How Do I Stop Overspending? 11 Ways Real People Broke the Cycle

More than once, you’ve thought to yourself, “How do I stop overspending?” Perhaps just after you’ve looked at your bank statement and noticed that familiar feeling in your gut. Perhaps you have a cart of items you don’t need after spending the night, and you don’t know how you got there again. The awful thing about all this advice is that it doesn’t address the core issue. When it comes to budgets, spending trackers, and willpower pep talks, they’re all about treating the symptom, and not the problem.

I had to deal with impulse spending for years without knowing what was causing it. I began to review the psychology behind the buying, and everything began to shift. This is the topic of this article.

Why You Can’t Stop Overspending (It’s Not What You Think)

The one thing that really got me to think differently about money was the realization that overspending isn’t a character defect or discipline issue. It’s a clash between old brain and a new world.

Humans have developed over about 200,000 years in environment of scarcity. Food was limited. Resources were uncertain. In order to get us to seek and acquire things before they were depleted, our brains evolved potent reward systems. That’s perfect for most of the history of humans.

Then in past 50 years we built one click shopping, 24 hours store, targeted ads and infinite product feeds. The evolutionary world turned upside down in a blink of an eye, but the brain didn’t receive the message. We live in a world of instant abundance, and walk around with prehistoric reward-seeking hardware in our brains.

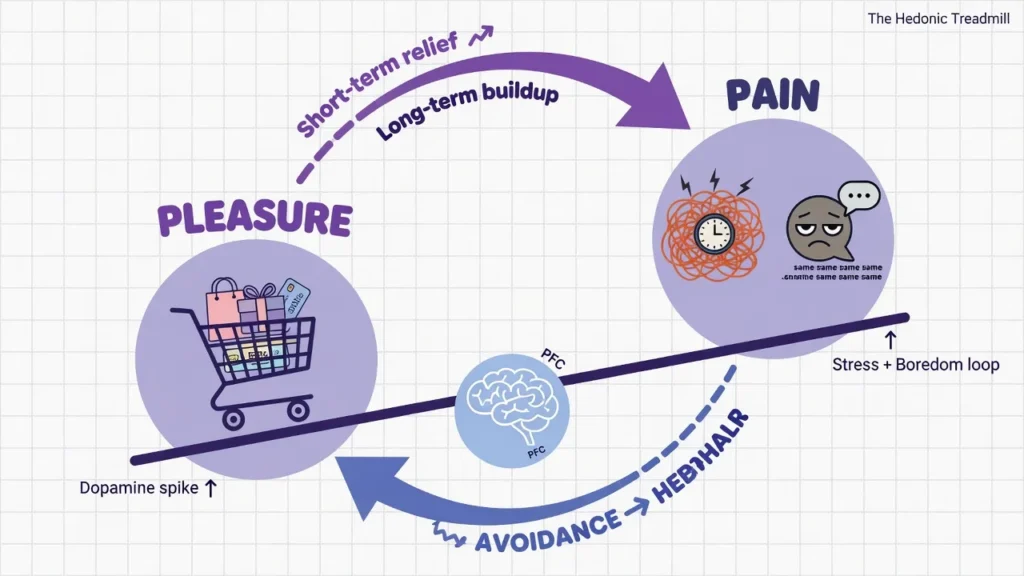

The more you add to your cart or click “buy,” the more dopamine your brain releases, and the more instant gratification you get. It feels good. It’s as if you sorted out a problem, it feels like progress. However, the more you activate that sensation of pleasure, the higher your base. Excessive enjoyment leads the brain to shift towards reduced satisfaction, seeking balance. You feel bored and empty or a little frustrated in your idle state. So you spend again, just to feel normal.

Excessive spending isn’t a habit you are trying to break. You’re going to be playing against evolution programming in an environment that’s optimized to exploit it.

It’s important to know this because it will affect how you approach things. You don’t blame yourself anymore, you begin to ask yourself: What systems and strategies work with your brain rather than against it?

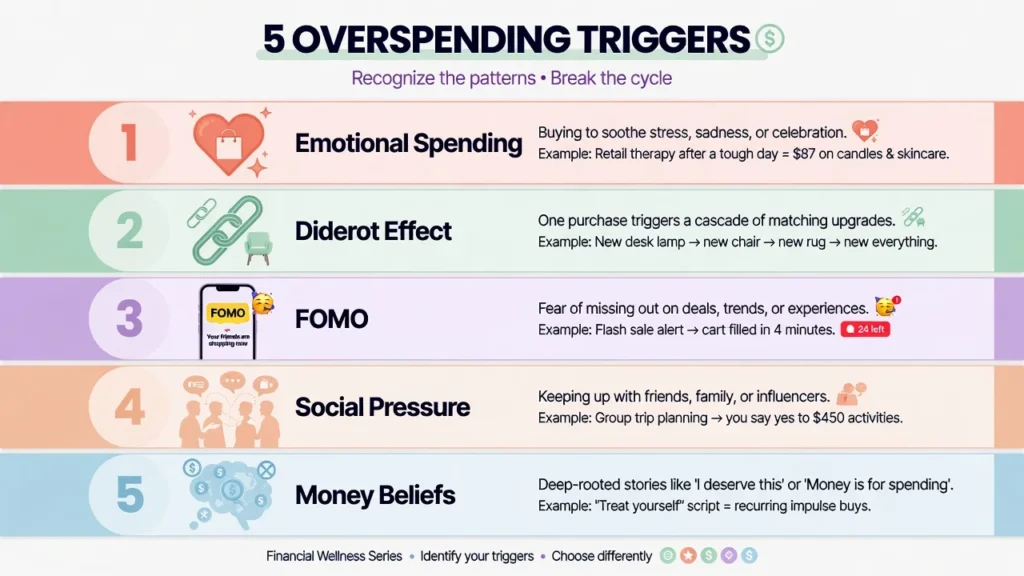

Why Can’t I Stop Spending Money? The 5 Hidden Triggers

The first step to addressing a behavior is to determine what is triggering it. There are 5 common triggers that most people who are in overspending issue are reacting to. The first step is to identify yours.

Emotional Spending: When Shopping Fills a Void

Consider a time when you bought something impulsively. What was your last thought just prior to its occurrence? Bored? Stressed? Lonely? Frustrated at work?

Immediate emotional relief is shopping. If you’re feeling down, shopping gives you a quick flash of excitement and a feeling of control over something. It really helps at the time, which is why it becomes a habit of emotional spending. The thing is almost irrelevant. People are ordering an emotion.

This reframe changed something for me. So I began to ask myself, “What did I want to feel when I bought this item?” rather than, “Why did I purchase this item?” That’s a better question at the heart of the matter.

The Diderot Effect: Why One Purchase Leads to Ten More

The Diderot Effect is a theory about a French philosopher, Denis Diderot, of the 18th century who received a new handsome robe as a gift and began to purchase the same type of garments for his home, his family, and his friends, as soon as he got it. That purchase made him feel he had to spend more on all of his other purchases, and thus began a pattern of overspending.

It is an everyday occurrence in contemporary society. A new camera is purchased and after some time, the bag you have been using for years appears to be worn out and the lens seems restrictive. You finally own a new car and a week later, you’re looking into ways to customize your seats, get a new phone mount, or pick out the best audio system upgrade. Every purchase adds a seed of dissatisfaction which sprouts into the next purchase.

The best defense is a cooling off period. Purchase new items, at least a fortnight before any other purchases. The desire to buy more will naturally die down when it comes to acquiring more of the new item.

The FOMO Factor: How Social Media Makes You Spend

It’s proven that 66% of Millennials actively try to match up with the amount their friends are spending, which is why it’s one of the least recognized causes of overspending. The pressure is even worse on social media where everything we see becomes our highlight reel. You are not comparing yourself to the true image of people’s life. You’re comparing your every-day Tuesday to their stellar Saturday.

Worship the ad, the culture of spending money frivolously, and algorithmically-targeted advertising, and you have a system close to being optimally designed to generate artificial desire.

There is not only a financial risk of overspending here, but also a psychological risk. Social pressure spending means you’re paying for a life gone by the plans of others. The less of that exposure is not so much about willpower as it’s about what gets in front of your eyes in the first place.

Before You Try Another Budget: Do This First

Any budget management advice begins with the budget. I don’t think so; I don’t think that’s a good starting point. Not that budgets don’t work, but because the underlying problem isn’t addressed.

When you are spending money due to stress and you make a budget, it will lose to the stress. A spreadsheet will not alter the situation if you are spending because your friends want to have a certain lifestyle.

I have watched people carry detailed budgets and significant debt at the same time for years because they never asked the honest question underneath the numbers: why am I actually spending this way? Once you understand your triggers, then you can learn the fundamentals of budgeting that actually stick because they’re built on self-awareness, not just spreadsheets.

When she finally stopped lying to herself, that’s when Christina Mychas’ life turned.The turning point for Mychas was when she stopped lying to herself, and her debt was something over $120,000. She even acknowledged that she was a shopaholic. It was their admission, and not the budget that made all that possible.

The 30-Day Spending Audit (What to Track and Why)

A spending audit is not simply a counting exercise of categories. That can be done with a bank statement by anyone. What I do suggest is that you keep three separate columns on your expenses for all discretionary items – this is where you spent the money, the type of item, and the emotion you felt when you made the purchase.

This is the one that makes the difference in that third column. At the end of 30 days you will not only be able to see where the money has gone. You will see how you spend money and how your emotional state relates to your spending. That’s a helpful piece of information. That is just a list of numbers, without context, to feel bad about.

To complement the audit, get rid of the categories that have too many unnecessary expenses. Probably one of the best reality checks is to go through the things you have used in your problem areas.

11 Proven Ways to Avoid Overspending (From People Who Paid Off $250,000)

These strategies are from those who have actually worked. In five years, one couple paid off $250,000 in household debt, including a considerable amount of credit card debt. Christina Mychas paid off $120,000.

These are not abstract approaches gleaned from a book. These are tried solutions that were derived from actual financial stress and actual financial recovery. If you’re also carrying debt, combining these overspending tactics with strategies to become debt-free can accelerate your progress even faster.

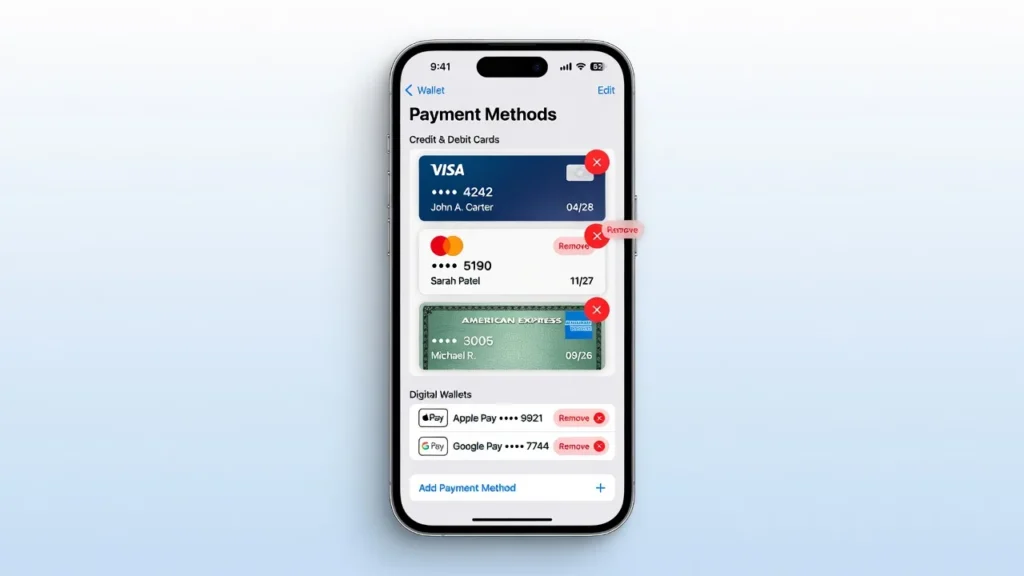

Tactic 1: Delete Saved Payment Info Everywhere (Yes, Even Amazon)

The first thing you can do is delete saved payment details from each app and website you have. Gone is Apple Pay, gone is Google Pay, gone is Amazon, gone are all the favorite clothing sites.

This change was described by one Reddit user and that’s what happened for him, impulse shopping ended virtually right away. Not because they were more self-controlled than others, but because they had to get up, look for a card, type in the numbers, and go through several confirmation steps to buy now. The impulse didn’t last till the checkout.

In this case, friction is your ally. It can be eliminated by modern checkout systems, which are designed with less friction in mind, so there’s more money spent. The removal of your saved cards is on purpose to reverse that engineering.

Tactic 2: The “Leave It in Cart” Trick (Get the Dopamine Without Spending)

Again this may seem counter-intuitive, but it always works: put products in your cart and then don’t checkout.

The reward from shopping is largely experienced prior to the purchase. The browsing, the imagining, the adding to the cart. With items added, the anticipation surge is reduced. When he shuts off the tab without purchasing anything, it is a delayed gratification, but also a manageable one. The urge typically goes away in a day or two.

One woman on Reddit went so far as to say she would fill her cart with stuff from Macy’s and love the shopping but rarely actually sought to purchase anything. The cart was no longer a list of purchasing items, but a wish list. Use this as a guideline for making unplanned purchases for 24 hours.

Tactic 3: Calculate “Work Hours” Before Every Purchase

One of the most effective conscious spending reframes of all time! Calculate how much of your time is required for purchase.

If you are making $20 an hour and you’re about to spend $80 on something that you impulsively want, well, that’s four hours of your life. Four hours of waking up, getting to work, sitting at a desk, and doing the work.Four hours of waking up, getting to work, sitting at a desk, and doing the work. Does this item justify that? While a price tag doesn’t quite do the same, that concrete comparison cuts through the abstraction of numbers.

Tactic 4: The Cash Envelope Method (30% Less Spending, Proven)

Based on behavioral research on the psychology of payment methods, financial psychologist Dr. Brad Klontz discovered that people spend around 30% less when they are paying with physical cash than when they pay with a card. This is because the handing over of bills generates a sense of discomfort in the person, which a card swipe does not. Cash is a real pain to pay with.

The technique is to alter the way you pay for different categories of expenses one by one, beginning with the ones you spend too much on. Make a weekly cash limit for food or meals out or entertainment. If the envelope is empty, the category is no longer spent. Using debit cards instead of credit cards also has a similar effect, since you are not spending money that you don’t have.

One caveat: This doesn’t always work for anyone. Others believe that when they take money from the bank, they’ve spent it, meaning that they may be more inclined to use it. Try it with the one category for two weeks and then make a full commitment.

Tactic 5: Unsubscribe, Unfollow, and Block (Digital Detox for Your Wallet)

You can’t wish for what you haven’t experienced. With that one fact, making less advertising influence on your daily decision one of the highest leverage things you have as a consumer to do.

If you can, unsubscribe from all the retailers on your list now. That goes away and eliminates dozens of fake crises each week. Next, remove shopping apps from your mobile phone, install an ad-blocker in your browser and disable or unfollow any social media that have the habit of making you want to buy.

This is the protection against systems that are designed to create desire. Not deprivation, that is what? That’s just common sense about what you see. The impact is subtle. Minimize the inputs and thus the impulses to control.

Tactic 6: Move Money to a Different Bank (Create Time Friction)

One of the least sexy strategies is to set up an automatic transfer to your savings account from your paycheck when you get paid. However, time friction is not just about automation; it’s a strategy.

Take some funds out of your main bank that doesn’t have a debit card or instant transfer. Online banks can usually offer a high yield savings account that is just the type you are looking for. Impulse spending from that account becomes almost impossible with transfers taking 2-3 business days. The defense’s excuse is the delay.

This is the one thing that a bunch of people in the personal finance world say made saving stick for them. Not discipline. Simply inconvenient access.

Tactic 7: The “One In, One Out” Rule (Stop the Accumulation)

This rule is easy and highly effective at cutting away any needless items: If you want a new item in your home, you must have a like item come out of your home. Purchase a new shirt and give one away. Purchase a kitchen item and discard or donate an old kitchen item.

When you do this regularly, two things will occur. First, with each purchase, there has to be an active decision on what one already has that slows down the accumulation process. Second, you are now judging the new things in the light of what you currently have. In most cases, the things you already have are fine.

Tactic 8: Try a 2-Week Spending Detox (Reset Your Dopamine)

A no-buy challenge of 2–4 weeks takes place neurologically. It allows your reward system in the brain to get back to a neutral state.

Recall from the first section, the dopamine seesaw. A spending detox is a way to reset your spending habits when you’ve become more discontented with your lifestyle than usual due to impulse buying. Things you used to take for granted feel like they’re actually good again: homemade meal, walking outdoors, quiet time.

This is a reset and NOT a rule. After two weeks of giving your brain a break, it’s still long enough to reset how much it really needs to feel fulfilled from spending stimulation.

Tactic 9: Create Your Personal “No-Buy” List

A no-buy list is a personalized means to your own particular spending pattern. It’s a list of categories and should be things you don’t buy until you use up the things you have.

Details are up to you! Jeans are on the list if you have 10 pairs of jeans. Small appliances are stored if your kitchen drawers are filled with things you don’t use. It’s not a spending holiday. It goes directly where your money goes secretively.

An alternative rule for using the list is that you are able to purchase a new version if the old one is truly complete or if it has been rendered unworkable. Not just old. Actually done.

Tactic 10: Find Your Accountability Partner (Or Join r/nobuy)

Having someone else on your journey to financial objectives helps to alter your spending mindset. Studies indicate that an accountability partner is highly effective at increasing follow-through when working on goals. If the person you’re interested in knows of your plan, breaking it can have a definite impact.

If no one at your place or around you will take you seriously, you’ll find plenty of people doing exactly what you’re doing in the r/nobuy subforum on Reddit. When people share their experiences of success and challenges, it becomes less of an isolated experience. It also makes it much more difficult to give up when no one is looking.

Tactic 11: Track “No-Spend Days” on a Calendar (Gamify Your Progress)

This seems like a no-brainer, but it’s one of the best things that can help promote financial discipline. Write NO SPEND DAY on a paper or digital calendar.

Throughout the next few weeks, don’t want to throw the ball. You will be able to see for yourself that you are improving. The more you achieve, the more confident you become and the more it feels like a no spend day and less like a sacrifice. The level of gamification is not light and easy here. It focuses the same reward-seeking pattern that makes spending attractive on the constraint of spending.It channels the same reward-seeking pattern that makes spending attractive to the constraint of spending.

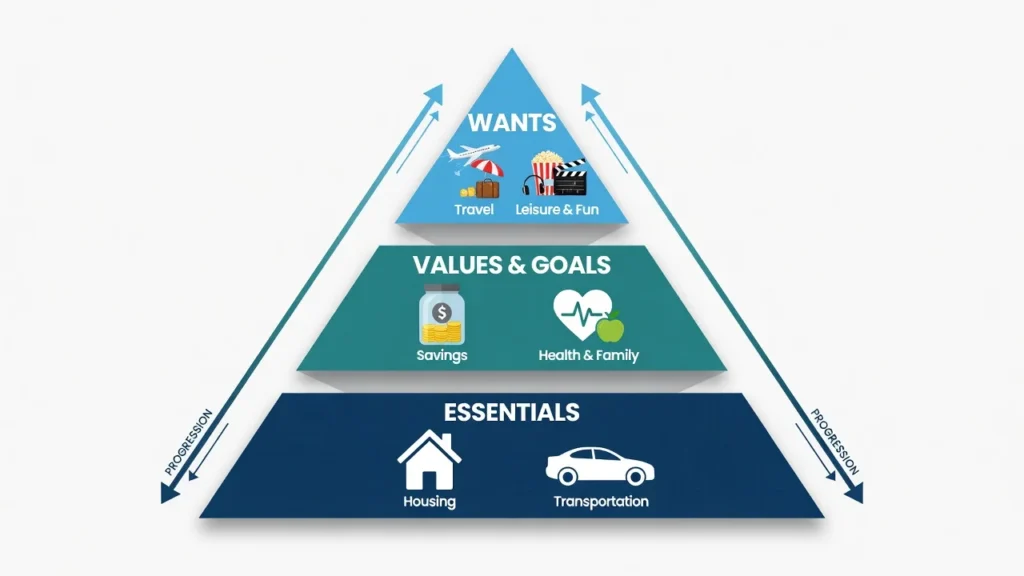

Build Your Priority Pyramid (A Better Alternative to Traditional Budgeting)

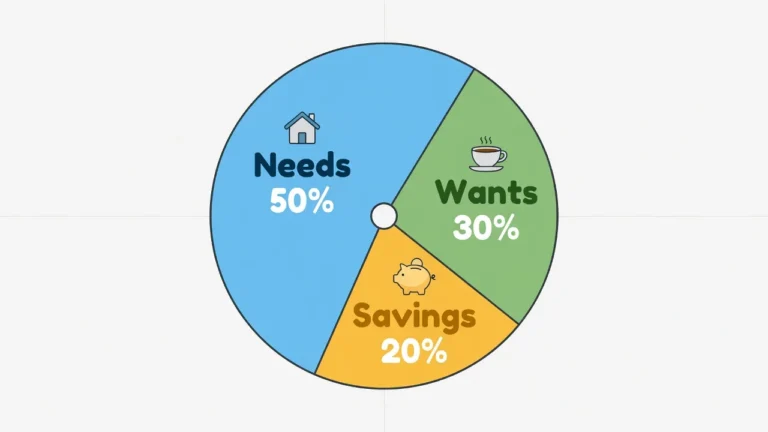

The system that did something for me is something I call the Priority Pyramid. Imagine three levels and visualize how money moves up from the bottom. If you’ve heard of the 50/30/20 budget rule, this works similarly but instead of percentages, it uses a visual hierarchy to help you prioritize spending decisions.

The foundation tier consists of the essential budget line items that you cannot stop paying for such as rent or mortgage, insurance, utilities, transportation etc. These are the first ones to get paid – they are paid monthly and without fail.

Your financial objectives and real values are at the middle level. Spending well on things that are important to you, like quality food or health, saving up for a down payment, paying off debt, etc., investing for retirement. They are not a reaction, they are a choice.

With the top level, it will be your allowance for things you want to do: hobbies, vacations, eat out, entertainment. These are not available until the bottom two tiers are funded. Not the reverse.

How to Define What You Actually Value (Beyond What Instagram Says)

When people are asked about their values, they have answers based not on true values, but on the basis of social comparison. Travel, family and health. However, their spending habits seem to be conscious.

A more open exercise: Reflect on your best experiences in the last 2 years. Not the ones that were ‘good for social media’. The ones that at the time were really good! What is your actual job?

Experiences and connection turn up a lot more often than objects for most people do. Spend time with people who are important to them. Learning something new. Getting outside their bodies. Items actually purchased, as opposed to physical items, show up a lot less than people think, based on what they actually spend.

At its heart, conscious spending starts with finding the answers, not the answers you think you should get. It’s also the one area in which no budget spreadsheet can help you.

The Identity Shift That Makes Controlling Spending Easier

Systems and tactics are important. However, I have seen that most people who made this change for good talk about a change in their perspective rather than just in their actions.

It’s not the same thing as saying to yourself, “I want to spend less,” when you’re saying, “I’m a saver.It’s not saying “I want to spend less” to myself versus saying, “I’m a saver. One leaves you in a battle. The other communicates to your brain who you are collaborating with. Your spending becomes the proof of your identity, one decision at a time.

As the bestseller Atomic Habits author James Clear says, “Who you are is the most powerful force at your disposal for transforming your habits. Choose a persona, then gather flecks of evidence to support it. Each No-Spend Day is proof. All items in the Shopping Cart are evidence. Each time you refrain from matching your friend’s lifestyle is evidence.

The turning point according to Christina Mychas was when she decided to stop the inwards narrative that made her feel bad about money. The same narrative was now becoming its own reality. The behavior followed her change in story.

No fixing needed. You have to choose a character to become.

The 5 Overspending Mistakes Almost Everyone Makes

There are lots of articles out there that are only about how to do something. It’s also important to recognise some of the common pitfalls, as there are some patterns so common that people will repeat them without knowing there is another way. It’s as crucial to learn the habits of the over spenders as it is to learn the tactics.

Mistake 1: Treating Shopping as a Hobby

Shopping for fun at the mall, scrolling through retail apps when bored, or shopping to take advantage of flash sales all perpetuate the culture and make it easy to shop impulsively at any time. Consumption turns into how you invest your time, as well as your money.

If you recognise this pattern, it’s not about improving your budget. It’s substituting shopping with entirely different activities, and not shopping, comparing, buying!

Mistake 2: Lifestyle Inflation (The More You Earn, The More You Spend)

When you start earning more money there are expenses that go along with it. With a higher income comes a nicer place to live, a newer car, a nicer restaurant, nicer clothes.

All of the upgrades appear to be singularly warranted. However, the lifestyle inflation syndrome tends to work against you because the difference between income and expenditure remains constant or increases. You never become wealthy, because your lifestyle increases in proportion to your income.

The answer is simple: Use every increase in income to save it rather than spend it. Setting specific savings milestones based on your age and income gives you a concrete target to hit instead of letting lifestyle inflation steal your raises.

Mistake 3: Buying Cheap Instead of Quality

The phrase “one of low means buys twice” is true. The least expensive version of a product that will fail or wear out will actually come out to be more expensive in the long run than a product that is of high quality and purchased initially. No, this isn’t an excuse for luxury brands. It’s an argument to look for durability before purchase and to not spend money for novelty.

If you’re purchasing an item that you use often, make sure to read reviews for durability. That habit alone saves more money than most budgeting tactics.

Mistake 4: Trying to Change Everything at Once

If you’re trying to make a major financial overhaul, diet overhaul, exercise program and sleep routine change all in one go, you will most certainly fall into overwhelm and ditch them all.

Studies on behavior change have proven and proven that one habit change at a time is much more effective than changing everything. Select your most important spending change. Try to make that one thing work first. Then add the next.

Mistake 5: Keeping Up With Friends’ Spending

66% of Millennials say they are “trying to keep up” with their friends’ spending. This is not vanity at all. Humans are sensitive to the importance of maintaining appearances to signal belonging and status in the group.

However, if you spend money you do not have to keep up that image, you’re borrowing from your future self to support the image for other people. It’s very rarely a good deal. If you are in a situation where this is impacting your finances, the next part on relationships below explains specific ways to set the boundaries without ruining friendships that are important to you.

What to Do the Day After You Overspend (Because You Will)

All those who have succeeded in changing their spending habits have had their share of setbacks. The gap between individuals who make the change a permanent one and those who go back is not that the first group doesn’t slip up. It is because they get over them quickly and without embarrassment.

The principle for this practice is straightforward, “Don’t miss twice. It’s just a mess-up. Every time he fails a test, this is a new pattern that begins with two slips in a row. Once you’ve gone over your allotted spending, all you have to do is go back to your old ways the next day.

The “Never Miss Twice” Recovery Plan

If you go over your limits, don’t fall into a spiral of shame or severe self-judgement. Christina Mychas, who paid off $120,000 in debt, singles out this one as the one that stuck with her for the longest time. Self-criticism for failures will increase not decrease the chances of further failure. It de-motivates.

Rather, have a strong and caring tone. That was the trigger, I see it now and I’m back on track today.

Do 3 things within 24 hours. Examine the reason for the money spent. Re-state your financial objectives or identity statement. Do one small thing that shows you are on track, such as not buying coffee on the way to work.

Reward yourself with something meaningful when you really hit a milestone, but not a purchase. Positive reinforcement creates the habit loop that you want to construct.

When Your Relationships Are Making You Broke

Most financial advice doesn’t address this question at all, likely due to discomfort. However, the people you live near have a tremendous impact on your spending habits – more than any budget or tactic ever could.

No matter how intended or planned your spending is, or what your financial goals are, your intentions can be led astray by a past partner, a social group where expensive trips are considered “the norm” for connecting, or a family culture that encourages people to spend money as a way to demonstrate their love for each other.

How to Say No to Friends Without Losing Them

You don’t have to explain or apologize for your decisions when cancelling a costly plan. Most scenarios are taken care of by a simple and honest script: I have some savings objectives right now and I’m more mindful of where my money goes. Looking for an activity at my house?

Offer alternative solutions that are free or cost-effective. The walk or the home made meal or the movie night or the game evening! People generally appreciate honesty and a solid plan, if both of these elements are combined. If they don’t respond to you, they’re telling you something to be learned about the friendship.

When to Re-Evaluate the Relationship

The financial impact can be more profound at times. These are situations beyond tactics: A partner who does not contribute and expects to share in the lifestyle, a social group whose social value is entirely based on consumption, or a family member whose validation is based on consuming in the same way as the rest of the family.

Mera, who assisted her family in paying off $250,000 in debt, says one cause of her financial woes stems from a previous relationship in which she took on minimum wage jobs to support a non-working partner. Breaking up with him altered her whole course of money-making. The company you keep, is as important as any budget.

Special Case: How to Stop Overspending With ADHD

For those with ADHD, it is not simply a case of making better choices that leads to overspending. Impulse control and a drive for dopamine are key features of the neurological profile of ADHD, and may be stronger than in brains that are neurotypical.

The common wisdom that everyone carries around of “stop and think before spending” does not always work for ADHD brains. What works is not motivational, but structural.

Friction-based methods work well in particular. Taking out saved payment data and clearing shopping apps from your phone creates much needed breaks, avoiding the impulse control void in the moment. Saving decisions are taken out of the equation completely with automatic savings transfer. The funds are queued up without you having to see them as cash to spend.

The visual tracking systems are also suitable for ADHD brains. Preference for concrete and immediate rewards is met with a physical calendar that has no spend days marked or a visual savings goal chart.

The object is to having the right behavior as the norm. Don’t out-willpower your neurology. Instead, develop systems that work.

When to Seek Professional Help (Yes, Shopping Can Be an Addiction)

Most people will be satisfied with the strategies in this article. However, for some, the problem of overspending has become more of an addiction that is a behavior.

Financial psychologist Dr. Brad Klontz says that it can start out as retail therapy and end up as a shopping addiction or complete compulsive buying disorder. Once there, you are probably making purchases that are financially harmful, concealing purchases, feeling as if you can’t stop, and over shopping as a way to numb down emotional pain as if you were doing another compulsive act.

Signs You Might Have Compulsive Buying Disorder

Addiction to shopping is a continuum and the symptoms of compulsive buying disorder are: You spend more than you can afford, even though you know it will cause problems; you think you need to hide shopping from close friends and relatives; you feel intense anxiety or distress when you can’t go shopping; the emotional benefit of shopping decreases and lasts for a shorter period of time, making it necessary to shop more often to get the same effect.

The financial stress, the strained relationships, and the urge to draw from savings or from others to pay off bills are also serious signs that professional assistance would be beneficial, not advice on good spending habits.

Where to Get Help

CBD can be treated. The most evidence based therapy is cognitive-behavioral therapy with a therapist that specializes in behavioral addictions. If you’re looking for a financial therapist, or a CBT specialist for compulsive buying, then you’ll be able to find someone that is a better match for you quickly.

Free support groups, such as Debtors Anonymous, are based on 12 step groups and are free. They provide a recovery pathway and a sense of accountability and community. Your doctor or mental health professional may be able to suggest other sources of help.

It’s not a shame to need some more help than a set of habits can give. In understanding that and responding to it, one has engaged in another type of self-awareness, the self-awareness this process requires.

Your First Step Toward Stopping Overspending (Take It Today)

If you have been asking yourself “How do I stop overspending and feeling like I am failing to do so?” then I want you to take one thing from this: it’s not a lack of morals. It’s a brain designed for scarcity, in a world designed for consumption. If you know how to change, what you do next changes.

Not all 11 of the tactics need to be implemented right now. Choose the most similar pattern or trigger to your own. Start there. Do that one time, and demonstrate to yourself that you are on your way to being intentional with money. As you master controlling impulse spending, you can also reduce your monthly expenses in other areas to accelerate your financial progress.

Mera and her husband paid off $250,000 of debt in five years, after falling into the same sort of over-spending habits that the article mentions. Christina paid off $120,000. They were evenly matched with no hidden advantage. They did decide what they were and they did what they were meant to do, one little thing at a time.

There is no perfect plan to get financial freedom. It begins with one choice that’s different from the previous one. Do that today:

Frequently Asked Questions

How do you get individuals to save money when they know they should save?

Knowing and doing occur in different areas of the brain. The emotional center of the brain, the limbic system, overrules the prefrontal cortex, which is responsible for long-term thinking and planning, on a regular basis and insists on some immediate relief. The release of dopamine fills emotional voids such as loneliness, stress and boredom. It’s not a lack of knowledge or a lack of willpower, it’s a neurological response. The most obvious solution to the question “How do I stop overspending” is to establish a budget and/or set some rules, but the underlying answer is to first understand and address your emotional triggers.

Is it really an addiction, as in the case of alcohol or drugs?

Neurologically it can be: Shoppers activate the same dopamine reward pathways as other addictive activities. Completely addictive shopping can exhibit the typical behaviors of an addiction: a need for increasing amounts to get the same effect, using shopping to numb or dull painful feelings and the persistence of the drug use despite knowing that the results are harmful. Fortunately, as with other behavioral addictions, compulsive buying disorder can be treated by the right professional support.

What number of months does it take to free oneself from negative spending?

Dopamine baseline resets usually take 2 to 4 weeks to occur with lowered discretionary spending. Full habit change takes a longer path – there are three phases of awareness, preparation and sustained new behavior, prior to things becoming automatic. Over time, the brain is constantly rewiring the pathways in the brain and consistency is more important than speed. Instead of looking back at what has taken place, look at the small consistent wins. They build up much quicker than you think.

What to do on the second day after exceeding the budget?

Use the Never Miss Twice rule. One miss is a coincidence. When 2 numbers are in a row, they begin a new pattern! Avoid focusing on the negative self talk because research indicates that negative self talk is counterproductive to long-lasting change. Speak to yourself in a gentle but strong tone and acknowledge the trigger for the slip, and resume your regular habits on the same day. It is not about getting it perfect, it’s about how quickly you recover.

Does cash only model work?

Research in behavioral finance indicates that cash is 30% less effective at controlling spending because handing over cash makes people feel a sense of loss that they don’t feel when they are using cards. It works for most people, however not everyone. Retracting cash can cause less friction for some people because they feel it is already out of the way when it is pulled out of the bank. Know if it works for your mind and spending habits by trying it out in one spending category for two weeks.

What to do if friends always want to go out but I am always getting into trouble with my finances?

66% of millennials say they feel pressured to “catch up” with their social group when it comes to spending. Setting clear limits and recommending free or less expensive alternatives is most effective; don’t go into too much detail. It’s a simple statement and I’m doing that now: I’m doing my saving goals right now and being more selective. Support is what true friends do. If it appears to be based on them spending the same amount, it should be looked at on its own merits.

What is the Diderot Effect and why should it matter?

The Diderot effect is the phenomenon that occurs when you acquire something new and consequently feel unhappy with all of your other possessions, leading you to make more purchases. You purchase a new camera and realize that you need a new bag, better lenses and software to go with it! An interruption to this pattern is achieved by naming it. If you are feeling the urge to purchase more after one purchase, recognize that it’s the Diderot effect, and give the item a period of cooling off before the next purchase is made.

So what if I spend more than I need on essentials such as food, rather than luxuries?

Examine first if these are truly necessities or if they’re just a part of lifestyle that is falsely labeled as a necessity. Organic versions of everything, top brand in every category or regular small trips to the top-ups all seem like essentials. With respect to actual necessities, a rigid shopping list and a hard-and-fast policy of purchasing only those items are a huge help in decreasing the total. Learning to create a grocery budget with specific weekly limits prevents overspending in this category. Limiting the time spent in stores and putting a price cap on each trip also helps. Look for signs of category creep when you’re saying you need to spend money on this item.

What is the solution to the small, regular subscription costs being excessive?

One of the most neglected forms of over-spending is subscription services – every single charge amounts to little. On a mobile banking application or your bank’s in-built subscription tracker, record all subscription charges you currently have. Stop or cancel any unsubscribed product that has not been used within 30 days. Then schedule a reminder on the calendar every 90 days to go over the list again. The small amounts of charges add up quickly over the course of a year and people are usually amazed by the amount they have forgotten about.