Budget 101: A Beginner’s Guide to Your Money

When I was first searching for budget 101 basics, I was overwhelmed! I began to budget for a beginner budget for the first time in my life and I believed it meant I couldn’t enjoy anything. Which is why I didn’t use to go to them for years. I guess I got it all wrong.

A budget isn’t a penalty. It is not a diet that you take away everything you like. A monthly budget is nothing more than a plan that informs your money where it should go before you spend it and it’s created again every month based on what you are realistically earning and what you are realistically spending. The one turnaround mentality of that difference in thinking has changed my whole financial life.

I found myself down to my last few dollars every month after a few years, having a pretty good job.After a few years, I found myself with the last few dollars in my bank account, and I did have a pretty good job. I was always broke today, I never really knew why.

The reality was so simplistic, I had no control over my money, because I had no plan for it. I sat down and made my first “real” budget, and I was surprised to find out this. I still had the freedom to go out with my friends, get coffee and treat myself occasionally. It was different this time, because the buying this time had meaning and limits. Real money management is about deliberate, not limiting.

The whole point of budgeting is to control finances. Rather than asking yourself at the end of the month, “Where did my money go?,” you’re taking proactive steps with your money before it has even been used. “It isn’t deprivation, it’s freedom.” Each dollar is allocated for a reason and each spend is part of a plan.

I have learned that budgeting is the beginning point of all financial planning and one of the personal finance basics. Without it, saving and investing and growing wealth is akin to a shot in the dark. You finally have a budget base that will support you in life when things get rocky.

The reason that most people don’t want to budget is that they believe it will reveal their shortcomings or make them “cut back” on their consumption. I felt that way as well. My discovery, though, was freedom. As I learned I don’t have to feel guilty about spending money because I knew exactly what I could afford.

I have since been able to go to the bank without worring about having to pay my bills because I had a true system in place. The reality is that money management is not a difficult task. It must be honest.” But it all begins with knowing that a budget is not a straitjacket.

The Budget 101 Step Most Beginners Skip (Do This First)

Here’s my first three budgeting blunders – and it’s one of the most prevalent budget 101 mistakes that newbies make. I sat down with a blank spreadsheet and made a guess on what I spent every month.

I knew I had spent something around $400 on groceries, perhaps $100 on gas, and I’m sure I spent $200 on dinner outings. Those figures seemed like they had been taken out of a hat. Their understanding was totally incorrect.

Choose a starting date today is good. Record all of your every purchase for the next 30 days. All coffee, all grocery shopping, all subscription fees, all gas fill-ups. All of it. There’s no need for a sophisticated application to monitor expenditures.

I noted it on my cell phone in the notes app and updated it all day. After a month, I sorted it all into categories. It is at this point that the real wake-up moments occur.

I knew I had been subscribed to more than $80 per month and was racking up way more than I was using. I realized that my ‘occasional’ DoorDash usage was bringing me a cost of $300 per month. Then it dawned on me that my perception of what I was spending and what I truly was spending were in two different worlds.

It’s just as crucial to track your income as it is to track your spending, yet most beginners skip this step entirely. If you’re unsure where to start, learning how to calculate your monthly income accurately makes a huge difference. I thought I earned a steady amount each month, but when I actually wrote down the numbers, I realized my side hustle income varied by hundreds of dollars from one month to the next.

The other months I brought in an additional $400. Other months, nothing. If the income is not regular, then it’s difficult to create a reliable budget.

The next steps are all dependent on spending awareness. There simply are things you cannot fix if you can’t see them. After having a full month of real data, classify it. Set up spending buckets: the house, transportation, food, entertainment, and subs.

There are patterns you will notice you have never seen before. You will be able to see exactly where the money is going. This is the most important thing you’ll do, and that is rather tedious, as I will not sugarcoat it. It makes budgeting more than a guess, it’s a true plan with actual numbers. Leave it out and your budget is unsound. If you do, the remainder of the situation is much easier.

How to Create a Budget in 5 Steps

After I finally had a good grasp of my actual spending, I was prepared to create a budget that really would stick.

Most people go to this step first and forget to track. Hence their budget problems. Making a budget is really just five simple steps, and they follow the same budgeting process I’ve been using for years one that’s recommended by certified financial planners and personal finance educators such as the National Foundation for Credit Counselling (NFCC).

Once you get it, it’s not hard to understand, but it does call for self-discipline in viewing numbers you don’t want to see. Let me show you how I do it.

Step 1: Add Up Your Real Monthly Income

The initial thing you need to do is understand what your real income is per month.

Not what you are making or what you made last year, what’s getting into your pocket? I did an early mistake of basing my budget on the number I was offered, my gross income. This was a disaster! You don’t pay your rent with gross income. Net income does.

If you are like me and have several income streams, put them all down: your main job, a side hustle, freelancing, rental income, anything that brings you a steady income. The hard-learned lesson: only use conservative numbers! I would work through the budget and budget a monthly income of $500 because for a few good months I was making that much money as a freelancer.

Then there was a lull in the work and all my finances were ruined. Now I’m only counting income I can count on. If it is something extra then it is a bonus not part of the base plan.

Step 2: Write Down Every Expense

That month of tracking will come back to bite you on the ass when it comes to the actual part in the story. You’ll record each item of expenditure, which can be divided into fixed and variable costs.

The fixed expenses are the ones that are the same every month rent or mortgage, car loan, car insurance, health insurance, phone bill, internet, and the recurring bills such as streaming services or any software that I pay for for work.

These are guaranteed and fixed. You’ll have a firm understanding about the price and when they are due.

Variable expenses are more complicated because they change depending on your decisions and situation – groceries, gas, meals out, entertainment, clothes, personal care. These are the categories that you will need, but the amount spent on these can vary widely from month to month.

When I was getting started, one error I would often make was approximating these costs in my head. I’d estimate I was spending around $300 on groceries, but memory is a terrible record keeper. If you struggle with estimating food costs like I did, budgeting for groceries specifically can help you set realistic numbers based on your actual household needs.

I look at the bank and credit card statements from the past month or two and write down the REAL values in my budget. Every dime that I spend on food, gasoline, restaurant meals, check. I count them all up and take that genuine total as my starting point.

If it was not consistent, take the previous 2-3 months and find the average to create a more accurate baseline. At this point, it’s not about limiting, it’s about seeing the big picture of where your money is going.

Step 3: Set a Specific Financial Goal

If you don’t have a goal, then your budget is simply a spending tracker, and it won’t help you get anywhere!

I would have financial goals that were motivating but would never get me anywhere like increase income or save more money or get out of debt. The problem with “wanting to” is that there’s no “how” to try.The problem with “wanting to” is there’s no “how” to try.

Rather than, “save more,” I began to tell them to save $1,000 for an emergency savings account in four months.

Rather than ‘pay off debt’ I told them ‘pay off my $2400 credit card debt in 12 months, paying an additional $200 in each payment. The change resulted in an all-changing. All of a sudden I had a goal something I could measure, track, and know if I am winning or losing.

The first question to ask yourself regarding your financial objective is: what exactly do I want to accomplish? How much will it cost? When do I want to achieve it? If you’re wondering what realistic goals look like for your age and situation, checking savings benchmarks can help you set targets that are both challenging and achievable.

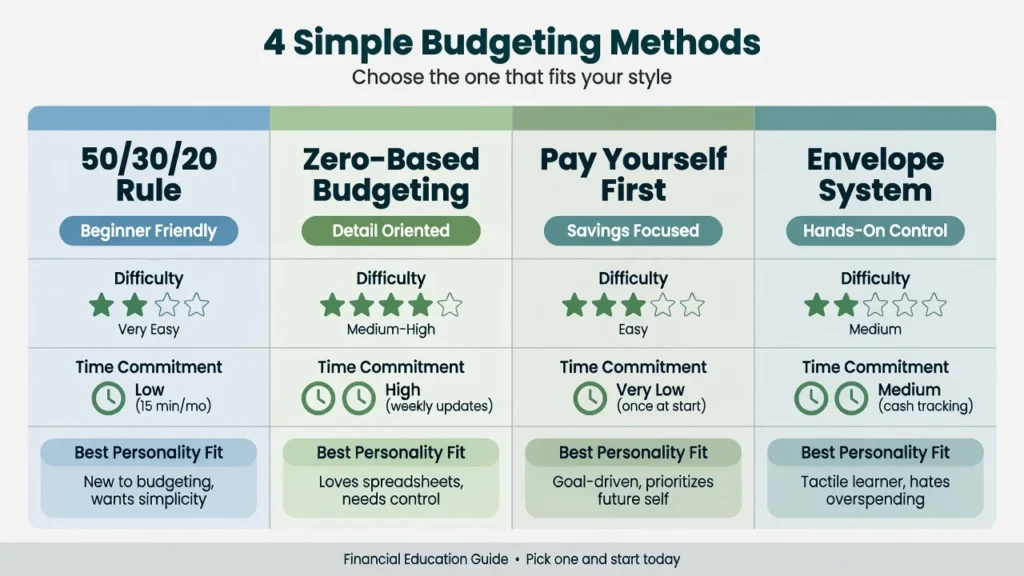

Step 4: Pick a Budgeting Method

There isn’t one “right” way to budget. Over the years I’ve done a lot of things and when my financial situation shifted, what worked in my twenties no longer works for me. The right choice will depend on your personality, your goals and what type of control you are looking for over the details.

There are four popular approaches to budgeting: 50/30/20 rule, zero-based budgeting, Pay Yourself First and the envelope system and I’ll go through each one so you can judge them fairly.

Step 5: Assign Every Dollar a Job

This is where a budget becomes a reality. With your income and expenses known, and method in place, the next step is to allocate your money, meaning you must designate each and every dollar for a specific purpose before the month begins. Any dollar that comes home to you must be claimed before you spend a single penny.

For this I have a simple budget worksheet. At the top I write my total income, then I begin subtracting. Rent, $1,200. Utilities, $150. Groceries, $400. Car payment, $250. Insurance, $100. I continue to work through each category until I have no more to assign. My money balance always decreases whenever I spend money. I continue until there’s no more money to be spent!

That includes savings – and that’s where most people fall short. Saving is not “what remains after you’ve used up everything else. It should be in your budget, like rent or food.

I put a set amount in the budget of my dollar bills every month and pay it just as if it were a bill that was due.

The Personal Budget Categories You Actually Need

I would use, like, five expense categories when I made my first budget. Rent, food, gas, bills, and all. That’s the last, ‘everything else,’ which every month I had to leave my budget there.

I’ve found over the years that the right budget categories sit somewhere in the middle specific enough to track your spending accurately, but simple enough that you’ll actually maintain them. These categories are among the key components of successful budgeting, so let’s break them down one at a time.

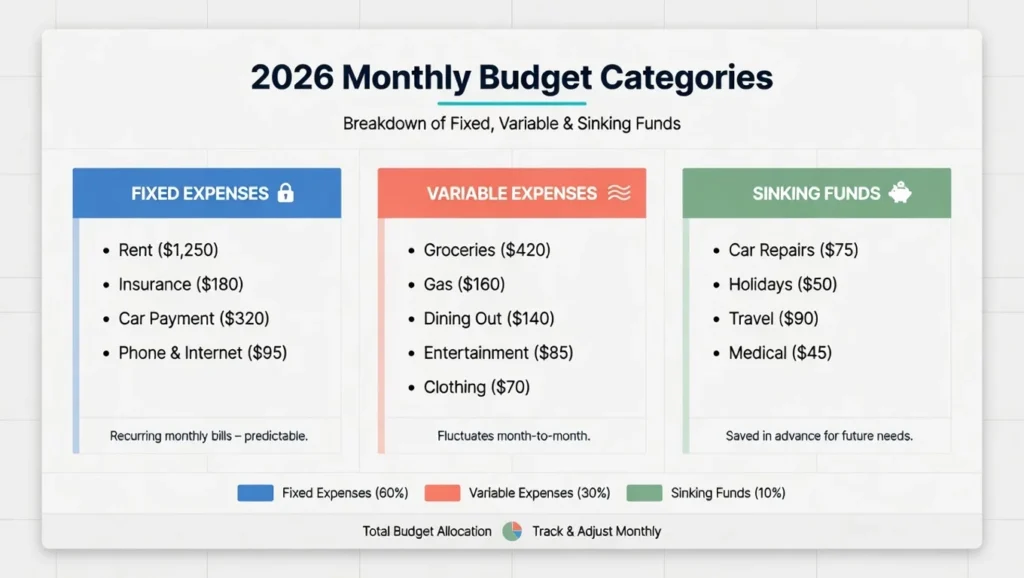

Fixed Expenses

These are the expenses that remain constant each and every month. They are predictable, there is no negotiation when it comes to them, and they always get paid first.

Fixed expense categories are things that I have to pay every month, like rent, car payment, car insurance, health insurance, phone bill, internet, recurring subscriptions – anything that I have to pay each month like a streaming service or software for work.

Variable Expenses

Variable expenses are the expenses that change by month. They are required, but to an extent they are also up to you; they may be the most flexible and the most risky component of your budget.

There is discretionary spending here, as well this is where I used to blow my budget every single month without even realizing it. If you find yourself consistently overspending on variable costs, learning specific strategies to reduce monthly expenses can help you gain control without feeling deprived.

Sinking Funds

A sinking fund is money that is saved on a monthly basis for an expense that does not occur on a monthly basis – a car repair, annual insurance premium, holiday expenses, travel or medical expenses.

It’s one of the items that everyone forgets to include in their budget categories list and that’s why so many budgets fail on schedule. Those were the costs that used to kill my plans off each time as I was simply not planning for it!

I also have travel savings, medical savings and home repair savings. I’m saving a fixed amount into a high-yield savings account that’s designated for each category, contributing a little each month. If the cost is involved, the funds are already right there, with no hassle, no credit card and no scramble. Financial wellness in practice is that.

Budgeting Methods Compared: Which One Actually Works for Your Personality?

Over the years, I have tried 4 different ways to budget, with varying degrees of success. What I kept finding myself running into is not the failure of the method, it was the failure of the method being adopted in my brain around money.

That’s the basic principle behind any comparison of honest budgeting methods – the ‘best’ method is the one that your brain will actually follow.

The 50/30/20 Rule

The 50/30/20 budget rule is a financial framework that divides your income into three large categories: needs, wants, and savings/debt repayment.

Fifty percent goes to needs, thirty percent goes to wants and twenty percent goes to savings and debt payment.

This rule worked for me when I was first starting out, as it was simple to understand and kept to a minimum of maintenance. If you are the type to despise counting each and every dollar, this is a straightforward plan which may be difficult to get wrong.

It does have its limits, however. In a time at a high price point, you may require 60% or 70% of your paycheck and the formula falls apart completely. For those who are aggressively trying to pay off their debt, this may be almost too low a number to dedicate to savings and debt payoff.

Zero-Based Budgeting

The approach I take now is zero based budgeting, and it’s really nothing like 50/30/20. In a zero-based budget, all of your money is allocated to a category before the month starts. You continue assigning until you have no money left after you’ve planned all of your spending and saving.

There’s one thing that I would like to add to the process of a Zero Based Budget that made it much easier for me to manage my cash flow, and that’s creating a buffer for the monthly process.

I would do a zero based budget, so that by the end of the month, my checking account would be almost empty, just one additional charge away from an overdraft. I still have a $500 – $1,000 buffer in the budget just for that. It changed everything.

Pay Yourself First

Pay Yourself First turns the budget process on its head. Instead of saving what you can after you’ve spent the rest, you save what you can first get money into savings and investments before spending the first dollar of discretionary funds. If that is the case, then you’ll base the rest of your budget on that amount.

A common rule of thumb among certified financial planners is to save and invest at least 10% of your income. If your income goes up, the goal is to increase this percentage to 20% or 25%.

But honestly, even if you can only manage 5%, that’s valuable progress the percentage doesn’t matter as much as building the habit. If meeting these targets feels impossible right now, there are specific strategies to save money even on a tight budget that can help you get started.

The Envelope System

The envelope system is the most practical budgeting system of all and can be surprisingly effective for people who aren’t able to stick to other budget systems but still find themselves overspending.

You create a cash envelope for each of your variable costs (groceries, gas, eating out, entertainment etc.). If there is no envelope, then no spending is allowed in that category for the month. It is hard to overspend, because of the physical restriction.

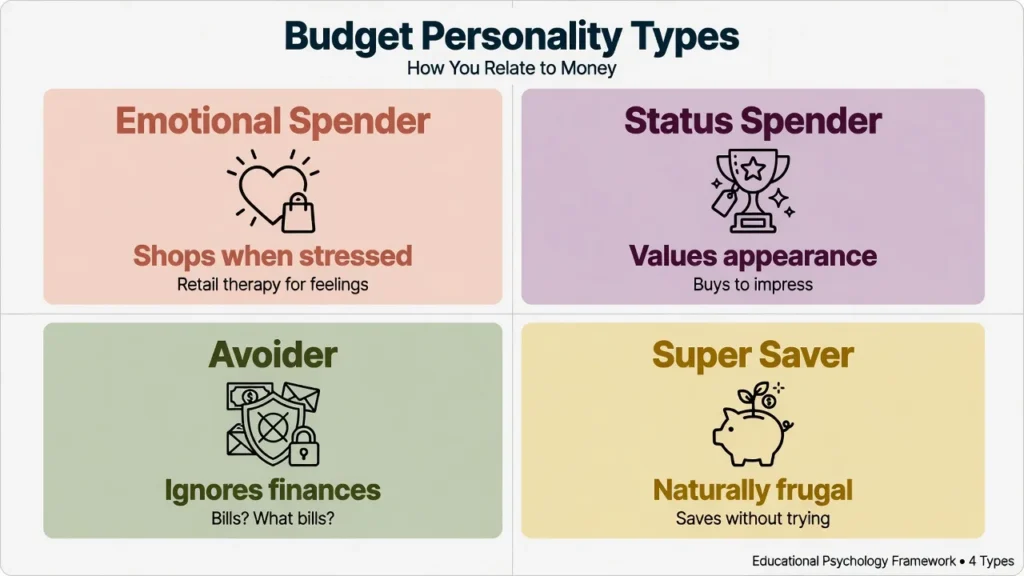

What Your Budget Personality Says About Which System Will Stick

I always felt I didn’t have financial discipline, that I was just one of those people who couldn’t stick to a budget. I tried everything, I came out strong in a couple of weeks, slipped, and I felt like a failure each time.

What I came to discover was that it wasn’t about my willpower. I was just continually trying to use techniques that didn’t work for me because I thought that way.

I stumbled upon it in personal finance research and it finally made sense to me why some strategies were working for me and others weren’t. The model divides budgeting up into four personality types: the emotional spender, the status spender, the avoider and the super saver.

The Emotional Spender

The emotional shopper shops when they feel stressed, bored, or have some painful emotions. These are habits you may not even be aware of, I’m not saying ‘I’m buying this because I am anxious’. You simply end up at the check-out and just don’t know why.

I’m not exempt of emotional spending, either, particularly when I get overwhelmed or burned out. If you are an emotional spender, then you will not benefit from strict budgets that leave no room for discretionary spending.

You must have built in rewards and a fun category that’s guilt-free: structure without punishment.

The Status Spender

The spender sees his self-worth in his possessions and his image. This type cares a lot about keeping up with a lifestyle, possessing the very latest or looking good financially sometimes more than it does about feeling financially secure.

Status spenders tend to rebel against budgeting, because rather than acknowledging that their image and income don’t match, they’d prefer to see no difference. This is where the envelope system and zero-based budgeting, in which every dollar is on display, can work well once the initial reluctance is overcome.

The Avoider

The avoider doesn’t want to know what’s in their bank account. When they’re checking, it’s stressful, so they don’t. There’s no money because it’s so overwhelming to open the bills.

If you are this type of person, you don’t need to make many decisions each day that would otherwise lead you to avoid a savings approach that is so simple: Pay Yourself First! Do everything you can to automate and to make as few decisions as possible.

The Super Saver

The super saver is a natural frugal and disciplined person they don’t have to say no to spending, and they really feel good about saving. Super savers can go overboard with budgeting, though. Self-deprivation is followed by some burn out.

Others save and save and never indulge themselves in enjoying what they have saved. If you’re this kind of person, there’s no such thing as a ‘fun money’ budget category: it’s a sign of sustainability.

The Savings and Emergency Fund Rules Every Budget Needs

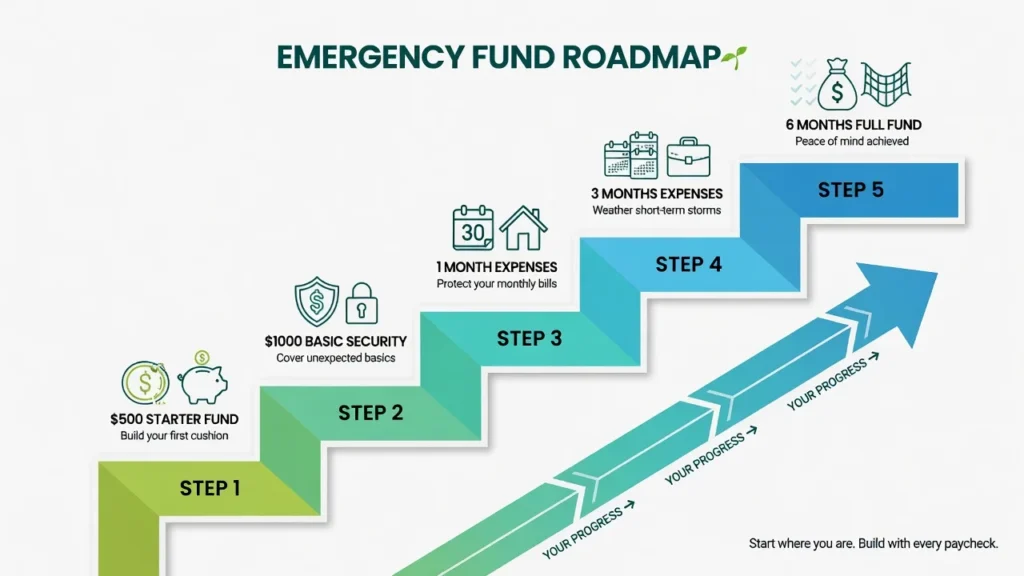

Why You Need an Emergency Fund?

An emergency fund is a fund where you save specifically for emergencies, like a job loss, medical expenses, emergencies involving your car, or emergency trips for a family crisis.

This isn’t a vacation account or a holiday shopping account. It is simply for the occasions when you would certainly have a complete catastrophe if you didn’t have cash on hand to help you manage it.

Consumer Financial Protection Bureau (CFPB) recommends setting aside 3 to 6 months of living costs. CFPB study finds that homes with just one month of expenses saved are much less likely to miss a bill payment if they suffer a financial disruption; even starting small is important when it’s hard to imagine doing so for the whole goal.

This is a daunting prospect if you’re starting up from scratch, I know because I did. The only time I worked out just the essentials of what I would need to survive for three months not for my whole life, just for three months I calculated my number at $6,200. That all at once, sounded like $100 a month was a realistic amount.

I save my emergency fund in a high yield savings account that is not used for my regular bank checking account. It is available when I really need it, but I’m not tempted to use it for anything that I don’t need.

Save vs. Pay Off Debt: What to Do First

One of the most frequently asked questions from newbies on debt management is, ‘Should I save first or pay off my debt first?

One of the most common beginner questions on debt management is whether to save first or pay off my debt first? I found myself in the same situation I paid a significant amount of credit card debt and had student loans, and I really was torn between paying off debt and making any additional savings.

This is the structure that I ultimately landed on, similar to what many CFE’s suggest – start with a small emergency fund of $500-$1,000 first. Then focus on paying off high-interest debt aggressively anything with a rate higher than 15-20% APR should be treated as a financial emergency. If you’re not sure whether your credit card debt levels require immediate attention, understanding the warning signs can help you prioritize correctly.

When high interest debt is eliminated, start putting money into your three to six month emergency savings and transition into long-term savings and investing.

One final word of caution: If you’re in the midst of a payday loan or predatory loan with an APR over 36 percent, the CFPB has resources to help you recognize and rectify predatory lending situations.

The Budgeting Tools That Actually Help (And When to Skip Them)

Over the years, I’ve used a lot of tools over the years to budget apps, spreadsheets, printable worksheets, pen and paper. Some made the whole thing a lot easier. Some made it so complicated, I wanted to give up budgeting altogether.

These are some of the things that really work.

Budget Spreadsheets

I began with a free budget template that was created in Google Sheets – no frills, just simple columns, categories and auto sum formulas. I had liked the fact that I could customise it totally. It was free, it was in the cloud so that from my phone I can access it, and I had complete control of every number.

A budget spreadsheet is a no-brainer for you if you are a nitty-gritty type who enjoys having it all in one spot.

Budgeting Apps

Where people need automation, they are better suited to apps. I was forced to find a new budget tracker as Mint died in 2024. It’s at this point that I tried YNAB (You Need A Budget) and it did change my perspective about managing my money.

The whole concept behind YNAB is a zero-based budget. Each dollar you deposit will have a task when it arrives in your account. Not free, but if you have people who have difficulties with manual tracking, then the automation is worthwhile.

Pen and Paper

I also know some people who swear by pen and paper. Uses a physical budget planner or a simple notebook and hand writes all items. It’s an old fashioned thing, but for some, numbers are more real when written on paper than when on a computer screen.

If apps and spreadsheets are too much hassle, just don’t do them. The most effective budgeting tool is the one you will use!

How to Keep Your Budget Alive After the First Month

Creating a budget is the easy part. It’s at the maintenance stage where most people lose it. People who have a budget are different from people who benefit from a budget because they are able to maintain it and track it. It’s important to have a plan.

Real financial change comes when you check in, make changes, and remain connected to your finances.

The Weekly, Monthly, and Quarterly Budget Review System

I check in with my budget weekly, it takes about 10 minutes. I review my budget and compare how much I’ve spent vs. how much I planned.

This is the heart of my budget tracking practice and stops issues getting out of hand. Am I ahead? Great. Did I miss my dinner bill so much that I’m running out of money by Tuesday? Not on the 30th, I need to know now.

Every month I perform a full review, which takes me about 30-45 minutes. I compare my intended spending to what I spend and see if there are patterns I need to alter my budget for.

Am I spending too much in the same category each of the past three months? It is NOT a discipline issue, it is a sign that the budget number is a non-reality number. I’m not changing my self esteem, I’m changing the number.

Every quarter, I revisit my bigger financial goals. Am I on track to save my goal? Has my pay increased or decreased? Has a new cost appeared that requires a new category? The quarterly review is where I make adjustments to the entire plan, which is not where I make the day to day plans.

The One Trick That Prevents Budget Deserts and Overdraft Fees

I was first in a budget desert a cash flow management problem was not my fault because of the low income. I had the funds available for the month but the timing was way off. It led to me always having to pay attention to stress, and sometimes even overdrafting, although I could actually afford my bills.

Once I figured out what was causing the problem, it was easy to resolve: align the dates of my bills with my paychecks. Created a calendar listing all bills and their due dates.

I also moved the due dates, most lenders and utilities will allow you to adjust your due date by a week or two with a call; it made my due dates more spread out throughout my pay period. The budget desert was gone in a flash.

If You Overspent Last Month, Read This

Last month I spent more money than I had. And a month ago. Most months if I’m being honest. Overspending doesn’t indicate that you don’t know how to spend money or budgeting is ineffective. It’s what makes you human. There is no such thing as success with a budget, it’s about what happens after you fail.

I’m not seeing failure anymore, I’m seeing data. It was a change in spending awareness that made all the difference. If I spent $100 too much on food, that’s good information — perhaps my grocery budget is too low or perhaps I’m wasting food, or perhaps I’m going to the grocery store hungry.

Anyways, the excessive spending is telling me that I need to hear what I need to hear. Financial responsibility is not a matter of never falling into the same mistake; it’s about what you construct after every mistake.

The recovery plan is easy. Identify which category went over first. Secondly, if that is a problem, try to determine the cause, was it one time or recurring or regular? Third, determine: Am I changing the budget category or am I changing the behaviour? Both answers are correct. Fourth, move on. Don’t have regrets for months from month to month. New month = New plan.

The Budgeting Mistakes That Quietly Kill Your Progress

In all of my years of experience I’ve made almost any budgeting mistake you can think of, and also picked up the tips to fix any budgeting mistake.

There were some clear errors which were rectified promptly. Others were more clever and slowly siphoned away my momentum for years until I realized what was going on.

Mistake 1: Ignoring the Silent Busters

The little things that cost you a few dollars, but if you add them up, they’re hundreds of dollars a year – I call them the silent busters. Services you forgot you had, app subscriptions that renew, memberships that you don’t use.

These are among the least expensive places to cut expenses with no change to the way you do things. Review each monthly fee on your bank statements each quarter. Remove any that have not been used in 60 days.

Mistake 2: Forgetting Irregular Expenses

There are expenses that occur periodically – car registration, insurance premiums every six months, holiday spending, back to school shopping – these things happen on a regular basis, but most people consider them a surprise every time they come up.

The solution: sink costs, as explained above. If you do know that the registration fee for a car is $600 and it is due each October, you would have $50 per month to save. The ‘surprise’ is no surprise at all.

Mistake 3: Budgeting to Zero Without a Buffer

My initial experience with zero-based budgeting involved taking it too seriously, and at the end of the month I found myself with virtually no money in my checking account. If I got charged for something I didn’t expect, I would be in debit.

The solution is to create a $500-$1,000 buffer, and label it as a fixed budget item such as ‘buffer’ or ‘float’. It is not spent in your checking account. It’s not an emergency fund. It’s a buffer that can prevent financial emergencies from occurring.

Mistake 4: Setting Unrealistic Category Limits

You’re spending $600 per month for groceries and you decide to cut it down to $300 per month; you’ll fail. The number is not connected to reality, not because you’re not disciplined. Use your actual expenditures averages.

Make the budget based on your real life. As soon as the habit is established, you can begin to cut categories on purpose, but not by half, or more, all at once 10-15% at a time.

Mistake 5: Quitting After One Bad Month

This is the largest of them. Budgeting is not a “no no” if you overspend one month. It means that you received a month. I’ve been working on a budget for years and still have months when I blow it. I don’t give up anymore I evaluate, modify and restart.

People who are successful at budgeting over the long haul are not those who never fail. They’re the ones who return.

All of these are easy to correct and most of them require only one decision and one phone call. The problem is, you can’t fix anything if you’re not aware of it. This is why all commentators on budgeting are more important than spending awareness. When you start to see your patterns clearly, then you can go about adjusting without drama. You’ll still have bad months.

However, the bad months become shorter, the recoveries become quicker, and the wins begin to count.

Frequently Asked Questions About Budgeting

Here are the top questions I receive from those who are starting to learn the basics of budget 101. I’ve responded to them all honestly as I have experienced myself and what I have learned from years of trial and error.

If you’re making a budget for the first time, what should you do first?

Before constructing, keep track of your spending for a month. I know it’s not the thrilling answer, but it’s the correct answer. The number one reason first budgets fail is you are trying to budget without knowing what your money is going on. Write it all down for 30 days, and then sit down with the numbers and create your budget from actuals, not guesses. That’s the essence of budget 101.

So what is the difference between zero based budgeting and the 50/30/20 rule?

These are two completely opposing methods, and I’ve experienced both. The 30/30/30 rule is a very simple strategy that divides investment income into three broad categories and needs very little day-to-day management and oversight this is great for those who want something simple. Zero-based budgeting is all about giving every dollar a purpose good for those who want to be specific about what their money is doing and are ready to stick to a strict budget. The best one for you will depend on your personality and your level of watching your money.

A: Budgeting on a variable income isn’t too difficult, provided you know where to start?

I experienced this in my “freelancing days” and it was initially really hard to budget. What I eventually learned is to budget based on my lowest typical monthly income not my average, and definitely not my best month. Build your budget around that conservative number, making sure it covers essentials, minimum debt payments, and at least some savings. If income fluctuation is a constant challenge for you, the strategies for how to budget on a low income can help you build stability even when earnings aren’t consistent. In good times, everything above is put into savings, debt repayment, or your sinking funds. Plan on the bottom and adjust to the top.

Q: Using a spreadsheet or budgeting app?

I have tried both spreadsheets, apps, even a simple budget calculator — and the truth is, it’s whatever the best tool is depending on the person, and their behavior, not their plans. If you love numbers and customization, then a spreadsheet will provide you with total control. If you don’t like manual input and want to keep things consistent, an app such as YNAB takes away the friction. Use it for 60 days, free of charge. Switch if it is not working. The tool is simply the container, the habits are what are poured inside.

A: The results of budgeting can be noticed after a few days?

The first 2-3 weeks is when you will notice a change in awareness – the data you are keeping is showing you patterns you were not aware of. Consistent budgeting will usually show signs of financial progress in 2-3 months, such as debt reduction, increased savings and reduced stress. The first month is never going to be perfect. This is an expected and normal reaction. Do it for the first month and beyond, and it works for you and not against you. True to the name of budget 101, the point is not to get results overnight, but rather, a steady stream of results.