How Much Money Should you Have Saved by 30? Here’s the Real Answer

If you’re wondering how much money should you have saved by 30, you’re probably feeling some pressure right now. Maybe you’ve seen the benchmarks floating around. Maybe a friend casually mentioned their 401(k) balance and you quietly panicked. That anxiety is understandable but before you spiral, let’s look at what’s actually true about savings at 30, not just what the textbooks say.

Personal finance milestones like the 1x salary rule exist to give you direction. But the gap between those targets and what most people actually have is enormous and it exists for real, documented reasons.

I spent most of my late 20s avoiding this question entirely. Partly because the answer felt uncomfortable, and partly because nobody explained it clearly. When I finally sat down and added up my actual accounts at 29, the number was both better and worse than I expected in different ways. That experience is exactly why I wanted to write this.

The Reality: What Most 30-Year-Olds Actually Have (Not What They Should)

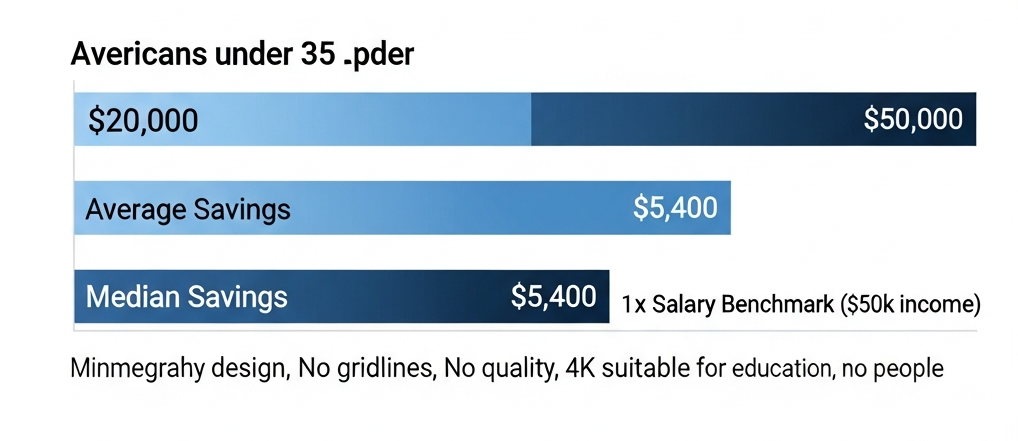

Millennial savings statistics from the Federal Reserve’s 2022 Survey of Consumer Finances tell a clear story: the average American under 35 holds less than $20,000 in total savings. When high earners are removed from that calculation, the median drops to just $5,400. That means half of all people in your age group have under six thousand dollars saved. Many of them are also carrying credit card balances and student loan debt on top of that.

The average savings by generation shows a wide range some 30-year-olds have $300,000 saved, others have nothing. Both groups can still build wealth from where they stand.

Financial experts typically say you should have 1x your annual salary saved by 30. If you earn $50,000, that’s a $44,600 gap from the national median. That gap is real, it’s documented, and this article addresses every part of it.

Here’s what that means for you practically: if you have $15,000 saved by 30, you’re already ahead of the majority of people your age. If you have $30,000, you’re well ahead. If you have $5,000, you’re right at the national median which means you’re not alone in that position at all.

The 1x Salary Benchmark: What It Means and Why It Exists

The 1x salary rule comes from Fidelity Investments and has become one of the most cited retirement savings benchmarks in personal finance. It’s the industry standard for measuring retirement readiness, and once you understand the logic behind it, the whole framework makes more sense.

By age 25, about halfway through, you should have roughly $10,000 to $15,000 accumulated a checkpoint that helps you gauge whether you’re tracking toward the 1x salary goal by 30.

The logic is this: if you earn $50,000 and have $50,000 saved by 30, you’re on pace to retire comfortably in your late 60s assuming you keep contributing and investing consistently. It assumes you started working around age 22, saved 10 to 15 percent of your income each year, and invested that money so it could grow.

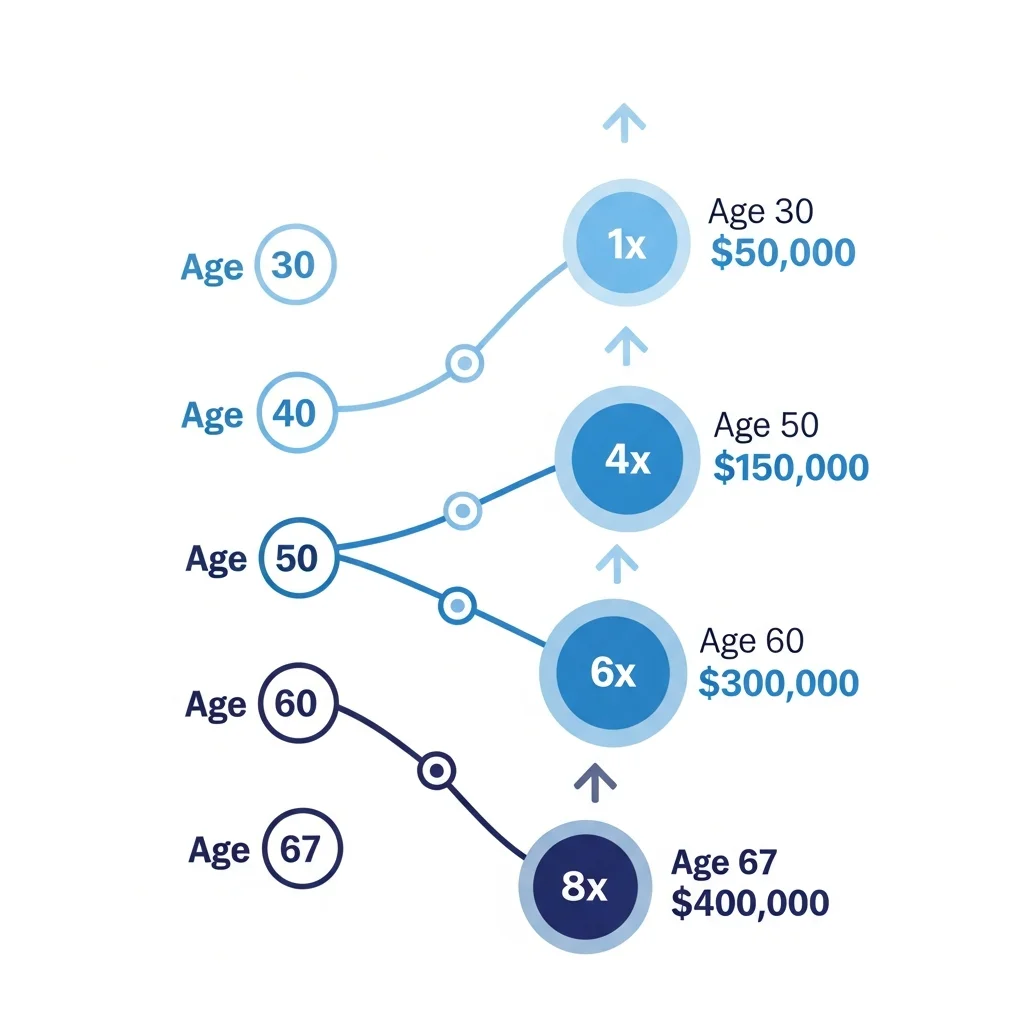

Financial planning by age works on a tiered milestone system:

By age 30, the goal is 1x your annual salary. On $50,000, that’s $50,000 total. By age 40, it jumps to 3x so $150,000 on that same income. By age 50, it’s 4x ($200,000). By age 60, it’s 6x ($300,000). By age 67 the standard target for retirement age planning the goal is 8x your annual salary, or $400,000 in this example.

The reason the multiple accelerates is compound interest. Your money isn’t sitting still it’s invested and growing year after year. The earlier you start, the more that growth does the heavy lifting.

The problem is that this benchmark assumes a lot went right for you. It assumes no major student loan debt. It assumes you weren’t earning minimum wage in your early 20s. It assumes no medical emergency or family crisis drained your accounts. For a lot of people, those assumptions simply don’t hold up.

Why Most People Fall Short (Without Judgment)

Three patterns consistently explain why most people fall short of the 1x salary benchmark and none of them are about laziness or bad character. These reflect real millennial financial challenges: student debt, stagnant wages in early careers, and a cost of living that keeps outpacing income growth.

Lifestyle inflation is when a raise quietly disappears into spending rather than savings. You were living on $45,000, got promoted to $55,000, and then upgraded your apartment, started eating out more, and swapped your phone. A year later, you’re spending almost all of that $10,000 increase and your savings barely moved. If that pattern sounds familiar, the first practical step is to reduce monthly expenses before the next raise arrives.

The financial education gap is real. Most people were never taught how money actually works. Schools covered algebra and history, but not budgeting, compound interest, or the difference between saving and investing. So we enter adulthood trying to make major financial decisions with no foundational knowledge which explains a lot of the savings shortfall.

Starting late is simply part of many people’s timelines. If you graduated with debt, spent your early 20s building a career, or dealt with family obligations, saving wasn’t a priority. But when you’re 30 and haven’t been investing since 22, you’ve missed eight years of compound growth. That gap is real — and completely catchable.

These reasons are about being human. They’re about living in a world where unexpected things happen, where jobs don’t always pay what you need, and where nobody handed you a roadmap. This isn’t a moral failing. It’s just how most people’s financial lives actually unfold.

What “1x Your Salary Saved” Actually Means

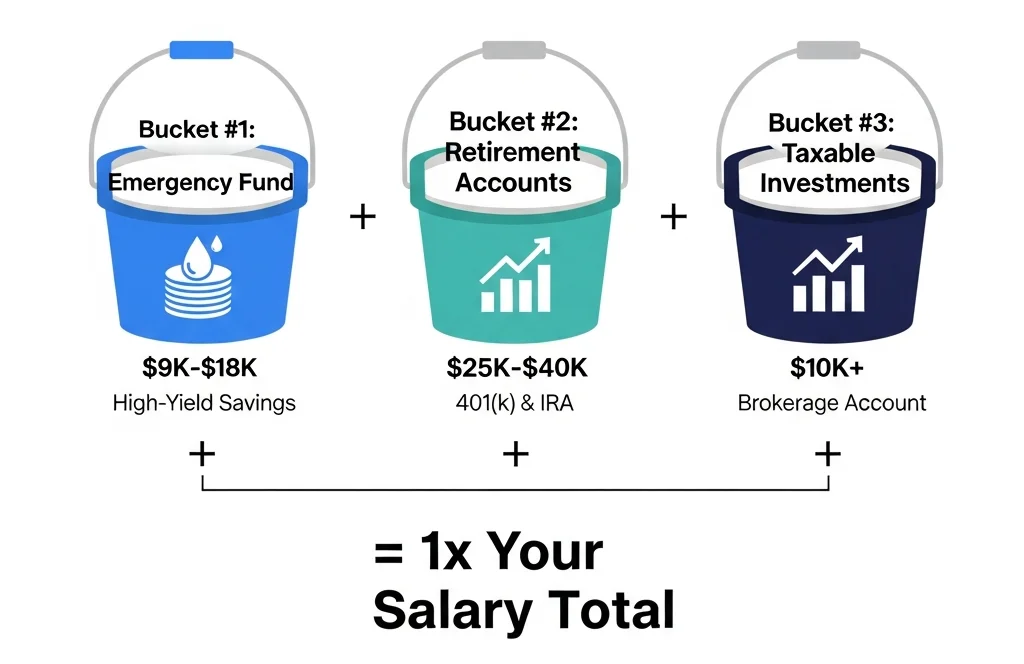

One thing most people miss about the 1x salary rule is what it actually includes. The confusion around saving vs. investing at 30 starts here: most people assume “1x your salary saved” means $50,000 sitting in one bank account. That’s not what it means at all.

Your total savings picture is the sum of three completely different buckets each with a different purpose, a different account type, and a different role in your financial life. Understanding this removes most of the anxiety immediately.

Bucket #1: Emergency Fund (3 to 6 Months of Expenses)

This is your financial foundation, and it’s the bucket that gets funded first.

The emergency fund guidelines are simple: keep between three and six months of living expenses in a high-yield savings account where you can access the money immediately. If your monthly expenses are $3,000, you’re targeting $9,000 to $18,000 in this bucket. The range depends on how stable your income is. If you’re self-employed or work in a field with frequent layoffs, lean toward six months. If your job is stable, three months often works fine that’s the three-month emergency fund rule in practice.

This money doesn’t live in the stock market. It doesn’t chase returns. It sits in a high-yield savings account (HYSA) currently earning around 4 to 5% APY and if you want to calculate what your HYSA is actually earning on your specific balance, the math is simpler than most people expect. The goal of this bucket isn’t growth. It’s peace of mind.

The goal of this bucket isn’t growth. It’s peace of mind. It’s what keeps you from reaching for a credit card when your car breaks down or your hours get cut.

Bucket #2: Retirement Accounts (401k and IRA)

This is where most of your real wealth accumulates and where most people dramatically underestimate how much they’ve already built.

If you’ve been contributing to a 401(k) since age 22, you likely have somewhere between $20,000 and $40,000 in retirement accounts by 30. That money doesn’t show up in your checking account, so people often forget it exists. But retirement account contributions are a huge part of your actual net worth at 30, and they absolutely count toward your 1x salary target.

When you contribute to your 401(k), you get the power of employer matching typically 3 to 6% free money plus tax-deferred growth and decades of compound interest. That $25,000 at age 30, with continued contributions at a 7% average annual return, can grow to well over $200,000 by age 65. You’re building wealth in the background whether you think about it or not.

This bucket also includes IRA contributions. A Roth IRA grows tax-free forever you pay taxes now, and every dollar of growth comes out at retirement completely untaxed. A Traditional IRA grows tax-deferred, reducing your taxable income today. If you’re weighing which structure makes more sense for your situation, understanding how to reduce the tax on your savings more broadly is a useful starting point.

One often-overlooked option: if your employer offers an HSA-eligible health plan, a Health Savings Account gives you triple tax advantages contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. For many people, maxing out an HSA before a taxable brokerage account is the smarter move.

Bucket #3: Taxable Brokerage Investments

The third bucket handles whatever remains between your emergency fund, retirement accounts, and your total 1x salary target.

If your goal is $50,000 by 30 and you have $15,000 in your emergency fund and $25,000 in retirement accounts, you’d need roughly $10,000 in a taxable brokerage account to hit your number. This money is invested in low-cost index funds not individual stocks, not crypto, not anything speculative. This is where the wealth-building timeline really accelerates over time, because you’re adding capital to a tax-advantaged system.

The beauty of starting this at 30 is compound interest by 30 working in your favor for the next three and a half decades. At a 7% average annual return, $10,000 grows to approximately $106,000 in 35 years without adding another dollar. Add regular contributions, and the number climbs dramatically from there.

Where Each Dollar Goes

Here’s the quick reference for account placement:

Emergency fund → High-yield savings account (HYSA). Currently earning 4 to 5% APY. Fully liquid, zero risk.

401(k) contributions → Through your employer’s payroll system. Pre-tax dollars, which lower your taxable income today.

IRA contributions → Roth IRA (tax-free growth forever) or Traditional IRA (tax-deferred growth). Which you choose depends on your current tax bracket and expected future income.

Taxable investments → A brokerage account at Vanguard, Fidelity, or Charles Schwab. Index funds only. Accessible anytime, though capital gains taxes apply on profits.

Once you see the three buckets this way, the 1x salary target stops feeling like an impossible pile of cash you need to stockpile. It’s distributed across accounts that serve different purposes, and together they add up to your actual financial foundation.

Do You Actually Need to Hit This Benchmark Exactly at 30?

The 1x salary rule is a guideline, not a verdict. It’s a measuring stick, and like all measuring sticks, it works better for some people’s timelines than others.

Financial educator George Kamel of Ramsey Solutions uses a letter-grade net worth system that removes the pressure of hitting one specific benchmark at one specific age. It gives you a realistic picture of where you stand regardless of income level:

Grade A: $100,000 to $1,000,000+ net worth. You have significant assets and minimal debt. You’re on track.

Grade B: $10,000 to $100,000 net worth. You’re building wealth and ahead of most people your age. Keep going.

Grade C: $0 to $10,000 net worth. You’re just getting started, but you’re starting.

Grade D: Negative $1 to negative $100,000 net worth. Your debt exceeds your assets. Common for young people with student loans. You need a plan.

Grade E: Below negative $100,000 net worth. Serious attention required, but fixable with a multi-year strategy.

If you’re at 30 and hit 1x your salary, you’re in Grade A or high Grade B. If you have $30,000 saved, you’re solidly Grade B. If you have $5,000, you’re Grade C. None of these is a life sentence they’re life stage financial planning indicators that tell you where you are and what to work toward next.

The question isn’t whether you hit this benchmark by exactly age 30. The question is whether you’ve started building wealth. Whether you’re moving in the right direction. Whether you’re making progress, even if the textbook says you should be further along.

Income-Based Savings Targets: What You Should Actually Have Saved by 30

What you should have saved by age 30 varies dramatically based on your actual income and life circumstances. The 1x salary rule means something very different on a $35,000 salary versus a $90,000 one, and treating them the same ignores the real math behind cost of living.

If You Earn $30,000 to $45,000 Annually

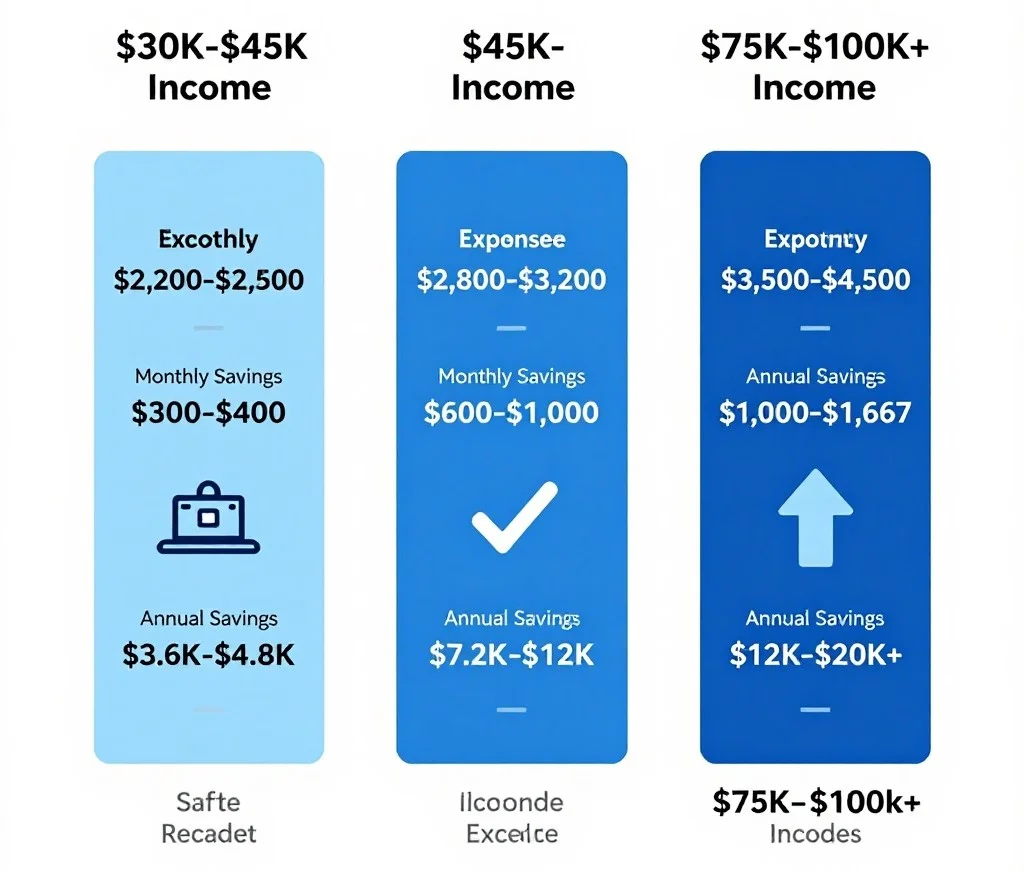

At this income range, the strict 1x benchmark asks for $30,000 to $45,000. But the math of daily life at this income level makes that genuinely difficult to hit.

On $35,000 in a mid-cost city, rent alone at $1,200 per month is $14,400 annually. Add utilities, food, transportation, and insurance, and you’re looking at $2,200 to $2,500 per month in essential expenses. That leaves a narrow window for savings. Saving $300 to $400 monthly is aggressive but realistic at this income level and it would get you to roughly $28,000 by 30 if you started consistently at 22.

Regional cost of living differences are real. In a higher cost-of-living city, that same income leaves even less room, and your realistic savings target will be lower. That’s not a personal failure — it’s a mathematical reality, and there’s no shame in acknowledging it.

The good news: if you can consistently save 10 to 15 percent of your income at this level, even $20,000 invested at 30 can grow to hundreds of thousands of dollars by 60 or 65. The savings discipline and habits you build now matter more than the dollar amount you’re starting with.

If You Earn $45,000 to $75,000 Annually

This is the income range where the 1x salary benchmark becomes genuinely achievable for most people.

On $60,000, your target is $60,000 by 30. Breaking that down: $60,000 over 8 working years is $7,500 per year, or $625 per month. If you’re saving 15 percent of your gross income standard financial planning advice you’re saving $750 per month. You’re right in the zone.

The income and savings correlation at this level is more favourable than at lower incomes. Essential expenses consume a smaller percentage of your paycheck, leaving more room to breathe, to save, and to invest without feeling perpetually deprived.

That said, reaching the benchmark still requires intention. Most people in this range who haven’t been deliberate about money will land somewhere between $25,000 and $40,000 saved by 30. That’s still a solid position and it’s a foundation you can build from quickly.

If You Earn $75,000 to $100,000+ Annually

High earners share one predictable pattern when it comes to savings anxiety: they often feel like they should have more than they do. Someone making $100,000 might expect to have $100,000 saved by 30, then add up their accounts and find $60,000 and feel behind even though they’re objectively ahead of most people their age.

The culprit is almost always lifestyle inflation or a late start. Reaching 1x your salary at this income level is very achievable you have more money left after essential expenses, and saving 15 to 20 percent doesn’t require radical sacrifice. But it only happens if the higher income is paired with deliberate savings behaviour.

Earning more money is only half the equation. Someone earning $75,000 who saves 20 percent of their income will build dramatically more wealth than someone earning $100,000 who saves 5 percent. Income is the input. Net worth is the outcome. What happens in between is entirely up to you.

The Percentage Approach: Why Your Savings Rate Matters More Than the Dollar Amount

The specific dollar amount you save matters less than the percentage of your income you’re consistently putting away. This is the reframe that changes how most people think about building wealth.

If you’re earning $40,000 and saving 15 percent, you’re saving $6,000 per year. If you’re earning $80,000 and saving 15 percent, you’re saving $12,000 per year. The dollar amounts are different, but you’re making the same financial commitment keeping 85 percent of your income and directing 15 percent toward your future.

Personal savings rate is the metric that actually predicts long-term wealth accumulation, not the dollar balance at any given age.

The key is picking a percentage you can sustain. If you try to save 30 percent and it’s so painful you quit after three months, you’ve lost. If you save 10 percent consistently for the next 30 years, you’ve won — compound interest handles the rest. Savings rate benchmarks exist as targets, not finish lines. Start where you can, automate it, and increase the percentage every time your income grows.

Net Worth at 30: Why Your Income Doesn’t Determine Your Financial Health

This is the insight that changed how I think about money. I used to assume someone earning $200,000 per year must be wealthy. Then I learned that the same person could have $200,000 in student loans, a $400,000 mortgage, car payments, and credit card debt. Subtract what they owe from what they own, and their net worth could easily be negative. Six figures of income, technically broke.

Meanwhile, someone earning $50,000 with no debt and $40,000 in savings has a higher net worth. They’re wealthier, even though they earn a fraction of the first person’s salary.

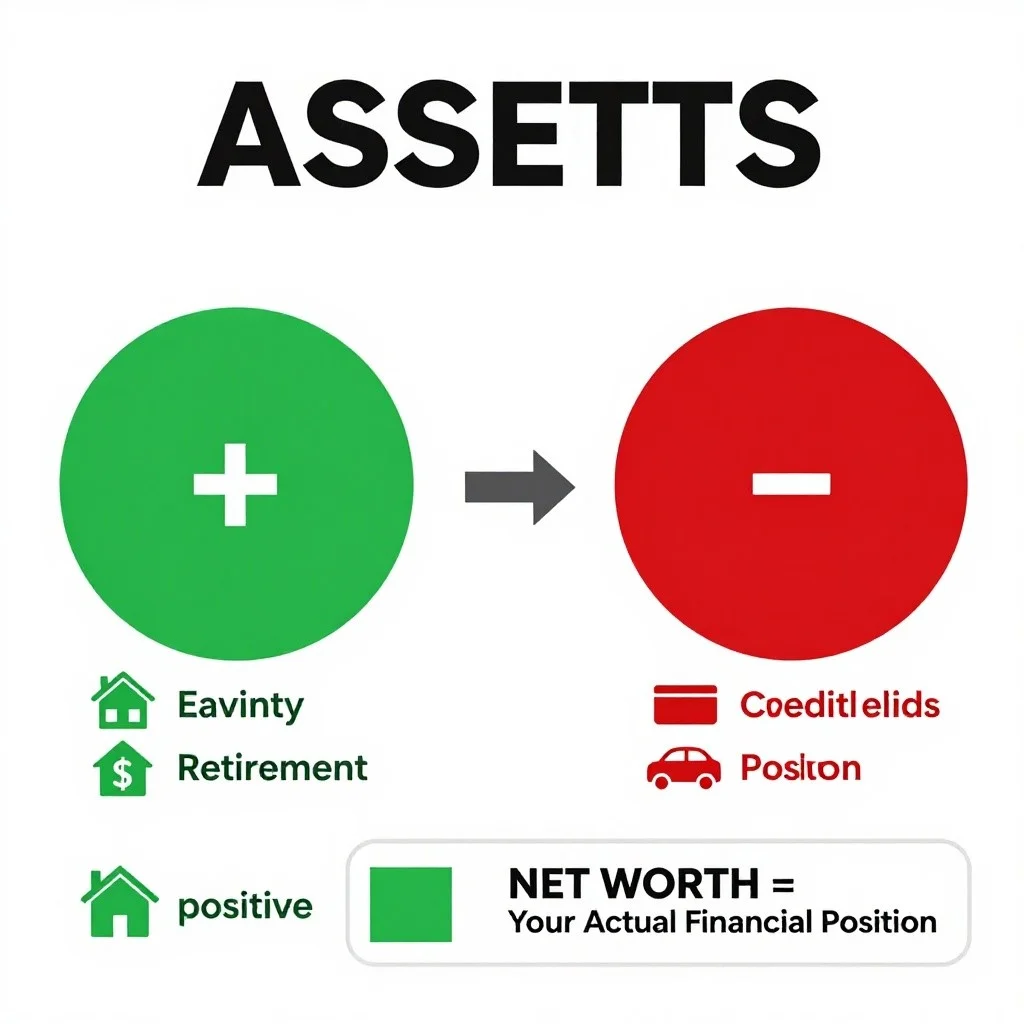

The net worth calculation formula is simple:

Net Worth = Assets − Liabilities

Your assets include everything with value: savings accounts, home equity, car value, retirement accounts, and taxable investments.

Your liabilities include everything you owe: mortgage balance, car loan, student loans, personal loans, medical debt and how much credit card debt is too much is a question worth answering before you calculate your final number. Subtract liabilities from assets. That number is your actual financial position.

Real Examples: Why High Earners Are Sometimes Behind

Person A : Medical School Graduate: She’s 30, earns $150,000 as a physician. Impressive income. But she has $200,000 in student loan debt, $50,000 in home equity, and $80,000 in savings and retirement accounts.

Net worth: $50,000 + $80,000 − $200,000 = −$70,000.

Her income is high, but her debt is higher. That said, her income trajectory means she can close this gap within 5 to 10 years which is why current net worth at 30 and future earning potential are both part of the real picture.

Person B : Software Engineer: He’s also 30, earns $100,000. No student loans, no car loan. He has $80,000 in home equity and $70,000 in savings and retirement accounts. His only debt is his mortgage.

Net worth: $80,000 + $70,000 = $150,000.

He earns $50,000 less per year, but his net worth is $220,000 higher. Same age, dramatically different financial position because of debt management at 30, not income.

This is why net worth at 30 is the number that actually matters, not what shows up on your paycheck.

How Debt Affects Your Savings Target

The credit card debt vs. savings question is one I encounter constantly and the answer genuinely depends on your debt-to-income ratio and the interest rate you’re paying.

High-interest debt makes saving feel pointless, because mathematically it often is. If you’re paying 22% interest on a credit card while earning 7% in investments, you’re losing 15% every year on the overlap. You can’t outpace 22% credit card interest with any reasonable investment return. The debt has to go first.

But not all debt is created equal, and your strategy depends entirely on the interest rate.

Credit card debt (18 to 25% interest): Pay this aggressively before building a large investment portfolio. This is non-negotiable.

Personal loans (8 to 12% interest): Second priority. Attack these fairly aggressively, but you can begin building other savings simultaneously because the rate isn’t completely destroying your progress.

Student loans (4 to 6% interest): These can coexist with investing. If your loan charges 4% and you can historically earn 7% in index funds, the math says invest the extra money rather than overpaying the loan. Make your regular payments, but don’t sacrifice your retirement contributions to pay these faster. If you do want to pay off student debt faster alongside investing, there are specific strategies that make that possible without derailing your savings progress.

Mortgage (rate varies widely): Mortgage rates vary depending on when you locked in recent buyers may carry 6 to 7%, while those who refinanced in 2020 to 2021 may have rates closer to 3%. Either way, a mortgage is expected long-term debt. Most financially healthy people carry one for 30 years. Unless your rate is unusually high, prioritizing early payoff over investing rarely makes mathematical sense.

The rule of thumb: if the interest rate is above 10%, attack it. If it’s below 5%, you can invest alongside it.

The Debt Snowball vs. Debt Avalanche

Two methods dominate the debt payoff conversation.

The debt avalanche is mathematically optimal: list debts by interest rate, highest first, and attack them in that order. It minimizes total interest paid over time.

The debt snowball ignores interest rates entirely: list debts from smallest balance to largest and attack the smallest first. Once that debt is gone, roll its payment into the next one.

Research in behavioral finance consistently shows that people complete debt payoff plans when they get early wins which is exactly what the snowball provides. Personal finance educator George Kamel of Ramsey Solutions teaches that compliance rates matter more than mathematical optimization in debt elimination. The best debt payoff method is the one you’ll actually finish. For most people, that’s the snowball even if the avalanche would save slightly more on paper.

I’ve watched people quit after three months of avalanche because they saw no visible progress. I’ve watched people finish the snowball because each small payoff kept them going. The behavior is what matters.

Can You Pay Off Debt AND Build Savings at the Same Time?

Yes and the sequence is what makes it work.

First, build a $1,000 emergency fund. This is your minimum safety net. Without it, any surprise expense creates new debt while you’re trying to eliminate existing debt.

Second, attack all high-interest debt aggressively. Credit cards, personal loans, anything above 10%.

Third, once the high-interest debt is gone, expand your emergency fund to 3 to 6 months of expenses.

Fourth, then shift into aggressive savings and investing toward your full 1x salary target.

One person I know was 30 with a mortgage, a personal loan, and a household income around $85,000. They still managed to contribute $15,000 per year to retirement and investments while making aggressive debt payments by automating savings first and treating debt payoff as a fixed monthly expense. It’s possible when you have a clear sequence and you stick to it.

Four Savings Methods That Actually Work : Which One Fits You?

There’s no single right way to save by 30. Different strategies suit different personalities, income levels, and starting points. Here’s how four proven frameworks compare, using real numbers so you can see what each one actually produces over time. Savings rate benchmarks vary widely across these methods from 10% to 25%+ and the right one is the one you’ll maintain for decades, not just months.

Method #1: The Richest Man in Babylon (Save 10%)

One of the oldest personal finance books ever written makes the simplest argument: save at least 10% of your income, invest it, and let time handle the rest.

On a $50,000 salary, that’s $5,000 annually about $417 per month. Invested in a basic index fund at a 7% average annual return, that $417 per month grows to approximately $1.2 million over 35 years. The math is almost uncomfortably simple, which is the point. This method works because it’s sustainable. You’re not cutting your lifestyle in half. You’re not obsessing over every dollar. You save a consistent personal savings rate, automate it, and let compound interest by 30 work in your favour for decades.

Best for: people who value simplicity and want a strategy they can maintain forever without burning out.

The catch: you need to start early and never stop.

Method #2: The Dave Ramsey Approach (15% After Debt)

This method takes a different sequence: eliminate all consumer debt first using the debt snowball, then redirect 15% of your income into retirement savings.

The reason this builds more wealth than the 10% method is the freed-up cash flow. When you’re no longer making debt payments, that money goes directly into savings. Using a 7% average annual return, saving 15% for 30 years after a 5-year debt elimination phase produces approximately $1.8 million by age 65.

Building wealth in your 30s accelerates sharply once debt is eliminated. The psychological and mathematical advantage of becoming debt-free before aggressive saving is real — you feel lighter, your money works harder, and you stop fighting upstream against interest charges.

Best for: people carrying meaningful debt credit cards, personal loans, or high-interest student loans.

The downside: the debt elimination phase requires serious, focused commitment.

Method #3: The 50/30/20 Budget Rule

This is a whole-budget framework, not just a savings target. Fifty percent of after-tax income covers needs (rent, utilities, groceries, insurance). Thirty percent covers wants (dining out, entertainment, hobbies). Twenty percent goes to savings and debt repayment.

On a $50,000 income, investing that 20% ($10,000 annually) at a 7% average return produces approximately $2.4 million by age 65. That’s nearly double the Babylon method’s outcome because you’re saving twice the percentage.

The 50/30/20 budget rule appeals to people who need structure and visual clarity. You always know where your money is going. You’re not guessing. The framework is clear, and if you follow it consistently, the results follow too.

Best for: people who like concrete rules and clear allocation — and who are willing to actually track their spending.

The challenge: it requires honest budgeting. Some people love this; others find it exhausting.

Method #4: Aggressive Savings (20%+)

This is for people who want to maximize wealth accumulation or pursue financial independence by 30 or 40 whether through the FIRE (financial independence, retire early) movement or simply a desire to retire well ahead of traditional timelines.

Saving 25% of your income over 35 years at a 7% return produces approximately $3 million or more by age 65. Some people reach this level significantly earlier by combining high savings rates with income growth.

On $50,000, saving 25% means living on $37,500 per year. That requires real lifestyle decisions, not just minor adjustments. It’s achievable, but it isn’t casual. Most people underestimate their ability to do this and most also overestimate how much their quality of life will suffer.

Best for: high earners, those motivated by aggressive wealth-building timeline goals, or people with unusually low fixed expenses.

Which Method Is Right for You?

The honest truth is that any of these methods will build serious wealth if you maintain it for decades. The best method is simply the one you’ll actually follow for the next 20 or 30 years.

Do you have high-interest debt? Start with the Dave Ramsey approach. Do you want simplicity above everything else? Go with the 10% Babylon method. Do you need clear structure and category rules? Use the 50/30/20 budget rule. Do you want to maximize growth and have the income to back it up? Go aggressive at 20%+.

Your personality matters more than the percentages.

The Compound Interest Math: Why Starting at 30 Still Gives You a Massive Advantage

If you’re 30 and haven’t started investing yet, you might feel like the damage is already done. You’re not too far behind. The math proves it. Starting at age 30 with consistent savings and letting compound interest work for you over 35 years is genuinely a strong position. Here’s why. The key is to start investing now rather than waiting for the ‘right’ moment—because time in the market consistently beats timing the market.

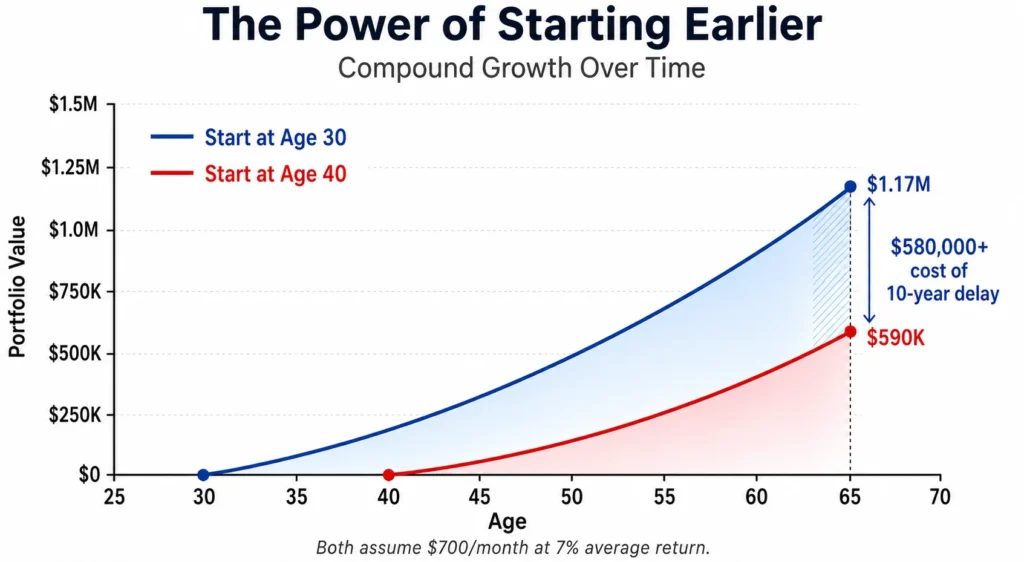

If you save $700 per month about $8,400 per year and invest it in a basic index fund earning an average 7% annual return (reflecting the historical average of the S&P 500, as documented by sources including NYU Stern’s market data and Vanguard’s long-term return analysis), here’s what happens by age 65:

After 35 years, that $700 monthly contribution grows to approximately $1.17 million. Past returns do not guarantee future results, but this figure reflects the 7% return assumption used consistently throughout this article.

You’re contributing roughly $294,000 out of pocket over 35 years. The remaining $876,000 is pure compound growth money you never had to earn, just allow to accumulate.

Now here’s what the 10-year delay actually costs. If you wait until age 40 to start that same $700 monthly contribution, with only 25 years to grow at 7%, you accumulate roughly $590,000 by 65. The difference between starting at 30 and waiting until 40 is over $580,000 more than half a million dollars lost to a single decade of inaction.

Your time horizon is the most valuable asset in your investment strategy. At 30, you still have 35 years of it.

What About Inflation?

This is a legitimate concern. At a 3% annual inflation rate over 35 years, your $1.17 million in future dollars would have purchasing power closer to $400,000 to $450,000 in today’s dollars. That’s still a meaningful retirement foundation.

Using the 4% withdrawal rule the standard guideline that lets you safely withdraw 4% of your portfolio annually a $1.17 million portfolio supports roughly $46,800 per year in retirement income. With Social Security added, for many people that’s a comfortable retirement.

More importantly, this is why market returns and inflation context matters: keeping your money in a savings account earning 0.5% while inflation runs at 3% is actively making you poorer. Investing in the market is how you stay ahead of inflation. That’s the entire point of a 35-year time horizon.

Real Catch-Up Stories

Real catch-up stories are common in personal finance communities, and they all share the same pattern.

One person shared their journey starting at 30 with under $3,000 saved. They committed to a 15% savings rate, automated it immediately, and stayed consistent through job changes, market downturns, and unexpected expenses. By age 43 13 years later they had accumulated over $220,000.

Another started at 30 with absolutely nothing on a $45,000 salary. By age 40, they had $150,000 saved. Not through a windfall or inheritance. Through consistent saving, automation, and refusing to quit when progress felt slow.

The pattern in every success story is the same: they started, they automated it, they increased contributions when their income grew, and they didn’t quit when life got hard.

You’re 30 With Nothing Saved? Here’s Your Realistic Catch-Up Plan

If you’re reading this at 30 with zero saved, you’re not doomed. You still have 35 years until standard retirement age, and that is not a consolation it’s a mathematical advantage. What you need now isn’t guilt about the past. It’s a clear, step-by-step plan for the next 10 years.

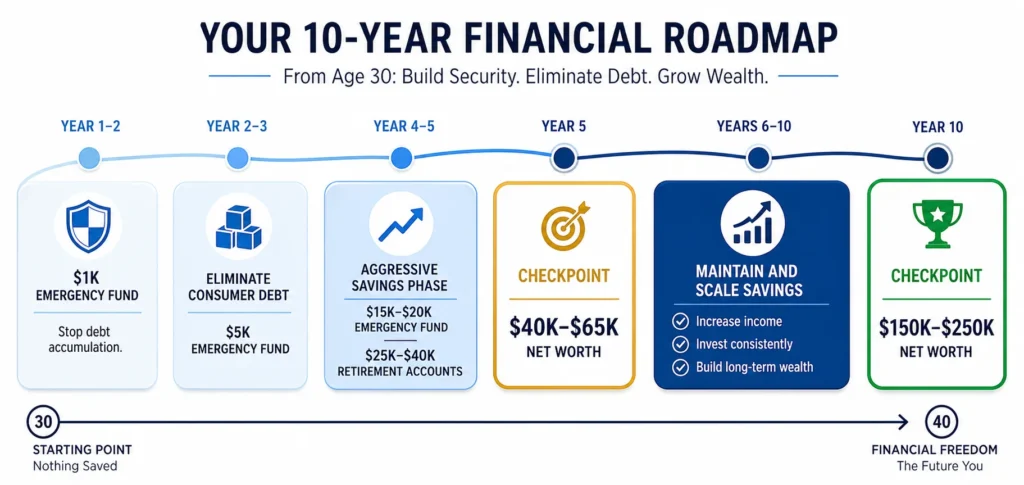

Year 1: Stop Adding Debt and Build Your Foundation

First priority: stop accumulating high-interest debt. If you’re still regularly carrying credit card balances, that stops now. Not because of shame because the math makes saving nearly impossible while you’re paying 20%+ interest on growing balances.

Second priority: build a $1,000 emergency fund. This is your buffer against life. Car repair, medical bill, one difficult month whatever happens, this cushion keeps you from sliding backward.

Third priority: if your employer offers a 401(k) match, contribute enough to get it. If they match 3%, you contribute 3%. This is a 50 to 100% instant return on your money, and it compounds for 35 years. It’s not optional. It’s the foundation of your retirement account contributions strategy.

Setup time: 4 to 5 hours. Then it’s automated forever.

Years 2 to 3: Eliminate Consumer Debt

With your $1,000 buffer in place and employer match secured, focus entirely on eliminating credit cards, personal loans, and any high-interest debt using the debt snowball. List debts smallest to largest, attack the smallest with every extra dollar, and roll each paid-off payment into the next debt.

Simultaneously, push your emergency fund up to $5,000. This takes the financial stress down meaningfully.

By the end of year 3, you should be consumer-debt-free or very close to it.

Years 4 to 5: Aggressive Savings Phase

This is where the wealth-building timeline actually starts to accelerate. Your debt payments are gone. That cash flow is now yours to direct. Push 15 to 20% of your income straight into retirement and taxable investments.

On $50,000, that’s $7,500 to $10,000 per year going to work for you. Complete your emergency fund to the full 3 to 6 months of expenses if your monthly expenses are $3,000, your target is $9,000 to $18,000.

Year 5 Checkpoint — What You Should Have:

Emergency fund: $15,000 to $20,000 Retirement accounts: $25,000 to $40,000 (depending on contributions and employer match) Taxable investments: $0 to $5,000 Total net worth: roughly $40,000 to $65,000

You’ve gone from $0 to over $50,000 in 5 years. That’s real. Celebrate it most people never do what you just did.

Years 6 to 10: Maintain, Scale, and Don’t Get Bored

Consistency is what turns a good start into actual wealth. Continue your 15 to 20% savings rate. Every time you get a raise, increase your savings by half of it. Let the other half improve your quality of life — but don’t let the whole raise evaporate into lifestyle.

Year 10 Checkpoint : Where You Actually Are:

At age 40, following this plan with reasonable market returns, your net worth should be in the $150,000 to $250,000 range. You started at zero a decade ago. You built this from nothing.

More importantly: from 40 to 65, at a 15 to 20% savings rate and 7% average returns, you’re on track to add another $1 million to $2 million to that foundation. You’re not just catching up — you’ve caught up.

Monthly Savings Targets by Income

$40,000 annually: Save $400 to $600 per month (10 to 15% of gross). At this income level, hitting those targets likely requires cutting discretionary expenses significantly or adding supplemental income through a side gig or raise.

$60,000 annually: Save $600 to $1,000 per month. Reasonable and sustainable for most people at this income.

$100,000 annually: Save $1,000 to $1,667 per month. This is where catching up becomes genuinely achievable without radical lifestyle sacrifice.

Common Catch-Up Obstacles (And Real Solutions)

“I can’t save on my salary.” Either increase your income or decrease your spending often both. A side gig earning $200 to $300 monthly adds $2,400 to $3,600 annually. Negotiating a $3,000 raise is possible if you actually try. Both are real options.

“Life keeps happening : medical bills, car repairs.” That’s exactly what the emergency fund is for. Once you have 3 to 6 months of expenses saved, these aren’t crises anymore. They’re just expenses you cover and move on from. Build the fund first.

“I don’t have the discipline.” Automate it. Savings discipline and habits are far easier to build when the system removes the decision entirely. The money moves before you see it. You can’t spend what isn’t in your checking account.

“I feel demoralized because I’m behind at 30.” You’re 30, not 50. You have 35 years until retirement. The difference between people who build wealth and people who don’t isn’t that they started earlier — it’s that they started, and they didn’t quit when they felt demoralized. Start today. Don’t quit. That’s the whole strategy.

The 30-Day Action Plan: Start Building Wealth Right Now

Everything in this article is useless unless you do something with it. Here’s your first month, broken into specific steps you can start today.

This Week: Calculate Your Target Number

Spend 15 minutes on this. Open a spreadsheet, a notes app, or a piece of paper. Write your annual gross income (before taxes). Multiply it by 0.10 for a baseline 10% savings rate. Multiply by 0.15 if you want to follow standard financial planning advice. Multiply by 0.20 if you want to be aggressive.

Adjust for your situation. If you have high-interest debt, scale back to 5% for now and prioritize the debt. Write your number down and put it somewhere visible.

That’s your target monthly savings. That’s what you’re aiming for.

Week 2: Audit Your Current Savings

Thirty minutes maximum. List every financial account you have: checking, savings, 401(k), any investments. Write down every balance. Add them up. That simplified number is your current net worth.

Subtract your liabilities credit card balances, student loans, car loan. That’s your real net worth at 30. Write it down. That’s your starting point.

Week 3: Set Up Automatic Transfers

One hour to set up, then automated forever.

If you don’t have a high-yield savings account currently earning 4 to 5% APY, open one today. Wealthfront, Marcus, and Ally are commonly used options compare current rates on a site like Bankrate before choosing, as rates change frequently. This is not a sponsored recommendation.

Set up an automatic transfer on payday. Your target monthly savings amount moves to your HYSA automatically. The money transfers before you see it. You can’t spend what isn’t in your checking account.

If you have access to a 401(k) and you’re not getting the full employer match, fix that immediately. That free money is non-negotiable.

Week 4: Find $100 to $300 Extra Per Month

Two to three hours total. You don’t need to overhaul your life. Look for small wins:

Meal prep twice a week instead of eating out saves $100 to $200 monthly for most people. Cancel one subscription you haven’t used in three months. Call your phone company or internet provider and ask for a better rate. Many people save $20 to $50 monthly just by asking. Commit to a small side income stream tutoring, freelancing, delivery driving that brings in $100 to $200 monthly.

Goal: find $100 to $300 extra per month without destroying your quality of life.

Month 2: Verify and Celebrate

Five minutes. Confirm your automatic transfer went through. Open a simple spreadsheet and write today’s date and your current total savings. That’s your baseline.

Run a quick calculation using a free compound interest calculator to see your projected growth: at your current monthly savings rate, what will you have by 35? By 40? By 50?

Set a monthly reminder first of every month to spend 5 minutes checking this number. Not obsessing. Just checking.

Year 1 Milestone: Assess and Adjust

By the end of month 12, at $500 to $600 monthly, you should have roughly $6,000 to $7,000 saved (before investment returns). With a 7% annual return, you’re closer to $6,200 to $7,200.

You went from $0 to over $6,000 in one year. That’s real progress. Celebrate it. Then update your plan: did you get a raise? Increase your savings percentage. Did your expenses change? Adjust accordingly.

The automation continues. The compounding continues. Thirty-four more years of this and you’ve built the $1.17 million we talked about earlier from $700 per month, starting from zero at 30.

The 5 Mistakes That Cost 30-Year-Olds Hundreds of Thousands of Dollars

You can follow a solid savings strategy and still lose hundreds of thousands of dollars by making one critical error. These are the mistakes I see most consistently and each one has a specific, actionable fix.

Mistake #1: Ignoring Your Employer 401(k) Match

This is the easiest money you will ever make, and it’s staggering how commonly it goes uncollected.

If your employer matches 3% of your contribution on a $50,000 salary, contributing $1,500 gets you another $1,500 free a 100% instant return. That employer match alone, compounding at 7% annually for 35 years, grows to roughly $400,000 by age 65.

If you’re not contributing enough to get the full match, you’re giving away $400,000. Not metaphorically actually. If your employer offers matching, you must contribute enough to capture it completely. This is the single most important retirement account contribution decision you can make.

Mistake #2: Lifestyle Inflation

You get a $5,000 raise. The nicer apartment sounds reasonable. The newer car feels deserved. More restaurants feel like a fair reward. A year later, the raise has completely disappeared into spending and your savings rate hasn’t moved.

Lifestyle inflation is how people earn six figures and still feel financially stressed. Catching it early — before the habits lock in is far easier than reversing it later.

What actually works: when you get a raise, let 25 to 50% improve your lifestyle if you want that. Take the other 50 to 75% and increase your retirement savings immediately. You still feel the raise — life gets a little easier but you’re also building real wealth. Someone who gets three $5,000 raises and invests 75% of each one accumulates $30,000 to $40,000 extra in invested assets over 8 years. At a 7% return, that becomes $50,000 to $70,000 by age 40.

Mistake #3: Keeping Money in a 0.1% Savings Account Instead of a HYSA

Your bank is paying you 0.01% on your savings. High-yield savings accounts are currently paying 4 to 5%.

On $50,000, that difference is $50 per year versus $2,500 per year a gap of $2,450 annually. Over 10 years, you’re missing $30,000+ in interest you’re simply not collecting.

Banks are designed to make switching feel inconvenient that friction keeps your money earning them money instead of you. But you only have to overcome it once, and then the automatic transfer runs forever. Open a high-yield savings account, move your emergency fund there, and collect the interest you’re owed.

Mistake #4: Carrying High-Interest Debt While Trying to Save

You’re trying to save at a 7% average annual return while carrying credit card debt at 20% interest. Mathematically, this doesn’t work. The debt is eating your gains faster than your savings can build them. You’re fighting upstream.

Paying off high-interest debt isn’t glamorous, but it’s foundational. You cannot build lasting wealth while paying 20% interest on revolving balances. Once you’re debt-free, your money can actually work for you instead of against you. That’s when wealth-building actually begins.

Mistake #5: Comparing Yourself to Others and Quitting

Your friend has $200,000 invested at age 32. You have $40,000. You feel demoralized, and you quit trying.

What you don’t know: your friend inherited $100,000. Or their parents paid for their entire education. Or they started saving at 22 and had 10 uninterrupted years to accumulate. Comparison destroys motivation because you only see the final number, never the full story.

If you’re 30 and you start now and stay consistent for 35 years, you’ll have over $1.17 million. If someone else also has $1.17 million at retirement, you’re not behind. You’re equal. The only difference is the journey.

Focus on your trajectory, not their position. Compete with your past self. Be better at 35 than you were at 30. That’s it. The people who build real wealth are the ones who start, stay consistent, and refuse to quit when they feel behind. That can be you.

FAQs: How Much Should I Have Saved by 30?

I’m 30 with Only $15,000 Saved. Am I Completely Behind?

No, you’re ahead of the national median of $5,400. The 1x salary benchmark is a target, not a verdict. At 30, you still have 35 years until standard retirement age, and that time horizon is your most valuable asset. Focus on your savings rate going forward, automate it, and use the catch-up plan in this article. You’re not behind you’re starting.

Does the 1x Salary Rule Apply if I Have High Student Loan Debt?

If you’re carrying substantial student loan debt, adjust your expectations and your sequence. Stop creating new debt, commit to at least 10% of your income toward retirement savings to protect your future, and build an aggressive debt payoff plan. As you pay down debt, your net worth increases even if your savings balance stays the same a $10,000 loan payment improves your net worth by $10,000. You’re building wealth on two fronts simultaneously.

I Just Got a Raise. Should I Save More or Improve My Lifestyle?

Increase your savings first, not your lifestyle. This is the single most powerful wealth-building move available to you at this stage. Keep living on your previous income and invest the entire raise for the first year. Then, if you want to let some of it improve your life, make that a deliberate choice not a default drift into lifestyle inflation.

Should I Save in My 20s, or Is Starting at 30 Okay?

Starting in your 20s is better. But starting at 30 is absolutely fine if you actually do it. The only question that matters now is whether you’ll start today. The past is locked in your future wealth depends entirely on what you do from this moment forward.

What Percentage of Income Should I Save: 10%, 15%, or 20%?

Ten percent is the minimum. Fifteen percent is the standard target for building real wealth at a sustainable pace. Twenty percent or higher is for those who want to accelerate significantly or pursue financial independence early. More important than the number: pick a savings rate benchmark you can maintain for years without burning out. Consistency beats perfection every time.

Should I Pay Off Debt or Build an Emergency Fund First?

Build a $1,000 emergency fund first. Then attack high-interest debt aggressively. Then expand the emergency fund to 3 to 6 months of expenses. Then invest. This sequence protects you from recreating debt during the payoff phase which is the most common reason debt payoff plans fail.

Can I Catch Up if I Start Saving Seriously at Age 35?

Yes, with real commitment. Hitting 1x your salary by 35 is probably off the table, but reaching 3x to 4x by 50 is completely achievable with a 15 to 20% savings rate, increasing income, and strict spending discipline. The people who catch up fastest are those who increase their earnings and refuse to let lifestyle inflate with them.

Why Do Some 30-Year-Olds Have $200K While Others Have $0?

Different life paths create dramatically different starting points. Some people started at 18 with no student debt and family financial support. Others graduated at 25 with significant debt and entered a workforce that didn’t pay what they expected. The benchmark assumes you started at 22, earned a steady income, saved consistently, and faced no major disruptions. Real life is rarely that clean. Stop comparing your Chapter 2 to someone else’s Chapter 10.

What Should I Never Do With My Money?

Avoid high-fee investment accounts a 2% annual fee costs you roughly $400,000 by retirement compared to a low-cost index fund. Avoid picking individual stocks roughly 90% of stock pickers underperform simple index funds over time. Avoid treating crypto as an investment strategy rather than speculation. Avoid dipping into your emergency fund for non-emergencies. And avoid carrying high-interest debt while trying to build savings you’re working directly against yourself.

The pattern across all of these: boring strategies beat exciting ones. Index funds beat stock picking. Consistency beats chasing returns. Discipline beats speculation. Build wealth slowly and deliberately, and you’ll actually build it.

All compound interest projections in this article use a 7% average annual return, reflecting the historical long-term average of the S&P 500 as reported by sources including NYU Stern School of Business market data and Vanguard’s long-term investment research. Past performance does not guarantee future results. This article does not have affiliate relationships with any financial institutions mentioned. Platform suggestions are based on commonly referenced options always compare current rates before opening any account. This article is for informational purposes only and does not constitute financial advice. Consult a licensed financial advisor for guidance specific to your situation.