Tight Budget? 11 Real Ways to Save Money That Actually Work

You’re about to discover the truth, so let me tell you from the beginning. The vast majority of the articles on the subject of living on a tight budget are authored by people who haven’t had to choose between food and lighting their home. They give you tips like “don’t drink that morning latte” as if that’s what you are missing.

I have been there. Being on the verge of paying your bills does not imply you’re reckless with funds. It typically refers to not keeping up with your cost of living, and the reality of that situation is happening for millions of homes today.

The content of this site is unique. I am going to explain to you 11 strategies that real people use, but that most financial websites fail to mention and a very real action plan you can take this week.

What “Tight Budget” Actually Means (And Why Most Advice Misses the Point)

One usually associates a tight budget with a person who is spending too much. Actually, a tight budget is when you’re making too little money or not enough to cover your basic bills.

In recent years the cost of living has risen significantly. supermarket prices continue to rise, rents are higher than they were three years ago, and there’s been little wage growth for many people. The Federal Reserve has reported that the total amount of consumer debt in the United States has surpassed $17 trillion, according to recent reports, which is a record high. These are not personal shortcomings, they are economic facts.

It’s really difficult to save when you’re already as stretched as possible. It’s all about the small victories that will create a little wiggle room in your budget. $10 per week can make a significant difference over a year’s time. Sometimes, though, cutting is not the complete solution. I will speak about that truthfully later in this article.

When Is a Budget Considered “Tight”?

For some, a tight budget means saving as much as possible.For others, a tight budget is defined as spending as little as possible. This is dependent on the location, the number of people you support and your fixed costs.

In one person’s case, a tight budget could be $1,500 in a month’s income and $900 in rent. It could be a family of four that makes $50,000 per year but has $20,000 of consumer debt that has high monthly payments taking a bite out of their paychecks.

They all have one thing in common: bills for basic needs (housing, food, utilities and transportation) consume the majority or entire income. There’s little money left to save or spend on the unexpected. It’s clear to see that’s the first step to changing it.

Why Inflation Makes Tight Budgets Even Harder Right Now

The inflation rates have been high and most workers’ real wages have been stagnant for three years. Consumer debt has surged and people have been using their credit cards to cover their spending needs. In most cities the cost of living is just ahead of income.

This is an economic fact, not a budget issue. Naming is important as guilt and shame do not do a job. This is not your fault and it is not something that you can remedy by eliminating all the little pleasures in your life.

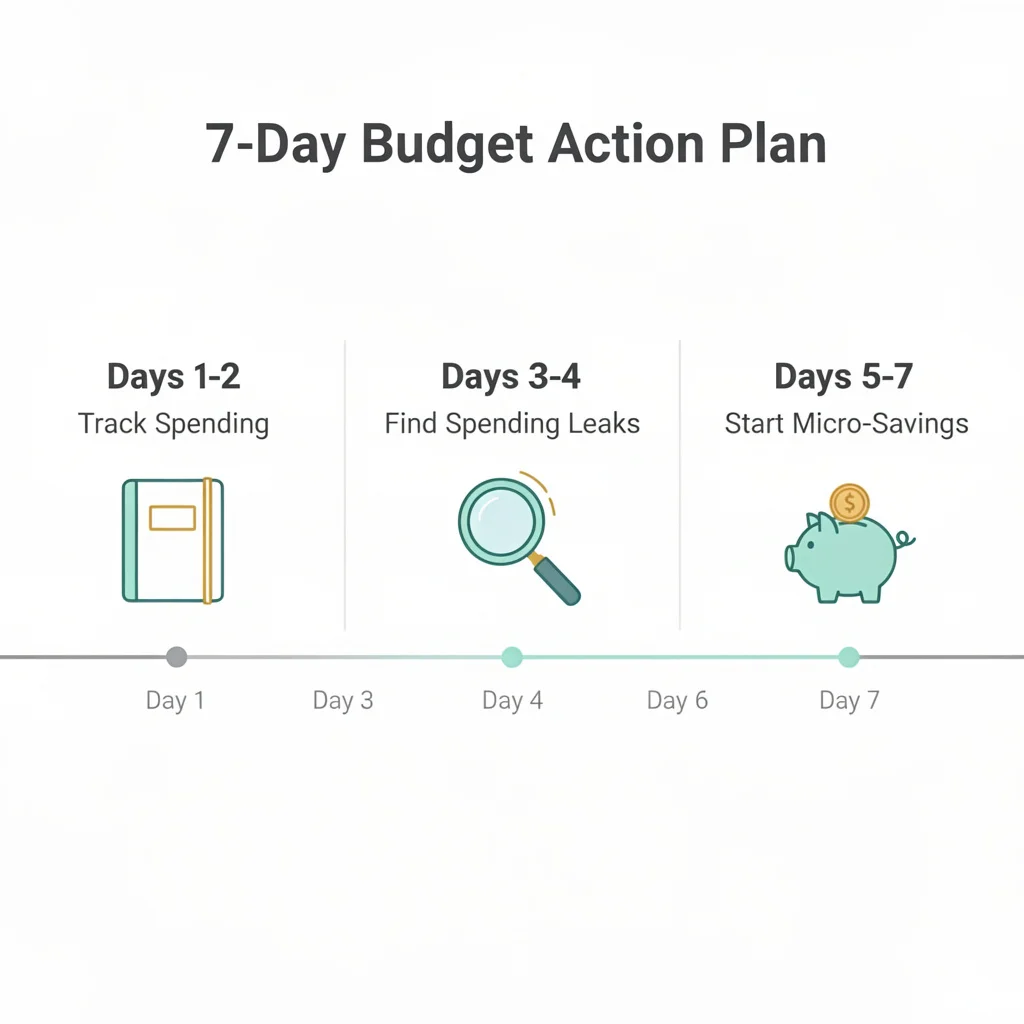

Start Here: What to Do in Your First Week on a Tight Budget

Many people decide against keeping track of their finances because they attempt to change everything at once. They read a list of 20 tips – and then they freeze before putting any of them into effect. Here’s an easier one for you, a strategy for the first seven days.

No flashy app needed! No perfect system needed. If you’re completely new to managing money, start with the budgeting basics to build your foundation then use this 7-day plan as your first action step. The first step in managing the money is to find out where it’s going and not where you think it is going.

even $2 per week counts.

Day 1–2: Write Down Every Dollar You Spend This Week

Wait until you don’t have to open a budgeting app. Take a notebook or the notes app on your cell phone, and record all of your purchases! Each and every cup of coffee, each and every grocery trip, each and every online impulse purchase. Everything.

Any amount of money that is spent is an expense, even if it is small. A customer purchases a stick of $3 coffee five times per week for a year, paying a total of $780. Most people are surprised when they manually record their expenses for the next 2 days. Not shameful at all. It’s about providing yourself the genuine data you require to make modifications. You can’t change what you’re spending until you can see it.

It is also here that the “cash flow management picture” becomes clear. You’ll begin to realize just how much difference there is between your actual spending and your perceived spending.

Day 3–4: Find Your Two Biggest Leaks

After 2 days of tracking, check your list and identify the two biggest spending leaks! Most on a budget fall into three categories: They’re paying for subscriptions that they forgot about, going out to eat more than they expected, or making more small purchases that add up over time.

Determine the two largest leaks and work on them. Don’t do it all in one go. If you cancel two unused subscriptions quietly that quietly cost you $10 a month, you will save $20 to $50 immediately. Getting that reinvested in cutting costs in a particular area creates momentum quickly.

When cutting spending, it’s best to first cut discretionary spending because you will see results right away and will be motivated to continue.

Day 5–7: Set Up Your First Micro-Savings Transfer

On Day 5, automate a transfer to a savings account that you can afford. Any amount of $2 a week is acceptable. It’s not how much it is. It’s developing the discipline of transferring funds prior to using them.

Automated savings takes the decision away. You don’t need to make any effort to increase your savings rate; it begins to grow starting in week 1. No need to be a big income earner to get going. It takes only a regular practice and a level of self-discipline to leave that money where it falls.

Why Your Budget Keeps Failing (And the Fix Nobody Talks About)

I want to share one thing I learned from a budgeting creator that is extremely frugal, Kate Kaden, that changed the way I approach budgeting. Most people have one budget that they then copy in exactly the same way each month. Monthly repeats of the same numbers, categories, allocations. And then, when it continues to fall apart, they are confused.

The answer is simple—life doesn’t happen in a vacuum, but each month is different. Static monthly budget is almost certain to fail as it does not take into account the flow of money in your life.

The “Same Budget Every Month” Mistake

Kate pays her car insurance twice a year (May and November) to get a discount. It may be obvious, but her May budget is very different than her April budget. During the summer months she spends more on food and experiences. During winter her heating costs go up.

If you’re operating on the same budget each month, you’re not taking into account any of these. A fourth quarterly bill that shows up without warning will cause a budget that wasn’t prepared to meet it to explode. The variable costs such as paying your bills, food, and gas change from month to month and can cause constant pressure if you don’t recognize that change.

The solution is to create a new budget each month, reflecting the actual activity and circumstances for that particular month—follow a step-by-step budgeting process to make this monthly review systematic and sustainable. Review upcoming payments, seasonal bills and areas where variable costs will require added buffer.

How to Build a Budget That Actually Fits Next Month

Here’s how I do it at the beginning of every month. I record all of my known expenses for this particular month (including odd costs such as school fees, insurance renewals, annual subscriptions etc.). Then I round up my variable costs by approximately 10 to 15 percent.

For instance, if I’m spending about $130 on groceries, then I set aside $150. If the actual bill ends up being $130, then I just transfer $20 of that amount into savings. This rounding up policy is effective because no cutting is done. You are taking the money that is already saved – the money that naturally exists – which will quietly go away.

It is also beneficial for cash flow control as you never get surprised by having a variable expense slightly more than anticipated. The buffer has already been paid for.

11 Ways to Save Money on a Tight Budget (Ranked by Impact)

All strategies for saving money are shown in order of effectiveness in the real world, with the easiest ones to implement first and the greatest impact in saving real-world dollars listed top to bottom. For a comprehensive overview of all the ways you can reduce your monthly expenses, we’ve covered that in depth—but these 11 strategies are the ones real people on tight budgets say actually work.

the fastest results.

1. Do a Subscription Audit This Week

This is the one quick, no-cost method to save money. The majority of people are paying for 3-5 services that they use very little. The creator of frugal living, Jennifer Cook, cancelled the Hulu, STARZ and Audible channels, as they no longer offered any value. She didn’t miss a single one.

Review the bank and credit card statements and identify all the recurring transaction. If you have to ask yourself, for each one, “Did I use this in the past two months?” then it probably isn’t. Otherwise, cancel it now. With only one afternoon of review, you can save $30 to $100 a month by cutting back on unused household subscriptions.

2. Master Grocery Shopping Before You Step Inside the Store

You’re saving money at the grocery store when you’re not there! I have found one of the best ways to do this to be pantry cooking: Using what is already in the pan before it is time to purchase more. Always start by looking in the fridge and cupboards and prepare a meal using these items. You save food waste and delay your next shop by a couple of days.

If you must go out and shop, pre-price your list before you leave the house to know the complete count a grocery budget calculator can help you set realistic spending limits before you shop. Or better yet, make an online pick up order rather than going in person.

One redditor commented: “My family had a single rule that we would remove stuff from our cart before checking out since we could see the total.

With a strict list, and pairing it with meal planning, comparison shopping will be much easier and will help to keep impulse purchases to a minimum!

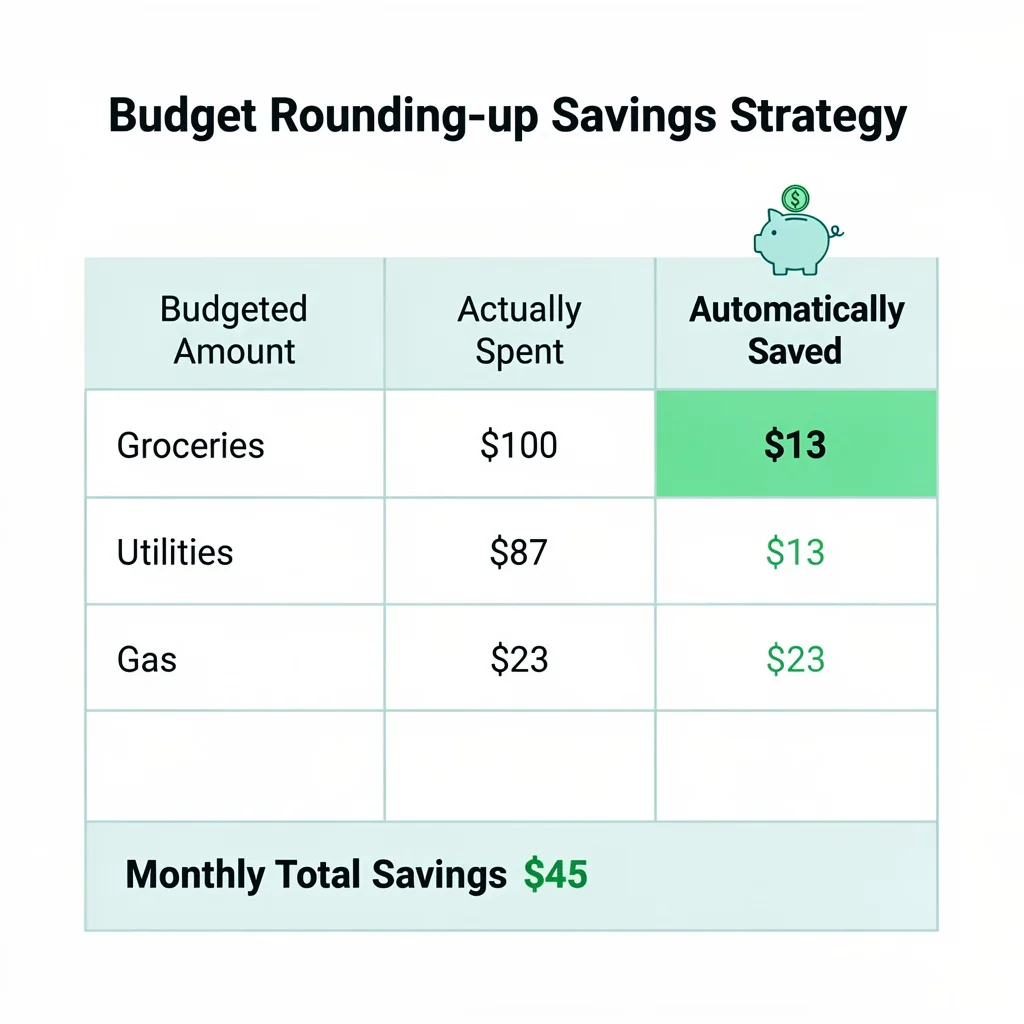

3. Use the Rounding-Up Strategy to Save Without Trying

This is Kate Kaden’s way and it is one of the most helpful tips on frugal living that I’ve seen. You rather round up the variable budget categories and have the difference automatically saved each month.

most people save $30-$80 monthly without noticing.

Your grocery budget is $100, and you spend $87 of it, so you put $13 into savings. If your utilities are supposed to be $150 and you spend $135, $15 goes into your emergency fund. Over the course of a month, it saves you $30 to $80 without even realizing it, across a range of categories.

You built these automated savings into your initial budgeting and that’s what they are, automated.

4. Negotiate Bills You Think Are Fixed

Some bills, such as cable, internet and insurance, are not fixed as many people think. These companies would like you to stay a customer and loyalty discounts are not a myth. I called my internet company, and I just said, “Hey, I’m looking around and I want to see if I can get a cheaper rate.I called my internet provider and just said, ” Hey, I’m looking around and I want to see if I can get a cheaper rate. After five minutes, my monthly bill went down $20.

Tap into internet and cable providers, then insurance. Call and haggle over bills directly: explain that you’re on a budget and their options if you’re a loyal customer. If you can cut $15 off a bill you will save $180 per year.

5. Apply the 24-Hour (or 30-Day) Rule to Every Non-Essential Purchase

Wait 24 hours before purchasing anything other than food or utilities. Wait 30 days for larger purchases. This one habit will reduce the most of impulse purchases because most of the time, you will simply forget about that product or know that you didn’t really need to purchase it.

A practical tip from a video maker I follow: Set up a tangible or digital reminder of your financial objective that is easily seen. The impulse is interrupted by a note that says “emergency fund goal: $500” stuck to your card or set as your phone’s lock screen. This 30-day rule is particularly effective when shopping online, as online platforms are engineered in such a way as to create this gratification loop.

6. Become a “Free Stuff Expert”

This mindset was introduced to me by Jennifer Cook and it is a real life-changer when it comes to being in need. So, before I purchase anything now, I’m first going to see if I can get it for free.

The use of the public library is extremely low. With a library card, you can use the library to make use of virtually all the resources it provides, including books, movies, audiobooks, magazines, and in many places, access the Internet. People often leave furniture, baby things, kitchen utensils and household goods for free on Facebook Marketplace or local buy nothing groups. The principle Jennifer follows: Take only what you need. You don’t want to pay off a debt problem with an organization problem.

Second hand clothes, furniture and tools can be the same quality as brand new and can be purchased for a much lesser price.

7. Use Cashback Apps and Stack Savings

Roundup Apps: These apps will reward you for comparison shopping and purchasing items you already intend to purchase, such as Ibotta and Fetch Rewards. The trick is to not let the app influence what you purchase. Include only things that are on your list.

One of the more sophisticated options is to stack the savings. Earning Target Circle with Ibotta cashback on the same product is a case of double discounts. For larger items and some travel bookings, Rakuten operates like this too. There is no way you are going to retire on cashback, and eventually it would add up to a few hundred dollars a year, even if you don’t change what you buy.

8. Cut Energy Costs with Simple Home Habits

One of the easiest variable costs to reduce in your household budget is utility costs. Switching off lights when they’re not in use, unplugging items that consume standby power and lowering your thermostat a couple of degrees can lower your bills by $20 to $40 each month.

Jennifer Cook revealed two things that most people fail to consider. Inspect your sink drains for slow leaks under the sink frequently – these can cause high water bills without you realizing it. Second, be sure that doors and windows are sealed, as inadequate insulation makes your heating and cooling system run a lot harder than it really needs to. Both of these costs are free to remedy and both can be seen on your next bill.

9. Plan Meals Weekly and Cook in Batches

t doesn’t take a great deal of effort to save real money on food; you don’t have to make elaborate meal plans. Choose 5 easy dinners for the week and make a list of what you need to make each night – then purchase those items. Cook 2-3 on weekends and freeze the rest.

Kate Kaden’s channel had one viewer post this recipe for a slow cooker white bean and ham hock soup, which serves a family of 4 for less than $5. There are plenty of budget-friendly recipes out there, and that’s a prime example. All you need is a plan before going to the store.

Another advantage of batch cooking is that by the time you get home at the end of the day you are tired, and dinner is ready to go. That’s enough to take the craving for takeout out of the equation.

10. Sell What You Don’t Use, Fix What You Have

Take a tour of your home and look around for items that have not been touched for the past 12 months. Pick up sell it on eBay or Facebook Marketplace. You will not get a salary when you sell what you have, but quick cash can get your finances going or help fill in a quick cash deficit without taking on debt.

You can also save on the cost of replacement parts by learning the basics of the repair work. Another Reddit poster recounted how he learned to fix cars enough to drive a $500 used car for years. He didn’t pay anything for his car. Simple DIY tasks can save money over time.

11. Automate Savings on Payday Even $5 Counts

Pay yourself first. Pay yourself first, by putting yourself in your savings account on payday before you pay any bills. $2 is sufficient to get a start. It isn’t so much the amount at this stage. It is easy to build the habit.

After you’ve gotten into the habit of saving, raise the amount transferred over time, if you can. You won’t have to make this choice again each month, and your savings will increase over time.

The Budget Framework That Actually Works on a Tight Budget

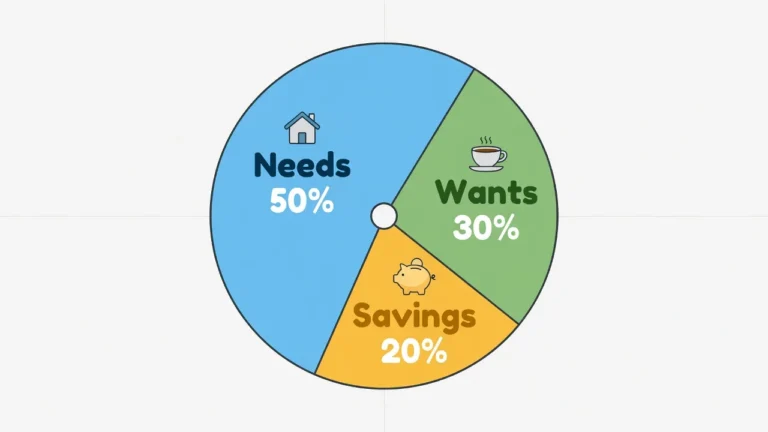

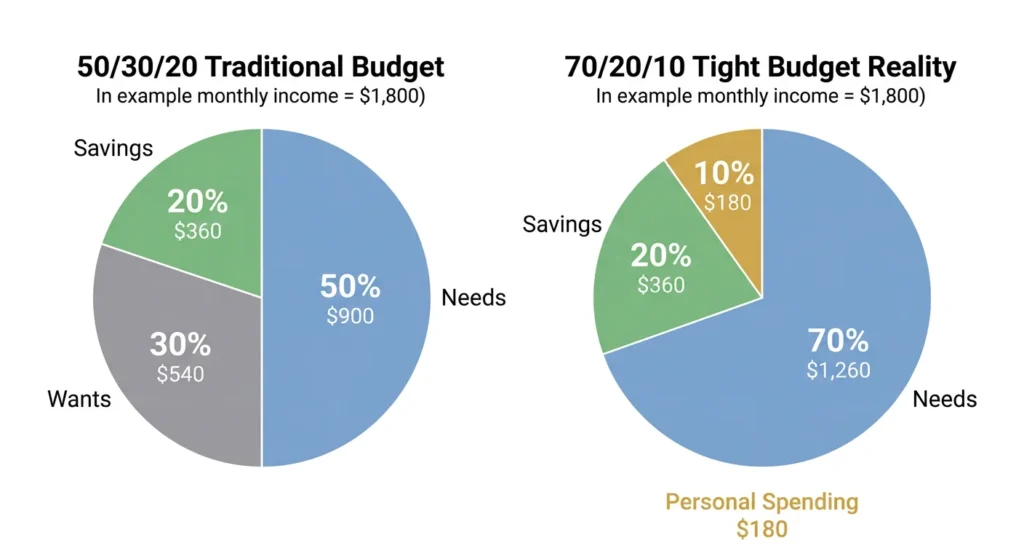

It’s only natural if you have ever heard of the 50/30/20 rule on a budget and thought, “I don’t have a 50/30/20 budget.” The rule makes the assumption that only half of the income goes toward needs. For the majority of the population on a strict budget, requirements do make up 70%, 80%, or even 90 percent. If it’s a plan designed for another person’s budget, it will not work for you.

a tight budget—making it more realistic than traditional advice.

Why the 50/30/20 Rule Doesn’t Work for Everyone

The 50/30/20 rule represents 50% of your income for needs, 30% for wants and 20% for savings. It is a good basis if you have an income that lets you cover all of your basic costs. However, if you are paying $1,200 in monthly rent, and you earn $1,800 per month, you have little room for any other expenses. That 30 percent is for wants sounds like a slap in the face.

The rule puts people who have a structural inability to spend in a situation where they feel guilty. If your essentials consume the bulk of your income, you must have a plan that recognizes this, rather than assuming you have some money to spend.

The 70/20/10 Rule: Built for Tight Budgets

A better rule of thumb is the 70/20/10 rule: 70 percent for needs, 20 percent for savings, and 10 percent for personal spending and small indulgences. It understands that needs take precedence over constrained budgets, and preserves room for saving and some fun.

When you see what that looks like on a $1,800 monthly take-home pay, you’ll see $1,260 for needs, $360 towards the savings and $180 for personal spending. If 20 percent savings seems unattainable, begin by saving 5 or 10 percent and ramp it up as much as possible. The key is that you make saving a stated objective in your budget, rather than putting it off to the side because of whatever is there.

Building an Emergency Fund When You Feel Like You Have Nothing Left

I know what it is like to read a piece of advice to build up an emergency fund and say “with what money? However, what I have learned is this – even a little emergency fund can make a huge difference in real, immediate ways to your finances. The difference between a flat tire that is just a nuisance and a flat tire that is a financial disaster.

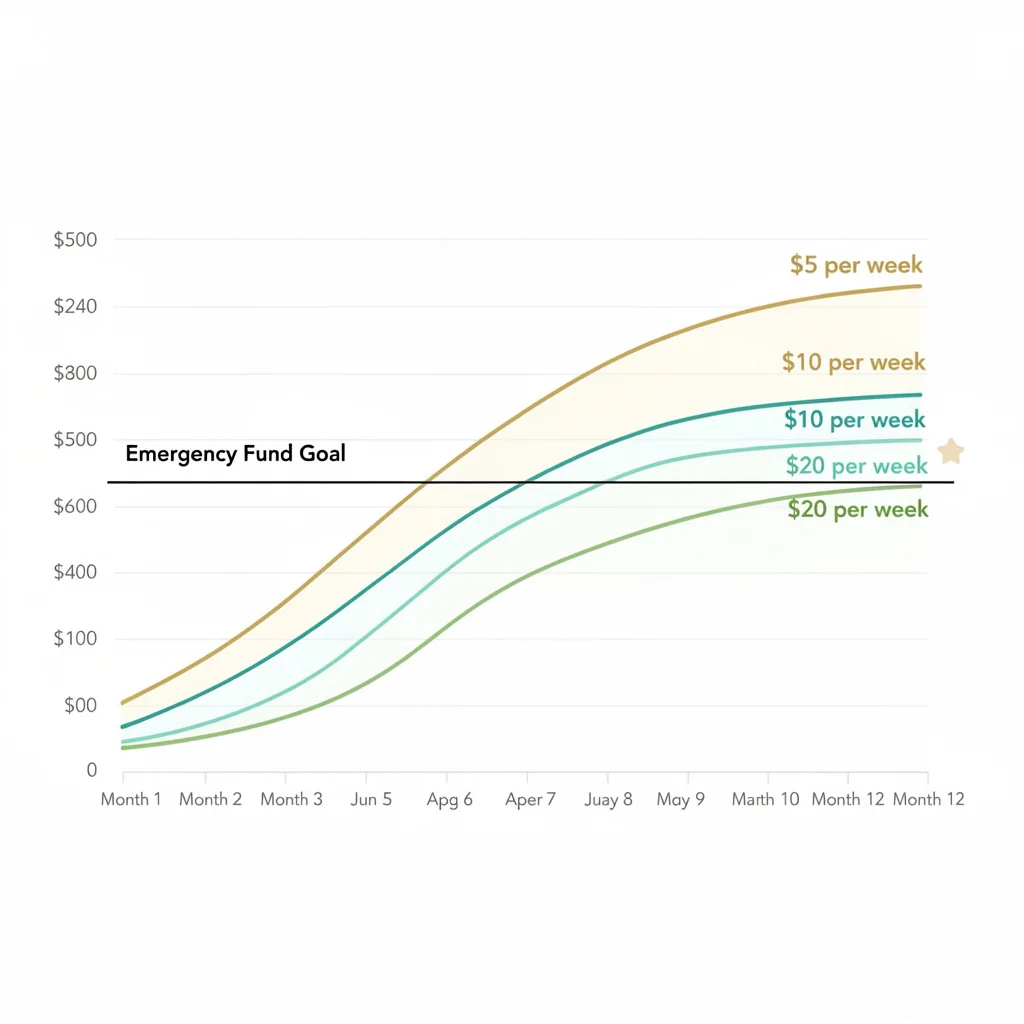

When you are starting to save, you should save $500 first—ideally in a high-yield savings account where it earns interest while staying accessible. That is enough for most little setbacks: your car needs repairs, your doctor charges a co-pay, your refrigerator breaks down, you have an unexpected bill.

You can reach it in approximately 50 weeks at $10/week. You can get there in 25 weeks at $20 a week.

fund buffer.

This savings rate is like paying rent or a phone bill – it is a necessary expense. The second you save $500, your financial objectives change from simply making ends meet to taking action to create something. That’s a change in perspective for more than the $500.

Some people find themselves in the position of borrowing on credit cards or from pay lenders whenever an unforeseen expense comes up if they don’t have this buffer. This perpetuates the cycle.

Budget Buffer vs Emergency Fund: What’s the Difference?

Kate Kaden is the only budgeter I know who has called attention to this distinction, which is not found in any traditional budget guide: Budget buffer and emergency fund are two entirely different animals and you need both.

Your budget cushion is the amount of money that you always have in your checking account that is equal to one month of your normal living expenses. It absorbs the natural cash flow bumps that occur each month: a bill that comes in a bit earlier than expected, a subscription that renews a little sooner or a variable expense that costs a bit more than you anticipated.

Your emergency fund is not part of the savings account, and is only used in emergencies – such as a job loss, major medical bill, or serious repair bill. Create the buffer first since it helps to safeguard your daily cash flow. Add the emergency fund to that.

Dealing With Debt on a Tight Budget Without Making Things Worse

I had been spending years seeing how my budgets got eaten away by debt until I figured it out how to plan the debt in a way that would make them work.

If you pay a big chunk of your income on high-interest consumer loans, you’ve got little to spare on anything else, including saving or paying off other debt. Wondering how much credit card debt is too much? If your monthly minimums exceed 10-15% of your income, aggressive action is needed.

When it comes to establishing any type of financial stability, it’s not something individuals can opt for, but they need to understand how to manage debt.

Pay Off High-Interest Debt Before Growing Savings (With One Exception)

The mathematically correct solution is to first pay off the debt with the highest interest, and then pay off the next debt after that debt has been paid off. This is the debt avalanche strategy and over time will save you more interest than any other repayment strategy.

But there’s one caveat. Paying down debt debt aggressively on your credit card is not a best practice until you have a small emergency fund of at least $500. When you are living off your credit and debt and then come across an unplanned expense, you will have to take on more debt right away. The small buffer breaks it.

Once debt is out of the picture, attack the buffer with all you have! If you’re ready to tackle debt elimination seriously, an aggressive debt payoff plan can help you become debt-free faster than you think—even on a tight budget.

If it really lowers your rate and your monthly payment, a lower interest rate personal loan may be helpful when consolidating your debt. It only does this if you also don’t add more charges to the cards after consolidation.

Why Payday Loans Make Tight Budgets Worse

Payday loans feel like relief in a crisis, but they are among the most damaging financial tools available. Interest rates are extraordinarily high. According to the Consumer Financial Protection Bureau, the typical payday loan carries an APR of around 400 percent. What starts as a $200 loan to cover a gap can trap borrowers in a cycle for months or years.

If you are facing a genuine emergency, explore these alternatives before considering a payday loan: a local credit union emergency loan, a direct payment plan with the company you owe, community assistance programs in your area, or employer programs that offer pay advances to employees in need.

It is also worth checking whether you qualify for the earned income tax credit, which provides meaningful tax relief to lower-income workers and could represent hundreds or even thousands of dollars annually that many eligible people never claim. The earned income tax credit is available to workers who earn below certain income thresholds. For a single filer with no children, eligibility may apply at income levels under roughly $18,000, and families with children qualify at higher thresholds. The IRS Free File tool can help you determine eligibility and claim it at no cost.

Not every alternative will be available to you, but any of them is worth checking before taking on payday loan debt.

When Cutting Expenses Isn’t Enough The Income Problem Nobody Wants to Admit

If saving money is the only solution to the problem, then we need to talk about income.If cutting expenses is the answer, then we need to talk about income.

This isn’t something that you’re going to find in many personal finance articles outright: When income is extremely low, reducing spending will only get you so far. The bottom line on spending is that it can be cut no further when it is already at the lowest possible level. No, that’s not a lack of discipline. It is just math.

I have witnessed this admitted openly among those who are dealing with a budget constraint. If you make $25,000 a year in a high cost of living city, you might actually be in the red. In that case, the solution is NOT another frugality tip! The solution is greater income.

Realistic Side Hustles That Don’t Require Special Skills

There are side hustle opportunities that can be started pretty easily and quickly that don’t require a lot of skills or money. The quickest place to begin selling is on Facebook Marketplace or eBay for items that are NOT being used around your house. You get rid of clutter, and make money too.

Older students can tutor younger students in a topic they are knowledgeable about, walk dogs in the neighborhood, grocery deliver through apps, and provide basic handyperson services in the community – all of these are real jobs people do to make extra money. It is not about business building here. It is building a second income which can help you fill the money gaps and make your financial goals more attainable.

When to Consider Upskilling as Your Biggest Budget Move

The best financial move you can make is sometimes to get a credential that increases your income for life. I stumbled upon one very moving story that has stuck with me: A young woman, working about $25,000 a year in retail, became a dental assistant and now a dental hygienist. She earned approximately $80,000 annually. A year of canceling subscriptions and stacking coupons couldn’t have made the impact.

Whether it’s healthcare credentials, trade skills, technology credentials, or licensed professional programs in areas with true demand, these new credentials can make a significant difference in your income path. Many community colleges have low tuition, and some programs are eligible for financial aid. The initial expense is genuine, but the earning potential over time is enormous compared to the ability of being frugal.

But, I would like to state that upskilling is not an instant solution. It takes months to years to complete the certification. But, this shift in income trajectory is often the most impactful financial move that a low-wage worker can make.

If it’s a lack of income, then it’s important to go for income growth, which is the most critical long-term strategy you can have to improve your financial situation.

Save Your Next Raise Before You Spend It

So, if you are already living comfortably and you are getting a raise, there is a great way to not let your lifestyle creep up. When your raise comes, establish an automatic transfer into your savings account of the exact increment you receive.

You have already been living on your old salary, so you’re not going to notice the lack of the extra money. You can’t get used to paying for it, so you don’t miss it. Jennifer Cook takes this route, and calls it the easiest method to save money without feeling deprived.

The Psychological Side of Living on a Tight Budget (This Part Is Hard)

This isn’t discussed enough. It is not only a financial issue to live on a shoestring budget. It’s an emotional one, and that’s something that isn’t pretending to bring anyone happiness. The daily grind of living on a budget, the worry associated with logging in to see how much money is available to you, and the embarrassment and awkwardness of declining requests from friends and family that you know you aren’t able to afford these situations really take their toll.

I wanted to touch on this topic directly as I don’t really think frugal living is something that you can do if you feel that it is something that you are trying to avoid.

Stop Making Your Budget Feel Like a Punishment

What I wish to share here is a reframe offered by Kate Kaden that I believe is a true transformational. She has a budget and not a limit, it’s a permission to spend. With a budget, you’ll be aware of how much you can spend in each category without remorse. It’s not the budget that’s holding you back. It’s the one thing that is clearing your path.

This budget cannot be maintained by financial discipline. The reason budgets usually don’t work is there isn’t any will power involved; it is simply that the budget is so restrictive that it leads to a feeling of deprivation that just cannot be taken. If the budget even includes a little bit for something fun, like a cup of coffee, a treat, a small experience, then you can actually adhere to the budget on a long term basis.

Set aside $5 or $10 to spend without any remorse. That little bit allows for that mental space to continue.

The Quarter Jar Trick That Changes How You See Yourself

I heard a story about a guy who had three jobs, was doing college full-time and was still living from paycheck to paycheck. They were feeling bad about themselves and it was taking its toll. At the end of each day, they poured out any coins they had on them into their dresser glass jar for a period of time.

One day it was a quarter. There were no days some days. Then, when they saw that jar slowly filling a little something had changed for them in their own eyes. They no longer thought of themselves as low on funds but rather they thought they were on a journey toward something. That was the beginning of a new attitude towards money.

Making progress is a huge motivator! Use a physical method to monitor yours, like a savings tracker on paper, a jar of change or a progress bar on an app.

Free Ways to Socialize Without Spending Money

There are many ways to socialize without spending any money, including: Some ideas for socializing without spending money are:

Social pressure is one of those hidden expenses of living on a tight budget. Owning to the norms of going for a dinner with friends, paid events, buying gifts for every occasion, etc., these aspects work quietly against even an elaborate budget.

The answer is not to turn away from the social life. It is redirection. Propose a walk in the park in place of a restaurant. Watch a film at home rather than in a movie theater. Take advantage of free events in your community such as community festivals, library programs and outdoor concerts. There are a lot of places that offer free entertainment, if you’re looking for it.

This way, frugality and socializing come hand in hand.

5 Tight Budget Mistakes That Keep You Broke Longer

These are the things I learned the hard way from real people dealing with a limited budget. Most of the tips in this article will do less for you to progress than avoiding them.

Error #1: Applying a fixed amount monthly. Your budget shouldn’t be the same as life! Rebuild it each month according to what actually occurs – bills due, seasons changing, irregular bills expected etc.

Error #2: Bills placed on auto-pay and never checked. Companies quietly and incrementally increase prices. I’ve heard of one individual who had their streaming service triple in cost without them realizing since they weren’t checking the cost. Prior to paying bills, check them by hand.

Mistake #3: Coupons for items that you wouldn’t otherwise purchase. Coupons only save money if you’ve already planned to purchase the item. It’s spending money, not saving.

Error #4: Accepting freebies that aren’t necessarily needed. While there may seem to be a benefit to free, there are definite costs to clutter—space, organization, and sometimes disposal fees. Only use what you will actually need.

Mistake 5: Delaying savings until you have more money to save. You can get started at $1 per week. The amount in the beginning is almost irrelevant. The habit matters. It grows in proportion to your income when you get more money.

Your Tight Budget Action Plan: What to Do This Week

Here is your plan for this week. Not next month. Not when things calm down. This week.

This week’s five priorities:

- Record all spending over the one-week period.For 1 week, record all spending. Try not to assess or criticise what you see. Simply observe it from a distance.

- One or more subscriptions that you do not use in the last two months should be cancelled.

- Before your next payday, any amount, transfer your money into a savings account automatically.

- Plan to use the kitchen in the pantry before your next grocery shopping. Make do with what you have before purchasing more.

- Record your first specific money goal. If it’s $500 in savings or if you’re paying off one debt, you’re paying off one debt.

What saving money on a tight budget actually looks like over time:

During Month 1, you pinpoint the biggest spending holes and uncover where your money has been going.

In month 3, you can see that the recurring savings occur for canceled subscriptions. You’ve silently accumulated some money in your automated transfer. You have roughly $100 to $200 saved.

By month 6, most have their first $500 emergency fund. The financial strain begins to become a little more manageable.

Month 12: $10 a week becomes $520. $20 a week becomes $1,040. Little things done consistently add up to something real.

This week isn’t the week to make radical changes in your life. It’s simply a matter of getting going.

One tracking habit, one cancelled subscription, and one automated transfer. That’s all you need to start moving your money in the right direction. Ready for more? Learn how to save money fast on a low income with additional proven strategies.

Frequently Asked Questions

What does being on a ‘budget’ mean to you?

When you live on a low budget, the money you spend on bills such as housing, food, utilities, and transportation is making up the bulk, if not all, of your paycheck. There’s barely anything left to save for emergencies or anything else. It is not a personal failure in finances but is more about the economy such as wages not keeping up, inflation, etc.

When I have no money to save, how do I get off this tailspin frugality?

Do less than you think you can. Before you spend any money, arrange to have $2 or $5 transferred to your savings on payday. Meanwhile, conduct a subscription audit and cancel all the subscriptions you haven’t used in the last 2 months. These two actions combined can free up $20-$50 per month almost instantly.

What is the best way to budget when you have a low budget?

There are more realistic guidelines when it comes to limited income, the 70/20/10 rule. It sets aside 70 percent for needs, 20 percent for saving and 10 percent for personal spending. If you can’t save 20 percent at this time, consider saving 5 percent, and gradually increase your savings rate as your situation improves. For more detailed strategies, check out this complete guide to budgeting on low income.

What are some ways to cut costs if it’s all too much to pay for?

Consider trying subscription services first because they don’t involve major changes in your lifestyle. Next, read about grocery spending by meal planning and cooking in the pantry. Call the internet and insurance companies and discuss the bills with them to try and lower the price. These three areas combined can save a typical home $50 to $150 a month, or more. Determine if you are eligible for the earned income tax credit which many lower income individuals may be eligible for and don’t claim.

If I have a tight budget, what is the best initial financial objective to have?

The first step is to have a $500 emergency fund. This one time payment will cover most minor financial needs and not have to rely on credit card debt or payday loans in case of an unexpected event. It costs $10 per week and requires 50 weeks. You can get there in 25 weeks if it costs you $20 per week.

What do I do if I already have debt and am already maxed-out on my budget?

Use the debt avalanche technique, or pay off the debt with the highest interest rate first, but create a small emergency savings buffer of $500 before you start paying off debt aggressively. If you didn’t have that cushion, then if there is an unexpected expense you have to take on new debt right away. Consolidate debt only if it actually can help you to save in your interest rate and monthly payment.

What’s a reasonable amount of time for the progress to be visible?

Here in month one, we become aware. In month 2, you’ll see your first measurable changes due to cuts in the subscription and tracking. If you’re sticking with it, you’ll see your first savings of $100-$200 in month three. Most individuals are able to save enough to have their first Emergency Fund by month 6. The math: $10 a week equals $520 per year and $20 a week equals $1,040. From there, it’s increasingly viable to make small employer contributions to a retirement plan. Any little bit added up can make a difference.