How to Be Debt-Free in 6 Months: The Honest Answer

But before I guide you through the exact plan for, I want to give you something most debt guides skip: the reality of whether this timeline is actually realistic for you.

While it is possible to learn how to be debt-free in 6 months, it ultimately depends on the numbers. I have seen this strategy work for people with $5,000 in credit card debt and even for those carrying $18,000 spread across four different accounts. However, success requires the right debt-to-income ratio, a solid repayment strategy, and more discipline than most guides prepare you for.

The #1 reason people quit around month three is that they start the process without understanding their actual financial numbers. Most people searching for want a neat and simple plan, but the first and most important question is this: can your current financial situation realistically support becoming debt-free within six months?

The Simple Math: Calculate Your Required Monthly Payment

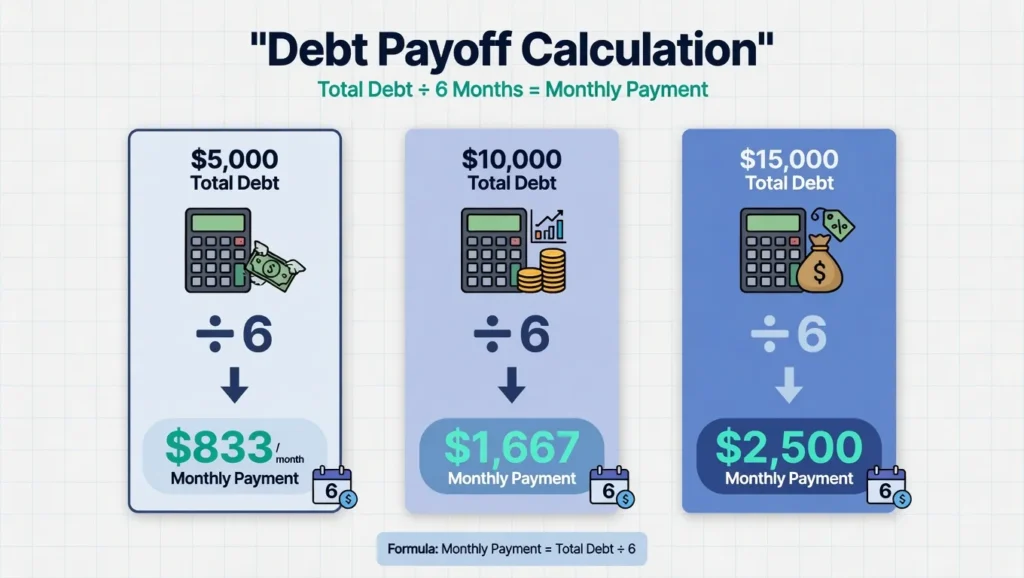

This is the quickest reality check you can get for your timeline. Divide your total debt by six. This is the total amount of money you need to pay each month to pay off the debt over 180 months without paying any interest.

Total Debt ÷ 6 = Required Monthly Payment

- $5,000 in debt → $833/month

- $10,000 in debt → $1,667/month

- $15,000 in debt → $2,500/month

Note: If the debts have high interest rates (20% and above), the monthly interest will be added to the required monthly payment, so that the real monthly payment will be a little bit more. Allow for an additional 5-10% margin to account for on track.

It’s a figure that’s fairly modest: at about $6,000 to $8,000, it’s about what the average American household with credit card debt has on its books, according to the Federal Reserve’s latest consumer finance release and a figure that’s attainable with disciplined efforts over a span of 6 months.

Next, deduct your fixed unavoidable expenses from your after-tax income (rent, utilities, food, and transportation). The money left over is your extra cash – the money that you have to apply to your debt payments other than the amount you have to pay as minimum. If the amount of debt you’re facing each month is more than 40% of your take-home pay, then the 6-month timeframe won’t be feasible without a significant increase in your earnings.

Which is exactly why income acceleration is as important as cutting expenses and I talk about some strategies later in this guide.

Warning Signs This Timeline Won’t Work for You

The aggressive 6-month debt payoff is best suited for those with debt that’s not too much to handle within their income stream, and a surplus in their monthly cash flow. A 6-month plan will break when your debt load is right up to your annual income and you’ll know by month two.

But this is not an end of the road situation. It means that your realistic goal is 12 months and that’s still a life-changing result. The important thing is to run the numbers beforehand and not try and burn out after figuring it out.

Let’s get the red flags straight, because they tell me (and them, you and me) when 6 months is not the right period at this time:

- If you’re having trouble with minimum payments

- you’re not alone.If you’re having trouble paying off your minimum payments, you’re not the only one.

- You are not employed or income is inconsistent

- There isn’t a realistic way for you to make more money soon

- Your debt to income ratio has very little left over after paying for basic expenses

If you have 2 or more of these apply to you, then plan for 12 months. It’s a very real accomplishment to pay off in a year and that’s a far better idea than ditching a 6-month plan after 3 months. There’s no such thing as a bad plan unless you abandon it.

Your Complete Debt Assessment: The Starting Point Most People Skip

For most people, this step is postponed for weeks. I get why, because if you don’t know how much you don’t think it’s that much worse than you think. However, avoiding comes at a price of time and money every day one waits.

When you sit down and write the entire number, there’s a change. No longer is debt a vague fear but a real problem with a real solution. I have helped individuals who are carrying $2,300 in credit card debt and people who have $47,000 in debt on eight credit cards. Before you begin, it’s important to assess whether your credit card debt is manageable for your income level. The one thing I’ve seen over and over again is that successful people are not not the highest earners. They make this first step without flinching.

Take a seat with your bank statements, credit card bills, student loan portals and any other account that you need to pay a balance on. Write down all credit cards, personal loans, medical payments, student loans, etc. that you owe, as well as any money that you owe formally to family members.

To ensure you have all the information, visit AnnualCreditReport.com to get your complete credit report for free. It will display all of the accounts that you have, including those that you may not know about or have forgotten about, as well as the ones that are in collections. This also allows you to detect any of your mistakes that might be bringing down your credit score without any reason.

Your Debt Assessment Template

Make a basic table in a journal or spreadsheet with these five columns. This document will be used throughout the next six months and will be referred to repeatedly.

| Creditor | Total Balance | Interest Rate (APR) | Minimum Payment | Payoff Date at Minimum |

|---|---|---|---|---|

| Credit Card A | $3,200 | 24% | $64 | 7+ years |

| Credit Card B | $1,800 | 19% | $36 | 5+ years |

| Personal Loan | $4,000 | 11% | $120 | 3.5 years |

| Medical Bill | $600 | 0% | $25 | 2 years |

| Student Loan | $5,400 | 6% | $58 | 10 years |

This will be your most important financial document for the next 6 months once finished. Do not skip it.

The Mindset Shift That Actually Creates Change

The vast majority of debt doesn’t come all at once. It’s built little by little over months or years, a few hundred here, a few hundred there, a few hundred there. That pattern is important to grasp, but it’s not something you’re doing wrong, it’s just a fact: If you made small decisions, you can make small decisions to take down the debt.

Taking ownership of the result is what is really moving people from stuck to moving. Not guilt. Not shame. The quiet determination you make that it’s you who’s going to solve this – it is.

How to Become Debt Free in 1 Year: The 12-Month Alternative Plan

If the numbers you calculated in the previous exercise indicate that you can’t afford the 6 month payment, then don’t consider the 12 month option you’re making the smart choice! It’s not settling if you pick a timeline that you can adhere to. It is strategy.

If you can reduce your monthly payment by half by learning how to become debt free in 1 year, you need to pay exactly half as much. With just this one tweak, the plan is viable for those with moderate incomes or balances on their debt more than $10,000. It also gives it enough breathing room that you are not susceptible to burning out and quitting the plan halfway through.

Adjusting the Numbers: What 12 Months Changes

Let’s take a closer look at the details for a $10,000 amount:

| Timeline | Required Monthly Payment | Total Interest Paid (est. 20% APR) |

|---|---|---|

| 6 months | $1,667 | ~$580 |

| 12 months | $833 | ~$1,100 |

| 24 months | $417 | ~$2,300 |

| Minimum only (~$200) | $200 | $10,000+ over many years |

Do some math on these columns and choose the ride that your income can afford. Taking the twelfth month plan to the end is better than giving up on the six-month plan at the third month.

Proven Strategies for Debt Repayment: Snowball vs Avalanche

You’ve got your numbers and your timeline now, so you need to select how you’re going to pay them back. Financial gurus have been debating two approaches to paying off debt that have worked for years and both of them work. It’s not math that is the difference; it’s psychology. I’ll explain both so you can select the one that really works for you and not the one that looks great on a spreadsheet.

The one rule: choose one and stick with it for 90-days minimum. Note: If you have student loans, you may want to explore specific strategies to pay off student loans faster alongside these general methods.

Changing tactics halfway through will bring the momentum back into the plan.

The Debt Snowball Method: Smallest Balance First

The debt snowball technique was popularized by Dave Ramsey. List your debts by size, in order, not considering the interest rates. All additional dollars are applied to the smallest balance and the minimum balance applied to the remaining. Once it’s paid off you roll the entire balance of that debt into the following debt, and your monthly payment increases for each debt you pay off.

Most people do this because it doesn’t have to do with math. It’s all in the mind. It’s possible to enjoy real success early in the process by paying off one debt even a small one and this is what helps get you that much closer to making it through the tougher parts.

The study, published by the Journal of Marketing Research, revealed that individuals who started paying off debts based on the smallest first also paid them off faster, in no way mathematically, but rather because of the psychotronic side effect of seeing their debts diminish. Here’s the science of why the snowball method works.

Debt repayments are a behavior problem. The snowball method solves for that directly.

The Debt Avalanche Method: Highest Interest First

The debt avalanche method is the mathematically best way. You pay off debts in order of interest rate starting with the highest, and paying the minimal payment on all other debts. When the highest rate of debt is paid off, you proceed to the next debt.

The snowball pays more interest on the entire loan, and sometimes more than a hundred times as much depending on the balances and interest rates. The compromise: If the debt with the highest rate has a large balance to pay off, then the payout may be months in the making, and that’s not a motivator.

It’s effective with those who are more motivated by data and longer-term math than they are by short-term emotional wins.

During the debt free process, the snowball method will save more interest in the end, but this will only happen if you continue to use it long enough to make a difference.

The 5-Minute Call: How to Negotiate Lower Rates on Your Credit Cards

First, before you choose either type of payment, call your credit card companies and request a lower interest rate! Many don’t bother with this at all, but it does appear to work much more often than one could imagine particularly if you’ve been a customer for longer than a year and have a good payment history.

Here’s the script you can use: “I have been a customer of your company for several years and I want to remain with your company, however, I am thinking about transferring my balance to a lower rate card, is there something you can do to lower my rate?

By going from 24% to 18% on a $5,000 loan, you will save around $150 over six months, which is better for the principal. Just 5 minutes for free. Do this before beginning your payoff plan.

Should You Consider Debt Consolidation or Balance Transfers?

Debt consolidation and balance transfers can be ways to speed up debt repayment if they’re done correctly. Let’s take a look at each of them.

The idea behind a balance transfer is to transfer your high interest credit card debt to a new card that offers a 0% promotional rate on your balance, typically for a 12 to 21 month period. Paying the full balance before the promotion expires means that you will be able to save a lot of interest. If you don’t, many cards will charge retroactive interest on the full amount that was owed in the past and that can set you back months’ worth of progress in an instant.

Debt consolidation is combining several debts into a single loan at a lower interest rate, thus simplifying your payments. The risk is behavioral: After consolidation, the credit cards are paid off and many people begin using them again, leading to an increase in overall debt.

Both of these tools can help you to complement your payoff plan and NOT replace it. Both should never be used without first reading the complete terms in writing.

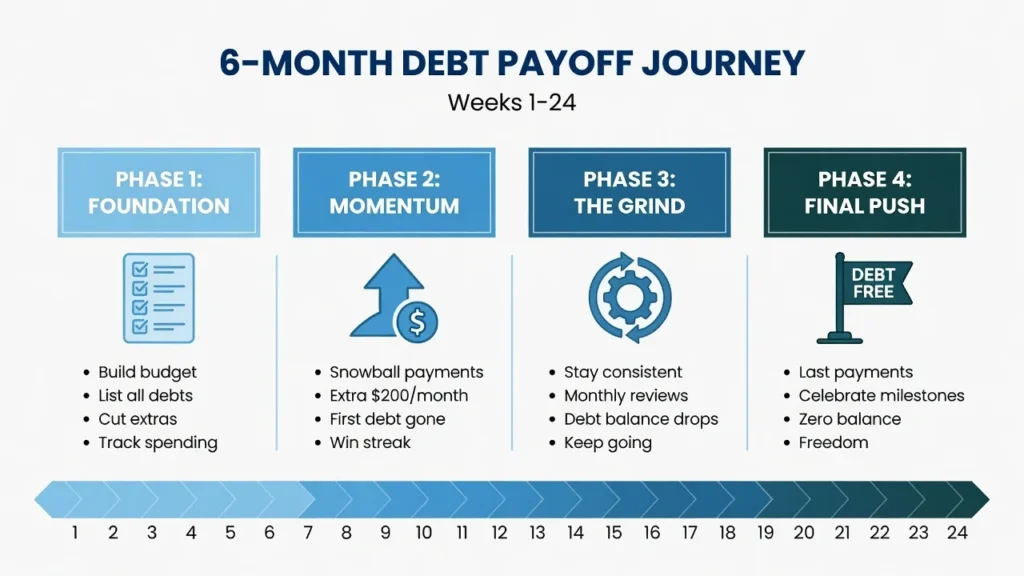

Your Month-by-Month Plan to Be Debt-Free in 6 Months (24-Week Breakdown)

Weeks 1 and 2: The Foundation Phase

The two weeks are dedicated to setting up, and not speed. The aim is not to make great strides it is to lay the foundations of the next 22 weeks.

Week 1 actions:

- Fill out your Debt Assessment Sheet

- Annually have your credit report at AnnualCreditReport.com.

- Call credit card companies to understand what they can do to lower rates.

- Make minimum payments on each debt automatically so that you do not miss any payments (and avoid using credit cards altogether during the debt snowball plan). New charges during a period of payments will make all payments frustrating and will cancel out all progress.

- Create a simple spreadsheet to organize all of your monthly payments following a structured budgeting process to see where each dollar is going each month.

- Open a separate savings account to store your $1,000 emergency fund in.

- Select the repayment plan (snowball or avalanche)

Week 2 actions:

- Start your own budget of only essentials.

- Eliminate all unnecessary paid publications, including magazines.Cut all un-needed paid publications, such as magazines.

- List items around your house to sell

- Look up 1 or 2 side hustle ideas that you can get started with in 7 days or less

Your financial goal for week 1 and 2: pay off your priority debt with your first $500 to $1,000. That money is from two sources: selling items around the house, or cancelling subscriptions or expenses that you can do right away.

Weeks 3 Through 8: The Momentum Phase

This is where the work begins to really become apparent. Your side hustle income is already in and your debt balances are really declining and if you took the snowball approach, you could actually pay off your first full debt while in this stage. That initial zero balance is a different kind of hit it feels real, math doesn’t.

The psychological challenge comes in at week 4 or 5. The novelty wears out, and the new thing is disciplining yourself when it’s not fun anymore. The fifth week, as far as I have seen, is the most perilous week in the whole plan. It’s been a while since the novelty wore off, the finish line is still far away and the exceptions sound reasonable. It’s half the battle to be prepared for that week.

This is the moment when everybody makes the first little concession – one restaurant meal, one unnecessary online purchase, one little extra they know they can afford – and it sneaks up on them all. Notice it early. Correct it immediately.

Weeks 9 Through 16: The Grind Phase

You’ve now paid off one or two smaller debts and your snowball payment is increasing. In the books, it is a good thing. This is also the time when mental fatigue can be the biggest obstacle to your plan fatigue that sets in over the course of months of strict discipline not math, not income, but mental fatigue.

You have been living on a tight budget and thought that was all that you could do for 2 months. It’s totally okay to “treat yourself. But at this stage, a $400 weekend vacation isn’t just a $400 expense, it is a month’s worth of debt reduction. This is the compromise to consider during the internal negotiation process.

What works in this phase:

- Review weekly every Sunday, do not skip

- When motivation wanes, refer back to the “Why” list.

- Pick one low dollar reward and reward your progress with it – It can be a nice meal at home, a free day off from your side hustle jobs etc.

- Reconnect with your accountability partner –

Weeks 17 Through 24: The Final Push

The finish line is now close! The hikes in debts are finally being addressed and those numbers you have been looking at for months are on the downward swing. The most difficult emotion to overcome now is more the process of not giving up it’s staying focused whilst your head is already celebrating.

Your life after your debt is done is planned out BEFORE it’s even finished. That the forward energy is good. Of course, be sure it doesn’t drag your foot off the accelerator in the final section. Hold down the keys until the final countdown is at zero. You will find one of the best feelings you will experience in the financial realm at that moment, when a balance that seemed to last forever is finally gone.

How to Pay Down Debt Fast: Income Acceleration Strategies

The majority of debt payoff programs devote 80% to reducing spending. If you want to pay down debt quickly on an aggressive 6-month timeframe, then you need to reverse that – making more money will make more difference than cutting more.

Costs cannot be decreased. The minimum amount of money you can spend is zero. But there’s no limit to the amount of income you can earn and for many of you, there are two or three additional income streams you can discover and work consistently – and it’s those that will keep you on track between what your regular budget can cover and what the 6 month plan calls for. With that extra income covering about 30-40% of the difference between what your regular budget can afford and what the 6-month time span will need, that means you have a closer chance of getting the gap filled.

There are two levers in any debt payoff plan; cut expenses, increase income. Income is the stronger of the two for a 6-month time frame.

The “10% Edge” Method: Monetize What You Already Know

The “10% Edge” approach is straightforward: No expert needed to make additional money. You simply have to know something, do something that is better than the average person who may be willing to pay for it. That gap is a business and even if it’s a small gap.

Use the three questions to guide you:

When friends and family reach out to you for help, what are you helping them with?

What is the hardest thing about your job?

What have you done for years which you don’t even think about doing, yet would take someone else months to figure out?

That’s likely to be your first side hustle.

Side Hustles That Pay Quickly

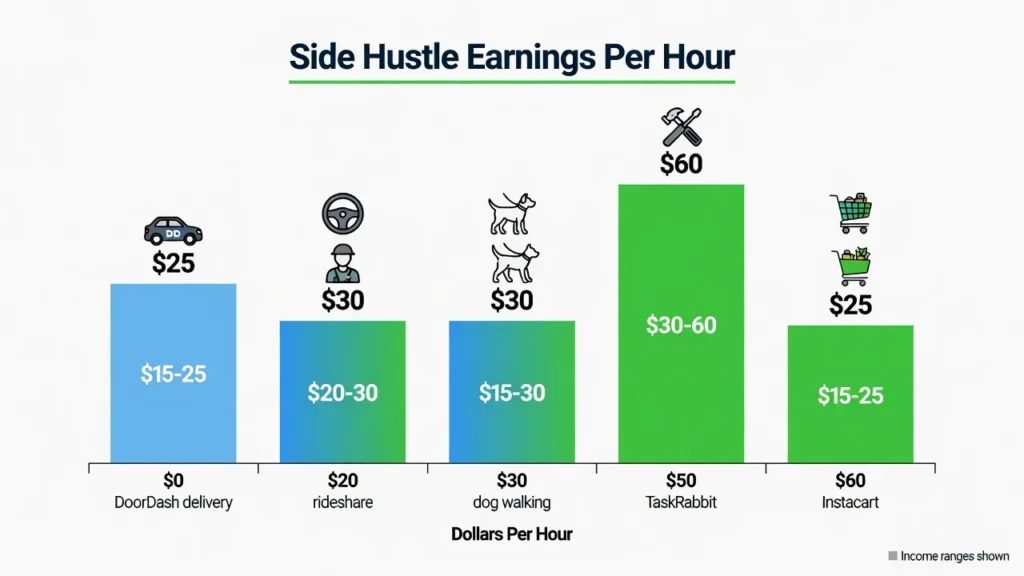

Gig work offers the quickest way to get income if needed in the next one week or two. There’s no need to create a business; just come along every day. These are some realistic weekly earnings:

- Delivery driving (DoorDash, Uber eats): $15-$25 per hour

- Rideshare driving: $20-$30 / hour, based on market

- Dog walking/pet sitting (Rover): $15–$30 per walk or day

- Handyman/Moving Job (TaskRabbit): $30 – $60/hour

- Grocery shopping (Instacart): $15–$25/hour

But if you don’t have time to find gig work, see if you still have enough time to work overtime with your regular job, even if that means 5–8 hours at time-and-a-half per week, which could bring in $400 to $800 more per month without the mess of gig platforms.

If a traditional second job would be a better fit for your schedule than gig work, you might want to do a retail or warehouse job, or weekend work in the service industry, the hours are set and the pay is immediate.

Sell Everything You Don’t Need (Week 1 Cash Injection)

Selling what you have is one of the quickest methods to get quick cash. There are $3,000 to $7,000 in underused or unused goods in the average household: electronics, furniture, clothing, tools, sporting goods, and collectibles are just some examples stored in closets and garages.

Facebook Marketplace, eBay, Poshmark, and OfferUp are just a few platforms that are fast sellers. If you can sell any of the items you won’t use for two weeks in a row, the money you make will help pay off your first debt.

Also, the psychological part is something to consider: If you sell something to pay off debt, it’s a real thing to do and a real goal to achieve, whereas budget adjustments are not.

How to Manage Side Income Without a Tax Surprise

This is what most first-time side hustlers don’t do and it can lead to a major shock at tax time. Freelance / Gig Income – No tax is withheld on your behalf. You are responsible to pay yourself either at the end of the year or by quarterly estimated payments.

Many people are unaware that they can also be taxed on their self-employment income at a rate of 15.3% (combined Social Security and Medicare taxes) in addition to regular income tax. If you aren’t prepared, you may find yourself paying 30 to 35 percent effective tax rate on the side income.

A realistic solution: save 25-30% of all extra income in a separate savings account. From what is left, allocate at least 50% towards your priority debt.

Create Your Bare-Bones Budget: Cutting Expenses to the Core

Six months is not a lifetime of living on a bare bones budget, it’s a short race with a clear end line! That’s one thing to reduce your spending on non-essential for six months, and another to be told to do it for the rest of your life.

The objective of a bare-bones budget is just one: reduce your monthly expenses to essentials just what is truly required and pay off the debt with the rest. If you’re spending money on anything that isn’t your mortgage, utilities, food, transportation, or debt, then it’s not essential spending – and it’s going elsewhere for the next six months.

Consider it this way: You are not giving things up. You’re giving up 6 months of spending and are getting years of breathing room. The hardest part of most people who have done it, is the decision itself to do it.

The “Small Leaks” Audit: Find Hidden Money in 30 Minutes

Look at your bank and credit card statements for the past three months and circle each of the charges that you know you don’t need.

Examples of common leaks include unused gym memberships ( $30-$60/month ), monthly fees for streaming and app services, subscription boxes, subscriptions to apps that automatically renew, premium phone plans with features you don’t use, and insurance policies that need to be re-quoted.

The money you can cancel from this 30-minute audit can add up to $100 to $400 per month and go by the wayside without any effect on your lifestyle except you had no idea it was there.

The $300 Per Month Food Challenge

One of the biggest items in any budget is food. The average American family spends $600 to $800 a Month on food, including eating out with their family. Reducing that figure to $300 is a different story; it’s something that’s actually possible for one person or a couple if you budget your groceries effectively. If you have kids, it’s more like $400 – $500.

The most powerful lever: Ban restaurant food and takeout for six months. If you are eating out frequently, it can be $200 to $400 a month for one person. This is a rare occasion and means that you are saving between $250 and $350 per month saving $1,500 to $2,100 over the course of your payoff sprint!

Practical grocery strategies for this phase:

- Grocery ideas for this stage: Plan meals weekly prior to shopping.

- Purchasing in bulk for basics (rice, beans, oats, pasta)

- Prepare large quantities and share them out for a meal later in the day.

- Don’t shop when you are hungry; make a shopping list and follow it!

- Temporarily switch to store brands across the board

The Cash Envelope System vs Digital Budgeting

There are two different ways to do this; they both work. The one that’s right for you is the one that you believe in.

No more plastic money: Take your monthly budget out in cash and cut it up into named envelopes (groceries, gas, dining, personal). If you have no points in that category for the month, then all the work has been completed for that one. The act of giving physical cash makes spending feel real, when there is no transaction as when using a card.

Zero-based budgeting for the digital age: YNAB (You Need a Budget) and Every Dollar are apps that take the concept of zero-based budgeting and bring it to your smartphone. Each dollar is given a task prior to the start of the month. Note: YNAB is roughly $14.99/month and if that doesn’t make sense when you’re trying to save money, you can use EveryDollar for free or a spreadsheet to do all the same things.

Either system works. The important thing is to select one at the beginning of the month and stick with it. The only thing budgeting after the fact is doing is record keeping. Planning is done in advance of the month, and is known as budgeting.

Should you do your Emergency Fund or should you pay down your debt? How to Handle Both

Emergency Fund or Debt Payoff First? How to Handle Both

The $1,000 Rule: Your Minimum Financial Cushion

Make sure to establish a $1,000 starter emergency fund, which will be held in a high-yield savings account that is separate from your everyday budget or checking account, before you begin aggressively paying down your debt.

The $1,000 amount is based on Dave Ramsey’s “Baby Step 1” and the logic makes sense because that’s the sum of the most typical financial emergencies car repair, minor medical bill or broken appliance and isn’t a huge amount of money you need to pay on a regular credit card or skip on your debt payments. It is NOT a full emergency fund. That comes later. However, it is enough of a distance to sustain your plan even if face to face with real life.

What to Do When Emergency Strikes in Month 4

Apply the money in your emergency fund to actual emergencies: If the car breaks down and you can’t get to work, if you need a medical expense that you can’t put off, or if you suddenly lose your job. Those qualify. Those do not include a sale on an item that you desire, social pressure to participate in an event, or an upgrade to your home.

When using the fund, take a break for 1-2 months and top it off again with $1,000 before you start using it again. You’re still on the same payoff schedule, but it might just be a few weeks.

How to Stay Motivated During 6 Months of Extreme Frugality

It’s really difficult to sustain a discipline for 180 back-to-back days. Research on habit formation and behavior change has consistently demonstrated that willpower is a limited resource: The longer a restrictive plan is followed, the more difficult it becomes to stick to it without a structure. Most people don’t fail at the math, they fail at getting excited through the weeks when it doesn’t seem like there’s anything thrilling and the goal is still a long time away. Here’s what systems really work.

The Weekly Review Ritual (5 Minutes Every Sunday)

An aggressive payoff plan isn’t feasible because monthly reviews are too infrequent. A spending drift or missing side hustle payment can add up to a real issue over the course of 30 days. Weekly tracking allows you to identify those problems early, and get 26 small progress wins each week, over the course of 6 months, versus just 6 times you think you are making progress.

Every Sunday, review:

- Update the tracker of the total amount of debt (total debt remaining)

- Money earned from side hustles this week

- If any budget line is overspent,

- You will be different this coming week because of one thing you are doing.

Gamify Your Debt Payoff: Visual Progress Hacks

An unmarked number on a spreadsheet is simple to overlook. A fridge thermometer that is coloured in each Friday, it’s not.

A visual tracker – one you review daily – transforms a spreadsheet balance into a real, earned balance. The way is not as important as consistency. Progress is repeated daily and will make it easier to form a habit than any notification on your app.

Visual tracker options:

- A printout of a debt thermometer, colored in weekly.

- Having a bar chart on your wall, with each debt as its own bar.

- A running total on a sticky note on your bathroom mirror

- A spreadsheet dashboard that changes color when balances fall below a certain threshold.A spreadsheet dashboard that changes color when balances get low.

Find Your Accountability Partner

Share your dream with someone. It sounds easy but it’s the basis of the attitude you’ll take to it. If the goal is kept entirely private, no one will notice and no one will ask and it is easy to easily give up on. A written goal that is known by another person has other significance.

You don’t need to go to a financial adviser or expert for your accountability partner. All they have to do is to ask you once a week: “How is the plan going?

One of the most active communities of this type is r/debtfree on Reddit people post their progress weekly, give each other feedback when they have a problem, etc., and hold each other accountable. Free of cost and the motivation is authentic.

The “Why” List: What’s Waiting on the Other Side

Write your motivation to go on a six-month sprint. Not only being debt-free, but what debt freedom will allow you to do in your life!

Examples:

- Stop running numbers at 2am at night and get to sleep!

- Have a real emergency fund for the first time Don’t argue with your spouse about finances.

- Be prepared to exit an undesirable job.

- Know how to exit an unwanted position.

- Don’t use a credit card to pay for it!

- Make, don’t live

When motivation wanes (which it will during weeks 5, 10 and 15), retrieve that list! That list is what will keep you going on the days that it goes wrong (and it will).

After 6 Months: Living Debt-Free and Building Wealth

It’s good to reach a zero balance really. It’s during the following weeks that most people make the most progress or regress into their old ways. The way you go next is as important as the way you got here.

Your New Money Allocation: Where Does the Debt Payment Go Now?

From Months 7–12, continue to build up your entire emergency fund of 3-6 months of living expenses and maintain it in a high-yield savings account. This is the cushion you put in place that keeps you from having to incur high interest debt again if the times get tough.

By the end of Month 13: Invest 15% or more of your income towards retirement. At this point, you’ll want to evaluate whether you’re hitting savings milestones for your age to ensure you’re on track for long-term wealth building.

First, contribute as much as you can to your full employer match (which is 100% never pass it up on your 401(k)), then max out your Roth IRA ($7,000/year in 2026), then go back and max out your 401(k) again.

In addition to that: save for sinking funds, 5-10% for car repairs, house maintenance, yearly bills that don’t come up regularly. This is not a chore as you have developed a financial discipline over the 6 months. The rest can go to you without any regrets. You earned it.

Avoid Lifestyle Creep: The Trap That Brings Debt Back

For months, you’ve carefully watched every penny, so you’re ready to spend some freely and you should! However, there is one discipline that you must have to live free from debt each day: spending on purpose instead of on impulse.

It’s often not one major decision that takes it down. It’s a succession of insignificant enhancements that seem relatively benign on their own nicer apartment, slightly newer car, a couple extra subscriptions, going out more often. After 6 months, all the extra money you earned has been put into a lifestyle you don’t even realize.

Try to set a “lifestyle inflation cap” you may increase your spend to 30-40% of your previous debt payment. All the other goes into savings and investing.

From Liabilities to Assets: The Wealth-Building Mindset

When no longer paying for the past you can begin to create the future. This is easy to do: don’t spend money on anything that depreciates and incurs interest your car loan, credit card debt, personal loans, etc. Begin to allocate funds to assets that appreciate or create income – index funds, dividend stocks, apartment/rental property, side business you’ve been working on.

This shift from liabilities to assets is the backbone of long-term wealth building. Not only getting out of debt, but getting out into debt which pays you back.

The top five mistakes people make when it comes to their 6-month plan and how to avoid them

Common Mistakes That Derail Your 6-Month Plan (And How to Avoid Them)

Mistake 1: The Minimum Payment Trap

One of the most costly financial behaviors you can have is paying minimum payments on debt. If you have $5,000 on your credit card, with an annual percentage rate of 27%, that means that it will take you about 25 years to pay it off at $100 a month and you’ll have paid over $10,000 in interest charges on $5,000 in principal. Instead of assisting you to pay off a debt, minimum payments are meant to retain you in it for as long as possible.

On your card statement you will have to read how many months/years it will take to pay off your balance if you only make your minimum payment this is a number you are legally due to receive from your credit card company (check the next statement). It’s frequently the most motivating number on the entire bill.

Mistake 2: Keeping Up Appearances While Drowning

A common, less pleasant personal finance situation is to live on credit while spending money on things you can’t afford. Paying 20%+ on your credit cards and spending money on expensive outings, new clothes or premium experiences is NOT keeping up appearances. It’s exacerbating the issue, bit by bit.

I have seen this happen for more payoff plans for debt than any math problem — it is subtle, hidden, and doesn’t seem like an issue until it is at the end of the month.

Short-term submission is the condition for long-term liberation.

To breathe through the years on the other side is a very small price to pay for the six months of simplicity. Most people who have tried it have reported that the difficulty is in getting started.

Mistake 3: Debt Consolidation and Balance Transfer Traps

Not every consolidation or balance transfer offers is bad, but there are these predatory offers out there. Red Flags to look for:

- Fees which are not explicitly stated at the outset.

- Interest rates that adjust rapidly as soon as the promotional period ends. Interest rates that change dramatically when the promotion ends.

- Companies that tell you to discontinue payments to your current creditors

- Strategies that pressurize you to make a decision right away

For legit assistance navigating your choices, look for a nonprofit credit counselor by means of NFCC.org. A professional credit counselor will examine your debt, negotiate with creditors for you and create a debt management plan without charging you excessive fees for a for-profit debt settlement firm.

Tools and Resources for Your Debt-Free Journey

Free Budgeting Apps and Debt Calculators

If you’re new to budgeting, start with budget basics to understand core concepts, then choose one of these tools:

YNAB (You Need a Budget): The most thorough budgeting app out there.

Each dollar has its assignment before the start of the month. Expensive at $14.99 a month, but if you use it then it’s worth it.

EveryDollar: Free zero-based budgeting app from Ramsey Solutions. Less complex than YNAB, but works well for most people entering the program. Unbury.me is a free online budget calculator and debt payoff tool that allows you to enter your balances and interest rates and see how long it will take you to pay off your debt using the snowball or avalanche method. Great for visual planners.

AnnualCreditReport.com: Request all three credit reports once a year in a single application and obtain a copy of all three at no cost. Must have starting point to your debt assessment.

A paper notebook or spreadsheet: Any notebook or spreadsheet will do to track debt payoff progress as well as an app. Don’t let the choice of tools be the excuse to not get started.

When to Seek Professional Credit Counseling

In some cases professional intervention is not just welcome but vital. Before making big financial changes, talk with a nonprofit credit counselor if you have too much debt, if creditors are threatening to take legal action, if you can’t afford minimum payments on your debt, or if you are thinking about filing bankruptcy.

The National Foundation for Credit Counseling (NFCC.org) has access to certified counselors that can review your debt management plan, negotiate with creditors for lower interest rates, and create a plan for you to structure your debt without predatory fees from for-profit debt settlement companies. It’s not a failure if you need help, you take it. This is the most cost-effective option you have.

Frequently Asked Questions

Does it seem to be possible to become debt free within 6 months when earning a low income?

It depends largely on your debt to income ratio. Even if you have less than $6,000 of debt and can allocate 40-50% of your after-tax income to debt repayment, the 6-month plan can be accomplished on a moderate income. The 12-month journey will be more beneficial to you if your debt is greater than your income. For specific strategies to save money on a low income, focus on the expense-cutting tactics in this guide combined with at least one income stream. This is how to be debt-free in 6 months, or close to debt-free, even if it’s not a smooth and linear path.

Should I decrease my contributions to my 401(k) to reduce my debt?

This depends on the interest rates. When your credit card APR is 20%+ and you’re making an anticipated investment return of ~10%, the numbers are in your favor when it comes to paying off the high-interest debt. During aggressive debt payoff, Dave Ramsey advises to take a break from all retirement contributions, except the employer match. Other advisors disagree. The one thing you have to do: don’t stop contributing enough to max out your employer match. Regardless of either choice, pledge to resume full payments once the debt is paid.

If there is an unplanned event during the plan period, what will happen?

This is where your $1000 emergency savings comes in. Only use it if it’s a real emergency, refill it before you start making aggressive payments and remember that the time frame may move up and down a few weeks. It’s not failure if it takes a little longer — it’s quitting!

Which is better a debt snowball or debt avalanche?

Both work. Go for snowball if you want quicker wins to keep you motivated. Pick avalanche, if you’re motivated by numbers and are disciplined enough to not get too much of a rush from wins. If you’re not engaged in the method then it’s not the right one.

How to easily release some cash?

Three steps that make a difference right away: Cancel all the unnecessary monthly costs ($100-$400 recovered per month, depending on the person for a single person), get rid of eating out almost completely ($200-$400 recovered per month, depending on the person), and start one gig income stream this week. Together, these three are enough to produce an additional $500 to $1,000 in monthly cash flow without making any other changes.

Is the balance transfer card a good way to get rid of debt?

If you’re sure you can pay the balance in full before the promotion is over. Read the full terms and conditions. Make sure you know what happens when your promotional period ends. Don’t use balance transfer as a pretext to collect your old card and spend some money.

So what becomes of me when I pay off my final debt?

Refer to the “After 6 Months” section above for complete instructions. To summarize: establish a complete emergency fund of 3–6 months, save all 401(k) employer match, max out your Roth IRA, save for irregular bills with sinking funds and don’t let lifestyle creep up on you. This financial discipline you’re developing during the payoff sprint can form the basis for the rest of your life.

The ranges of earnings listed for gig work are approximate averages reported and may vary by hours worked and city/market. Don’t make projections for your debt payoff plan without first checking out current rates on that platform.

The content of this article is for information only, and is based on general personal finance principles. Seek advice for your particular situation from a professional financial advisor or credit counselor.