Budgeting for Teens: How to Take Control of Your Money in 2026

This is a story that keeps coming up more often than is generally believed. A mother of a teenage son contacted us about the issue she was struggling with, that her son had a job, was making real money, and was “all broke” days after every paycheck.

Never once in a while. Every single time. One day he approached her and asked, “Why is my money just going away?One day he went to her and asked her, “Why does my money just go away?

I’ve been working with youth for years to help them understand money, and the same story I hear over and over again.

I got hit by that question as it’s not just his story. It’s the tale of nearly every teenager who begins to make money without a strategy.

This side is not a willpower thing, no one speaks about it. A planning issue.

Algebra and essay writing is taught to you for years in school. No one explains to you about budgeting for teens, basic money management, or how it all works in real life. It should be your own responsibility to figure it out, and most teens wait years to get it right the first time.

The budgeting process for a high school student isn’t as difficult as it may appear. Just a system is required. After the first one, the world changes. Financial responsibility isn’t something your parents preach about anymore, it’s something you feel like you own.

Why Every Teen Who Gets Paid Ends Up Broke

What a budget actually means (no, it doesn’t mean you can’t spend!)

I believe many teens don’t want to budget because they imagine what it would look like. They picture themselves denying themselves all kinds of fun, meticulously counting every single penny, and essentially being broke when they aren’t. That’s not what a budget is.

A budget is a spending plan. It’s a blueprint of your money! Before you spend any of that dollar, you make the decision of how it will be spent; you are the one in control rather than asking yourself where it went at the end of the month.

This is the easiest way to explain it: communicate with your cash as to where it’s going, and it’ll follow.

The Teen Budgeting Rules That Actually Fit Your Life

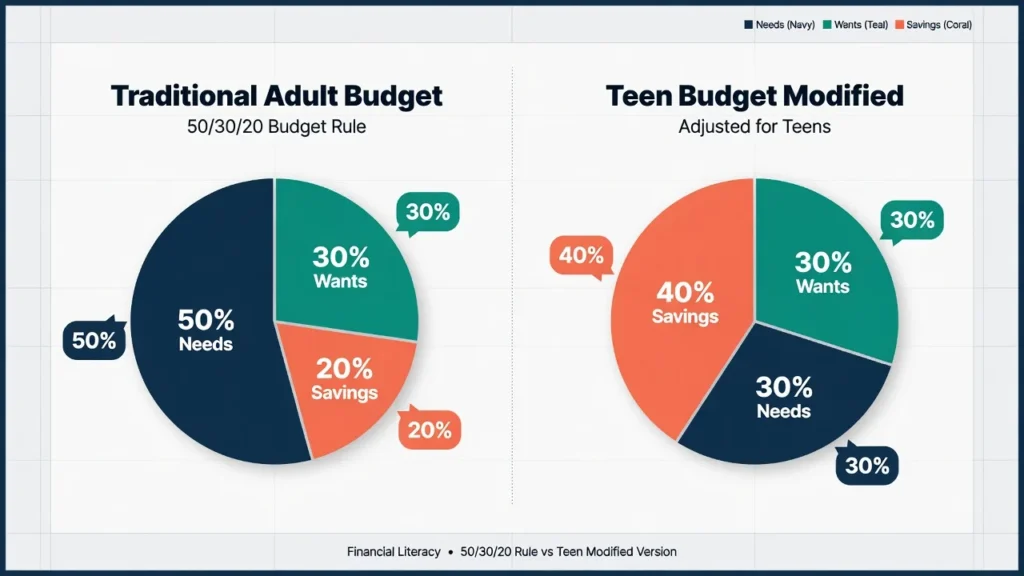

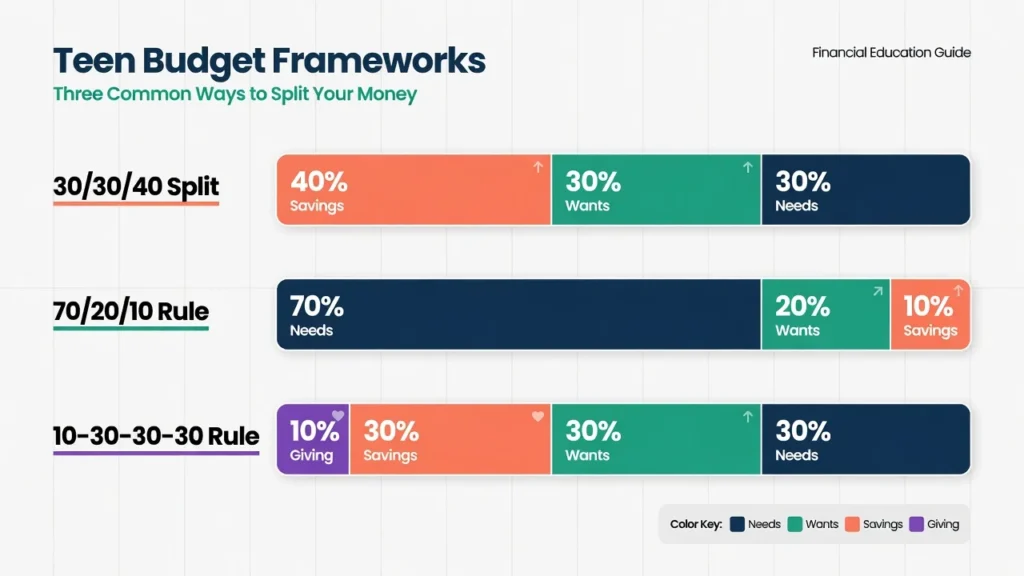

Most teen budget guides give you the 50/30/20 rule, and leave. I want to do something different, because that rule doesn’t necessarily always fit the way a teenager really lives.

The 50/30/20 rule was created with people in mind who have rent, utilities, groceries and car payments. If half of your income is spent on the necessities at 50% then you have 30% for fun and 20% for saving.

That math is for an individual who is living entirely alone. But as a teenager? You probably split the house and food costs with your parents, as well as a lot of other big bills. Your true needs are significantly less than half (50%) of what they are assuming. That’s where you can truly make money benefit you.

The 50/30/20 Rule and Why You Might Want to Tweak It

The 50/30/20 rule is a budget guideline that allocates 50% of your income to your essentials, 30% to your wants, and 20% to your savings. 50% covers needs fixed expenses such as a phone bill, gas or bus fare. Thirty percent is for wants such as entertainment, clothing and outing. 20% is saved.

If you’re an adult with complete financial responsibility, that works well and is tried and tested. The needs category is typically rather small for teens because their parents deal with the large expenses. This means that you can save more when it comes to your savings percentage.

Many teens would do better to allocate 30 percent towards the things they actually need, 30 percent towards the things they want and 40 percent into savings.

Two Other Frameworks Worth Knowing: 70/20/10 and 10-30-30-30

If you are planning to incorporate the act of giving into your budget, the 70/20/10 rule is easier to follow. Give 10% in charity or to a cause you support and save 20% and spend 70%.

The 10-30-30-30 rule goes further. 10% to giving, 30% to saving, 30% to needs, 30% to wants. One of the more aggressive in terms of saving, but realistic if parents are responsible for all major expenses for teens.

Which budgeting approach is right for you depends on the situation. Here are the three frameworks to know and you choose which one resonates with your life. So long as more is saved than is spent and saving is the most important thing, there is no wrong answer.

How to Make a Budget for Teens: A Real Step-by-Step Guide

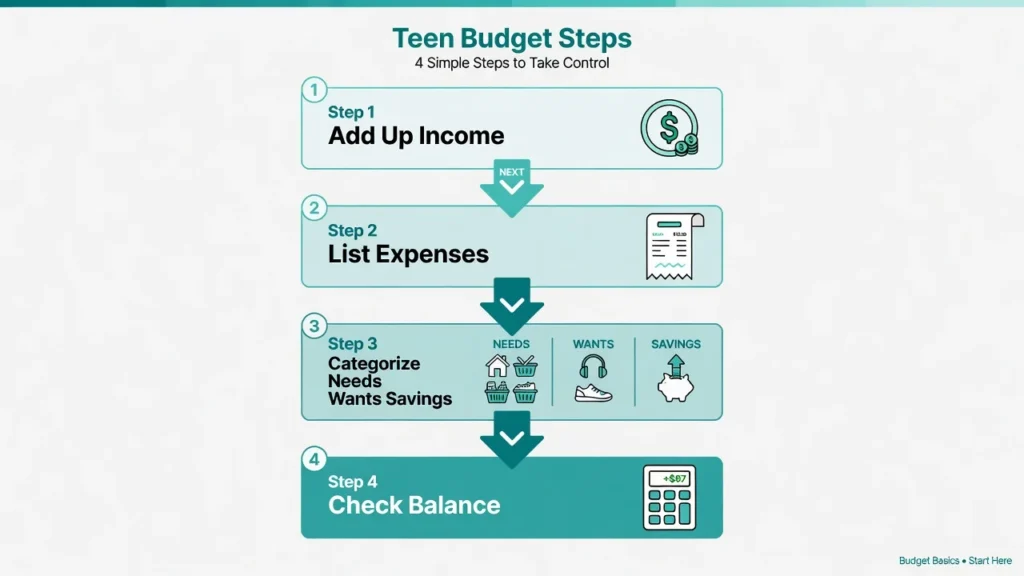

Making a teen’s budget doesn’t need to be complicated or have any finance expertise. You will need 4 bits of information and approximately 20 minutes. Before you spend one dollar you will know where the money will go.

If you want to understand the full budgeting process before diving in, that foundation makes these steps even easier. This is the difference between teens that are growing their savings and teens who are asking themselves, where did my money go this month?

Step 1: Add Up Every Dollar Coming In

Begin by making a list of all the sources of income that you have every month. That means your allowance, your part-time job, babysitting, mowing lawns or any other regular income.

Quick note about gifts: birthday money and holiday cash can be helpful when it is present, but can’t be counted on to create a budget. Only budget what you can afford.

If Alex works part-time and earns $400 per month and receives a $50 allowance each month, for example, then you can calculate the total amount he receives each month. He earns a total of $450.00 per month. This is the number with which he works.

Step 2: Write Down What You Actually Spend Money On

Now make a list of all expenses, regardless of how insignificant they may seem. Write it all down – gas, a streaming subscription, lunch money, phone bill, clothes, etc.

A second thing that you need to do is to categorize the fixed expenses and the variable expenses. Fixed expenses are costs that do not vary from month to month such as a phone bill. Variable expenses fluctuate, such as the amount spent on clothes or entertainment on a monthly basis. Understanding what is what can be useful when it comes to a reduction in expenditure later on.

Step 3: Divide Everything Into Needs, Wants, and Savings

After you have your list of income and expenses, divide your expenses into three categories: Needs, Wants, and Saving.

Needs are things you really need in order to get work done gas to get to work, a phone bill, bus fare. Wants are items that are selected – also referred to as discretionary spending. When your current phone works just fine, an upgrade for a new phone is a want. A want is to go out to dinner with friends.

New gaming system is a need.

Saving is not a choice but a requirement. Treat it as a need, not a left-over. This is a money-skill that is essential to learn at any age, and it’s worth making a habit of learning early. These three categories — needs, wants, and savings are among the key components of a successful budget that determine whether your plan actually works long-term.

Step 4: Does Your Budget Balance? Run This Check

After you enter all of your income and expense categories, add all your expenses together and subtract that from your total income. The answer is right there in the title.

If it is positive, then take the remainder and deposit it into a savings account. If it’s zero, your budget is balanced. If it’s negative, you are spending more than you take in and that means that you’re going to go into the month in debt.

Failure does not have to be a negative number. It’s feedback. It instructs you to cut away precisely the wants you have until they are all gone. This is the one step which most budgeting guides don’t mention, but it is the one step that helps everything else work.

Set Financial Goals for Teens That Actually Keep You Motivated

The one thing I have seen that most teens give up on budgeting in a few weeks is that they have no idea of what they are saving for. It doesn’t make sense to save money without a plan, particularly when everyone around you is spending.

The fix is to give your savings a name.

Divide your savings objectives into two parts. Short term goals are what you want within the next few months, such as new shoes, a concert with friends, gaming system or a new phone. Long-term goals are more distant, like saving for a car, saving for college or saving for your first apartment.

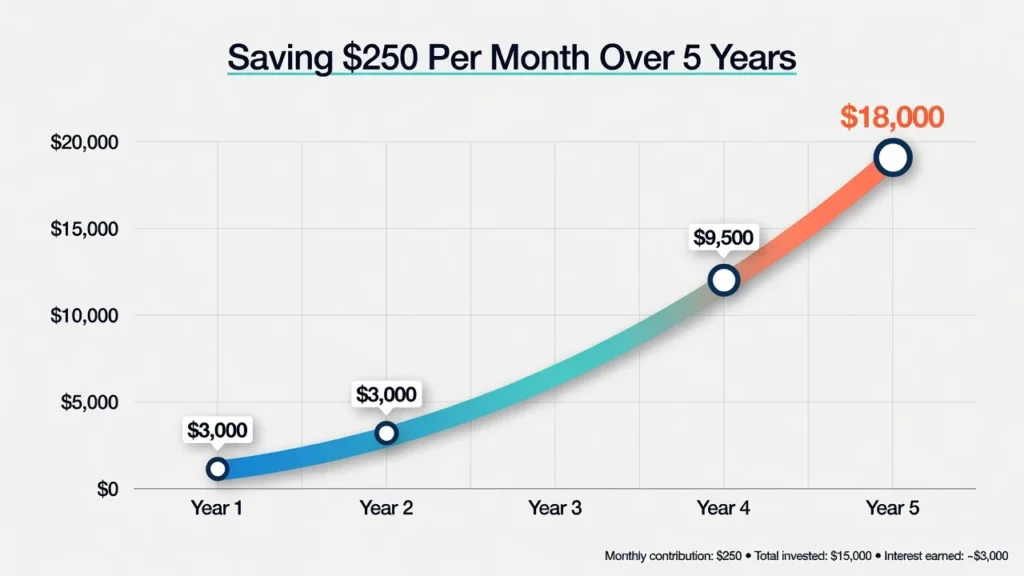

The numbers are more motivating than most people realise. The result is that you’ll have $3,000 in your pocket at the end of the year by saving $250 per month. If you had that same $250 per month put in an investment account that has a reasonable rate of return, you could have $18,000 in that account in 5 years with compound interest. These are true results of real teens who begin early and are consistent.

Get your money targets proper. Display them in a place you visit each day. Make them your excuse to not overspend the budget when it’s tempting.

Track Every Dollar : Even the Small Ones That Don’t Feel Like Much

Let’s get straight to the point: If you’re not regularly monitoring your spending, you’re budgeting in theory only! The best budget on paper can be the most well-laid plans if they’re not tracked.

Once you begin tracking, it happens very rapidly. The numbers in black and white reveal that you’ve spent more on snacks and coffee this week than you have on savings. What is not a judgment, but information: And information is what enables you to make better decisions the next time.

Keeping track of expenses doesn’t mean that you’re not allowed to spend money. It simply makes your spending transparent. Spending you can see is spending you can control.

Three Ways to Track (Pick the One You’ll Actually Use)

The most effective tracking is simply the one that you will use on a regular basis. All of the following options below are viable it’s just a matter of choosing one and going with it.

A physical notebook is the easiest option. Take it with you, record each item as it is bought and add up at the end of the day. No batteries required, no app needed and a handwritten countdown makes the numbers more real.

A Google Sheets or Excel spreadsheet will work well for visualizing patterns over time. Simple formulas can be set up to automatically total totals and the categories can be color coded to show the flow of money. Budget planner for teens is available in Google Sheets, and you can find and customize it in just a few minutes!

A mobile budgeting app will help you with most of the organizing, and many are free. Read on about the best ones, in the tools section.

Regardless of your option, stick to it for a minimum of 30 days prior to changing. It’s easier to see what different categories of spending are after a month of actual data.

Saving Money as a Teenager: The Habits That Actually Work

It’s never too early to start saving your money as a teenager will make it a lot easier for you in the years to come. The sooner the money is invested, the longer it can grow.

Saving is more than just saving what is left. A system must be put in place. If you feel like your income is too small to save meaningfully, these strategies for how to save money on a limited income might change your perspective. These are the habits which actually work.

Pay yourself first. As soon as money arrives, save an amount in addition to what you spent on bills. When you save what’s left at the end of the month, there will be no money at the end of the month. Save first, spend second, if you need to save some money.

If possible, automate it. If the bank permits automatic transfer, create one for the day after your pay is deposited. You’re putting $20 in your savings account, and it’s not a dime, it’s a dollar.

Apply the one week wait. If it is something that is not a must-have and the cost is greater than $30, delay the purchase for one week. In most cases, the urge subsides. If it doesn’t, you know that it wasn’t an impulse and was indeed a true need.

Why a High-Yield Savings Account Beats a Regular Savings Account

The vast majority of teenagers who do open a savings account open the most basic account possible. That’s understandable. However, there is a better solution that not a lot of people know about when they are still young.

The interest rate for a regular bank savings account is 0.01% per year. That translates to literally 10 cents a year with a $1,000 balance. Not ten dollars. Ten cents.

The online bank I have a high-yield savings account at now pays about 3% to 5% per year. With that same $1,000 balance, that’s $30 – $50 a year for no change in behaviour unless you select the appropriate account.

Most banks require the account holder to be 18 years old or older, so if you are under 18 you will need a parent’s assistance in opening an HYSA. There are several banks that provide joint accounts just for teens. It only takes one conversation and one visit to a bank website to get it set up, and after that, your money begins to earn real interest, and not 10 cents a year.

Keep in mind that the HYSA rates may differ from one bank to another and can change over time always double check the latest HYSA rates before opening an account.

The Emergency Fund Every Teen Actually Needs

I know the idea of an emergency fund is adult advice. But hear me out. There is no need to have rent and grocery money in an emergency fund. That is your parents’ job. However, what occurs when the display on your phone becomes cracked? Your car needs a repair.

You are about to go for a job interview next week and you need to get new shoes for it. These are genuine crises that don’t seem like emergencies until they become one and if they do, you lose a large portion of your savings or get stuck on a credit card.

The quantity doesn’t need to be substantial. If the only regular expenses of a teen are gas and car insurance, then the total expense for those two items might be as little as three to six months at under $1,000. Build up an emergency fund of $200. Then $500. Continue to save for it gradually along with the rest of your goal. The idea is, it is there when you need it.

The Mindset Trick That Changes How You See Your Money

It’s the one thing I wish someone had told me earlier and it’s not something I see in the articles I read about teen money.

Most of the people who have difficulties of budgeting look at their bank account balance, and consider that number as the total amount that they have to spend. The brain sees $400 to be spent when the balance reads $400. Now $400 doesn’t seem like much when $120 of it is already being used on your phone bill, $80 on gas, and $60 for savings.

The remedy is a mere mental adjustment. Think of each budget category as a separate bank account. If your food budget is $80 this month, then you have $80 to spend on food, not $400!

Consider it like this. What if you had 5 different envelops for 5 types of spending? You wouldn’t take the money out of the phone bill envelope to buy pizza when you can tell it’s for telephony!

This one mental change makes the difference in the effectiveness of a budget. Successful budgeters are not more self-controlled than others. They simply begin to view their account balance as nonexistent and begin to think of each dollar as used.

The Money Mistakes Most Teens Make (and How to Avoid Them)

I wish to present the patterns that I have observed and heard from real people. The monetary blunders that repeatedly happen to teens that are bad at budgeting and what to do in their place.

Spending before saving. The biggest error is to consider savings as the balance of money available after spending on wants. Save first, spend later, and there will seldom be a “later” because you’re running out of money. Pay your own first, all the time.

Making unbalanced budget. When spending more than you are earning, you don’t have a spending plan, you have a debt plan. Use the balance check from Step 4 at all times. In a negative number, cut down the number until it is zero.

Thinking “I don’t make enough money to budget.” This one is upside down. When you have limited funds, a budget is more crucial. Even $50 a month has a destination when you give your money a plan — and that’s exactly what budgeting on a low income looks like in practice. Budgeting isn’t about how much you make. It’s about the use of resources.

Forgetting irregular expenses. But there are other expenses that seem out of the ordinary to most people because they weren’t planned for, such as annual fees, back-to-school shopping, holiday gifts, car registration, etc. Calculate annual costs and save $ amount monthly. When the bill is paid, cash is already in hand.

Learning too late. I remember the mother from the beginning of this article’s story saying that. It wasn’t until she was in the middle of her 30s that she realized how to budget properly! She was because she didn’t want her own teenage son to be stuck without these skills for decades like she was. This is where you’re right now. In fact that’s a different story.

Peer Pressure Is a Real Budget Killer : Here’s How to Handle It

Peer pressure and money is an equation that most money-management guides for teenagers don’t cover, but it’s one of the most difficult aspects to juggle in everyday budgeting.

Your friends are hungry for food. They would like to be taken to concerts, go to the expensive thing, buy the new thing. Refusing is not easy, particularly if you don’t want to explain that you are keeping a track of how much you are spending.

The first thing to keep in mind is that you don’t have to share all your budget with anybody. You can just state that you’re saving for particular thing and recommend a less expensive alternative. “Saving for a car want to come over instead?” doesn’t indulge in the money aspect of the situation.

The second is to plan a category called “social spending. If you allow yourself to spend $40 on outing each month, you won’t have to feel guilty about saying “yes” to plans it’s already planned.

Budgeting Worksheets for Teens and the Best Apps to Try

The most sophisticated budgeting tool isn’t the best. It’s the one that you’ll open every day, and that’s the one that you have to use every day. I have divided your options into three categories from free to dedicated apps so you can choose what is suitable for you at this moment.

Free, hassle-free: It’s as easy as using your phone’s Notes app today. Open a note, list your income, list your expenses, subtract one from the other. That’s a budget. Do not assume that you don’t start because of a lack of tools.

Google Sheets templates to make a budget planner for teens: Google Sheets offers a variety of budget planner for teens templates that you can find and edit in mere minutes. A typical budget sheet for teens will have a section for income, a section for expenses, and a section for a balance. A quick Google Sheets search for teen budget template will turn up a number of templates that you can use for free.

Budgeting apps: There are a number of budgeting apps that have great free options for the teen to get started.

Apps Worth Downloading Today

Here are the best teen budgeting apps to check out now:

YNAB (You Need A Budget) is ideal for serious budgeters who are looking to allocate EVERY dollar to a category. Has a learning curve, but develops financial discipline over time. It comes with a price, but the student frequently can get a complimentary first year.

Every Dollar is best suited for those who prefer a clean, simple, zero-based budget that is free for a basic budget.

The teen-specific apps Greenlight and FamZoo have built-in parent visibility features. Both feature a teen spending card and spending limits. If you’re looking for an account for your teen with some structure, these are great options.

If it’s a little too much for apps right now, notes or Google Sheets are the next best thing. Begin with simple and then make them more difficult as they build.

If you’ve decided to get a teen checking account, find a checking account that has a low or no monthly fee, a low minimum balance, and easy mobile access.

The Old-School Method That Still Works: Kakeibo

If you don’t like apps and spreadsheets, here is a Japanese budgeting technique called Kakeibo you should know. Kakeibo is a mindful spending journal.

Every month you record 4 questions: How much money do I have? What amount of money would I like to save? So how much am I spending? How can I improve?

Then you handwrite everything you purchase into your records, in four classifications: survival, optional, culture and extra. Writing is the act that makes people aware, tapping a card never does!

Researchers found that those who write on a Kakeibo journal save an impressively higher amount than those who don’t. It’s because writing down what you buy before or after you make it brings the experience of purchasing into their consciousness and relates it to their actual feelings about the purchase.

For Parents: How to Teach Budgeting Without a Power Struggle

If you are a parent reading this on behalf of your teenager, I want to give you a more constructive list than rules to enforce.

This quote from the mother in the beginning of this article stuck with me. Her son wasn’t a student. He wanted a system and a “why.He wanted a system and a “why”. The aim is not conformity but understanding.

Lead by example. Don’t hide the fact that you budget, do a budget, and talk about it freely with your teen; they will learn it as a normal adult behavior, not as a punishment.

Make financial responsibility the connection and not only chores. Chores are a way to learn work ethic. Give allowance based on budgeting – learn money management. These are various skills.

Open a savings account with your student. Allow them to select the bank. Allow them to create the account. Ownership of the process equals investment in the product.

Celebrate progress openly. If your teen reaches his or her target savings amount, no matter how small, reward it. It’s the sense of accomplishment that comes when they achieve a goal that motivates them to set the next one.

The One Conversation That Changes Everything (Show Them the Real Numbers)

One of the most important things a parent can do is to share financial information with their teen. Let them know the realities of how much things cost to live rent or mortgage, utilities, groceries, insurance, and the actual amount they put out for a home each month.

The real numbers in the home change when it comes to a teen. Saving for independence no longer seems like a distant concept, it feels like it’s needed. This type of financial education isn’t taught in school, and it’s one of the most important things a parent can provide.

You’re not looking to have a teen who is simply going through the motions until they go away to college; rather a teen who’s actually learning to manage his money.

Check and Adjust: Your Budget Should Grow as You Do

Your initial budget is not going to be flawless. No problem, it is normal and it is a process of this sort.

It’s not about making your budget ideal and sticking with it for life. The aim is to develop the habit of reading it, learning from it and developing it month by month.

Conduct monthly budget check! Every month, ask yourself some simple questions: Did my income increase or decrease? Did any expenses come up that I didn’t plan for? Am I on track to save my target amount? Whenever I find myself wondering, “Where did I blow my money? Was it worth it?

These questions don’t take long. However, they give a static plan a life of its own that can really be incorporated into your actual life.

Adjust without guilt. You don’t have to punish yourself if you spent more than you need to on food this month. You’ll have to figure out how to either raise or lower that category next month. Your budget is for your benefit, not theirs.

One of the keys to developing good saving plans and practices is to realize that discipline is not a lack of flexibility. It’s about getting back on track following each deviation.

Finances are created monthly, one month at a time. What you learn about money during your teens will compound, like interest does. The more you follow a budget each month, the more months your future self will thank you for.

Ready to Go Further? What Comes After Budgeting

After you’ve developed a solid budgeting habit and you have money in your savings account, it’s logical to take your money and place it somewhere productive.After you have a solid budgeting habit and have money in your savings account, it makes sense to take your money and give it to something productive, which means investing.

Budgeting results in a surplus. That surplus can go to work when invested. The two of these habits, performed in the early years, are the basis of long term financial independence.

Compound interest is the interest that is accrued on interest, over time. The more you leave your money invested, the more it can multiply itself. The difference is hundreds of thousands of dollars in retirement benefits just due to the extra years compounded, starting at 16 rather than 25.

For example, if you’re a teenager who invests $100 a month at 16 and a 35-year-old who invests $500 a month, the 35-year-old has more money at retirement age just because he’s invested in his account longer.

The simplest and safest bet is the index fund. An index fund is made up of hundreds of companies, rather than just one, making it less risky than betting on a single company.

They’re not spectacular returns, but they’re steady returns, and they can really add up over the long haul, decades. Under 18, you can begin investing through a custodial account – an investment account opened by a parent or guardian.

Budgeting is directly linked to investing. A surplus is generated with budgeting. That excess is put to work in investing. This is something that most adults would have liked to know before they turned 25. Now is your opportunity to get a head start.

The first step to financial independence is the proper budgeting of teens habits – a basic spending plan and the dedication to review it monthly. From there, all of the valuable things build.

Frequently Asked Questions

Which budgeting plan do teens use?

The smartest approach to budgeting for teens is the one that they will actually use. The 50/30/20 rule can be a good guideline for most teens, though with the modulations that most living expenses are taken care of by parents which leaves 30/30/40. This means, 30% of the money goes to the needs, 30% goes to the wants, and 40% of the money goes straight to savings. If you do want to give, then the 10-30-30-30 rule is also effective.

What is the best way to budget money with a small allowance?

Simply giving the child $50 a month can be budgeted. Using a 30/30/40 split: $15 goes to needs, $15 to wants, and $20 to savings. Most will see it as a small income, and that’s $240 saved over a year. The quantity isn’t as important as the habit.

If a 16 year old has $600 per month to spend, how does he divide it up?

One good way to spend $600 a month is the 10-30-30-30 rule: $60 for giving or charity, $300 for savings, $300 for teen needs (such as gas), and $300 for wants. If you like the 50/30/20 rule, allocate $120 to your savings, $300 to your needs, and $180 to your wants. Either way, the real benefit that the teens have is that the housing and food costs are usually paid which allows you to save a larger percentage of your income than most adults. Make the best of that advantage.

If teens go over their budget one month, what should they do?

Do not start with 0. Consider if the category exceeded, if it was a single incident or if budget needs to be adjusted, and proceed. It takes about 10 minutes per month to review the budget, and it can be done once to avoid overspending.

Why is it that teens always run out of money?

The most frequent is a lack of planning when spending. One teen asked his mother, “Well, why am I always short of cash after we get my paycheck?” One answer: “If you don’t have a plan for your money, you can’t control it. Budgeting for teens is a strategy that will address this by assigning a purpose to each dollar before it leaves your wallet.

What is an appropriate age for teens to begin budgeting?

When they get any money at all – even a small amount of pocket change. The more the habit is established the more natural it will seem when real financial responsibilities come along. A 13-year-old with a $20/week budget is developing the same kind of thinking as a 30-year-old with a $3000/month budget.

What is a zero-based budget for teens?

A zero-based budget is when all income is allocated to a category until it is completely utilized. Income minus all spending categories, including savings, is equal to zero. No tasks are undone. This approach works well because it has to be intentional spending and not mindless.

Should teens have an emergency savings account?

Yes, but a small one, specifically designed based on their costs. Most teenagers need a $200 to $500 emergency fund to pay for unexpected expenses such as a cracked phone screen, an unanticipated school expense, or an immediate transportation need. First, build up the emergency fund, and then make plans for long-term savings.