budgeting process steps: 8 steps to help with personal finances or business budgeting

Most people think that the budgeting process steps are only for accountants or CFOs. I did, until I took control of my own finances, and discovered that I didn’t know where my money was going. It was the watershed moment.

I used to have to do it for personal budgets first when I was working freelance, and then when I starting to work as a consultant with project teams and small businesses because I needed to manage budgets. The information I am sharing is not theory. This is the system I use.

Budgeting is the sequence of actions you have to take in order to plan your expenditure before the money actually goes out of your account. It is like a financial roadmap a roadmap that lets you know where you are heading rather than where you have already arrived.

For a long time, I treated budgeting like a punishment. Every time I sat down to look at my finances, I felt guilty before I even opened the spreadsheet. What I didn’t understand yet was that a budget doesn’t tell you what you can’t have. It tells you exactly what you can because you planned for it.

I was making budgets a chore for a long time. I would feel guilty before opening the financial spreadsheet every time I sat down to review my finances. I hadn’t realised, however, that a budget doesn’t actually tell you what you can’t have. It informs you what you can, since you planned for it. Budgeting involves establishing goals, recording income and expenses, organizing expenses, forecast, allocating resources and obtaining consensus from those affected, communication, and then tracking actual results. The key steps are the same whether you are on top of your personal income budget or you are on top of your company’s multi-million dollar budget.

Imagine that each dollar has an employment contract. If it doesn’t have one, it floats. If they have a clear budget, then each dollar will know where to go.

The goal of a budget is not to restrict, it’s to give you freedom

I didn’t read a book, or take a course, to get me started in budgeting. One month in which I tracked every single thing I was spending and realised how much I was spending on items I wasn’t really interested in.

A budget helps to minimize stress it’s not just a fact. The American Psychological Association (APA) has found over the years that money is the leading cause of stress among adults. One of the most straightforward approaches to that is to have a plan. Prior to understanding the budgeting process, I would be lying awake at night asking myself whether or not I have enough money to pay my bills, if I am making progress towards my financial goals or if that unpaid car repair will completely empty my bank account. Now I’m where I’m supposed to be, since I planned it out ahead of time.

The true goal of a budget is to match up your spending to what is important to you. If you are looking to travel, then you need a travel line in your budget. When you’re working to get out of debt, all your money should go toward that debt as long as you’re able to pay your bills.

There’s also the less obvious side benefit I didn’t notice for awhile, which is that I no longer engage in mental arithmetic when I want to purchase something. There was always that feeling in the back of my head about if I should be saving this or if I can afford to do that, and with the plan it was gone. Those decisions were made for me in the budget.

The true benefits of budgeting are clarity and control. Making a budget makes you feel wealthier, not necessarily more wealthy, but you know what you have and you know where it’s all going.

Who is involved in budgeting? (Hint: Everyone)

Whether you’re someone fresh to financial planning and budgeting or not, you should understand this process. It doesn’t matter if you make $30,000 a year or $300,000. The principles are applicable at all levels of income because they are focused on planning resources to go towards priorities.

Company budget planning is an essential skill that small business owners must master. This is where I have found myself when I began freelancing and I found that not being paid the same paycheck each week demands more attention to budgets than a regular income. You must be aware of your business costs, anticipate your earnings and prepare for the down months.

In bigger companies, project managers use accounting budgeting to prioritize resources among projects, to monitor spending against budget forecasts and to report to management on project progress. These steps are essential to know if you’re in charge of delivering a project on time and within budget.

In a nutshell: When money enters or goes out of your life or when you are involved in some way in your work, budgeting is relevant to you. This is a reference to nearly all of us who are reading this very moment.

Understand the purpose of Budgets (The Real Benefits)

I would make budgets for years, and disregard them until I got to the end of the month and would open my bank account, and ask myself, where did all my money go? That’s not budgeting. That’s only the best of luck with a spreadsheet.

People often say that everyone is in the game for the same reasons. It is said that you are in the game for the same reason as everyone else.

Strategic Benefits: Aligning Resources with Goals

But it was when I began to see my budget as a planning tool instead of a record of expenses that I got it. I no longer made financial decisions that were arbitrary they made sense to me where I wanted to go.

A budget-less strategic plan is a wish list. The cash is the actualization of the plan.

Operational Benefits: Coordination and Control

Budgets establish accountability and that’s one benefit of the budget that wasn’t widely acknowledged.

If the budgeting process involves everyone in the organization, everyone will not only be aware of the amount they can spend but also the rationale behind the budget constraints. I have seen teams which were having trouble finding the money to do what they wanted, but then became much more creative and efficient as soon as they grasped the big picture.

Budget controls provide a benchmark for looking at performance. If I have $500 for food and I always have to spend $700, then there is an important message there for me. I must have got it wrong or have to change my ways. Either way, I know what I’m in for instead of having a feeling of guilt each time I log in.

Personal Benefits: Stress reduction and confidence

I used to be gripping a financial anxiety, before I began a proper budgeting process. I didn’t know if I was spending too much, if I was improving, and I didn’t have the confidence that I could deal with anything I didn’t expect. Each time I had to pay for a repair, doctor’s note or any random thing, it was like an emergency that we were not ready for.

It’s a confidence that carries over to larger decisions as well. I did not have to agonize about the opportunity to take a professional development course when it arose. I glanced at my budget, at the amount I had, and I made my decision in about two minutes. What a good budget does, is it is able to answer the questions you would spend hours worrying about if you didn’t have a budget.

Budget Preparation Process: What to Do Before You Start:

I would sit down and open a spreadsheet and would attempt to create a budget from scratch for a long, long time. No history, no benchmarks, no system, just me trying to guess numbers and why the budget wasn’t able to last more than two weeks.

Know your scope and objectives before you start

This is a lesson that I learned in a home remodel.

If there is no scope then each new idea and unforeseen expense is added on at the end. My budget for renovating began with the idea that I wouldn’t be doing anything but the kitchen. It expanded to the adjacent hall way’s middle and then the bathroom because the contractor was already in the house. I had no budget left until I used half of it.

If you’re working in an organization, you need to secure this scope before beginning to create detailed budgets. I’ve witnessed teams spending weeks developing detailed budgets only to discover that leadership had a very different idea of what should be included.

The first thing I do when I begin the budgeting process is to write the answers to three questions: What am I budgeting for? What time period is this from? What would success be if it happened? Here are some simple questions that most first budgets miss and the reason that most first budgets fail.

Collect Your Historical Data

This was the moment that made me realize to quit playing guess and guess and get to work with real numbers.

It was the first time I did it that I was really shocked. I was assuming that I was spending around $50 for lunches and coffee each month. The actual number was over $200. If I didn’t have the data then, I would have spent $50 and then, come up short after the first week and feel like a failure.

This is done by taking your profit and loss statements, bank records, and expense reports from the past 12 months for business budgets. When it comes to personal budgets, it’s a process of checking your bank and credit card statements item by item.

If you don’t know your spending history, due to lack of data? Start now. Record everything for the next month before you create your budget! One month of real data is infinitely more valuable than made-up numbers.

Create Templates and Systems

Previously I would create all of my budgets from scratch, so I would make the same mistakes on each one. Templates fixed that.

A great template is not only time-saving, but it’s also valuable. It provides consistency which makes it much easier to compare budgets from month to month and department to department. Personal monthly budget, project budget and business annual budget are separate templates. They all have the categories that I use and the formulas that I always need and the variance columns that make it easy to track.

In the business world, the FP&A process typically employs more complex software but the concept remains the same. Set up your system before you need it.

How long is the budgeting process?

If you have all your financial information available, then it could take a couple hours to create your first personal budget. But mastering it? This will take approximately 90 days. It will be a rocky first month, forgetting things, underestimating categories, feeling like you’re doing it wrong. Most people have a monthly budget by the end of the third month that truly represents their monthly spending. Make it through that learning curve.

If your initial budget isn’t ideal, do not give up. The budget cycle is never-ending I have been doing this for a number of years and even today I am still adjusting my approach as my life evolves.

The time frame for organizational budgets is much longer. For midsize companies I’ve seen take anywhere from 2 to 3 months to complete each year, with each department taking some time to build the budget, roll it up into the master budget, negotiate when there is a need for budget cuts and revisions, and then finally get it approved at the end.

For larger organizations or government, budget preparation may begin six months or more before the start of the fiscal year.

I make this time a part of my calendar now. I begin preparing for budget in October at the latest if I have to have it approved on January 1st. Haste results in hasty assumptions and budgets based on false assumptions simply don’t last long in the real world.

The 8 steps of the budgeting process explained

After years of experimenting with various plans, the following eight steps are a foolproof budgeting sequence, no matter the scale of the project, from $1500 monthly to a $10 million project.

I’ll take you through each step of the budget process as I do it, showing you why each step is important, and what issues arise if you don’t do it.

The first step is to establish your financial objectives and connect them with your strategy

First, you set your financial goals and link them with your strategy. All of my budgeting processes begin at the same point – I list what I want to achieve before I do a single number.

In personal budgets, I list out my financial goals for the time frame I’m budgeting for. These can range from paying off a debt to building up a three-month emergency savings account, paying for a down payment or just making it to the end of the month without having to pay a late fee. Goals are tied to the strategic plan, whether they be about revenue or expansion goals, cost reduction or market share objectives, for business budgets.

If you don’t have financial goals, your budget is no more than accounting. Goals turn into strategic planning.

The alignment between what you are aiming to accomplish and where you’re really putting your money is the difference between a true financial plan and a spreadsheet of guesses.

Step 2: Monitor and Figure Out Ways to Increase Your Money Making Streams

You must calculate your income and make sure you know exactly how many dollars you are going to have before you spend a single dollar.

In the case of personal budgets, it includes all sources of income, such as salary or wages from the main job, freelance or side income, rental income, income from investments, income from government benefits, and any other regular income that is in the form of cash.

A golden rule I have is that I am conservative with my income estimates. Only include money for which I have reasonable expectations of getting. My side hustle made me $500 last month, but it’s a bit capricious so I plan on $300. If more comes in, that’s good. Otherwise, I’m not short.

The one thing I see all the time is the people counting the credit cards as income. Credit cards are a loan that must be repaid, typically with interest. Incomes – Debt you haven’t paid yet.

Predicting revenue is more complicated for business budgeting. I consider several revenue streams, look at past trends, take into account the market and competitive dynamics, and then make reasonable forecasts based on those.

Step 3 is the most important, as it involves determining and organizing your expenses

When I see what’s coming in, I plan what is going out.

First of all, for a month I keep a record of all my expenses. And I’m talking about it all. All that $3 coffee, $15 subscription that I forgot about, $200 grocery shopping all that and more. It is easy to see how little things that you do not foresee can add up quickly, and no one can anticipate spending that doesn’t occur.

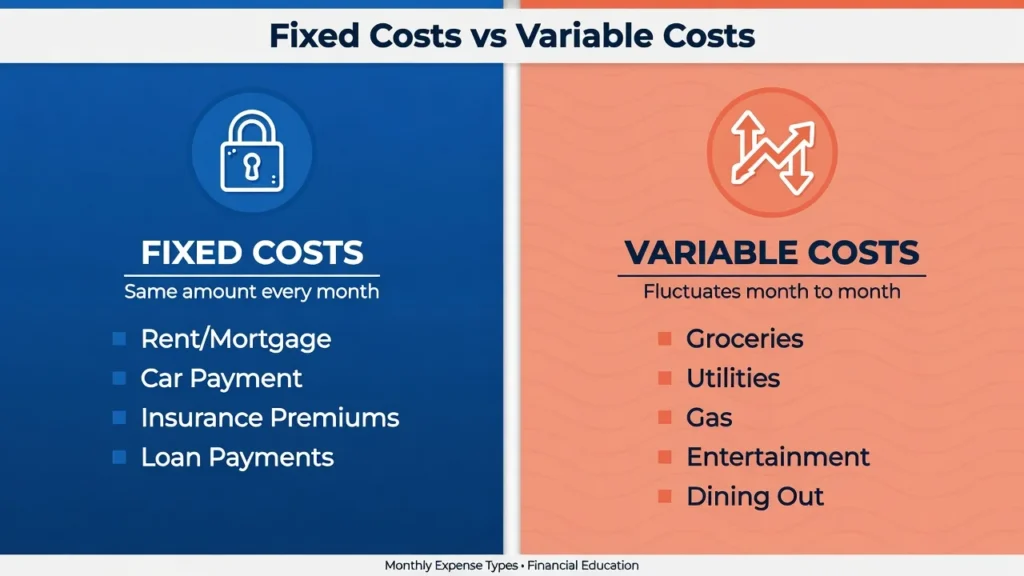

My fixed cost is different from my variable one. These costs remain constant from month to month: rent or mortgage, loan payments, insurance premiums, car payment. Variable costs change – food, electricity, gas, movies, clothes.

In those two categories, I distinguish between needs and wants. This is a very big deal if you have a budget you can’t cover.

Expense categorization for business budgets becomes more complicated. You’re distinguishing between operating expenses and overheads, between direct costs and indirect costs, and between capital expenditure and operating expenditure.

Step 4: Collect Data and Make Projections

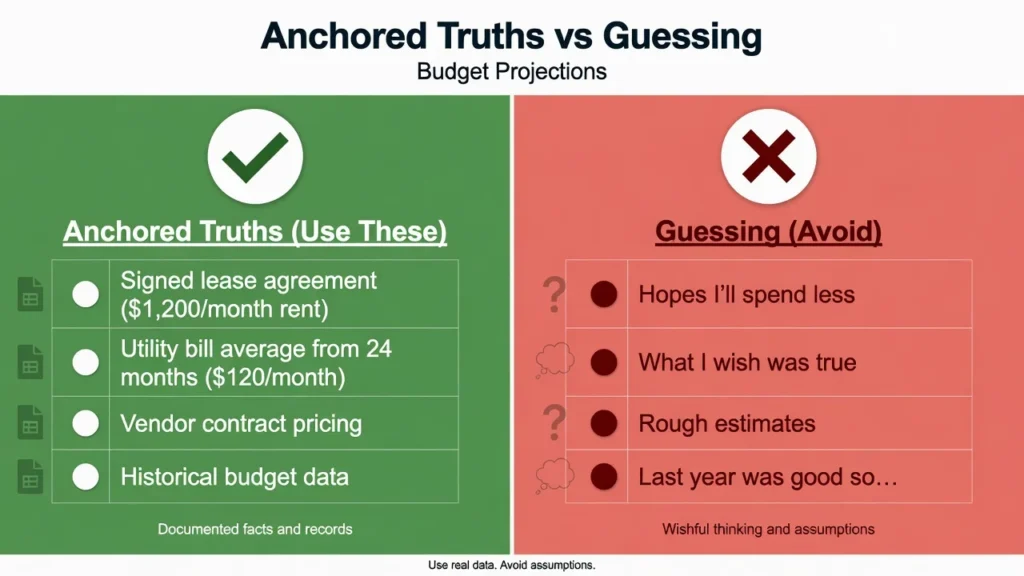

A budget is not only a statement of the present. It’s a guess for what is going to happen. This is the most crucial and the most simple step that makes it the most humble.

I don’t guess anymore, I now make projections based upon anchored truths (pieces of info that are solid and verified). An anchored truth could be a signed lease contract that lists precisely the amount of my rent over the next year. It could be an average of the last 24-months of total utility bills.

Even the things that seem obvious I always write down as assumptions on my budget. If I’m estimating, I might use a 3% inflation on most of my costs, or I might be estimating a 10% revenue gain because of a new product introduction. Once I write down these assumptions, I can come back at a later time and explain why my actual results did not match my expectations, and so on.

For businesses, it includes a wide variety of different departments providing input, performing scenario analysis for both best and worst case scenarios, reviewing contract terms with vendors, and incorporating any changes in regulatory requirements that may impact cost or revenue. If there are any past budgets, I also use those— even simple budget analysis such as comparing what was forecasted and what actually happened is enough to show the trends that you wouldn’t notice otherwise.

Step 5: Assign Resources and establish the Budget Document

This is where the plan comes to fruition. You’ve found your income, outlined your spending, and calculated your projections. Now you allocate.

I have a technique called zero-based budgeting, which is my income should be equal to my expenses. Each dollar is assigned a particular task. If I bring home $4,000, I divide up all $4,000 amongst the expense items, the savings objectives and the debt obligations. Nothing is left unassigned. (I discuss zero-based budgeting in greater detail in the methods section below.)

Resource allocation is the process of putting your strategy into action. For companies, it’s about which departments, projects, and initiatives get money and how much. All decisions on allocations are strategic decisions.

This is also where you start to develop your master budget, which is the overview of all the departmental budgets, revenue forecasts and capital outlay plans in one place.

Step 6: Review, Negotiate and Obtain Approval

I was once lazy in including this in my personal budget. Even if it’s only a formality for yourself, a review will help you catch your mistakes when you’re in a hurry.

This is a critical step in the organizational budget process and is frequently debated. One thing I see in my consulting work with businesses from startup to mid-sized businesses is the lack of negotiation.

Every time the total of all the departmental budget requests is more than what is available. Every. Single. Time. It’s not a coincidence: that’s the nature of organizational budgeting. All department heads feel that their priorities are more important than others, and they are correct from their own perspective. The budget review process is a way for leadership to balance those competing priorities with available resources.

Don’t rush approval. Unapproved budget is a wish list.

Part 7: Share the Budget with Stakeholders

If a budget is not communicated, it’s not a budget. It’s a document.

When it comes to personal budgets, communication could include having a sit-down with your spouse or partner to go over the numbers together. For the organization’s budget, it involves briefing department heads, informing team leaders of specific parts, and making sure that all those who have the authority to make spending decisions know what they have at their disposal.

I also explain why, as well as what, is being done in terms of budget decisions. If they see that we are cutting back on something in order to more strongly support something else, they’ll be more willing to approve the budget even if it means less funding for their favorite projects.

It is the budget controls that ensure that outlays stay within the plan, and it is only when people who spend the money know what the plan says that the controls work!

Step 8: Monitor, Track and Adjust during the period

A financial plan without a financial plan isn’t a financial plan. Much of the work is done in the continuous monitoring and adjustments.

I review my own budget on a weekly basis, it takes about 10 minutes. I check what I am spending against what I have planned, tag items that are going over their planned budget and make changes before it becomes a large issue.

I’m looking for budgeted variance, which is comparing my budget to what actually happened. If that is positive, I made a profit. If it is negative, I spent more than I had saved. Not all the differences need to be addressed concentrate on material differences.

Monthly monitoring is the norm for organisational budgets. Departmental heads compare their actuals to their budgets and discuss any major differences from the budget with them; any changes in the forecast that could impact the remainder of the period are noted.

It’s not the end of the budgeting process when you make the budget. Monitoring and adjusting is the action phase where you do what you’ve planned and find out what is working.

The most effective methods for budgeting, and when to use them

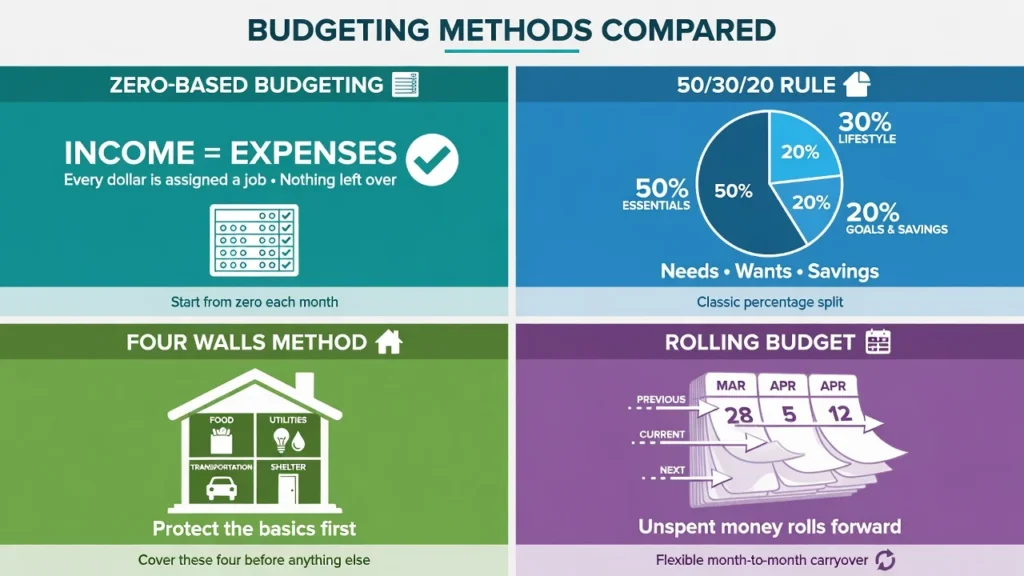

The one thing that got my budget to work was zero based budgeting

Zero based budgeting means that you begin each month from scratch. You don’t roll over the previous year’s numbers, you explain each expense. All spending has to be justified.

More work is required in the beginning. But it takes away the creep that accompanies an annual budget numbers that aren’t really examined; the things that always existed and everyone assumed were what they were.

I highly recommend using zero-based budgeting if you are new to budgeting, Deep in debt or have the “Where is my money going” question. It’s the discipline that makes it work.

The 50/30/20 Rule on Simple Budget Allocation

The 50/30/20 rule was made famous by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in the book, ‘All Your Worth. It’s one of the easiest budgeting plans out there and here’s why.

This approach recommends that you save half of your income for needs housing, groceries, utilities, insurance, and minimum debt repayments. You allocate 30% on wants and lifestyle decisions such as going to the movies, hobbies, entertainment and subscriptions. The remaining 20% is allocated to financial goals: Personal savings, investments, and additional debt payments over and above the minimum payment.

Note: Percentages are guidelines and not rules. These are the actual numbers you can expect to get depending on your cost of living, income and goals. It is okay if it takes someone in a high cost city 60% for their essentials. The framework is a suggestion, not a rule.

Four Walls Priority Framework

The Four Walls method is easy and effective, especially for those facing financial difficulties and beginners.

The Four Walls are food, utilities, shelter, and transportation. These are the essentials to stay alive. In every budget, you spend these four types of expenditures before you spend on any other.

Once the Four Walls are accounted for, anything else is paid for from a pool of “other” money (debt payments, savings, entertainment, etc., and subscriptions).

As far as housing goes, it’s best to keep your mortgage or rent payments at 25% or less of your take-home pay. I’ve witnessed people who find themselves in a lot of financial mess only because they are paying 40-50% of their earnings for their housing and have almost nothing to allocate to other things.

Rolling Budget for Dynamic Businesses.

As a business consultant I presented this concept of the rolling budget approach to my clients, and for companies in a rapidly changing environment, it helped them to plan differently.

A rolling budget (also known as a rolling forecast) extends the budget period as it goes on. A rolling budget always looks 12 months ahead, rather than a static annual budget which becomes less relevant by Q3. You take the month off the end of the budget at the end of every month, and add a new month on the beginning of the budget.

It demands more sustained effort, but is much more reliable and effective in generating a more accurate and informative financial picture for enterprises in dynamic industries.

The Difference between 4 Steps and 8 Steps of the Budgeting Process.

Perhaps you have read about budgeting before, and you’ve heard about the 4 steps to budgeting. You may ask yourself, how does this apply to the 8 Step Model I’ve outlined here?

The actual fact is, they’re talking about the same process, but on different details.

The four-step version is usually a simplified version of the above steps, covering prepare, approve, implement, and review. The four steps outlined correspond directly to the eight steps. Preparation involves Steps 1-4. Approval is Step 6. Implementation is done in steps 5 and 7. Review is Step 8.

Match the structure with the complexity of the work. Simple situations, simple systems. More detailed organizations are needed for complex organizations.

The differences between business budgeting and personal budgeting

The core budgeting process steps are the same whether you’re budgeting for your household or a corporation. However, the size, complexity and political nature of organizational budgeting are something else.

At the bottom line is that the Bottom-Up Budgeting Approach wasn’t successful.

In mid-sized and large organizations, the bottom-up budgeting approach is the most widely used budgeting approach. Each departmental budget is created from scratch, depending on the goals the department has in mind to achieve. These individual departmental budgets are then consolidated into the company’s budget.

You can only do bottom-up budgeting when you understand what the priority is for the company before you start putting in your numbers, otherwise you will be spending weeks negotiating what you could have agreed to in one meeting!

What is the difference between Operating Costs, Overhead Costs and Capital Budget?

There are many different ways to categorize expenses in business budgeting. It is important to comprehend these differences. Operating costs are the actual costs that are running the business day to day – costs directly related to your product/service.

Consider raw materials, direct materials and production costs. Overhead costs are indirect costs of maintaining the business, which would not be incurred if the business was not in operation. Overhead is any expense that is incurred by operating a business.

Overhead includes any expense that is covered when running a business, such as rent, utilities, administrative salaries, insurance, etc.

Capital budget is fully distinct. It includes large purchases of assets that can be utilized over a number of years, such as equipment, vehicles, and real estate. Most capital expenditures are ddeductible over a period of years, not in the year of purchase.

Understanding the role of FP&A, and that of the CFO

Larger companies have the Financial Planning and Analysis (FP&A) function that take ownership of and manage the budgeting process. FP&A teams are charged with developing financial models, consolidating departmental budgets, conducting scenario analysis, and making recommendations to senior leadership.

It’s the CFO or Chief Financial Officer who is accountable for the budget in most businesses. They are answerable to the board and the executive team on how the company can have a sound financial plan. As a consultant, the ones who I work with who have been the best are the ones that use the budget as a communication document, a shared understanding of the company’s priorities in financial terms.

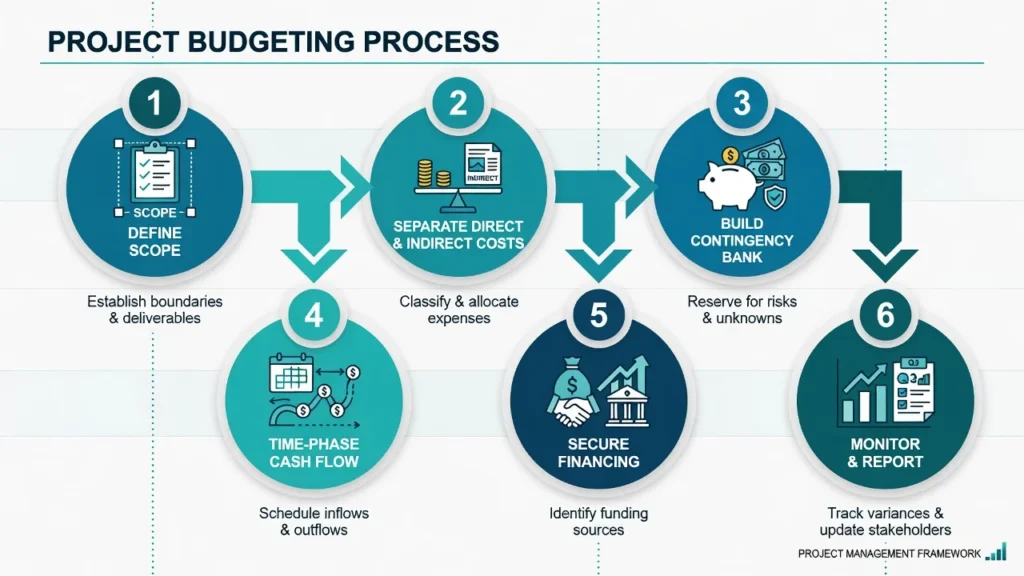

Project Budgeting: 6 Critical Steps for Success

Often, the success of a construction project depends on its budget.When it comes to construction projects, budget is a key part of success.

Project budgeting is essentially the application of steps of the budgeting process and is unique in that it poses some challenges not encountered in personal and operational budgeting.

The 1 step is to determine Scope before you budget anything

The biggest spill that I have seen (an error I’ve taken myself for more than once) in project budgeting is when you begin to estimate costs without first having a clear idea of what you are building.

The budget buster you never hear about is Scope Creep! If the scope is not clearly defined and approved, then all stakeholders who have an idea can contribute to the project and each contribution adds to the original budget.

When you realize that you’ve spent twice your budget, the scope has doubled.

Step 2: Separate Direct Costs from Indirect Costs

Direct costs are costs which can be directly attributed to this project such as contractor costs, materials, equipment hire, project related travel, etc.

Indirect costs are the overhead associated with this project a percentage of the office space, utilities, administrative support, project management overhead, etc. Both matter. It’s not uncommon to see projects that miss their budget because they do not consider the portion of organizational overhead that is consumed by the project.

Part 3: Developing a Contingency “Bank” for Risks

All projects involve some unexpected obstacles. The issue is not about having funds set aside for contingencies but whether you have planned for contingencies.

A contingency reserve of 10% to 20% of the overall project budget is generally recommended for most projects. The percentage will vary in accordance with the level of scope definition and uncertainty of the estimates.

If the project is highly defined, has known technology, and has experienced team members, it could require 10%. For an exploratory project that is pioneering, it may require 25% or more.

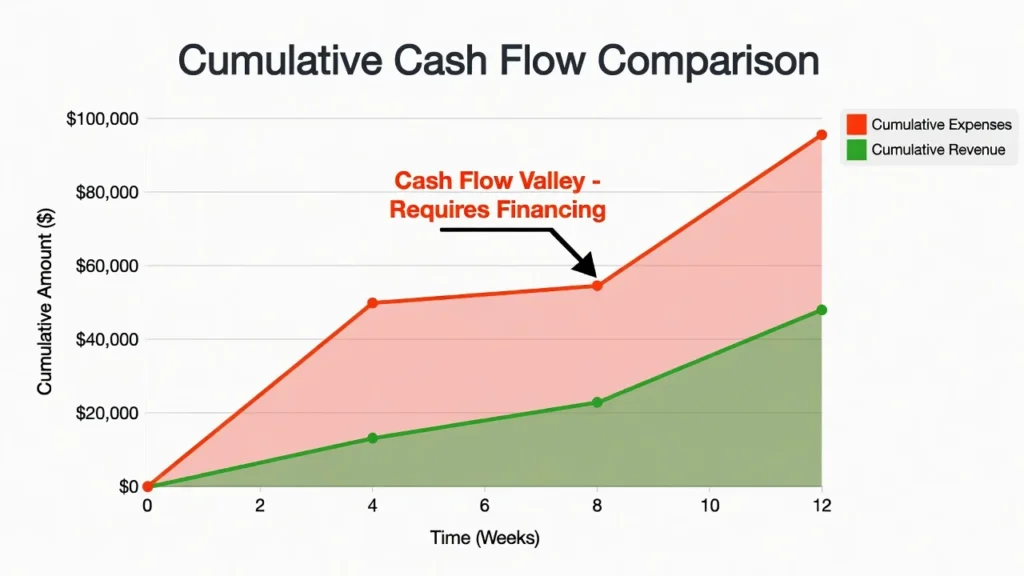

The 4 step is to time-phase your cash flow (avoid the valley)

The period where you’ve invested heavily into the project from the start and are spending a lot but haven’t had any milestone payments or something of value to show for that’s still invoice-worthy is one of the worst traps in project budgeting.

This moved me away from the brink of a disaster that nearly destroyed a valuable project. I had just secured a contract to do a training session for a business client. The overall budget was solid. Well, by week six, I had spent $20,000 on materials, facilitators and venue costs and had not yet received half of the payment. At the last moment I had to dip into my own savings to keep the project going and stopped the cash flow from ticking over.

Timephasing cash flow is a way to look at the total cash flow budget to see when the cash is going out and when it is coming in, either by week or by month, so that you never find yourself short of cash.

Step 5: Get Funding and Built into Your Proposal

If you need capital up-front that you’re not getting back until you’ve completed later milestones in your project, you must either possess that capital or finance the project before you begin it, rather than after you’ve already invested in the project.

Profit margins are not the only important aspect of project budgeting; cash flow management is also key. Numerous projects appear to be profitable on paper, but have unfortunately not got the cash in time to meet the revenue.

Step 6: Communicate and Communicate Progress to Steering Committee Monthly

Operational budget items need to be monitored less frequently and less formally than project budget items. The stakes are greater a project that has a 15% budget overrun in month two, can be a 50% overrun in month six if unnoticed.

To all project steering committees I work with, I give them monthly budget reports. This includes actual spend to date, remaining budget, forecast to completion, explanation of any significant variances and changes to the risk and contingency picture.

Budgetary Management: Monitoring and controlling your budget

Creating the budget is the beginning. The on-going task of managing it makes the difference whether the budget does its job or not.

What is Budgetary Control?

Budgetary control is a process of checking and adjusting the budget when there are any measurable changes against your prediction.

Budgetary control is a formalized management process in the field of organizational accounting. The Chartered Institute of Management Accountants (CIMA) describes this as the setting up of budgets and regular comparison of actual against budgeted results.

Budgetary control consists of three parts: tracking what has actually happened, comparing it to the planned events, and taking the right action on the results that are relevant. The third part, acting, is the one part that most people overlook.

The tracking of Budget Variance and KPIs

This is just the difference between what you actually spent and what you budgeted.

A variance of $200 is good, because it is favorable, as you had planned only $1,000 for marketing and spent $800. If your budget for utilities was $500 and you spent $650, then you have an unfavorable variance of $150.

Not all the variations have to be given equal attention: just the material ones. For personal budgets, a 5-10% materiality threshold is used. If I’m within 5% of my budget for a category, I make a note and sleep is not the issue. If I’m saying that I am 15% over, then that is investigated.

Key performance indicators KPIs are more than just numbers that track variances for business budgets. These could be things such as budget usage percentage, cost per unit, forecast versus revenue, percentage of revenue spent by departments, etc.

How often should you look at your budget?

For personal budgets: weekly check-ins are brief (about ten minutes) and provide early detection of problems.

A more comprehensive monthly review, which involves comparing all categories, revising projections and making changes to income and expenses, requires 30-60 minutes.

The normal reporting schedule for an organizational budget is done each month. In larger organisations, often quarterly reforecasts are conducted to adjust the annual budget for actual performance so far.

The time and method to make your budget adjustments

A budget is a plan and not a contract. However, as the situation evolves, the budget must evolve as well (and it always does).

Some good reasons for changing your budget are if your income has increased by a lot, if you have had an unexpected major expense, if your strategic priorities have changed, or if you have reason to believe that your initial assumptions were materially incorrect.

Make and avoid common budgeting mistakes

The 1 mistake is “beginning without a clear scope and goal.

If you do not know what you are budgeting for and what success means you are allowing dollars to chase a moving target. This principle is also valid for personal budgets, business budgets, and project budgets. When creating any budget, the three factors you want to write down are: what you’re budgeting for, the time period you’re budgeting for and the success you want at the end.

Mistake #2: Using Optimistic Income Estimates

This is the one mistake that is the root of all budget failures. People plan budgets as they think they will make a certain amount of money in the future, rather than as they expect to make a certain amount of money in the future. Be conservative. The more money you have, the better.

Erroneous Step #3: forgetting about Irregular Expenses

Annual insurance premiums. Car registration. Holiday spending. Back-to-school costs. These costs are not recurring, so they are simple to disregard when creating a monthly spending plan and they blow up the spending plan when they come due.

The answer is to take the annual expenses that are not regular and average them out to 12 monthly items and add them to a budget line.

Error #4 is creating the Budget but not checking it

If you don’t know how to track it, it’s just something to decorate with. It’s the monitoring step comparing actuals to the budget, investigating the variance and making adjustments where the budget gets its value. Plan your budget reviews as you would do for any other important meeting.

Avoid error #5: Ignoring Cash Flow Timing in Projects

The project budgeting was covered in the project budgeting section a project may appear to be profitable on paper but fail, due to the fact that the cash flow has run out and the money hasn’t come in. Time phase cash flows, not only amounts!

Mistake #6: Not Writing Your Budget Down

I have never known anyone who has done it completely in their heads. Those who have good money management skills either have a budget they adhere to or have developed the discipline to managing their money to the point that they don’t need to be actively managing it. If you are still establishing them, make it a habit to write it down.

When you’re struggling with budget problems, what do you do?

Many people don’t bother to budget because they have a budget deficit when your expenses are more than your income. Just turning a blind eye does not bring it to an end.

There are two ways to go: one, boost your income; and two, trim your costs and most people need both approaches. When you land on the other side, if you have an excess amount of money that is surplus to your needs, then this money goes directly to your priority goal: debt elimination or savings.

Option 1: Increase Income

Find valid means of increasing your income (overtime, a side hustle, sell unused items, rent a spare room, seek a raise). Sometimes an emergency is over before you’ve managed to reduce your spending, and even a short-term gain can help fill a shortfall in income.

Reduce your expenses by cutting back on non-essential items

When it comes to filling in a budget deficit, the quicker it will close is if you focus on discretionary spending, items that you want but don’t need. Take a look at your variable expenses category, item by item and ask yourself: is this a need, or is it a want? The first type of expense to cut is usually one of the most impulse spending categories, such as subscriptions, dining out, entertainment, or other categories.

A third option is to restructure the fixed costs

If saving variable costs isn’t sufficient, see your fixed costs. There are ways of cutting fixed costs that variable spending cuts do not equal—such as refinancing the debt at a lower interest rate, downsizing the house, or renegotiating insurance premiums.

Resources for budgeting tools and technology to make it easier

The best budgeting tool is the one you will use regularly. However, it will be much easier with the right tool.

The most flexible is a spreadsheet. Google Sheets provides a number of free budget templates, as does Microsoft Excel. Spreadsheets are harder to enter data into it, but it provides complete control over categories, formulas and format.

Special budgeting software automatically tracks transactions by linking to bank accounts and credit cards. They sort expenses automatically, give you a visual breakdown of when you have been spending more or less and will warn you before you cross a spending limit.

Business budgeting software, such as QuickBooks, Xero or FreshBooks, is the norm. These platforms connect with bank accounts, create financial reports, and offer detailed variance analysis—features manually spreadsheets struggle to keep up with at scale.

Project management solutions frequently have integrated budget tracking tools that automatically link resource allocation to task completion, helping with budgeting.Project management solutions sometimes have built-in budget tracking tools that link resource allocation directly to task completion, supporting project budgeting.

Frequently Asked Questions About Budgeting Process Steps

How many months does the budgeting process take?

If you have your financial records handy, it will take you just a few hours to create a basic personal budget. It takes about three months of trial and adjustment to get good at it to create a budget that works for your life.

What are the most important budgeting process steps?

All eight steps are important but if I had to pick just three, they would be: #1: establish clear financial goals before starting, #4: utilize actual historical data and not guesses and #8: review actuals against budget throughout the period. The vast majority of budget failures are due to the failure to budget for one of these three.

Are the steps of budgeting the same for personal and business budgets?

Yes. The basic process for the budgeting process is the same. These differences lie in their size, complexity and number of stakeholders. It could take you an afternoon to prepare a personal budget. A corporate budget could require 3 months and 50 people. The concepts behind it – objectives, income, costs, allocation, monitoring – are the same.

How do budget and forecast differ from each other?

A budget is a plan it’s what you will spend and earn during a specific amount of time. A forecast is a prediction, it is your best guess on what will actually occur, based on your current situation. Financial budgets are normally prepared on an annual basis. Forecasts are updated on a regular basis with new information.

What are some indicators that my budget is effective?

If you’re spending less money every month than you would like to be, then your budget is working. More specifically: you’re not constantly being caught off-guard by unexpected expenses, you’re increasing your savings, you’re paying down your debt (if that’s something you’re looking for) and you’re not overdrafting. The difference between people who plan and people who hope is knowing each of the steps of the budgeting process, from goal setting through monitoring.