How to Create a Budget for a Business: Step-by-Step Guide

I still remember the conversation that taught me how to create a budget for a business the right way.

A colleague was helping a client with business budget planning. This owner had built his company from scratch and reached $500,000 in sales that year.

He was proud. But when my colleague reviewed the books, he found something shocking. Despite half a million dollars in revenue, the business was bleeding money every single month.

The owner had no budget. He was spending money whenever he thought he needed to. He kept rough numbers in his head. He assumed profit would be there at the end of the year because sales were strong.

But it wasn’t there. He was operating at a loss and didn’t even know it.

This pattern appears constantly. Running a business without proper financial management is like driving at night with no headlights. You might move forward, but you have zero visibility on what’s coming or where you’ll end up.

Why Most Businesses Fail Without a Budget (And How to Avoid It)

I learned this the hard way early on. When you keep your business expenses and revenue in your head instead of tracking them properly, you create financial chaos. You might think you know your spending. You might feel like things are going well. But feelings don’t pay bills or build profit.

I used to do this myself. I would estimate costs, guess at my profit margin, and hope everything balanced out. It didn’t. I made financial decisions based on what I thought I had, not what was actually in the bank. That approach cost me money, stress, and too many sleepless nights.

Putting those numbers on paper changes everything. It gives you power. You stop guessing and start knowing. You see exactly where your money comes from and where it goes. You assign every dollar a job before it even arrives.

That shift from chaos to clarity is what a budget does for your business.

A business budget is more than just a budget spreadsheet with numbers. It is a complete business financial plan based on your real income and expenses. It forces you to answer hard questions before you are drowning in a crisis.

Can you afford to hire that new employee? The budget tells you.

Should you invest in that marketing campaign? The budget shows you if there is room.

Do you have enough saved for slow months? The budget makes sure you do.

Without this plan, every financial decision becomes a gamble. With it, you make decisions based on facts. You know your spending limits. You protect your profit margin instead of hoping for it.

I have seen businesses transform once they start budgeting. They move from reactive to proactive. They stop wondering if they can afford something and start planning for it months in advance. They build financial confidence because they actually understand their numbers.

That is the power of taking the chaos out of your head and putting it where you can see it, control it, and use it to grow.

This is the part most business owners completely miss. They think profit is whatever is left after expenses. But when you treat profit like a leftover instead of practicing proper cost control, you rarely see any.

A budget flips that thinking. You decide your profit margin first. You build it into your plan as a required expense. Then you structure everything else around protecting that profit.

I budget my profit the same way I budget rent. It is not optional. It is not what remains if I am lucky. It is a planned outcome that I manage toward every single month.

When the business owner I mentioned earlier finally created a budget, he started with profit. He decided he needed a 15% profit margin to make the business sustainable. Then he looked at his expenses and cut what did not fit. Within six months, he went from losing money to keeping more than he ever had before.

That is what budgeting does. It assigns a destination for every dollar. It guarantees profitability by making profit a priority, not an afterthought. And it stops you from mismanaging funds because you are forced to make intentional choices about where money goes.

If you have been running your business without a budget, you are not alone. But you are also not powerless. The moment you put those numbers on paper, you take control. You move from chaos to clarity. And you give yourself the best chance of building a business that does not just survive, but actually makes money.

What is a Business Budget?

Business budget planning is the process of creating a financial plan that shows how you will use the resources you get from sales. That is the simplest way I can put it.

When I first started my business, I thought small business financial planning just meant tracking what I spent. I was wrong. Tracking is looking backward at money you already spent. Budgeting is looking forward at money you are about to earn and deciding what to do with it before it arrives.

This matters because it flips your entire relationship with money. Instead of reacting to expenses as they pop up, you plan for them. Instead of hoping you have enough cash, you know exactly how much you need and where it is going.

A business budget typically covers a specific time frame. Most small businesses budget monthly or quarterly. Some plan annually. The time frame matters less than the habit of planning itself.

Budget vs. Financial Goals: What is the Difference?

I used to confuse these two constantly. I would say things like “My budget is to hit $1 million in sales this year.” But that is not a budget. That is a financial goal.

A financial goal is an aspirational target. It is where you want to end up. A budget is the detailed tactical plan showing exactly how you will earn that revenue and where you will allocate every dollar on a monthly basis.

Now I look at it differently. If I say “I want to make $1 million in sales next year,” that is my goal. It sets the direction. But my budget is the spreadsheet that breaks down those sales month by month, lists every expense category, assigns dollar amounts to each one, and shows me exactly what profit I will keep if I follow the plan.

Goals inspire you. Budgets keep you accountable. You need both, but they serve completely different purposes.

Budget vs. Income Statement: How They Work Together

This confused me for a long time, so I want to clear it up.

A budget predicts what you expect to happen in the future. An income statement shows what actually happened in the past. They are two sides of the same coin, and you need both to manage your business well.

I create my budget at the start of each month. I project my revenue based on trends and pipeline. I list my planned expenses. I calculate my expected profit. That is my prediction.

At the end of the month, I pull my income statement from my accounting software. It shows my actual revenue, my actual expenses, and my actual profit. Then I compare the two.

This comparison is where the real value lives. When I see that I spent $2,000 more on marketing than I budgeted, I ask why. Was it a good investment that brought in extra sales? Or did I lose discipline and overspend?

When revenue comes in $5,000 higher than projected, I investigate. Did I land an unexpected client? Is this a trend I can count on, or was it a one-time event?

This budget versus actual analysis helps me spot problems early. If I notice spending creeping up for three months in a row, I can correct it before it becomes a crisis. If revenue consistently beats projections, I can invest more confidently in growth.

The budget guides your decisions. The financial statement holds you accountable. Together, they give you complete financial visibility.

Types of Business Budgets You Should Know

When I first learned about budgeting, I thought there was just one kind. You list income, subtract expenses, and hope for a positive number. But as my business grew, I realized different situations need different types of budgets.

You do not need to use all of these. Most small businesses do fine with just an operating budget and occasional cash flow planning. But knowing what is available helps you choose the right tool for your situation.

Operating Budget

An operating budget covers your day-to-day revenue and operating expenses for normal business operations. This is the budget most people think of when they hear the word budget.

I use an operating budget to plan my regular monthly costs. Rent, salaries, utilities, software subscriptions, marketing spend, office supplies. These are the predictable expenses that keep the business running.

On the revenue side, my operating budget projects sales from my core products and services. I do not include one-time windfalls or investment income here. Just the regular money that comes in from doing what my business does.

This budget tells me if my normal operations are profitable. If my operating budget shows a loss month after month, I know I have a fundamental problem with my business model. Either I need to raise prices, cut costs, or sell more volume.

Capital Budget

A capital budget is for long-term investments in equipment, property, or major assets that you will use for years.

I learned about capital budgeting when I needed to buy expensive equipment for my business. The capital expenditure was too large to fit in my regular monthly operating budget, and I did not want to drain my cash reserves all at once.

So I created a separate capital budget. I identified the equipment I needed, researched the costs, and then planned how I would save for it over several months. Instead of taking on debt, I set aside a portion of my profit each month until I had enough to buy the equipment with cash.

Capital budgeting separates big investments from daily expenses so you can evaluate them properly. When you are deciding whether to spend $50,000 on a new delivery truck or $100,000 on office renovations, you need a different planning process than deciding whether to spend $200 on office supplies.

Cash Flow Budget

A cash flow projection tracks when money actually moves in and out of your business, not just when you earn or owe it.

This distinction tripped me up early on. I would land a big client contract worth $20,000 and immediately think I could spend that money. But the client would not pay for 60 days. Meanwhile, I had payroll due in two weeks.

A cash flow budget saved me from that mistake. It shows the timing of cash movement. When do invoices actually get paid? When are expenses actually due? Do I have enough cash on hand to cover the gap between when I pay suppliers and when customers pay me?

I have seen profitable businesses fail because of cash flow problems. They had plenty of revenue on paper, but the cash was not available when bills came due. A cash flow projection prevents that crisis by showing you exactly when you might run short and giving you time to arrange a line of credit or adjust payment terms.

Master Budget

A master budget combines all your other budgets into one comprehensive financial plan.

I only started using a master budget when my business got more complex. It pulls together my operating budget, capital budget, and cash flow projections into a single document that shows the complete financial picture.

For most small businesses, this is overkill. But if you have multiple revenue streams, several departments, or complex financial planning needs, a master budget helps you see how all the pieces fit together.

Labor Budget

A labor budget focuses specifically on employee costs including salaries, wages, benefits, and payroll taxes.

I created my first labor budget when I started hiring. Labor became my biggest expense category, and I needed to track it carefully. This budget helped me decide when I could afford to hire, what I could pay, and whether I needed full-time employees or contractors.

If you are a solopreneur, you might not need a separate labor budget. But if you have even one employee, it is worth tracking labor costs separately because they behave differently than other expenses. You cannot easily cut labor when revenue dips, so you need to plan for that fixed commitment carefully.

Essential Budget Categories for Business Success

Every business budget needs certain core components. These are the building blocks that make up your financial plan.

When I built my first real budget, I kept the expense categories simple. I listed where money comes from and where it goes. Over time, I refined these categories, but the basics have not changed.

Revenue and Income Sources

Revenue is all the money coming into your business. This seems obvious, but I have learned to be thorough about it.

I list every income source separately in my budget. Product sales go on one line. Service fees on another. If I earn investment income or rental income from business property, those get their own lines too.

Why separate them? Because different income sources behave differently. My product sales might be seasonal. Service income might be steady. Investment income might be unpredictable. When I track them separately, I can spot trends and make better projections.

I also learned to calculate gross revenue first. That is total sales before any costs. Some businesses make the mistake of only budgeting net revenue after subtracting the cost of goods sold. But I want to see the full picture of money coming in before I start subtracting anything.

One tip that helped me: always include all income sources, even the small ones. That $500 per month you earn from a side offer adds up to $6,000 per year. When you are budgeting, every dollar counts.

Fixed Costs: Expenses That Stay the Same

Fixed costs are expenses that do not change much regardless of how many sales you make.

My rent is the perfect example. Whether I sell $10,000 or $100,000 worth of products this month, my rent stays the same. Insurance premiums, base salaries for employees, software subscriptions, loan payments. These are all fixed costs.

I pay close attention to fixed costs because they create a minimum threshold I have to cover every month. If my fixed costs total $15,000 per month, I know I need to generate at least that much in gross profit just to break even.

One trap I fell into early was underestimating fixed costs. I would budget for the obvious ones like rent and salaries, but I would forget about annual insurance renewals, quarterly tax payments, or subscription services I signed up for months ago.

Now I review my bank statements and credit card transactions from the past six months when I am setting up a new budget. I look for recurring charges:

• That yearly domain registration fee? Fixed cost.

• That monthly accounting software? Fixed cost.

• Those quarterly estimated tax payments? Definitely fixed costs.

Another category within fixed costs is overhead costs. These are the indirect expenses of running your business that are not tied to a specific product or service. Office utilities, administrative salaries, general liability insurance, professional fees for your accountant or lawyer. I group these as overhead costs, and I track them carefully because they have a way of creeping up over time.

Variable Expenses: Costs That Fluctuate

Variable expenses change based on your sales volume or production level.

If I run a product business, my cost of materials is a variable expense. The more units I sell, the more materials I need to buy. If I run a service business, contractor fees and sales commissions are variable. The more projects I take on, the more I pay.

Variable expenses give you some flexibility. When sales slow down, these costs naturally decrease. When business picks up, they increase, but you have the revenue to cover them.

I budget variable expenses as a percentage of revenue. If materials typically cost me 30% of my product sales, I budget 30% of projected sales for that category. If sales commissions run 10% of revenue, I allocate 10%.

This percentage approach has saved me multiple times. When my sales dropped during a slow quarter, my variable costs automatically adjusted downward. I did not have to scramble to cut expenses because they scaled naturally with revenue.

Important note for contractors: If you have very high material or subcontractor costs, handle this differently. A friend of mine runs a construction company. His material costs can be 60 to 70% of project revenue. He subtracts those costs first to calculate his real operating revenue, then applies his budget percentages to what is left. Otherwise, his budget does not reflect the actual money available to run the business.

One-Time Expenses and Emergency Fund

One-time expenses are the purchases you do not make every month but need to plan for anyway.

I learned this lesson the expensive way. I budgeted for my regular monthly costs, and everything looked great. Then my laptop died. Then I needed to hire a consultant for a special project. Then I had to pay for an unexpected business license renewal. None of these were in my budget, and suddenly I was scrambling for cash.

Now I always include a line item for one-time expenses. Website redesign, new equipment, consultant fees, conference attendance, professional development. These do not happen every month, but they happen.

I also set aside money for an emergency fund. Business emergencies are not a matter of if, but when. Equipment breaks. Economic conditions shift. Unexpected opportunities require quick investment. A client does not pay on time.

I budget 5 to 10% of my revenue for unexpected costs. Some months I do not touch it. Some months it saves me. Over time, this fund builds up and becomes a cash cushion that lets me sleep better at night.

The key is treating this emergency allocation like any other required expense. It is not optional. It is not what you save if there is money left over. It is a planned part of your budget that protects you from the surprises that will inevitably come.

How to Create a Budget for Your Business in 7 Steps

Creating a business budget sounds intimidating, but I have broken it down into a simple process that works whether you are brand new to budgeting or refining an existing system.

I follow these seven steps every time I build or update my budget. The process takes a few hours the first time, but once you have a template set up, monthly updates take less than an hour.

Step 1: Set Your Business Goals and Project Revenue

I used to start budgeting by looking at last month’s expenses. That was backward.

Now I start with financial goals. What do I want to achieve this year? Do I want to grow sales by 20%? Launch a new product? Hire my first employee? Increase my profit margin?

Your business goals shape your budget because they determine what you need to spend money on and how much revenue you need to generate.

Once I have my goals clear, I start revenue forecasting for the budget period. This is your income forecast for the time ahead.

If you have historical data, use it. I pull up my sales forecast data from the last 6 to 12 months and look for patterns. Am I growing? At what rate? Are there seasonal fluctuations? Do certain months consistently perform better than others?

I do not just look at one or two months because that is too narrow a window. A single good month might be an outlier. Six to twelve months of data shows me real trends I can trust.

If you are starting a new business and building your first startup budget without historical data, you need to make educated guesses. Here’s how to research realistic projections:

• Research your industry and what similar businesses typically earn in their first year

• Talk to other business owners in your field

• Look at industry benchmarks from trade associations like SCORE, the Small Business Administration, and industry-specific organizations

• Consult with an accountant who knows your field

The key is being conservative. I have seen too many new business owners create budgets based on best-case scenarios. They project high sales, low expenses, and everything going perfectly. Then reality hits, and the budget falls apart in the first month.

I budget for a realistic scenario, even slightly pessimistic. If I think I can make $10,000 in sales next month, I might budget for $8,000. If revenue comes in higher, that is a happy surprise and I have extra cushion. If it comes in at my conservative estimate, I am still covered.

One more thing about revenue projections. Break them down by source. If you have three products or service offerings, project sales for each one separately. These revenue projections become your income forecast for the budget period. This gives you a much clearer picture than one lump sum revenue number. It also helps you spot which parts of your business are growing and which need attention.

Step 2: Calculate Your Fixed Costs

Fixed costs are the expenses you pay regardless of sales volume. These are usually the easiest numbers to pin down because they do not change much month to month.

I start by listing everything I pay regularly. Rent or mortgage for my business space. Salaries for any employees on fixed pay. Insurance premiums. Loan payments. Software subscriptions. Internet and phone. Accounting and legal fees.

This is where I go back through my bank statements from the last six months. I look for every recurring charge. This catches the things I forget about, like that $15 per month subscription I signed up for a year ago and have not thought about since.

I also include expenses that are not monthly but are predictable. My business insurance renews once a year. That is a fixed cost, so I divide the annual premium by 12 and include that monthly amount in my budget. Same with quarterly tax payments or annual software licenses.

Many business owners treat their own compensation as optional. They pay everyone else first and take whatever is left.

That is a terrible approach. You are working in your business. That work has value. You deserve to be paid for it, and that payment should be budgeted like any other salary.

I now budget a reasonable salary for myself based on the work I do. If I am handling operations, sales, and customer service, what would I have to pay someone else to do those jobs? That number goes in my budget as a fixed cost.

Your salary pays you for your labor. Profit, which we will budget separately, pays you for owning the business. These are two different things, and separating them keeps your financial planning honest.

Step 3: Estimate Your Variable Expenses

Variable expenses are the costs that change with your sales or production volume.

For a product-based business, this includes cost of goods sold like raw materials, packaging, and shipping. For a service business, it might include contractor fees, commissions, or project-specific costs.

I estimate variable expenses as a percentage of revenue. This is much more reliable than guessing dollar amounts because it scales automatically with your sales.

If I have historical data, I calculate what percentage of revenue each variable expense category has been. If materials cost me $3,000 last month and I had $10,000 in sales, that is 30%. If that ratio holds consistent over several months, I budget 30% of projected sales for materials.

If you do not have history to work from, you need to estimate based on your pricing and cost structure. Look at what you charge for your product or service. Subtract what it costs you to deliver it. That difference is your gross profit margin, and the cost part is your variable expense percentage.

Let us say I sell a product for $100. It costs me $35 in materials and shipping to fulfill each sale. That means my variable costs are 35% of revenue. If I project $20,000 in sales next month, I budget $7,000 for variable costs.

One thing I have learned is to review and adjust these percentages regularly. Supplier prices change. Shipping costs fluctuate. Your efficiency improves or worsens. What was accurate six months ago might not be accurate today.

For businesses with very high material or contractor costs, there is an important adjustment to make. If you are spending 60 to 70% of revenue on materials and subcontractors, you need to subtract those pass-through costs first. What remains is your real operating revenue, and you apply your other budget percentages to that smaller number. Otherwise your budget will not reflect the actual money you have available to run your business.

Step 4: Account for One-Time Expenses

One-time expenses are the costs you do not incur every month but still need to plan for.

I keep a running list of these throughout the year. New computer equipment. Website redesign. Consultant fees for a special project. Conference registration and travel. Professional development courses. Office furniture. Legal fees for a contract review.

These expenses can wreck your budget if you do not plan for them. I used to treat them as emergencies when they came up, but they are not really emergencies. They are predictable. I know I will need to replace equipment eventually. I know I will want to attend at least one industry conference per year. I know I will need professional help on certain projects.

Now I estimate what these expenses might total for the year and divide that amount by 12. If I think I will spend $6,000 on one-time items over the year, I budget $500 per month and set that money aside.

Some months I do not spend any of it. Some months I spend more than the budgeted amount. But over the course of the year, it averages out, and I am never caught off guard.

One specific type of capital expenditure deserves special attention. Big purchases like equipment, vehicles, or major renovations.

I learned a valuable approach for these. Instead of using debt or draining my cash reserves all at once, I save for them over several months.

Let us say I need a piece of equipment that costs $100,000. That is a huge hit to take in one month. But if I save $20,000 per month for five months, I can buy it with cash and avoid debt payments that would strain my budget for years.

This requires planning ahead. I have to identify the purchase need early enough to save for it. But the discipline of saving monthly is much healthier for my business than taking on debt or wiping out my emergency fund.

Step 5: Set Your Target Profit Margin

This step changed everything for me. Profit is not what is left over. Profit is a planned outcome that you budget for.

I decide what profit margin I need to make my business sustainable. For most small businesses, a 10 to 20% net income is reasonable. Some industries operate on thinner margins. Some have room for more.

After doing a basic break-even analysis, I look at my revenue projection and multiply by my target profit percentage. If I am projecting $50,000 in revenue and I want a 15% profit margin, I need to keep $7,500 in profit that month.

That $7,500 becomes a line item in my budget. It is a required allocation, just like rent or salaries. It is not optional. It is not what I hope to have left over. It is what I plan to keep.

Then I structure all my other expenses to protect that profit. If my revenue projection is $50,000 and I am committing $7,500 to profit, I have $42,500 available for all my expenses. My fixed costs, variable costs, and one-time expenses need to fit within that $42,500.

If they do not fit, I have three choices. Cut expenses. Find ways to increase revenue. Or accept a lower profit margin and understand what that means for my business sustainability.

This approach guarantees profitability as long as I stick to the budget. I am not hoping for profit. I am planning for it. I am making it a priority from the start instead of an afterthought.

I also separate my salary from profit. My salary is in the fixed cost section. That is payment for the work I do in the business. Profit is the return on my investment in the business. These are two different things, and budgeting them separately keeps my thinking clear.

Step 6: Build Your Contingency Fund

A contingency fund is money set aside for unexpected costs and emergencies.

I budget 5 to 10% of my revenue for this. It is not an expense category exactly. It is a cash reserve that I build and maintain to handle surprises.

Equipment breaks down. A key client does not pay on time. An unexpected opportunity requires quick investment. Economic conditions change and sales drop. A new regulation requires compliance work you did not anticipate.

These things happen. I cannot predict when or what they will be, but I know they are coming.

The first time I built a proper contingency fund into my budget, it felt uncomfortable. I was setting aside money that I was not planning to spend. It felt like waste.

But within three months, my laptop died without warning. The contingency fund covered the replacement without stress. Six months later, a major client payment came in 45 days late. The contingency fund helped me cover payroll without panic.

Now I see this fund as one of the smartest parts of my budget. It is not waste. It is protection. It is the cushion that keeps a bad week from becoming a crisis.

I also learned to budget for the worst-case scenario, not the best case. If I think revenue could range from $40,000 to $60,000 next month, I budget based on $40,000. If the full $60,000 comes in, the extra goes into savings or gets reinvested. But my core budget is built on conservative numbers, and that includes a healthy contingency allocation.

Step 7: Review and Finalize Your Budget

The last step is putting it all together and making sure the math works.

I add up all my projected expenses. Fixed costs, variable costs, one-time expenses, contingency fund, and my planned profit. Then I compare that total to my revenue projection.

If projected revenue is higher than total planned allocations, I have a surplus. I can choose to increase my profit margin, invest more in growth, or build my cash reserves faster.

If projected expenses and profit exceed projected revenue, the budget does not balance. I need to make changes before finalizing it.

When the budget doesn’t balance, I have three options: cut expenses, increase revenue projections, or reduce my planned profit margin.

Cutting expenses is usually the first place I look. Are there any costs I can reduce or eliminate without hurting the business? Subscriptions I am not using? Marketing spend that is not returning results? Can I negotiate better rates with suppliers?

If I have already cut everything I can, I look at whether I can realistically increase revenue. Is my initial projection too conservative? Are there quick wins I can pursue to boost sales? Can I raise prices?

If neither of those options work, I might have to accept a lower profit margin temporarily. But I never eliminate profit from the budget entirely. Even a 5% margin is better than treating profit as optional.

Once the numbers balance and I am confident in the plan, I finalize the budget. I save it as my official plan for the month or quarter. Then I use it in my budget review to guide every financial decision I make during that period.

This budget becomes my financial guardrail. When I am tempted to make an unplanned purchase, I check the budget first. Do I have room for this? If not, can I cut something else to make room, or should I wait until next month?

The budget keeps me disciplined. It stops impulse spending. And most importantly, it ensures that every dollar I earn has a job to do, whether that is covering costs, funding growth, or becoming profit that I keep.

The Profit First Method: An Alternative Budgeting Approach

Traditional budgeting starts with revenue, subtracts expenses, and hopes for profit at the end. The Profit First method, developed by author Mike Michalowicz in his book Profit First, flips that formula completely.

I discovered this approach a few years ago, and while I do not use it for my entire business, the core principle changed how I think about budget allocation.

The idea is simple but powerful. Take your profit first, then force your expenses to fit what is left.

How the 3-Account System Works

The Profit First method uses three separate bank accounts to physically enforce your budget allocations.

Every dollar your business earns goes into your main business checking account first. This is your income hub. All revenue lands here.

Then, as soon as money hits that account, you immediately transfer it out to two other accounts based on predetermined budget allocation percentages.

Twenty percent goes to your business savings account. This covers taxes and builds your emergency fund. You do not touch this money except for tax payments and true emergencies.

Forty percent goes to your personal checking account. This is your paycheck as the business owner. It is the money you pay yourself for running the business. It covers your personal living expenses.

The remaining 30 to 40% stays in the business checking account to cover all your operating expenses. Rent, supplies, software, marketing, everything.

This system forces discipline. You cannot overspend on business expenses because you only have 30 to 40% of revenue available. If your costs do not fit in that allocation, you have to cut them or find ways to increase efficiency.

It also guarantees that you pay yourself. Many business owners forget to take a salary. They reinvest everything back into the business and live on scraps. With Profit First, your personal pay happens automatically. It is not what is left over. It is a planned allocation that comes first.

I started using a modified version of this system. I do not follow the exact percentages because my business structure is different, but I do use separate accounts for different purposes. When I see money leave my operating account for taxes and personal pay immediately, I know exactly what I have available to spend. It eliminates the temptation to overspend because the money simply is not there.

When to Use Profit First vs. Traditional Budgeting

Profit First works best for businesses that struggle with overspending or business owners who have trouble paying themselves consistently.

If you constantly find yourself spending everything your business makes, this system puts up physical barriers. You literally cannot access the money you have allocated to taxes and personal pay, so you are forced to operate within the constraint of what remains.

If you are someone who reinvests every dollar back into the business and never pays yourself, this system fixes that problem. Your personal pay happens first, automatically, before you have a chance to talk yourself out of it.

However, Profit First has limitations. If your business has very tight margins or very high material costs, the system needs adjustment.

A friend of mine runs a contracting business. His material and subcontractor costs can be 60 to 70% of project revenue. If he tried to use the standard Profit First allocations, the math would not work. He would be trying to cover 70% in costs with only 30% allocated to expenses.

For businesses like his, you need to subtract the direct project costs first. Pull out what you need to pay for materials and subcontractors. What remains is your real operating revenue. Then you can apply Profit First percentages to that smaller number.

I think of Profit First as training wheels for financial discipline. It forces good habits until they become natural. Once you internalize the discipline of paying yourself first and living within your means, you can transition to more flexible budgeting approaches if needed.

But even if you do not adopt the full system, the core principle is valuable. Allocate profit and owner pay first. Make them required parts of your budget, not optional leftovers. Then structure your expenses to fit what remains. That mindset shift alone can transform your business finances.

Percentage-of-Revenue Budgeting: The CPA’s Secret

I learned this approach from a CPA who has worked with over 200 small businesses. It has changed how I think about expense allocation.

Instead of budgeting fixed dollar amounts for expenses, you budget them as percentages of revenue. This creates a budget that automatically scales with your sales.

Let us say I budget $10,000 for marketing next month. That is a fixed dollar amount. If my sales come in at my projection of $100,000, I am fine. My marketing spend is 10% of revenue, and I hit my target.

But what if sales drop to $70,000? If I still spend $10,000 on marketing, that is now over 14% of revenue. My profit margin gets squeezed. I might even go negative.

With percentage-based budgeting, I would have allocated 10% of revenue to marketing instead of a fixed $10,000. When sales drop to $70,000, my marketing budget automatically adjusts to $7,000. I spend less, but I maintain my profit margin.

This approach guarantees profitability regardless of whether my sales forecast is perfectly accurate. As long as I stick to my percentage allocations, my profit percentage stays protected through proper expense tracking.

How to Assign Expense Percentages

The key is figuring out what percentage each expense category should be.

If you have historical data, this is straightforward. I look at the past six months and calculate what percentage of revenue each expense category has averaged.

If rent has been $2,000 per month and revenue has averaged $40,000, rent is 5% of revenue. If marketing has been $4,000 and revenue has been $40,000, marketing is 10%. I do this calculation for every expense category.

These historical percentages become my budget template. When I project $50,000 in revenue next month, I multiply by 5% to get my rent budget, by 10% to get my marketing budget, and so on.

If you do not have historical data, you need to use industry benchmarks. Most industries have typical expense ratios. Restaurants often spend 25 to 35% on food costs. Retail stores might spend 50 to 60% on inventory. Service businesses typically spend 40 to 50% on labor.

Trade associations like SCORE, the Small Business Administration, and industry-specific organizations often publish these benchmarks. Your accountant probably knows them for your industry. You can also find them through research or by talking to other business owners in your field.

I start with these benchmarks and then adjust as I collect my own data. After three to six months of tracking actual expenses, I have enough information to refine my percentages based on my specific business instead of industry averages.

One important note about percentage budgeting. Some costs are truly fixed and do not scale with revenue. Rent is the classic example. My rent does not change whether I make $30,000 or $100,000 in sales.

For these fixed costs, I still express them as a percentage in my budget, but I understand that percentage will fluctuate based on revenue. If rent is $2,000 and I project $40,000 in sales, that is 5%. If sales drop to $30,000, rent becomes 6.7% of revenue. The dollar amount does not change, but the percentage does.

The value of percentage budgeting is that it keeps me focused on ratios and margins instead of just dollar amounts. It helps me understand the relationship between revenue and expenses. And it protects my profit margin when sales fluctuate because most of my variable expenses scale automatically.

How to Create a Budget for a Business on Excel (Free Template)

Excel is my budgeting tool of choice for building an excel budget. It is flexible, powerful, and does not require expensive software subscriptions.

I have built budgets in fancy accounting programs, and I have built them in simple spreadsheets. The spreadsheet approach works just as well and gives you more control over the structure.

I will show you exactly how I build my budgets in Excel.

Setting Up Your Budget Spreadsheet

I start with a blank budget worksheet and create a simple table structure.

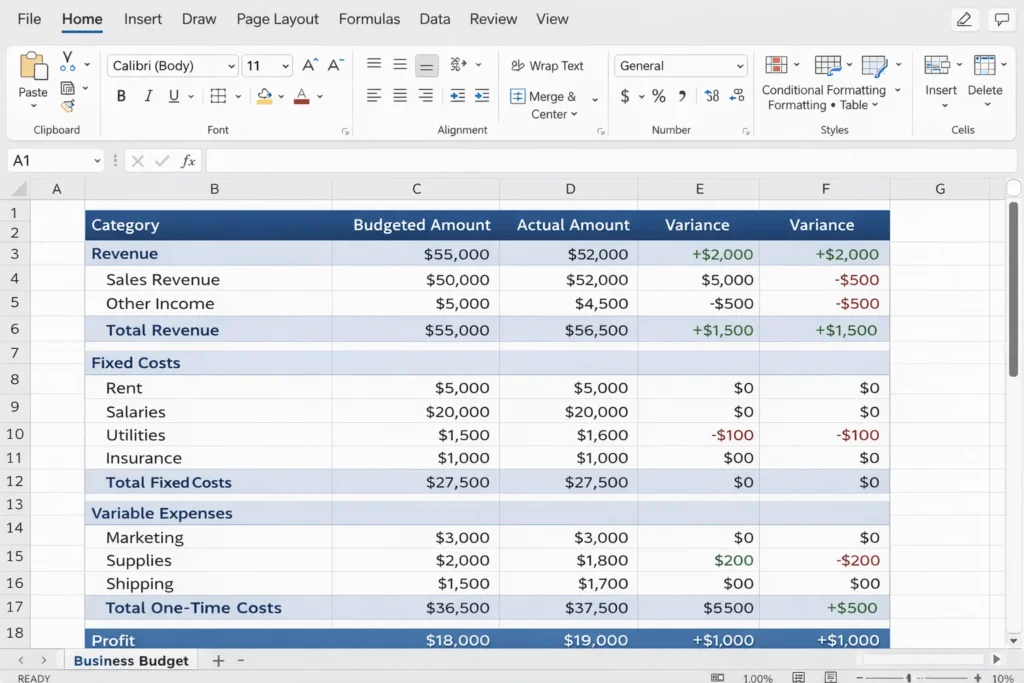

My column headers are Category, Budgeted Amount, Actual Amount, and Variance. These four columns give me everything I need.

The Category column lists all my income and expense categories. I group them into sections with headers. Revenue at the top, then Fixed Costs, then Variable Expenses, then One-Time Costs, then Profit.

Under Revenue, I list each income source separately. Product sales, service fees, consulting income, whatever applies to my business.

Under Fixed Costs, I list rent, salaries, insurance, subscriptions, and anything else that stays relatively constant.

Under Variable Expenses, I list cost of goods sold, commissions, shipping, and other costs that scale with sales.

Under One-Time Costs, I list any irregular expenses I am planning for that month.

At the bottom, I have a Profit line.

The Budgeted Amount column is where I enter my planned numbers for the month. This is what I expect to earn and spend.

The Actual Amount column stays empty until the month is over. Then I fill it in with what actually happened.

The Variance column calculates the difference between budget and actual. This shows me where I was on target and where I missed.

I also include a Total row at the bottom of each section. Total Revenue, Total Fixed Costs, Total Variable Expenses, Total One-Time Costs. These use SUM formulas to add up the numbers above them.

Finally, at the very bottom, I calculate net income, which I label as Net Profit. This is Total Revenue minus all the expense totals. It shows me whether I am projecting a profit or loss, and later it shows me whether I actually made or lost money.

Essential Excel Formulas for Budgeting

You do not need to be an Excel expert to build a functional budget. A handful of basic formulas handle everything.

The SUM formula adds up numbers. I use this for all my total rows. If my fixed costs are listed in cells B5 through B12, my formula in B13 is =SUM(B5:B12). This adds up all the fixed costs and puts the total in B13.

Subtraction calculates profit. If total revenue is in cell B3 and total expenses are in B20, my profit formula in B21 is =B3-B20. Revenue minus expenses equals profit.

The variance formula is just subtraction too. If budgeted marketing is in B10 and actual marketing is in C10, my variance formula in D10 is =C10-B10. Actual minus budget tells me if I overspent or underspent.

I also use percentage formulas. If I want to see what percentage of revenue I spent on marketing, I divide marketing expense by total revenue. If marketing is in B10 and total revenue is in B3, the formula is =B10/B3. Format that cell as a percentage, and Excel shows you the ratio.

I also use an IF formula sometimes to check whether I am hitting my profit target. If my target profit is 15% and I want to see whether I am on track, I can write a formula that compares actual profit percentage to 15% and displays On Target or Below Target based on the result.

But honestly, I keep most of my budget simple. SUM formulas for totals, subtraction for profit and variance, and percentage calculations to understand ratios. That covers 90% of what I need.

Download Our Free Business Budget Template

I have created a simple Excel template based on the exact structure I use in my own business.

The small business budget template has separate sections for revenue, fixed costs, variable expenses, one-time costs, and profit. All the formulas are built in. You just plug in your own categories and numbers.

I have also included a Google Sheets version for people who prefer working in the cloud. The functionality is identical.

The template includes sample categories to get you started, but you should customize it for your specific business. Delete categories that do not apply. Add ones that do. Make it fit your situation.

The template also includes a second tab for tracking budget versus actual over multiple months. This lets you see trends over time. You can spot patterns, identify problem areas, and watch your business improve month by month.

Using a template saves hours of setup time. You are not starting from scratch. You are building on a proven structure that already works.

10 Common Business Budgeting Mistakes (And How to Avoid Them)

I have made most of these mistakes myself. Others I have watched colleagues make. All of them are avoidable if you know what to watch for.

Mistake 1: Managing Without a Budget

This is the biggest mistake, and it is more common than you would think. Business owners operate on gut feeling and hope, tracking nothing, planning nothing.

I already shared the story of the business owner who made $500,000 in sales but operated at a loss. That happens when you have no budget.

Without a budget, you do not know if you are profitable until it is too late to fix it. You make spending decisions in the moment without understanding the cumulative impact. You cannot distinguish between a good month and a bad month because you have no baseline to compare against.

The fix is simple. Create a basic budget immediately. Even a rough one is infinitely better than none. You can refine it over time, but you need something in place now.

Mistake 2: Not Paying Yourself a Salary

Many business owners treat their own compensation as optional. They pay everyone else first and take whatever is left.

This creates two problems. First, your personal income becomes unpredictable. You cannot plan your personal finances because you do not know what you will earn.

Second, you undervalue your labor. You are working in the business. That work has market value. If you were not doing it, you would have to pay someone else to do it.

I made this mistake for two years. I reinvested every dollar back into the business, paid myself irregularly, and convinced myself I was being responsible by keeping costs low.

But I was not being responsible. I was being unfair to myself and creating an unsustainable situation.

Now I budget a reasonable salary for the work I do. If I am performing the roles of operations manager, salesperson, and customer service representative, what would those positions cost to fill? That number goes into my budget as a required expense.

Your salary is for your labor. Profit distributions are your return on ownership. These are separate things. Budget both.

Mistake 3: Using Debt for Business Purchases

I know this is controversial. Some business experts say strategic debt is smart. Leverage other people’s money to grow faster.

But I have seen too many businesses get crushed by debt payments they could not afford when revenue dipped.

Someone who built a $70 million Ramsey Solutions headquarters with cash taught me this. When you save monthly for big purchases, you avoid years of debt payments that strain your budget.

Let us say I need equipment that costs $100,000. I could finance it and pay $2,000 per month for five years. Or I could save $20,000 per month for five months and buy it with cash.

The saving approach requires more patience. But once I make the purchase, I am done. I do not have a $2,000 monthly obligation hanging over me for the next five years.

Those debt payments become fixed costs that you have to cover every single month regardless of sales. When you hit a slow period, they do not go away. They put pressure on your cash flow at exactly the wrong time.

I am not saying never use debt. Some situations might justify it. But I am saying that saving from retained earnings and paying cash is the safer, less stressful approach for most purchases.

Mistake 4: Wishful Thinking in Revenue Projections

New business owners especially fall into this trap. They create budgets based on best-case scenarios.

They assume everything will go perfectly. Sales will hit the high end of projections. No unexpected problems will arise. Every month will be better than the last.

Then reality hits. Sales come in below expectations. Unexpected costs pop up. Growth is slower than hoped.

The budget falls apart because it was built on optimism instead of realistic assessment.

Now I always look back six to twelve months. I account for seasonal variations. I identify trends over time rather than reacting to short-term fluctuations.

If you are a new business and do not have six months of data yet, use what you have but stay conservative. As you accumulate more history, your revenue projections will become more accurate.

Mistake 5: Confusing Goals with Budgets

I touched on this earlier, but it is worth repeating because I see this confusion constantly.

A goal is an aspiration. I want to make $1 million in sales next year. That is great. It sets direction. But it is not a budget.

A budget is the detailed tactical plan. It breaks down that $1 million into monthly targets. It lists every expense category. It assigns dollar amounts. It shows exactly where every dollar will come from and where it will go.

You need both financial goals and budgets, but they serve different purposes. Goals inspire you. Budgets keep you accountable and give you a roadmap for achieving those goals.

Do not confuse the two. Set your goals, then build a budget that supports them.

Mistake 6: Never Reviewing Budget vs. Actual

Creating a budget and then ignoring it is almost as bad as having no budget at all.

The real value of budgeting comes from comparing what you planned against what actually happened. This comparison tells you what is working and what needs to change.

I review my budget versus actual numbers every single month. I look at each category. Where did I overspend? Where did I underspend? Where was revenue higher or lower than expected?

More importantly, I ask why the budget variance occurred. If I spent $2,000 more on marketing than budgeted, was it because I found a profitable opportunity and invested more? Or did I lose discipline and overspend?

If revenue came in $5,000 higher than projected, was it a one-time windfall or a trend I can count on?

Understanding the why behind the numbers is more valuable than just seeing that they are different. It helps me make better decisions going forward through proper budget review.

Set a recurring monthly appointment with yourself to review your budget versus actual report. Make it non-negotiable. This habit will teach you more about your business finances than almost anything else.

Mistake 7: Using Fixed Dollars Instead of Percentages

I covered this in the percentage budgeting section, but it is worth including here because it is such a common mistake.

When you budget expenses as fixed dollar amounts, they do not adjust when revenue changes. You commit to spending $10,000 on marketing whether you make $50,000 or $100,000 in sales.

This puts your profit margin at risk. When sales drop, your expenses stay the same, and your profit gets squeezed or disappears entirely.

Percentage-based budgeting fixes this. When you allocate 10% of revenue to marketing, that dollar amount automatically scales. If revenue is $100,000, you spend $10,000. If revenue drops to $70,000, you spend $7,000. Your profit margin stays protected.

Use percentages for variable expenses. Use dollar amounts for truly fixed costs like rent, but understand that those fixed costs will represent different percentages of revenue as sales fluctuate.

Mistake 8: Only Reviewing One to Two Months of Data

When projecting revenue or analyzing expense patterns, do not rely on just one or two months of data. That is too narrow a window.

A single good month might be an outlier. Two months might miss seasonal patterns. You need at least six to twelve months of data to see real trends.

I learned this when I projected revenue based on two really strong months. I assumed that was my new normal and budgeted accordingly. Then sales dropped back to previous levels, and I had overspent based on an unrealistic forecast.

Now I always look back six to twelve months. I account for seasonal variations. I identify trends over time rather than reacting to short-term fluctuations.

If you are a new business and do not have six months of data yet, use what you have but stay conservative. As you accumulate more history, your projections will become more accurate.

Mistake 9: Mixing Business and Personal Funds

Keeping business and personal money in the same account creates chaos.

You cannot accurately track business profitability when personal expenses are mixed in. You cannot see true business costs when you are also buying groceries from the same account. Tax time becomes a nightmare of sorting through transactions.

I have seen business owners who pay for everything from one account. Business rent, personal mortgage, client lunches, family dinners, office supplies, kids school fees. It is all jumbled together.

Then they wonder why they cannot figure out if the business is actually making money.

Separate your accounts. Business income and expenses go through business accounts. Personal income and expenses go through personal accounts.

Pay yourself a regular salary or draw from the business to your personal account. That transfer is the dividing line. Everything before it is business. Everything after it is personal.

This separation makes budgeting, expense tracking, tax preparation, and financial analysis infinitely easier.

Mistake 10: Forgetting the Emergency Fund

Business emergencies are not a matter of if, but when. Equipment fails. Economic conditions shift. Clients do not pay on time. Unexpected opportunities require quick investment.

If you do not have an emergency fund, these situations become crises. You are scrambling for cash, making desperate decisions, or missing opportunities because you do not have liquidity.

I budget 5 to 10% of revenue for unexpected costs and emergencies. This builds a cushion over time.

When my laptop died unexpectedly, the emergency fund covered the replacement without stress. When a major client payment came in 45 days late, the emergency fund helped me cover payroll without panic.

Do not treat the emergency fund as optional. It is not what you save if there is money left over. It is a required allocation that protects your business from the surprises that will inevitably come.

How to Monitor Your Budget: Monthly Review Process

Creating a budget is step one. Monitoring it through consistent expense tracking and adjustments is where the real value comes from.

I review my monthly budget without fail. This habit has taught me more about business finances than any book or course ever could.

What is Budget vs. Actual (BVA) Analysis?

Budget versus actual analysis, often called BVA, is the process of comparing what you planned to happen against what actually happened.

At the start of the month, I create my budget. I project revenue, allocate expenses, and plan for profit. Those are my budgeted numbers.

At the end of the month, I pull my actual numbers from my accounting software or bank statements. Real revenue, real expenses, real profit. Those are my actual numbers.

Then I compare the two side by side. I calculate the budget variance for each line item. The difference between what I planned and what happened.

This comparison shows me where I was on target and where I missed. More importantly, it helps me understand why variances occurred.

If I budgeted $5,000 for marketing and spent $7,000, that is a $2,000 overage. But the number alone does not tell me much. I need to investigate.

Did I find a profitable advertising opportunity and intentionally invest more because the return justified it? That is a good variance. I made a smart decision to exceed the budget.

Or did I lose discipline and spend impulsively on marketing tactics that did not deliver results? That is a bad variance. I need to tighten controls.

The same goes for positive variances. If revenue came in $10,000 higher than budgeted, I need to know why. Did I land an unexpected one-time project? Or is my regular sales process producing better results than I thought?

Understanding the story behind the numbers helps me make better decisions going forward. It shows me what is working, what is not, and where I need to adjust my approach. This comparison between my budget and income statement spots problems early.

How Often Should You Review Your Budget?

I review my monthly budget without exception. That is the sweet spot for most small businesses.

Monthly reviews give you enough data to spot meaningful patterns without overwhelming you with constant analysis. You can see trends developing and course correct before small problems become big ones.

Some businesses do a quarterly budget review instead. This works if your business is mature, stable, and predictable. But I think quarterly is too infrequent for most small businesses. Three months is a long time. Problems can compound significantly in that window.

Weekly reviews are too frequent unless you are in a very volatile business or managing a tight cash flow situation. Most businesses do not have enough meaningful change week to week to justify that level of scrutiny.

I also do an annual budget review in addition to monthly ones. Once a year, I look at the full twelve months together. I analyze big-picture trends. I evaluate whether my overall financial strategy is working. I set goals and build budgets for the year ahead.

But the monthly review is my backbone. It is the habit that keeps me connected to my business finances and prevents surprises.

When to Adjust Your Budget Mid-Year

Your budget is a plan, not a prison. When circumstances change, you need to adjust.

I make budget adjustments when several things happen.

If sales significantly exceed or miss projections for multiple months in a row, I update my revenue forecast. One outlier month does not warrant a change, but if I have beaten my sales target by 20% for three straight months, I am clearly being too conservative. I raise my projection to match the new reality.

The same goes for consistent underperformance. If sales are missing targets month after month, I need to adjust my budget to reflect realistic expectations rather than wishful thinking.

Major cost changes also trigger budget adjustments. If my rent increases, that is a permanent change to my fixed costs. I update the budget immediately to reflect the new expense level.

When new opportunities arise, I evaluate whether to adjust the budget to accommodate them. If I identify a profitable marketing channel that requires investment beyond what I budgeted, I might reallocate funds from less productive categories or increase my marketing budget while accepting a temporarily lower profit margin.

Economic conditions sometimes require budget changes. If I see clear signs of a recession affecting my industry, I might cut discretionary spending and build my cash reserves faster.

The key is making adjustments deliberately, not reactively. I do not change my budget every time I have one unexpected expense or one slow week. But when I see sustained patterns or permanent changes, I update the budget to reflect the new reality.

I also learned something valuable about adjusting budgets mid-year. If you are trying to save for a critical purchase, like a replacement vehicle or essential equipment, you might need to temporarily adjust other priorities.

Let us say I need to save $30,000 for a service truck within six months. That is $5,000 per month I need to set aside. If that does not fit in my current budget, I might need to slow down debt payments temporarily or cut back on growth investments to free up that cash.

This is a strategic trade-off. I am accepting less progress in one area to ensure I can make a necessary purchase without taking on debt. Once the truck is purchased, I can redirect that $5,000 back to its original purpose.

Best Business Budgeting Tools: Excel, QuickBooks, and More

You do not need expensive software to budget effectively. But the right tools can make the process easier and more efficient.

I have used everything from simple spreadsheets to comprehensive accounting platforms. Here is what I have learned about the options available.

QuickBooks

QuickBooks is the most popular small business accounting software, and for good reason. It handles everything from invoicing to expense tracking to financial reporting.

The budgeting features in QuickBooks let you create budgets, compare them to actuals, and generate variance reports. Everything integrates with your actual financial data, so you do not have to manually enter numbers twice.

I use QuickBooks for my business accounting. The budget versus actual reports save me hours every month. I can see immediately where I overspent or underspent without building custom spreadsheets.

The downside is cost. QuickBooks is not cheap, especially if you want the advanced features. You are looking at $30 to $200 per month depending on which plan you choose.

For businesses that need full accounting functionality beyond just budgeting, QuickBooks is worth the investment. For businesses that only need budgeting and are comfortable with simpler tools, it might be overkill.

Excel or Google Sheets

I started with Excel, and honestly, it still works great for many businesses.

Excel gives you complete control over your budget spreadsheet structure. You can customize everything exactly how you want it. You can build in whatever formulas and calculations you need. You can create multiple tabs for different scenarios or time periods.

The learning curve is minimal if you know basic formulas. And the cost is zero if you already have Excel, or free if you use Google Sheets.

The downside is that Excel requires manual data entry. You have to pull numbers from your bank statements or accounting software and type them into the spreadsheet. There is no automatic integration.

You are also responsible for accuracy. If you make a formula error, you will not know until the numbers do not add up.

But for a simple, flexible, low-cost budgeting solution, Excel or Google Sheets work perfectly well. I still use spreadsheets for certain types of financial planning even though I have QuickBooks.

When to Hire an Accountant or Bookkeeper

Software helps, but sometimes you need human expertise.

I recommend working with an accountant or bookkeeper when your business reaches certain complexity thresholds.

If your revenue exceeds $100,000 per year, you probably benefit from professional help. At that level, the financial stakes are high enough that mistakes get expensive. A good accountant can save you more in taxes and financial efficiency than they cost in fees.

If you are spending more than five hours per week on financial tasks, that is a sign you should delegate. Your time is worth money. If you can pay someone $500 per month to handle tasks that take you 20 hours, and you can use those 20 hours to generate more than $500 in revenue, the math makes sense.

If you have employees, payroll complexity usually justifies professional help. Payroll taxes, compliance requirements, and reporting obligations create significant risk if handled incorrectly.

If tax complexity increases beyond basic Schedule C sole proprietor returns, an accountant becomes valuable. Corporations, partnerships, multi-state operations, or significant asset purchases all create tax situations where professional guidance pays for itself.

I work with a bookkeeper who handles my monthly reconciliations and financial statement preparation. I work with a CPA who handles tax planning and filing. These professionals cost me money, but the ROI is clear. They save me time, reduce my stress, and help me make better financial decisions. The investment has been worth every dollar.

Other budgeting tools worth mentioning include Xero, which is similar to QuickBooks but with a different interface that some people prefer. FreshBooks is good for service-based businesses that do a lot of client invoicing. Wave offers free basic accounting software with optional paid features.

The best tool is the one you will actually use consistently. Start with whatever fits your budget and skill level. You can always upgrade to more sophisticated tools as your business grows and your needs become more complex.

Start Your Business Budget Today

I have given you a lot of information in this guide. Creating a budget for a business can feel overwhelming when you are looking at all the pieces together.

But here is what I want you to remember. The most important step is starting. A simple, imperfect budget that you actually use is infinitely better than no budget at all.

You do not need to implement every strategy I have shared to create a business budget that works. You do not need fancy software or complex formulas. You just need to put your numbers on paper and start assigning every dollar a purpose.

That shift from managing money in your head to managing it on paper gives you power. You stop guessing and start knowing. You protect your profit instead of hoping for it. You make decisions based on facts instead of feelings.

I have watched businesses transform when they start budgeting. The business owner who was making $500,000 but losing money turned everything around with a budget. Within six months, he went from operating at a loss to keeping more profit than he thought possible.

That is what budgeting does. It reveals the truth about your finances. It forces you to make intentional choices. And it guarantees that you are building a business that actually makes money, not just generating sales.

Start simple if you need to. Pick the basic seven-step process I outlined. Project your revenue. List your fixed costs and variable expenses. Set a profit target. Build in a contingency fund. Make sure the math adds up.

Put those numbers in a spreadsheet. Compare them to what actually happens each month. Learn from the variances. Adjust as you go.

That is all budgeting really is. Planning what you will do with money before it arrives, then comparing that plan to reality and learning from the differences.

If you want help getting started, download the free business budget template I mentioned earlier. It has all the structure built in. Just customize the categories for your business and plug in your numbers.

Set aside two hours this week to build your first budget. Two hours to take control of your business finances. Two hours to move from chaos to clarity.

Your future self will thank you. Because putting those numbers on paper does not just change your business. It changes how you think about money, how you make decisions, and how you grow.

You now know how to create a budget for a business. The question is, will you actually do it? Will you assign a destination for every dollar? Will you protect your profit and build your financial confidence?

Start today. The power is already in your hands. You just need to put it on paper.

Note: While I have shared what works for me and many other business owners, every business is unique. Consider consulting with a CPA or financial advisor for personalized guidance based on your specific situation.

Frequently Asked Questions About Business Budgeting

How do I create a budget if my business has no historical data?

Creating a budget for a new business without historical data starts with researching industry benchmarks from trade associations or business groups in your field. Talk to other business owners in similar businesses to understand typical revenue patterns and expense ratios. Consult with an accountant who specializes in your industry. They often have data from other clients that can guide your estimates.

The key is budgeting conservatively. Do not project best-case scenarios. Use lower revenue estimates and higher expense estimates than you hope for. Start with percentage-of-revenue allocations based on industry standards. For example, retail typically spends 30% on cost of goods sold. Service businesses often spend 40% on labor.

As you collect your own data over the first three to six months, you can refine your budget based on actual performance instead of guesses. The important thing is to start with something, even if it is imperfect. You will adjust as you go.

What is the difference between a budget and a financial goal?

A financial goal is an aspirational target that sets direction for your business. When you say I want to make $1 million in sales next year, that is a goal. It inspires you and gives you something to work toward.

A budget is the detailed tactical plan showing exactly how you will earn that revenue and where you will allocate every dollar on a monthly basis. It breaks down the $1 million into monthly targets, lists every expense category with dollar amounts, and shows what profit you will keep.

Goals set direction. Budgets provide the roadmap for achieving those goals. You need both, but they serve completely different purposes. Without a goal, you have no destination. Without a budget, you have no plan to get there.

How should I pay myself as a small business owner?

Budget two separate components for owner compensation. First, pay yourself a market-rate salary for the work you perform in the business. If you are handling operations, sales, and customer service, what would you pay someone else to do those jobs? That amount goes in your budget as a fixed cost.

Second, take profit distributions for your ownership stake in the business. This is your return on investment, separate from payment for your labor.

Many business owners make the mistake of only taking leftover profit. This creates unpredictable personal income and undervalues the work you do. Budget your salary as a required expense, just like rent or any other cost.

The Profit First method allocates 40% of revenue to owner pay automatically. This forces you to pay yourself first instead of hoping there is something left over at the end of the month.

Should I use percentages or fixed dollar amounts in my budget?

Use percentages for variable expenses because they automatically scale with revenue changes. This protects your profit margin when sales fluctuate.

For example, if you budget marketing as 10% of revenue instead of a fixed $10,000, your spending automatically adjusts. When sales drop from $100,000 to $70,000, your marketing budget drops from $10,000 to $7,000. Your profit margin stays protected because expenses scale with revenue.

Use fixed dollar amounts for truly fixed costs like rent and base salaries since these do not change with sales volume. But understand that these will represent different percentages of revenue as your sales fluctuate.

The percentage approach guarantees profitability even when your sales forecast is wrong. As long as you stick to your percentage allocations, your profit percentage stays protected.

How often should I review my business budget?

Review your budget monthly using Budget vs. Actual reports. Compare what you planned to what actually happened in each category.

Monthly reviews give you enough data to spot meaningful patterns without overwhelming you with constant analysis. You can identify problems early and course correct before small issues become major crises.

Focus on understanding why variances occurred, not just seeing the numbers. If you overspent on marketing by $2,000, was it a smart investment that brought extra sales, or did you lose discipline? This understanding helps you make better decisions going forward.

Mature businesses with stable, predictable operations can sometimes manage with quarterly reviews. But for most small businesses, monthly is best practice. It is the habit that keeps you connected to your finances and prevents surprises.

What percentage of my budget should go to each expense category?

Typical small business allocations are marketing 5 to 10%, salaries and labor 20 to 30%, rent and overhead 5 to 10%, cost of goods sold 25 to 35% for product businesses, and profit 10 to 20%.

However, percentages vary significantly by industry. Restaurants typically spend 30% on food costs. Service businesses often spend 40% on labor. Retail stores might spend 50 to 60% on inventory.

Use industry benchmarks as starting points, then adjust based on your actual data after three to six months of operation. Your specific business model will determine the right ratios for you.

Trade associations like SCORE and the Small Business Administration often publish these benchmarks. Your accountant probably knows them for your industry too. The key is starting with reasonable estimates and refining them as you collect your own data.

When is the best time to create my annual business budget?

Create your annual budget in Q4, specifically October through December. This timing allows you to review the current year’s performance, identify trends, and set goals before the new fiscal year begins.

You have enough data from the current year to make informed projections. You can see what worked and what did not. You can spot seasonal patterns. And you have time to finalize your plan before January 1st.

For businesses with fiscal years that do not match the calendar year, start budgeting two to three months before your new fiscal period begins. This gives you enough time to analyze data, make projections, and finalize your plan before implementation.

The worst time to create a budget is when you are already in the middle of a crisis. Plan ahead. Give yourself time to think strategically instead of reacting to immediate pressure.

Should I save for large business purchases or use financing?

Saving monthly from retained earnings is the safer, less stressful approach for most business purchases. If you need $100,000 in equipment, save $20,000 per month for five months and buy it with cash.

This avoids debt payments that strain your budget for years. Once you make the purchase, you are done. You do not have a $2,000 monthly obligation for the next five years that you must cover regardless of sales performance.

Debt payments become fixed costs that do not go away during slow periods. They put pressure on your cash flow at exactly the wrong time.

However, financing might make sense if the purchase generates immediate revenue that covers the payment. For example, if you are a growing logistics business and a delivery truck will bring in $5,000 per month in new contracts, a $2,000 monthly payment might be justified.

Just budget the monthly payments as a fixed cost and understand that this obligation will stay with you through good months and bad. Make sure the numbers work before you commit.