover

If you’ve already used your full £20,000 ISA allowance and you’re still sitting on savings that are generating taxable interest, you’re in a good position. But you’re also probably looking for the next step.

Most articles stop at ISAs and Premium Bonds. I’m going to share three strategies that almost no one talks about, but that can make a real difference if you’re a high saver or part of a couple managing household wealth.

Doubling Your Allowances If You Have a Partner

This is one of the simplest and most powerful moves available, and it’s completely legal and tax-free.

If you’re married or in a civil partnership, you can transfer assets between each other without any tax consequences. That means you can effectively double your ISA allowance, your Premium Bond limit, and your Personal Savings Allowance.

Here’s how it works in practice. If one partner is a higher-rate taxpayer with a £500 PSA, and the other is a basic-rate taxpayer with a £1,000 PSA, you can shift savings into the name of the lower earner. Now that money benefits from the higher allowance.

You can also each open your own ISA and each contribute up to £20,000 per year. That’s £40,000 of tax-free savings per household, per tax year.

Same with Premium Bonds. Each partner can hold up to £50,000, giving you £100,000 in tax-free prize-eligible savings as a couple.

This is especially valuable if one partner earns significantly more than the other. The tax savings can add up quickly, and it’s all perfectly above board.

If you’re managing household finances together, this is an easy win that requires nothing more than opening accounts in both names and being intentional about how you allocate your savings.

What Government Gilts Are and When They Make Sense

This one is more niche, but it’s worth understanding if you’re a sophisticated saver with a large cash reserve.

UK government gilts are bonds issued by the government. You can buy them at a discount to their face value, and when they mature, you get the full face value back.

The key advantage: the capital gain you make when a gilt matures at par is exempt from Capital Gains Tax, making it effectively tax-exempt interest on the capital gain portion. The coupon interest is still taxable, but if you buy low-coupon gilts, most of your return comes from the capital gain, which is tax-free.

The coupon interest is still taxable, but if you buy low-coupon gilts, most of your return comes from the capital gain, which is tax-free.

For someone who’s already maxed their ISA, has no PSA left, and is sitting on a large cash pile, short-term gilts can be a way to earn a return with minimal tax impact.

This strategy isn’t for everyone. Gilts are less liquid than savings accounts, they require a bit more knowledge to buy, and the returns aren’t always better than a top ISA once you factor in the hassle.

But for high earners with significant savings and a good understanding of fixed income, it’s a legitimate tool that provides tax-exempt interest on the capital gain portion.

I wouldn’t recommend this as a first move, but if you’re already doing everything else, it’s worth knowing it exists.

T-Bill ETFs: A Savings Account Alternative With a State Tax Bonus (US)

If you’re in the US and looking for a tax-efficient place to park cash, Treasury bill ETFs like SGOV are worth considering.

SGOV holds short-term US Treasury bills and currently yields around 4.8%. The interest from Treasury securities is exempt from state income tax, making it tax-exempt interest for state purposes, which can save you a meaningful amount if you live in a high-tax state like California or New York.

The ETF is fully liquid, trades like a stock, and functions almost like a savings account in terms of stability and access.

The trade-off is that it’s not FDIC insured like a bank account. It’s held in a brokerage, and while the underlying Treasuries are backed by the US government, the ETF itself can fluctuate slightly in price.

That said, for cash you don’t need instant access to and that you’re comfortable holding in a brokerage, T-bill ETFs offer a higher after-tax return than most savings accounts, especially when you factor in the state tax savings.

This is a strategy I’ve seen recommended by tax professionals, and it’s a genuinely useful alternative to traditional high-yield savings for people who understand the trade-offs.

Municipal bonds and municipal bond funds work on a similar principle, offering tax-exempt interest at the federal and sometimes state level, though they carry a bit more risk than Treasuries.

If you’re in a high tax bracket and you live in a state with income tax, this is one of the few ways to boost your annual percentage yield on cash while reducing your overall tax burden.

When It Actually Makes Sense to Just Pay the Tax

I want to be honest with you about something most financial content won’t say: sometimes, the smartest move is to just pay the tax and move on.

Not every strategy is worth the complexity, and not every tax saving is worth the time, stress, or opportunity cost involved.

I’ve seen people spend hours researching obscure accounts and switching banks four times a year just to save £50 in tax. That’s not smart. That’s exhausting. That’s not smart. That’s exhausting.

If you’re earning slightly more than your Personal Savings Allowance and the tax bill is £100 a year, paying it might be simpler and less stressful than restructuring your entire financial life.

Remember the principle I mentioned earlier: don’t make bad financial decisions just to avoid tax. Spending money or accepting worse terms purely to dodge a tax bill often costs you more than the tax itself.

If you’re a high earner with significant savings and investment income, hiring a professional tax advisor is almost always worth it. Even if it costs a few thousand, the strategies they can find often save multiples of that in tax.

The value of professional advice isn’t just the money saved it’s the peace of mind. You stop second-guessing yourself, stop worrying about mistakes, and know someone qualified is handling it.

For straightforward situations, a Cash ISA and basic awareness of your allowances is usually enough. For complex situations involving multiple income sources, investments, or cross-border issues, professional help pays for itself.

The goal isn’t to minimize taxes on interest at all costs. The goal is to make smart decisions that leave you better off overall, financially and mentally.

If paying a small amount of tax means you sleep better, keep your money accessible, and avoid products you don’t understand, that’s a win.

Tax efficiency is important. But clarity, simplicity, and confidence in your plan matter just as much.

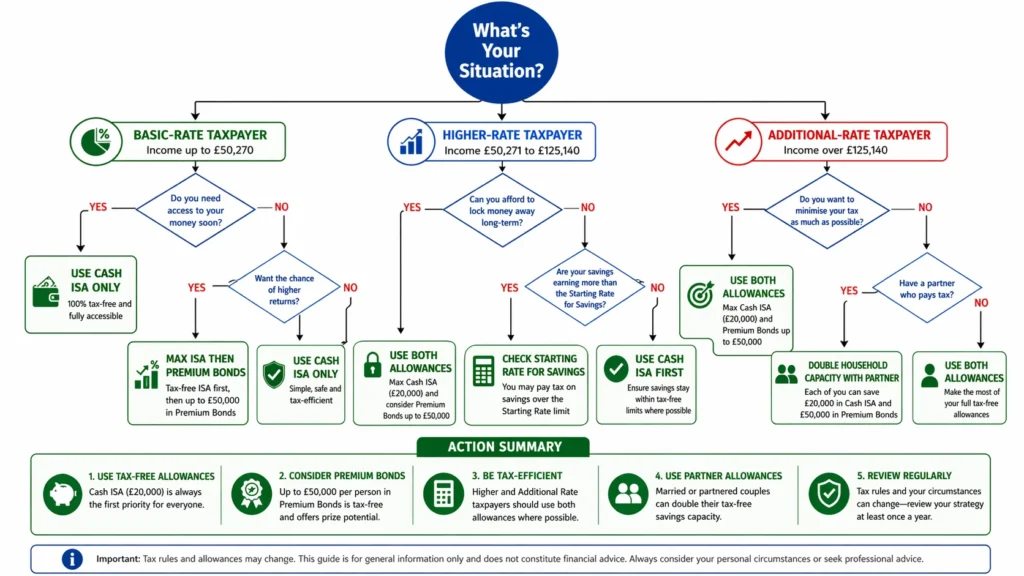

Your Action Plan: Which Strategy Fits Your Situation

Let me help you figure out which strategies to legally avoid tax on your savings actually apply to you. You don’t need to do everything. You need to do the right one or two things for your situation to reduce tax liability effectively.

If you’re a basic-rate taxpayer with less than £20,000 in savings, start with a Cash ISA. It’s simple, offers tax-free savings options, and you’ll likely never pay tax on your interest. Look for a flexible ISA if you want the freedom to withdraw and replace funds.

If you’re a basic-rate taxpayer with more than £20,000 in savings, max out your ISA first, then check if your remaining interest stays within your £1,000 PSA. If it does, you’re fine. If it doesn’t, consider Premium Bonds or moving savings into a partner’s name if they have unused allowances.

If you’re a higher-rate taxpayer, your PSA is only £500, so tax-free accounts matter even more. Max your ISA, use Premium Bonds for the next layer, and if you’re near the threshold between basic and higher rate, consider pension contributions to drop back down and double your PSA.

If you’re a retiree or low earner with income under £17,570, you may qualify for the Starting Rate for Savings. This can shelter up to £5,000 in interest on top of your PSA, giving you huge tax-free capacity. This is one of the most overlooked opportunities available.

If you’re part of a couple, use both partners’ allowances. Transfer savings to the lower earner, open ISAs in both names, and use both Premium Bond limits. This can double your tax-free capacity without any complex planning.

If you’re in the US, prioritize accounts in this order: max your HSA if eligible, max your Roth IRA, then use a traditional IRA or 401(k) for pre-tax contributions. For cash savings, consider T-bill ETFs if you’re in a high-tax state.

The key is to start simple. Most people only need a Cash ISA and awareness of their PSA. Don’t overcomplicate it unless your situation genuinely requires more.

And remember, the goal is to legally avoid tax where it makes sense, keep more of your money, and build savings that work for you, keep more of your money, and build savings that work for you without unnecessary stress.

Now you know exactly how to avoid tax on savings account interest using legal, proven strategies. Pick the one that fits your situation best, and take action this week. You don’t need to do everything at once. You just need to start.

Frequently Asked Questions

What is the maximum amount of savings interest I can earn without paying any tax?

For most basic-rate taxpayers in the UK, you can earn £1,000 in interest tax-free through the Personal Savings Allowance, plus unlimited interest inside an ISA. If you’re a low earner or retiree combining the Personal Allowance, Starting Rate for Savings, and PSA, you could earn up to £18,570 per year in interest completely tax-free. In the US, the limits depend on the account type. Roth IRA and HSA withdrawals can be fully tax-free if used correctly.

If I earn more than my Personal Savings Allowance, do I pay tax on all my interest or just the extra?

You only pay tax on the amount above your allowance, not on the full amount. If your PSA is £1,000 and you earn £1,050 in interest, you’re only taxed on the £50 excess. This is the single most common misconception about savings tax. The allowance isn’t all-or-nothing. It’s a threshold, and only the interest above it is taxable at your marginal rate.

Does putting money in an ISA mean I earn less interest than a regular savings account?

Not anymore. ISA rates have become very competitive in recent years. In many cases, Cash ISAs now match or even exceed the rates offered on standard taxable savings accounts. Always compare current best-buy rates before assuming an ISA will pay less. The old assumption that tax-free means lower returns is often no longer true.

Can I avoid tax on a high-yield savings account without moving my money?

If your total interest stays within your Personal Savings Allowance, you’re already not paying tax. But if your interest exceeds that limit, you’ll need to use a tax-advantaged account like an ISA, make pension contributions to reduce your taxable income, or use one of the alternative strategies I’ve covered. Simply leaving the money where it is won’t shelter the excess from tax.

Is it legal to avoid paying tax on savings interest?

Yes, absolutely. Using accounts and allowances specifically designed for this purpose, such as ISAs, IRAs, HSAs, Premium Bonds, and pensions, is completely legal. This is tax avoidance in the legal sense, meaning you’re using government-approved structures to reduce your tax bill. It’s not tax evasion, which is illegal. Every strategy I’ve covered is legitimate and encouraged by tax authorities.

Are Premium Bonds worth it for avoiding savings tax?

They can be, especially if you’re an additional-rate taxpayer with no Personal Savings Allowance left, or if you’ve already maxed your ISA. But in practice, a top Cash ISA often generates a better return than the average Premium Bond prize rate. Premium Bonds work best as a complement to ISAs, not as a replacement. They’re useful for diversification and the chance of a big win, but they shouldn’t be your only tax-free savings strategy.

Does moving money into a pension affect how much savings interest I can earn tax-free?

Yes, and this is a powerful but underused strategy. Pension contributions reduce your taxable income. If that reduction moves you from the higher-rate tax band back to the basic-rate band, your Personal Savings Allowance doubles from £500 to £1,000. So by contributing to a pension, you indirectly increase the amount of savings interest you can earn tax-free, on top of the tax relief you get on the pension contribution itself.

My spouse earns less than me-can we use their savings allowances too?

Yes. Transferring savings to a lower-earning spouse or civil partner is completely tax-free, and they have their own Personal Savings Allowance, ISA allowance, and Premium Bond limit. This can effectively double your household’s tax-free savings capacity. If one partner is a higher-rate taxpayer and the other is a basic-rate taxpayer, moving savings into the name of the lower earner can significantly reduce the tax you pay as a couple.