How Long Does It Take to Improve Your Credit Score?

How Long Does It Take to Improve Credit Score? (The Honest Answer)

If you searched “how long does it take to improve credit score,” you want a number, not a philosophy. Here it is: somewhere between 30 days and 24 months. Where you land inside that range depends on three things where your score is right now, what specific negative items are sitting on your report, and whether you stay consistent long enough for the changes to register with the bureaus.

Someone with a 700 score and high credit card balances can see meaningful score improvement in 30 to 60 days. Someone rebuilding from a 450 with active collections and a year of late payments is looking at 12 to 24 months of structured, disciplined work. These are genuinely different situations. They need genuinely different plans.

What tripped me up for a long time and what I see trip up most people is expecting the credit rebuilding timeline to move in a straight line upward. It does not. You can do the right things for months and see almost nothing happen. Then you cross a threshold and your score jumps 40 or 50 points in a single reporting cycle. Understanding that tipping point structure is the only thing that keeps most people from quitting two weeks before their biggest improvement would have arrived.

Why Timeline Varies: The 3 Key Factors

Your starting score is the first variable. In the 700 to 750 credit score range, you are already in reasonable shape. The adjustments are usually small, and they register quickly. In the 400 to 550 range, there is real damage on the report damage that has to be addressed before any building can begin.

The second variable is the type of negative items you are dealing with. High credit utilization is the most fixable factor. It can shift within a single billing cycle. Late payments, collections accounts, and charge-offs are a different matter. They require specific strategies and they do not respond to general good behavior.

The third variable is one most people underestimate. Consistency. One missed payment during the rebuilding process can push your improvement timeline back by 6 to 12 months which is why avoiding overspending that leads to missed payments is critical. Not a small setback. A real, measurable one.

Quick Reference: Timeline by Starting Score

Based on your starting point, here is what you are actually looking at.

700 to 750: You are close. Reduce utilization, keep payments clean, and expect real movement in 30 to 90 days.

650 to 700: Give it 3 to 6 months. Consistent payments and lower utilization will get you there.

550 to 650: Plan for 6 to 12 months. This takes secured cards and strategic debt paydown, not just good habits going forward.

400 to 550: This is the bottom of the 300-850 range severe damage territory. Recovery is a 12 to 24 month process. It is absolutely possible, but only with a specific, structured approach.

If your score sits at 630 and you are trying to qualify for better loan programs, you need to reach 750. That is a 120-point gap. Depending on what is specifically on your report, that is typically 12 to 18 months of focused, consistent action.

What Determines How Fast Your Credit Score Improves

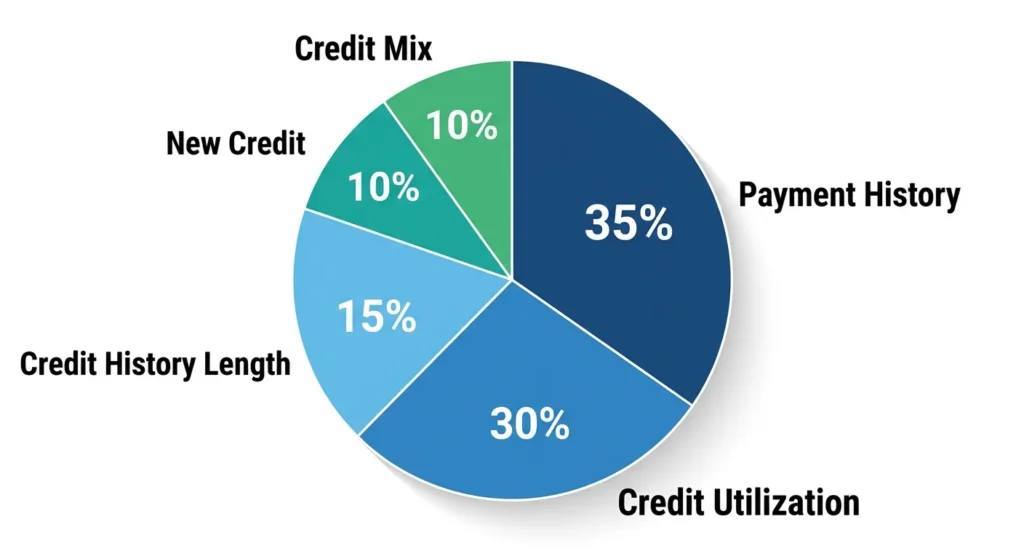

Understanding the five FICO score factors changes how you prioritize the next few months of your rebuilding plan. Each factor responds on a completely different timeline which means working on the wrong ones first wastes time you could be using on the ones that actually move.

According to FICO, payment history makes up 35% of your score. Credit utilization ratio accounts for 30%. Length of credit history is 15%. New credit applications carry 10%. Credit mix rounds it out at the remaining 10%.

Some of these respond within weeks. Others take years to shift. Knowing which is which stops you from investing effort in factors that cannot change fast while ignoring the ones that can move the needle right now.

Payment History: Why This 35% Controls Your Timeline

At 35% of your total FICO score, the 35% payment history weight is the single factor that controls everything else. You can have clean utilization, a solid credit mix, and aged accounts and still watch your score stagnate if payment history is inconsistent.

One late payment can set your improvement timeline back by 6 to 12 months. I have seen this happen to people who were otherwise doing everything right. Lenders look at payment history before anything else because it tells them the one thing they actually care about: do you pay what you owe, reliably, every time?

The fix is mechanical and takes five minutes to set up. Autopay on every bill credit cards, utilities, phone, subscriptions, anything that reports to a bureau. This only works reliably when you have a budget that supports consistent autopay without overdraft risk. Once autopay is running safely, the 35% payment history factor starts compounding in your favor without any further effort on your part.

Credit Utilization: The 30% Factor That Changes Monthly

Credit utilization ratio is the one factor in your FICO score that can actually move fast. Payment history takes years to rebuild. Account age takes years to grow. But utilization? Pay down a balance before your statement closes and the scoring model records a different number next month.

The formula is direct. If your card limit is $10,000 and your balance is $3,000, your credit utilization ratio is 30%.

Every article you have read on this topic probably told you to stay under 30%. That is the floor the point where the scoring model stops penalizing you. The real acceleration happens well below it. I cover the exact threshold later in this article, and it changes what your improvement timeline looks like.

The Factors You Can’t Speed Up (And Why That Is OK)

Credit history length requires time and nothing else. There is no tactic that makes your accounts age faster. Hard inquiries from credit applications stay on your report for 2 years regardless of what you do. These are not problems to solve. They are timelines to wait out.

So stop putting energy into what you cannot move. Payment history and credit utilization ratio together control 65% of your score. Get those two right and let the rest follow on their own schedule.

The credit account age factor does have one specific threshold worth planning around. When your average account age crosses the 2-year mark, lenders stop treating you as a new borrower and start reading your history as a track record. That shift often produces a meaningful jump in your score sometimes 20 to 40 points without any new action required. I cover this in its own section below.

Can You Improve Credit Score in 30 Days? (What Is Actually Possible)

You can improve your credit score in 30 days. But I am not going to pretend it works for every situation, because it does not.

In 30 days, you can realistically see movement if errors are sitting on your report right now, if your utilization is at 70 or 80 percent and you have the cash to pay it down, or if someone with excellent credit is willing to add you as an authorized user on a well-managed account. I came across a case in a credit community where someone climbed from 546 to 720 in roughly 4 months. They called every debt holder directly, negotiated balances down where possible, and kept utilization under 30% across every card without a single exception. That is not average. But it happened because every available lever was pulled simultaneously.

Five things can genuinely produce results within 30 days. Here is what they are.

Quick Win #1: Dispute Credit Report Errors (Immediate to 30 Days)

A Federal Trade Commission study found approximately 26% of credit reports contain at least one error significant enough to affect creditworthiness. These errors can include duplicate accounts, closed accounts still showing as open, wrong balances, or accounts that were never yours to begin with.

Pull your reports from all three bureaus and work through every line. Anything inaccurate is worth disputing. The bureau has 30 days to investigate. If they cannot verify the item, it has to come off. One removed negative mark can shift your score more than months of clean payment behavior which is exactly why this is always my first stop when reviewing a damaged file.

Quick Win #2: Pay Down High Utilization Cards (Reports Next Statement)

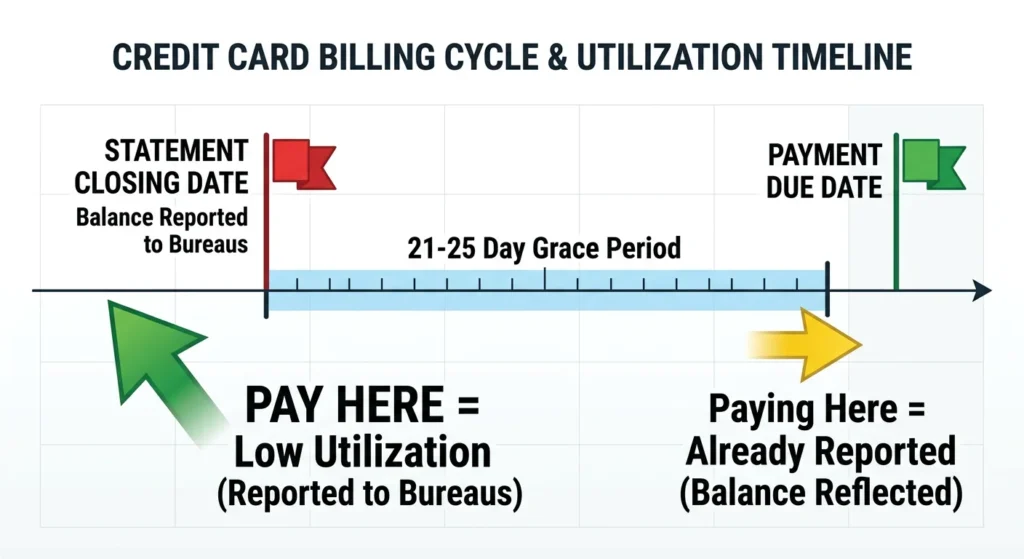

Here is a timing detail that catches most people off guard. Your credit card balance gets reported to the credit bureaus on your statement closing date not your payment due date. These are two completely different dates, usually separated by 21 to 25 days.

If you carry a high balance through the statement closing date and then pay it off before the due date, the bureaus already recorded the high number. To show lower utilization on your next credit report, the balance has to come down before the statement closes.

A card sitting at 80 or 90% utilization that drops below 30% shows up in your score the following month. That change costs nothing except timing if you already have the funds available though some readers may benefit from finding extra cash quickly to execute this paydown before the next statement closes. Most people are paying the same amount just on the wrong date.

Quick Win #3: Become an Authorized User (Instant History Addition)

Getting added as an authorized user on a family member or close friend’s credit card can pull years of clean payment history onto your report almost immediately. Not your payment history. Theirs. And the credit bureaus count it exactly the same.

The account needs to be the right kind. A score above 800 on the primary holder, several years of history, and low utilization. If the card is maxed out or has late payments, being added hurts rather than helps so verify the account before agreeing.

This is the fastest legitimate path I know to add real credit history length to a thin or damaged file. But it requires complete trust in both directions. If you run up the balance on that card, the primary holder’s credit takes the hit alongside yours.

Quick Win #4: Request a Credit Limit Increase (No Hard Inquiry Method)

Call your credit card issuer and request a credit limit increase. Before they proceed, ask specifically: will you perform a hard pull for this request? If yes, decline. If no, proceed.

The math on this is clean. If your balance is $1,750 on a $4,500 limit, your utilization is 39%. Push the limit to $7,500 and that same balance drops to 23% without touching the actual debt. No additional payment, no hard inquiry. Just a better ratio showing on your report.

Quick Win #5: Add Rent Payments to Your Credit Report (Retroactive History)

If you pay rent every month and it is not on your credit report, you are getting zero credit for a payment you make reliably every single month. Services like RentReporters.com can go back up to 24 months and add that entire history to your credit file within days.

For someone with a thin credit file who has been a reliable renter for two or three years, this can be the single largest one-time boost available. Two years of on-time payments appearing in one go is not a small thing. The bureaus treat it the same as any other verified payment history.

What Will Not Work in 30 Days (Honest Expectations)

Late payments, collections, charge-offs, and bankruptcies cannot be cleared in 30 days unless they are sitting on your report as errors. Full stop.

These negative items act as anchors. Even when every other signal in your file is clean, they cap how high your score can climb until they are properly resolved or age off the report naturally. Anyone promising a 30-day fix for actual late payments or real collections is telling you what you want to hear. The rest of this article shows you how to handle these over the realistic timeline they actually require.

How Long to Improve Credit Score by 200 Points (6 to 18 Month Realistic Plan)

How to improve credit score by 200 points is a real question with a specific answer. It typically means starting below 650 and working consistently for 6 to 18 months. The exact timeline depends on what specific damage is on your report and how aggressively you execute the plan.

The 546 to 720 case I mentioned earlier is real but it required calling debt holders directly, negotiating balances down, and maintaining sub-30% utilization across every card without exception. Most people cannot clear that many levers simultaneously. Plan for 6 months minimum, 18 months if the negative items are significant.

Here is the month-by-month breakdown.

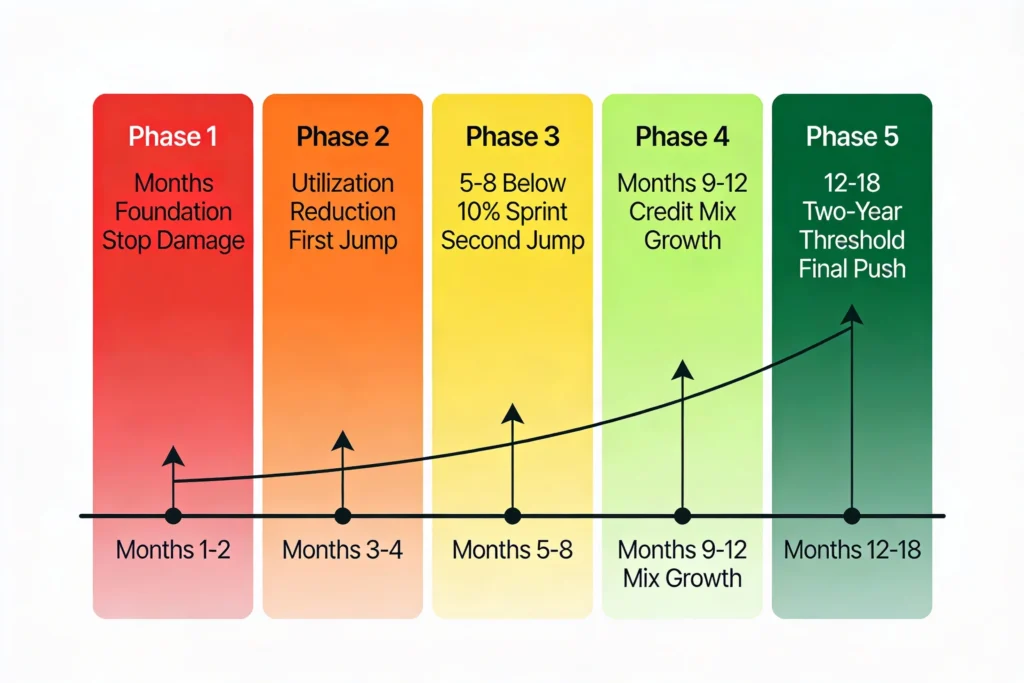

Months 1 to 2: Foundation Phase (Stop the Bleeding)

The first two months are about stopping new damage before building anything. Set up autopay for every single bill. Stop sending credit applications. Pull your reports from all three bureaus and go through every line mark every inaccuracy, every account you do not recognize, and every balance that does not match your records.

Build a simple list of everything you owe and to whom. You need the full picture before you can prioritize which is why creating a realistic budget is essential during this foundation phase, especially when working with limited income. To dispute credit report errors at this stage, file directly with the bureau that shows the inaccurate item. It is free and takes about 20 minutes online. Payment history runs 35% of your FICO score, and every payment matters starting right now.

Months 3 to 4: Aggressive Utilization Reduction (First Major Jump)

Months 3 and 4 are about one thing: driving down credit utilization ratio. Every extra dollar whether from reducing monthly expenses or other income sources goes toward the cards closest to their limit first. A card at 90% causes more scoring damage than a card at 20%, so start there.

The goal by the end of month 4 is every card under 30% utilization. When that happens, the scoring model stops docking you on that factor. Most people see their first real jump here 30 to 50 points in a single reporting cycle. That is the algorithm responding to a changed data signal, not a reward for effort. Keep going.

Months 5 to 8: The 10% Utilization Sprint (Second Major Jump)

Once every card clears the 30% threshold, keep pushing. Drop your total credit utilization ratio below 10%. This is where scores actually accelerate not at 30%, not at 25%, but in single digits.

Most financial content stops at the 30% advice. That is not wrong. It is just incomplete. When the scoring model sees 6 or 7% across your accounts, it reads that profile very differently than 28%. The jump from sub-30% to sub-10% is typically where the second major improvement in your score happens, and it catches most people off guard because no one told them 30% was only halfway there.

Months 9 to 12: Building Credit Mix and History (Sustained Growth)

If every account on your report is a credit card, months 9 through 12 are the right window to add a small installment loan. A credit builder loan from a local credit union is the cleanest option — you make monthly payments into a dedicated savings account, receive the money back at term end, and the lender reports every payment to the bureaus throughout.

Keep credit utilization low. Let accounts age. Do not open anything new unless there is a specific, strategic reason. By month 12, you have 12 months of clean payment history stacking on your file, utilization under control, and a credit mix that now shows both revolving credit and installment credit. That combination shifts your profile meaningfully without adding real financial risk.

Months 12 to 18: Approaching the 2-Year Threshold (Final Push)

As accounts cross the 2-year mark, lenders stop categorizing you as a new borrower and start reading your file as a track record. The scoring model reflects that. People who have been doing everything right and wondering why the score has stalled often hit this threshold and watch 20 to 40 points appear without making any new changes.

Do not open new accounts during this window. Every new account resets your average age down. Let the existing ones age. If you have been consistent through the earlier phases, the 200-point improvement you were working toward tends to arrive somewhere in this stretch often right around the 2-year threshold itself.

How to Fix a 400 to 550 Credit Score (12 to 24 Month Timeline)

A score between 400 and 550 means there is real damage on your report. Not just high utilization or a couple of missed payments actual negative items that need specific handling before improvement is even possible. Credit repair at this level is not about optimizing a decent file. It is about stopping active damage and then rebuilding from the ground up.

That said, it is not permanent. Scores between 300 and 525 will be declined by most traditional lenders, and between 525 and 600 you might qualify but at very high interest rates with lenders scrutinizing your debt to income ratio closely alongside the score. If you’re in this range while also managing financial crisis, prioritize immediate stability before aggressive credit rebuilding.

Getting above 650 opens real doors, and above 700 the lending landscape looks completely different. I have seen people rebuild from 430 to above 700 in under two years. It takes longer and requires a more specific strategy, but the path exists.

Why You Are Starting at 400 to 550 (Identify Your Damage)

Before any strategy makes sense, you need to know exactly what is causing the damage. Common causes at this score range include missed or late payments stacking up over time, accounts sitting in collections, charge-offs where the lender wrote off the debt entirely, utilization near or at the limit across multiple cards, too many loan applications in a short window, and too many unsecured loans taken on at once without the income to manage them.

Go through every line of your credit reports and categorize each negative item by type. Collections require a different response than charge-offs. Late payments require a different strategy than hard inquiries. Knowing which type of damage you have determines which steps come first.

The “Settled” Debt Trap (Fix This First or It Never Improves)

Most people do not know this distinction, and it costs them years of credit rebuilding progress. A debt marked “settled” and a debt marked “paid in full” are not remotely the same thing in the eyes of the scoring model or any lender reviewing your file manually.

If you previously settled a loan for 50 cents on the dollar, that “settled” status acts as a ceiling on your score improvement regardless of what else you do right. The fix is specific: contact the original lender, pay the remaining balance, and get a No Objection Certificate in writing on their letterhead confirming they will update the status to “paid in full.” Until that status changes in the bureau data, the ceiling does not lift.

How to Raise Credit Score With Collections on Your Report

Here is where the standard advice goes wrong. Paying a collections account does not necessarily improve your credit score. In most scoring models, a paid collection and an unpaid collection carry nearly identical weight. You lose the money and gain almost nothing on your score.

The right approach is to negotiate before any payment goes out. Contact the collection agency and offer payment in exchange for complete removal of the account from your report — a pay-for-delete agreement. Get that agreement in writing, signed, on their letterhead, before transferring a single dollar.

Also know this: making even a partial payment on an old collection restarts the statute of limitations clock. A collection account that is 5 or 6 years old and approaching natural removal from your report can get a fresh seven-year lifespan from one payment. If you do not have a deletion agreement in hand, do not pay old collections. Sometimes waiting is the smarter play.

Secured Credit Cards: Your Guaranteed Approval Rebuilding Tool

When your score is in the 400 to 550 range, most traditional cards will decline you. A secured credit card solves the access problem. You deposit money with the bank as collateral typically $200 to $500 and they issue a card with that deposit as your limit. Use it regularly, pay it off monthly, and the activity reports to the credit bureaus identically to any regular credit card.

The bureaus record secured card activity the same as traditional card activity. A secured card showing 24 months of on-time payments looks identical to a standard card showing the same history. That is the point. It is your re-entry point into the credit reporting system when the standard door is closed.

The 6-Month Secured Card Strategy (Months 1 to 6)

Get the secured card and route regular monthly expenses through it groceries, a phone bill, a subscription you were paying anyway. This works best when you’re following a simple budgeting framework that ensures you never charge more than you can pay off monthly. Keep the balance well below 30% of the limit at all times. Pay the full statement balance every single month, before the due date.

Six months of consistent, clean use builds the payment history foundation your score needs more than anything else at this stage. Miss a month, pay late, or max the card out and those months of work take real damage. The secured card only produces results when treated with the same seriousness as any other financial obligation you cannot afford to skip.

Small Installment Loan Method (Months 7 to 12)

After six solid months on the secured card, add a small installment loan. A credit builder loan from a local credit union is the cleanest option. Some people take a small consumer loan for an appliance or electronics purchase, pay it over 12 to 24 months, and that history demonstrates responsible repayment behavior to every future lender who pulls the file.

What this does is add credit mix diversification. Right now the report probably shows only revolving credit cards. Adding an installment loan means the scoring model sees two different types of financial obligation being managed well. That combination shifts the credit profile in a way that cards alone cannot.

Realistic Timeline from 400 to 650 and Beyond

By month 6, expect roughly 40 to 60 points of improvement if the plan has been followed consistently. By month 12, you should be approaching or crossing the 600 mark. By months 18 to 24, with the settled debts addressed and collections handled properly, a score above 700 is realistic for most people starting in this range.

The timeline depends entirely on what is on your report and whether you add any new damage during the process. Every late payment during the rebuilding phase resets part of what you have built. The plan works when nothing new goes wrong while the positive history stacks up.

The 30% vs 10% Utilization Rule (Why Timeline Accelerates at 10%)

Every credit article you have ever read told you to keep your credit utilization ratio below 30%. That advice is not wrong. But it is the minimum acceptable threshold, not the target and understanding how much credit card debt is sustainable helps you see why aiming for single-digit utilization produces consistently better results. Understanding that difference is exactly what separates people who plateau from people who see consistent improvement.

The 30% threshold keeps you out of the penalty zone. The real scoring acceleration happens when you drop below 10%. People with 800-plus scores typically maintain utilization between 1 and 6 percent. Not 28 percent. Not 20 percent. Single digits. The scoring model does not treat 29% and 7% the same way, and most credit content never mentions that.

Why 30% Is the Minimum, Not the Goal

Think of 30% as clearing the floor, not hitting the ceiling. Once you cross below it, the scoring model stops docking you on that factor. But it does not start rewarding you aggressively until you go considerably lower.

For a fast credit rebuilding timeline, 30% is a checkpoint, not a destination. Getting from sub-30% to sub-10% is a separate phase with its own distinct scoring impact often larger than the drop from over 30% down to below 30%.

The Statement Date vs Due Date Strategy

Most people pay by the due date, set the reminder on their phone, and assume the utilization on their report reflects that payment. It usually does not.

The balance that gets reported to the credit bureaus is the balance on your statement closing date — typically 21 to 25 days before your payment due date. These are two separate dates. If you carry a high balance through the statement closing date and then pay before the due date, the bureaus already recorded the high number.

Pay before the statement closes. Not before the due date. Before the statement closes. That one timing adjustment is the difference between 38 percent utilization showing on your credit report and 8 percent showing without spending any additional money. Same total payments. Different reported number.

How to Calculate Your Current Utilization (And Where You Need to Be)

The math takes about 30 seconds. Add up all your credit card balances. Add up all your credit card limits. Divide the first number by the second and multiply by 100.

If your combined balances are $3,800 against combined limits of $18,500, your credit utilization ratio is about 21 percent. Decent. To hit 10 percent, you need total balances under $1,850. To reach 6 percent where the strongest scores tend to live you are looking at roughly $1,100 or less across all cards.

Run those numbers right now. The gap between where you are and where you need to be is the exact paydown amount your improvement timeline is waiting on.

The 2-Year Age Threshold Nobody Tells You About

Nobody talks about this one clearly, and it causes more frustration than almost anything else in credit rebuilding. You can maintain perfect payment history for 14 months, keep utilization under 10%, and still find your score stuck below a ceiling you cannot explain.

The reason is usually credit account age. When your average account age crosses the 2-year mark, your creditworthiness shifts in how lenders read it. Before that point, your history is recent good behavior. After it, the same behavior becomes a verified track record the same principle that applies to building genuine financial stability over time. The scoring model responds to that distinction with a genuine jump same actions, different weight assigned to them.

Why Your Score Stays Stuck Under 2 Years (Even With Perfect Payment History)

Zero late payments, low utilization, solid credit mix — and still the score refuses to climb past a certain point. In my experience, credit history length is the most common explanation when everything else checks out.

Lenders need to see sustained behavior, not just recent behavior. Twelve months of clean payment history tells them you have been doing the right things lately. Twenty-four months tells them this is your actual financial pattern. The algorithm treats those two situations very differently, and the shift is often sharp rather than gradual.

The Delayed Impact of Closing Old Accounts

Here is the part that blindsides people years after the fact. Closing an old credit card does not hurt your credit account age right away. The closed account stays on your report for 6 to 10 years and continues counting toward your average credit history length during that entire window.

But when it eventually falls off, your average age drops. Maybe by a year. Maybe by several years, depending on the account. You will not feel it the day you close the card. You will feel it five or seven years later when your score takes an unexplained hit during an otherwise clean period. Keep the old card open. The inconvenience of managing an account you rarely use is small compared to the age protection you are holding onto.

How to Preserve Account Age Without Annual Fees

If the old card charges an annual fee you do not want to pay, call the issuer and ask to downgrade to a no-fee version. Most major issuers offer this option. The account number stays the same. The full history stays intact. The annual fee disappears. You protect the credit account age without paying for it.

Once it is a no-fee card, run a small charge through it every two or three months — a coffee, a small recurring subscription, anything under $20. Pay it immediately. Some issuers will close accounts they flag as completely inactive, so minimal periodic use prevents auto-closure and keeps everything working in your favor.

How to Improve Credit Mix Without Taking On Bad Debt

Credit mix is 10% of your FICO score. It is not the biggest factor on the list, but at the right stage in your rebuilding process, adding the correct type of account can push your score past a threshold it has been stuck at for months.

The important qualifier is “the correct type.” People take on high-interest personal loans specifically to add installment credit to their profile and end up paying more in interest over two years than the score improvement was worth. If those payments stretch the budget and create late payments, the credit mix addition does far more damage than good. Adding credit mix diversification only makes sense when it can be done at low or zero financial risk.

What Credit Mix Actually Means (Revolving vs Installment)

Credit mix refers to having different types of credit represented on your report. Revolving credit covers cards and lines of credit where the balance changes month to month based on spending. Installment credit covers loans with fixed monthly payments — car loans, student loans, personal loans, credit builder loans.

Having both types shows the scoring model you can handle two different kinds of financial obligation. If your report shows only revolving credit, you are missing 10% of your score by default. One qualifying installment account changes that without requiring significant new debt.

Credit Builder Loans: The Safe Way to Add Installment History

A credit builder loan from a credit union is the safest path to adding installment history without real debt exposure. Here is exactly how it works: you make fixed monthly payments into a dedicated savings account. At the end of the loan term, you receive the money you paid in—making this an effective strategy for building savings even on limited income while simultaneously improving your credit. The lender reports every single payment to the credit bureaus throughout the term.

You are paying yourself into savings while building a verified installment payment history. The only way this hurts your score is if you miss payments. If you can afford the monthly amount and can commit to every payment on time, there is almost no scenario where a credit builder loan works against you.

The Final Payment Boost (Tactical Timing for Maximum Impact)

Most people assume the scoring benefit of an installment loan is front-loaded — that opening the account is the win. It is not. The biggest scoring boost from an installment loan comes at the end, when you are in the final 10 to 20 percent of the balance remaining.

Paying off that final stretch signals completion of a financial commitment. The scoring model treats that completion as a distinct event, and the response is usually a noticeable jump. If you have multiple installment loans and want to time a score improvement before a mortgage application or another major financial event, pay off the one closest to being done first. The completion itself is the scoring event.

What NOT to Do for Credit Mix

Do not take a high-interest personal loan to add installment credit to your profile. Do not open a car loan you cannot comfortably afford just to tick a credit mix box. The interest payments over 24 months will cost more than any score improvement is worth — and if those payments strain your budget, the late payments that follow will do far more damage than the credit mix addition does good.

Here is something worth sitting with: a perfect 850 FICO score means someone spent years paying interest to lenders. The score is a byproduct of financial behavior, not a goal in itself. Chase the behavior — pay reliably, manage credit utilization, let accounts age. The score follows financial behavior automatically. Working the other direction, chasing the number by taking on debt to earn points, is backward.

Mistakes That Reset Your Timeline (What Slows Everything Down)

Strategy only works if you are not quietly reversing it at the same time. Every one of the mistakes below can reset months of progress without you realizing it and most of them feel completely reasonable in the moment, which is exactly why they keep happening.

Mistake #1: Closing Old Credit Cards to Clean Up Your Report

This mistake feels like responsible financial housekeeping. You paid off the card, you do not use it, so closing it seems logical. But it does two damaging things simultaneously: it shrinks your total available credit, which pushes your utilization ratio higher on every remaining card, and it puts a future expiration date on the credit history length that account was contributing.

Keep it open. Run one small purchase through it every few months. Pay it off the same day. The age of that account and the limit it provides are both actively working in your favor even when the card sits untouched.

Mistake #2: Only Paying the Minimum on Credit Cards

Paying only the minimum due does two things against your score. It keeps your credit utilization ratio high because the balance barely moves after the minimum comes out. And it signals to lenders reviewing your file that your finances are being managed at the narrowest possible margin. If you’re stuck in this cycle, aggressive debt paydown strategies can help you break free and start paying full statement balances.

Pay the full statement balance not the minimum, not half, the full amount showing on the statement between the statement closing date and the due date. When you do this consistently, you carry no interest charges and report the lowest possible utilization to the bureaus every single month. That is the behavior that builds a strong credit profile over time.

Mistake #3: Applying for Multiple Credit Cards or Loans at Once

Every credit application triggers a hard inquiry. One hard inquiry causes a small, temporary drop. Three in a 30-day window cause a more significant drop — and signal to every future lender that you recently shopped for credit in multiple places and may have been turned down more than once.

Each rejection is visible in your file. Future lenders see it. Apply for one product at a time, and only when you have specific reason to expect approval based on your current score and profile. Scattershot applications are one of the fastest ways to damage a score you have spent months building.

Mistake #4: Becoming a Guarantor for Someone Else

When someone asks you to co-sign or guarantee their loan, understand what you are actually agreeing to. If they miss payments, those missed payments appear on your credit report. If they default entirely, you are legally responsible for the full remaining balance — and your credit score takes the same hit as if you defaulted yourself.

Never sign as guarantor unless you are completely prepared to make every payment on that loan personally. Not because you plan to pay it — but because you may have no choice.

Mistake #5: Settling Debts for Partial Payment Without Strategy

Settling a debt for less than the full amount leaves a “settled” mark on your report that nearly every lender reads as evidence you agreed to repay an obligation and then negotiated your way out of part of it. That distinction carries real negative weight.

Before any debt payment goes out, negotiate in writing for either a complete pay-for-delete removal or a status update to “paid in full” in exchange for the remaining balance. Get that agreement on the lender’s letterhead, signed, before a single dollar is transferred. Verbal agreements in debt negotiation do not hold.

Mistake #6: Making Partial Payment on Old Collections

A collection account approaching the 6 to 7 year mark is close to falling off your report naturally. When it falls off, it stops affecting your credit score entirely. Making even a partial payment restarts the statute of limitations clock that old collections account gets a fresh seven years on your report.

Do not pay old collections without a written deletion agreement in hand. If you cannot get one, waiting it out is often the better play. The debt may still be legally collectible, but once it drops off your report, its impact on your score disappears. Your legal obligation and your credit score impact are separate things. Know the difference.

Track Your Progress: How to Monitor Score Improvement

Credit monitoring gets confusing fast once you realize your score looks different depending on where you check it. Before you start reading numbers and reacting to every shift, here are the three things most people misunderstand about how the scoring system actually works.

Soft Checks vs Hard Checks (Why Checking Your Own Score Is Safe)

There is a persistent myth that checking your own credit score will lower it. It will not. When you check your own score through a monitoring app, a bureau website, or your bank’s credit monitoring tool, it generates what is called a soft inquiry. Soft inquiries are invisible to lenders and have zero effect on your score.

Hard inquiries are different. Those happen when a lender accesses your credit report because you applied for something a card, a loan, a mortgage. Each one causes a small, temporary score drop and stays on your report for two years. A credit freeze can block hard inquiries entirely when you are not actively applying, which protects your score during periods when you want to pause applications.

Check your own score as often as you want. But think carefully before authorizing anyone else to pull it.

FICO vs VantageScore (Why Your Scores Look Different)

Credit Karma and similar free tools show you a VantageScore. Most lenders use a FICO Score when making actual credit decisions. These two models analyze the same credit file but weight the factors differently — so you might see a 720 on your monitoring app and a 675 when a mortgage lender pulls your report.

Neither number is inaccurate for its own model. But they serve different lenders and different decisions. When you are preparing to apply for a mortgage or major loan, pull your actual FICO score from myfico.com. That is the number the lender is likely to see, and knowing it in advance prevents surprises.

There is also a version difference within FICO itself worth knowing. FICO 8 is the most common for general credit decisions. Mortgage lenders typically use older FICO versions — FICO 2, 4, or 5 — which weight factors slightly differently. FICO 9 treats medical collections more favorably than FICO 8. Knowing which version applies to your specific situation can affect your strategy.

The Three Credit Bureaus (And Why You Need to Check All of Them)

Equifax, Experian, and TransUnion are the three major credit bureaus, and each one operates completely independently. Not every lender reports to all three. Not every error at one bureau exists at the others. This means your scores across the three can look noticeably different from each other.

Pull reports from all three at AnnualCreditReport.com — free, official, no subscription required. Review each one separately. An error on your Equifax report requires a dispute filed directly with Equifax. The same item on TransUnion needs a separate dispute there. One clean report and two damaged ones still means two damaged reports that lenders can see.

How Often Scores Actually Update (Managing Your Expectations)

Your credit score typically updates once a month, when creditors send their payment and balance reports to the bureaus. The timing varies by lender — some report right after the statement closes, others at the end of the month.

Actions you take today generally appear in your score 30 to 60 days later. A paydown made this week may not show in your score for three to four weeks, then it takes another reporting cycle for the updated score to reflect it. That lag is the most common reason people give up on a strategy that is actually working. They make the right moves, see no change in the following two weeks, and assume nothing is happening. Most of the time it is happening. It just has not reported yet.

Frequently Asked Questions About Credit Score Improvement Timeline

How long after paying off debt does my credit score improve?

Typically 30 to 60 days after the creditor reports the zero balance to the bureaus. That is the standard reporting lag. One thing to watch: if the loan you paid off was your only installment account, your credit mix just narrowed. You might see a small, temporary dip before the score recovers. It usually corrects itself within one or two billing cycles as the positive payment completion signal outweighs the reduced credit mix.

Why did my credit score drop after I paid off my credit card?

If you closed it: Your total available credit decreased (raising utilization on other cards) and your average account age may have dropped. If you didn’t close it: Check if it was incorrectly reported as “closed by grantor” instead of remaining open or “closed by consumer” dispute if wrong.

Will paying off collections immediately improve my credit score?

No. Paid and unpaid collections hurt your score equally. Negotiate pay-for-delete before paying, or for settled debts, pay the remainder and get written proof of “paid in full” status change.

Can I build good credit without going into debt?

Yes. Become an authorized user, use rent reporting services, and get a secured credit card that you pay in full monthly (no interest = no debt).

How long does negative information stay on my credit report?

Late payments, collections, charge-offs: 7 years. Chapter 7 bankruptcy: 10 years. Hard inquiries: 2 years (meaningful impact for 12 months only).

Should I use a credit repair company or fix my credit myself?

DIY is free and equally effective. Use a company only if you have complex issues (multiple collections, bankruptcy, settled debts) and no time. Choose NFCC-accredited agencies. Avoid guarantees of specific score increases.

How do I raise my credit score if I have no credit history?

Become an authorized user + use rent reporting + get a secured credit card. Combined approach can reach 700+ in 6-12 months.

What credit score do I need to buy a house?

FHA: 620 minimum. Conventional: 640-680. Best rates: 750+. No score? Some lenders offer manual underwriting with alternative documentation.

Does checking my own credit score hurt my score?

No. Self-checks are soft inquiries (zero impact). Only lender pulls (hard inquiries) when you apply for credit cause small temporary drops.

The Bottom Line: Your Credit Score Timeline Roadmap

So how long does it take to improve your credit score? The honest range is 30 days to 24 months. Where you land depends on your starting point, what specific negative items are on your report, and whether you stay consistent long enough for the changes to register.

I have watched people go from 546 to 720 in four months when every available lever was pulled simultaneously. I have also watched people spend 14 months doing most things correctly while a single misunderstood factor — high utilization over the statement date, or an approaching 2-year account age threshold — quietly kept the ceiling in place. The difference between those two outcomes almost always comes down to knowing which specific lever matters at which specific stage.

This article gives you that sequence. Now it is a matter of starting.

Quick Timeline Reference Guide

Here is the full picture compressed into one place.

30 days: Fix errors on your report, pay down high utilization before the next statement date, become an authorized user, or request a credit limit increase. Realistic gain: 10 to 100 points depending on your specific situation.

3 to 6 months: Consistent on-time payments, sustained low credit utilization ratio, and completed dispute resolution can produce 50 to 150 points of improvement for moderate credit issues.

6 to 12 months: Serious rebuilding after significant damage using secured credit cards and installment loans can generate 100 to 200 points of improvement.

12 to 24 months: Recovery from severe damage collections, charge-offs, settled debts — combined with the 2-year account age threshold crossing, can produce 200-plus points of total improvement for people starting in the lowest range.

Your Next Step Today

Do not wait for the perfect moment. Here is what to do before you close this article.

Pull your reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Find your starting score and mark every negative item by type. Match your specific situation to the plan in this article — high utilization, thin credit history, settled debts, active collections, or some combination.

Pick the single most impactful action available right now. Set up autopay today. File one dispute. Pay down the most maxed-out card before your next statement date. Call your card issuer about a credit limit increase with no hard pull. One action today beats a perfect plan that starts next week.