Budgeting for Young Adults: Real Examples That Actually Work

Why Budgeting for Young Adults Feels Impossible (And Why It’s Not Your Fault)

If you’ve tried budgeting and still failed, I want you to know this; you’re not a bad budgeter. This is not a system that ever was ready for you. Financial literacy is not taught in most schools. No one explained to you after high school what taxes are or how much that student loan will cost you each month or how you’ll ever make ends meet in a place where rent is always going up.

It is for this reason that the recommendation of budgeting for young adults requires a different approach from the recommendations that have been followed.

Too many young adults, consistently more than 60%, continue to live paycheck to paycheck, a statistic that has not budged for more than 10 years. This isn’t a flaw in their personality. It’s the result of a generation of students taking on the debt of their student loans, the cost of rent and an inability to see any wage growth and then being expected to solve it all on their own.

This is what turned my head upside down: Budgeting isn’t a restriction of anything really. It’s about taking control of your finances and achieving financial freedom. This is the way to end the question of whether or not your credit card will be accepted at gas stations. Financial independence isn’t some distant goal. It begins with one decision – knowing where your money goes.

The Reality: You’re Not Bad With Money

The majority of people in the 18-24 age range have never had formal financial lessons (a problem that could be solved by starting budgeting education during the teen years).

This is not a opinion, it is a fact. This is a real education shortfall that causes young adults to struggle with money and deal with a career and life.

The economy isn’t helping, either. Federal student loan data reflects that the typical student loan debt is approximately $39,000 with an average interest rate of around 4-6%. In so many cities, rent consumes 40% or more of take-home pay. Add gig economy uncertainty and you have a generation facing financial concerns that traditional budgeting tips can’t account for. This then was never going to feel relevant, as it was meant for a different economic age. Because it isn’t.

The ability to care for the financial aspects of life is not an inborn trait. It’s something that you can create one month at a time, with the proper system.

The most frequent request I receive from parents is how to get the budgeting to stick with young adults without it being a lecture. The short answer is: Give them the actual numbers. You can’t learn more about financial responsibility in your life than by using real-life examples of take home pay, real-life breakdowns of your expenses, and real-life examples of a budget. It’s that this guide’s on the design to give you that.

Why Generic Budgeting Advice Fails Young Adults

Most budgeting guides make some assumptions: that you have a stable income, no major debt, and that you are in control of your spending. However, when you’re a Gen Z or Millennial having to deal with student loans, gig work, side hustles and the constant message of the comparison culture you may think that is useless.

It’s harrowing enough as it is, with the subscription trap. Streaming services, cloud storage, food delivery apps, gym membership, buy now pay later services. These small charges are all adding up to hundreds of dollars a month that go unnoticed by anyone as insignificant on their own.

Young professionals deserve budgeting tips that are relevant to their life. This guide is for you if that’s you.

Your First Paycheck: Why It’s Smaller Than You Think

My first job was entry-level, so when I see my actual paycheck, I would be like, “What’s wrong with payroll?When I get my first job, my first paycheck after I’ve actually gotten a job, I’m like, “What’s the matter with pay?” The number in my offer letter and the number in my bank account were very different!

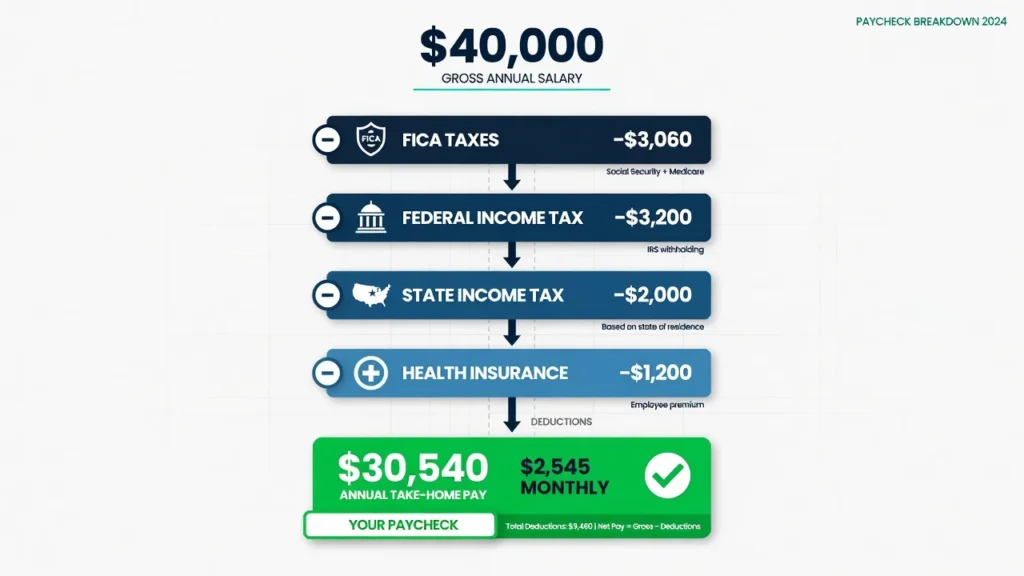

No one will tell you about this. The gross salary is the amount of money that you will see in the job offer. That’s a totally different number if you subtract out what the government and your employer have collected. FICA taxes (Social Security and Medicare) withheld as soon as the income is earned. On top of that there are brackets for federal income tax. The additional state income tax depends on where you live, but is about 5% in most states. If you have health insurance from your employer, those premiums are taken out of your paycheck before you see the funds.

With a $40,000 salary, you will get approximately $2,545 per month in actual take home pay, and $30,540 per year. This is the number to create your budget around. Not $40,000. Not $3,333, as you may think, by dividing by twelve. $2,545. One of the 101 ways to learn about money management as a young adult starting out is to budget from your take-home pay, not your offer letter.

Understanding Your Net Income (Take-Home Pay)

Let me put this in terms that are concrete. With a Gross Salary of $40,000:

FICA (Social Security and Medicare): $3,060 off

Federal income tax (estimated): -$3200

Expenses – State income tax (estimated 5%): (-2,000)

Lower health insurance premiums: $1,200 off

Retail sales: about $2,285 per month

This is the actual number. All budgets, all savings objectives, all category allocations begin here.

A simple way to earn more money each month without a pay raise is to change the withholding of your W-4 from your employer. When you are consistently receiving a large tax refund every spring, it’s the same as giving the government an interest-free loan all year long. Making some budget changes to send fewer dollars to your allowance can mean $50 to $200 more in every paycheck.Making a few changes in your budget to withhold fewer dollars from your allowance can mean $50 to $200 more in every paycheck.

Fixed vs Variable Expenses: What You Need to Know

There are two types of expenses: fixed and variable.

The first step to creating a budget is to know the difference between two kinds of expenses.

Fixed costs are a constant amount each month. This includes insurance premiums, student loan payments, car payment, and rent. You can foresee these just fine.

Variable expenses (also known as variable costs) fluctuate from one month to the next. Food, gasoline, electricity, restaurant and movie expenses all rise and fall. There are some months when you spend more. Some months less. The difficulty with these kinds of monthly expenses is the ability to create a realistic average instead of a unrealistically low number.

Knowing these differences is important because you will be treating them very differently. Once you’ve categorized your expenses, you can focus on strategies to reduce your monthly expenses without cutting essentials.

4 Budget Methods That Work for Young Adults

There is no budget system for everyone. The best one is the one that you’ll use regularly, rather than the most complicated one. Regardless of which method you choose, all successful budgets share key components of successful budgeting like realistic goals and consistent tracking.

I’ve narrowed down the four most practical choices here, as the method you choose to budget with is going to be based on your personality and your natural relationship with money.

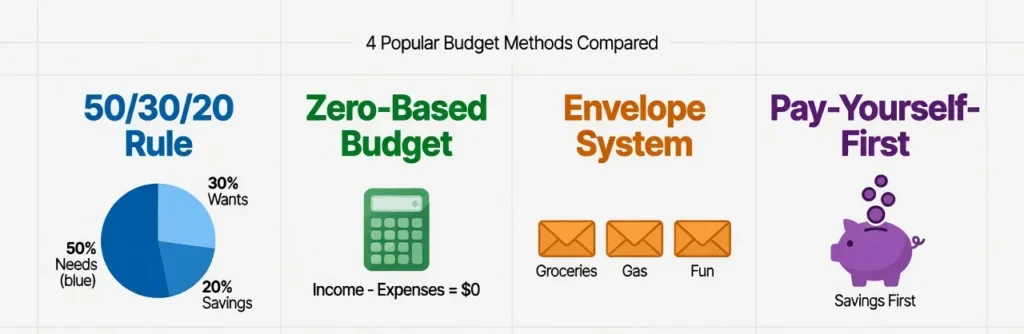

The 50/30/20 Budget Rule (Best for Beginners)

This is the easiest budgeting method and is the place to start for most young adults taking their first steps.

Under the rule, your take-home pay is split into three categories:

50% to needs: Rent, utilities, groceries, minimum debt payments, transportation

30-39% wants: Dining out, entertainment, subscriptions, hobbies, personal care

Make payments towards your debt and savings a priority. If you use the example of monthly take-home pay of $2,545, you’ll see that $1,272 is going to your needs, $763 is going toward your wants, and $509 is going toward your financial future each month.

The 50/30/20 budget rule is so effective for beginners because it is so easy to understand. There are only three types of categories to deal with. Not keeping all your grocery receipts. You don’t have to wonder if coffee is food or entertainment. For step-by-step implementation instructions, see our comprehensive 50/30/20 budget guide.

Zero-Based Budgeting (For Detail-Oriented People)

Zero-based budgeting means that each and every dollar has a specific use that must be recorded until the money runs out. That does not mean that you spend all of your money. It’s the idea that every dollar should serve a purpose – rent, food, savings, debt repayment, emergency savings.

A method which is hands on, and allows you full control. Zero-based budgeting is for those who want to know where $18 was spent on Tuesday evening. Control is more time consuming, but is very satisfying for many.

The problem is that it’s quite daunting to start with to decide on a spending limit for each and every possible type of expenditure. Begin with 10-12 categories and then go from there.

The Envelope System (For Overspenders)

The envelope system sets a hard limit in certain categories, where you are sure to overspend.

At the beginning of the month, you withdraw money in your bank account, and split it up into envelopes for food out, coffee, gas, entertainment. Once the envelope is empty, it’s the end of the month for spending in that category. No exceptions.

This is a strong psychology effect. When you hand over cash and see the envelope empty, it feels real and tangible – swiping a card just doesn’t do it. This is the best method for particular spending issues; no other application can be as effective.

Pay-Yourself-First Method (For Natural Savers)

You’re the type to keep your purse or wallet in check easily but saving money is just a second thought, this is your technique.

Once you receive your paycheck, your savings goal – usually 20% or more – is instantly transferred to a dedicated savings account. If so, then you save and spend what is left.

Make an automatic transfer so that you never even see the funds in your checking account. What you don’t see, you don’t remember.

Alternative: The Give/Pay Yourself/Live Framework

If you prefer a values approach, you can use the following order: you give 10% to charity, a cause you believe in, or someone who needs help; you pay yourself 10% of your income – split between long-term and short-term savings; you live off the rest, 80%. It develops financial responsibility, and something most budgets neglect the habit of giving.

How to Create a Budget as a Young Adult: 30-Minute Action Plan

No need to be a finance professional. There is no requirement to read 3 books before. With a little bit of time, and just your bank statements, you can have a budget that truly represents your reality in about 30 minutes. (If you prefer a more detailed budgeting process, we have that too, but this quick-start version works for most people.)

Your first budget will not be a foolproof one. This is not a must. The aim is to begin with something real and enhance it monthly.

Step 1: Gather Your Last 3 Months of Transactions

Log in your bank account and credit card accounts. Get the last 3 months of trades. Just don’t make judgements as you scroll. Simply gather the data.

This is very important as most people vastly underestimate their expenditure. You don’t really spend what you think you spend. The statements show you what’s really happening.

Step 2: Categorize Everything

For each transaction, categorize it. A decent initial package:

Housing (rent, renters insurance)

Transportation (Car payment, gas, insurance, parking, public transportation)

Food: Groceries

Food: At the table, takeout, and delivery Electric, Internet, TelephoneDebt payments (Student loans, credit card minimums)

Users subscribe to the streaming services, apps, and software.Streaming, apps, and software are subscribed.

19.9% of the total expenses were allocated to entertainment and personal spending.

Shopping and clothing

Everything else

Total up the amounts for each category over three months and then divide by three to find the average per month.

Step 3: Calculate Your Real Numbers

List each of your monthly averages. Compare the total to your monthly take-home pay.

If expenses are greater than income, you’re going into debt each month. When income increases, that is your actual disposable income the money you have for savings, debt repayment, and other spending. This is the starting reality, though uncomfortable number.

Step 4: Set Your Budget Categories and Amounts

If you’re going by the 50/30/20 rule, spend your take-home pay with your actual spendings, not what you would like to spend.

For example, if the monthly budget for groceries is $350, then the target of $150 will be reached by the end of the second week. So set $300, and gradually lower it over the course of a couple months. The aim is for improvement over the long term, not a drastic cut that will be abandoned before the end of the month.

Step 5: Set Up Your Tracking System (Choose One)

Choose one tool and get it up and running today. A comparison of all the options is located later in this guide, but here is a quick reference guide to get you started:

YNAB ($15/month): Transactions are entered in manually, so you are aware of every purchase made. Ideal for individuals who prefer control.

Monarch Money (free for one month, then ~$15/month): Links to your accounts and sorts transactions automatically. Best for Auto lovers.

Google Sheets (free): Totally adaptable. The best for people who wish to create their very own system without having to pay monthly charges.

Cash envelopes (free): These are envelopes with cash for problem categories. Best for overspenders.

The best personal finance app is the one that you use weekly.

Sample Budgets for Young Adults: 4 Real Examples with Dollar Amounts

Where most budgeting guides fail. They are teaching the theory, but never they are going to show you what a budget is like with real dollar amounts in your situation. Here are four sample budgets for young adults that are based on four different income and life situations.

Please note, all of the numbers in this Budget Example are taken from the most recent federal budget.Note: All numbers in this Budget Example reflect the latest federal budget.

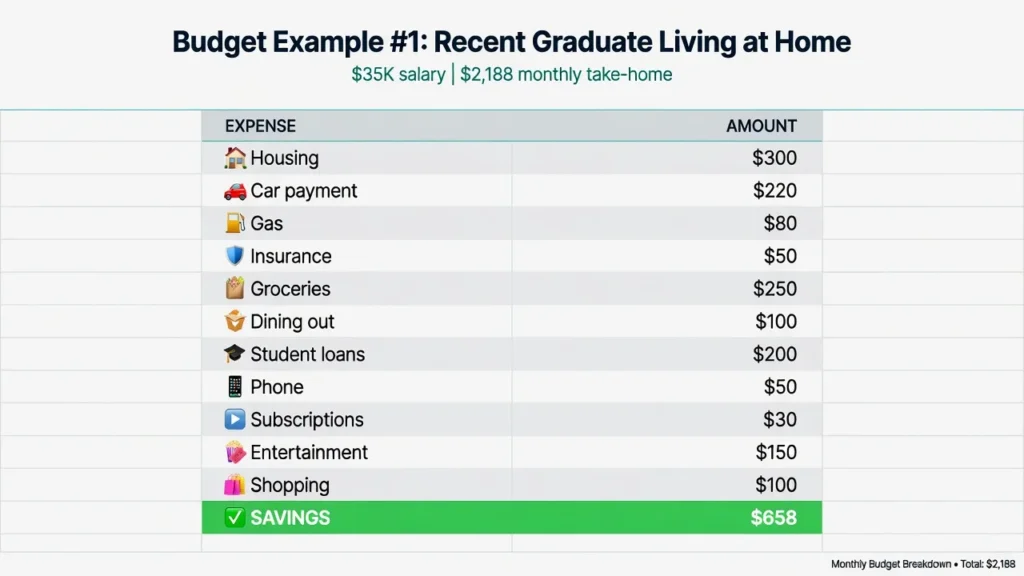

Budget Example 1: Recent Graduate Living at Home ($35K Salary)

Gross salary – $35,000 per year, Take-home pay – around $2,188 per month

| Category | Monthly Amount |

|---|---|

| Housing (contribution to parents) | $300 |

| Car payment | $220 |

| Gas | $80 |

| Car insurance | $50 |

| Groceries | $250 |

| Dining out | $100 |

| Student loan payment | $200 |

| Phone | $50 |

| Subscriptions | $30 |

| Entertainment | $150 |

| Shopping | $100 |

| Savings | $658 |

The biggest reason why it is possible to save aggressively here is that you’re living at home, so you don’t have rent to pay, which can be 25% to 35% of a young adult’s income. With this rate of saving, you’ll be able to save a $10,000 emergency fund in about 15 months. From there, it can be used to pay the car loan sooner, to save for the first time to pay for the first apartment, or for a combination of the two.

It is not “failure” to live in a household with parents. It’s one of the cleverest financial decisions that a new graduate can make when thinking about what to do with their money with a clear objective and a timeline.

Budget Example 2: Young Professional Managing Roommate Expenses ($45K Salary)

The gross salary is $45,000/year, with a take home pay of around $2,813/month.

| Category | Monthly Amount |

|---|---|

| Rent (split with 2 roommates) | $850 |

| Car payment | $180 |

| Gas | $100 |

| Health insurance | $70 |

| Car insurance | $50 |

| Groceries | $300 |

| Dining out | $150 |

| Utilities (split) | $80 |

| Phone | $60 |

| Student loans | $300 |

| Subscriptions | $45 |

| Entertainment | $120 |

| Gym | $40 |

| Shopping | $80 |

| Savings | $388 |

Here, rents make up a full 30% of take-home pay, and utilities costs are shared with roommates and kept under $80. Currently, savings are 14%. If it’s around 20 percent, then you are around $453 per month to save if you cut out $50 of dining and one streaming subscription. That’s a significant progress towards the 20% without changing your lifestyle.

Budget Example 3: Solo Renter Paying Off Debt ($50K Salary)

The gross salary of $50,000 a year is approximately $3,125 per month.

The list is not mutually exclusive, and you can try to gradually increase any amount you can afford.

The categories are not mutually exclusive, and you can attempt to gradually raise any amount you can afford.

| Category | Monthly Amount |

|---|---|

| Rent (1-bedroom) | $1,100 |

| Car payment | $250 |

| Gas | $100 |

| Car insurance | $50 |

| Health insurance | $100 |

| Groceries | $350 |

| Dining out | $150 |

| Utilities | $150 |

| Phone | $65 |

| Student loans (aggressive) | $450 |

| Credit card payoff | $200 |

| Subscriptions | $35 |

| Entertainment | $100 |

| Savings | $25 |

This individual is choosing to pay off their debt instead of saving money, and that’s a good idea, especially if they have debt with high interest rates. So the $200 balance is transferred straight to the emergency savings fund once he’s finished paying it off in about 10 months. The student loan debt decreases further and further, thus increasing savings. The way forward is straight and the times are clear.

Budget Example 4: Freelancer with Variable Income ($40K to $60K per year)

Average monthly income range: $2,500 – $6,000 Strategy: Use the LOWEST month

Baseline budget (critical expenses only):

| Category | Monthly Amount |

|---|---|

| Rent | $900 |

| Utilities | $100 |

| Groceries | $300 |

| Phone | $50 |

| Insurance | $150 |

| Minimum debt payment | $200 |

| Total Baseline | $1,700 |

| Income buffer (savings cushion) | $800 |

The baseline budget is a contingency plan. It specifies exactly what you need each month regardless of what. This number is your bottom line if you’re in the gig economy. All the above is a conscious decision.

Budgeting with Irregular Income (Gig Economy and Freelancers)

The general budgeting tips come with the assumption that you have a set salary that you receive on the 1st and 15th of each month. That doesn’t work for those who are freelance, a rideshare driver, or whose income for a side gig isn’t consistent from one month to the next.

If your income is variable, then you need a system all on its own, one that is based on your floor income and not your average.

The Baseline Budget Strategy

First, list all of the key costs: mortgage, utilities, groceries, minimum payments on insurance, minimum debt payments. Add them all up. This total is your starting point. Your base answers the question of what is the least amount that you have to make a month to pay your rent and utilities and have a roof over your head? This is your bottom line income. All of your spending begins here with your money.

Only budget baseline expenses as committed expenditures. All other uses, such as eating out, entertainment and additional debt repayment, or spending money on unnecessary items, are options.

Building an Income Buffer Account

If you have enough extra money to put into a separate buffer account, do so in months when you have extra money to put in. It is like a personal income stabilization fund.

If you have a “buffer” account, then if your income doesn’t cover your basic expenses, you don’t have to pay off any credit card debts that you’ve accumulated in the previous month. Stick to the one to two months of “normal” living for this account, and then make a concerted effort to save every other dollar.

Allocating Variable Income

As far as I can see, each month can be classified as falling into one of three income categories:

Low month (income at or below baseline): Fund baseline expenses only. No wants, no additions. This is essentially budgeting on a low income—covering only what’s absolutely necessary until your income rebounds.

Average month ($500 to $1,000 more): Spend baseline and make a small savings contribution, add some modest wants.

Strong month (baseline + $2,000 or more): Full wants budget, buffer account top-up, aggressive savings, cover baseline.

After you’ve classified the month based on income, you always know what to do with your money. The transparency eliminates much of the uncertainty of income fluctuations.

Building Your Emergency Fund (Start With $500)

The emergency fund is your first savings goal, ahead of retirement funds, investments, and aggressive debt payoff. The answer is simple; if you don’t have one, then any car repair, medical expense, or unexpected expense is just a new loan that you are charged interest on.

The first time I had a real emergency fund, even $500, immediately there was a psychological difference. A $400 auto repair became a minor bother. That’s a hard thing to explain until you know it.

Why $500 First, Not $10,000

If you get advice from financial advisors to save three to six months of living expenses, they’re on target about the place. For the average, or average-ish, person, that seems like a long shot and is generally demoralizing to work toward. Start with $500.

Most emergencies in real life are provided for: a flat tyre, a broken phone, a visit to urgent care, car repair bill. Makes an economic emergency an inconvenience.

Once you have $500, push to $1,000. Followed by one month of costs. Build from there. The secret is to begin with a number that seems attainable.

Where to Keep Your Emergency Fund

A high-yield savings account is the right home for your emergency fund. While rates fluctuate, high yield accounts have historically offered much higher rates than a typical checking account and your emergency fund will increase while it remains in the account.

Never place it in your checking account. Too easy to spend, too easy to get. Don’t put it into the stock market. Markets move having to swap in and out of the fund, not just spend it, is that small friction that keeps casual raids off the fund. Best kept at a different bank from one’s main checking.

The Automatic Transfer Strategy

Make sure that your emergency fund savings are set up to receive automatic transfers from your checking account on payday. With no effort, $50 a paycheck adds up to $1,300 in 13 months.

Automation is effective because it take the choice away. There’s no need to have to remember. There is no need to be motivated. Without you needing to think about, the cash shifts on payday and on each payday.

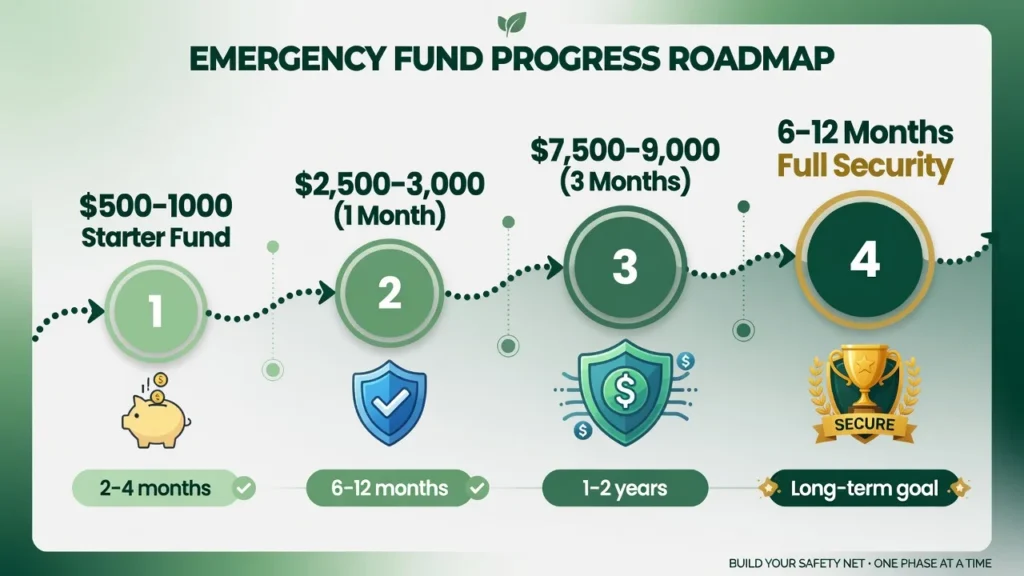

Progressive Emergency Fund Targets

The creation of the emergency fund is not an event. It is a process that takes place in stages:

Phase 1: $500 to $1,000 starter fund. This should be done in 2-4 months.

Phase 2: One month’s worth of running costs (typically $2,500 – $3,500 for most young adults). Take 6-12 months to complete.

Phase 3: Expenses for 3 months.

Goal #1-2 years.

Phase 4 = 6-12 months of spending. Goal of financial independence in the long run.

Every step you take takes you one step closer to a more stable and less stressful financial future.

The Psychology of Budgeting: Why You Struggle and How to Win

It’s not a conversation about the emotional part of budgeting. Worry about seeing how bad the numbers actually are. The frustration when other people spend freely and you are conservative with your money.

The anger when your friends are spending money when you are saving your money. The shame if you fail a category and ask yourself, “Why am I not cut out for this? The remorse when you fail at a category and ask yourself, “Why am I not cut out for this?

They’re genuine, they’re widespread and that is why most people are simply giving up on budgeting after the first few weeks.

I’ve seen people give up on a budget on a system that is absolutely fine, but because no one informed them how uncomfortable they would be the first month that they have to actually look at real numbers. Well, indeed, this section’s about that.

Overcoming the Fear of Looking at Your Numbers

Don’t squirm out from your bank statements because they won’t get smaller. It makes it grow.

When it comes time for the real numbers, something happens. The fear of the unknown that is often greater than the actual reality is eliminated. Clarity takes the place of what it has replaced. First of all, clarity is the ingredient of any turnaround in the finances.

Data is your current financial situation. It’s information. It’s not about your intelligence, it’s not about your value and it’s not about your future. Bankruptcy is overcome by people. Individuals have six-figures bills on regular earnings. The numbers are only a starting point, no matter how they read on today.

Building financial confidence – and the ability to actually achieve your financial goals – is done by facing reality, not running away from it.

Dealing with FOMO and Friend Comparison

Everyone’s highlight reel is displayed on social media. The pal who heads out each weekend and blogs on their favorite new restaurant could be a credit card bill payer you are not aware of. They may be receiving monetary assistance from their families. They may earn a lot more than you do. You really don’t have any idea.

There are no two ways to do it: You will never be happy with your budget sheet when you look at someone’s Instagram.

Your budget is based on your goals, your values and your situation. Focus there.

If pressure is getting high, offer low-cost options: potluck meals, hiking, free days at the museum, parks, home movie night. A budget is no barrier to good friendships. Those that only function when purchasing something you can’t afford are worth a look.

Budgeting as Freedom, Not Deprivation

The mindset shift that makes all the difference: Budgeting is not “I can’t afford this. It’s “I’m going to spend money on what is important to me.”

Of course, every dollar that you spend on an impulse buy is a dollar that you aren’t spending on the things you want to do in life: that trip that you’ve been wanting to take, that apartment that you’ve been wanting to move into, that job that you’ve been wanting to leave, that financial independence that allows you to make decisions based on your values rather than necessity.

The best gift that you can give yourself is financial stability. It feels ok to be living ‘paycheck to paycheck’ until it doesn’t. Options are what money saved provides you with at the day you lose your customer, face a medical bill, or just want to take a chance on something you love.

Avoiding Lifestyle Inflation as Income Grows

There is one financial pitfall I’ve seen people get into that they don’t realize until it’s too late:

They get more money, their lifestyle goes up, and six months later, it doesn’t really change. It’s lifestyle inflation and this is the single greatest reason for people with good incomes having little or nothing to show at the end of the month.

If your salary goes up, don’t immediately upgrade everything! Maintain a similar level of housing, transportation and discretionary expenses. Put the additional money into savings, investments and debt repayment. This one habit will have an amazing effect over 10 years!

You don’t need to make more money to do a good job of financial management. It calls for withholding a greater share of your income.

What to Do When Your Budget Fails (Because It Will)

The first budget you make is going to be a bust. Yep, probably your second one as well. That’s not pessimism. It’s the nature of learning any new skill. It is not a question of failure. It is what you do after!

Scenario 1: You Overspent in One Category

This will happen. You go on a date for someone’s birthday, and at the end of the month find you are $80 short of your restaurant allowance. Go out for someone’s birthday, and at the end of the month find you are $80 over your dining budget.

Solution: transfer $80 from a different flexible spending option to pay for it. Perhaps this is due to your clothes money or your entertainment allowance. Take the punishment: You do not purchase new clothes during this month.

Next, determine the cause of the overspending. Did you originally budget less than you need? Does meals out consistently become an issue that needs the cash envelope system? This was a “one-time exception”? Next month use the information to impose more stringent spending limits.

Scenario 2: Unexpected Expense Hit

Car repair. Urgent medical bill. Flight home for a family situation. These are the reasons your emergency fund was created.

Use a starter emergency fund. That is what it is all about. Then, reconstruct it over the coming few months.

If you don’t have an emergency fund set up yet, make this month’s budget change now! Eliminate all desires categories to the bare essentials. Cover the emergency. Learn from this painful experience and make up that $500 starter cash before it happens again!

Scenario 3: Your Budget Was Too Restrictive

If you cut your grocery spending in half on day one, you’ve set yourself up for failure. Dramatic cutbacks do not usually “take” and are likely to earn resentment, not discipline.

Make smaller adjustments. Cut eating out expenses in half, but not in six. Allow yourself a small entertainment allowance. If it’s not a budget that’s viable, then you’re going to give up on it in three weeks.

An 80% ideal budget but that is sustainable long term is better than a perfect budget that you give up after a month.

Scenario 4: You Lost Motivation

A fortnight on, you were keeping an eye on all the things. It has been 3 weeks since you opened your budget app. This is very typical.

Reconnect with the reason you started. What were you saving up for? A certain financial objective, a sense of security, the ability to quit a job that is not enjoyable? Write it down and put it somewhere you will see it every day and not in a notes app.

Visual progress is more beneficial than many realize. You can’t build the momentum with abstract numbers, but you can do it by showing a chart that shows your emergency fund from $0 to $200 to $500 to $800.

Be sure to consider how much of your budget still needs daily decisions. The more the system can be automated, the less will-power you will use and the less likely you are to be able to “stealth” off.

Scenario 5: Your Income Changed

Lost employment, cut hours, lost big freelance job. If your income decreases, go straight to the “base budget. Essentials only.

If needed, use your emergency fund. Explore other avenues of income: gig work, part-time jobs, freelance work. After your income has stabilized, make your budget based upon the new income level instead of hoping for that old income level to come back.

Your budget must be in keeping with your life, not your vision of what it should be.

12 Budgeting Tips for Young Adults That Actually Work

These, these are the tactics that actually make a difference and I’ve found to be quite useful, not the same generic advice that you’ve heard a hundred times. Some are on the subject of saving. Some are about thinking about money differently. They are all right here and all down to earth.

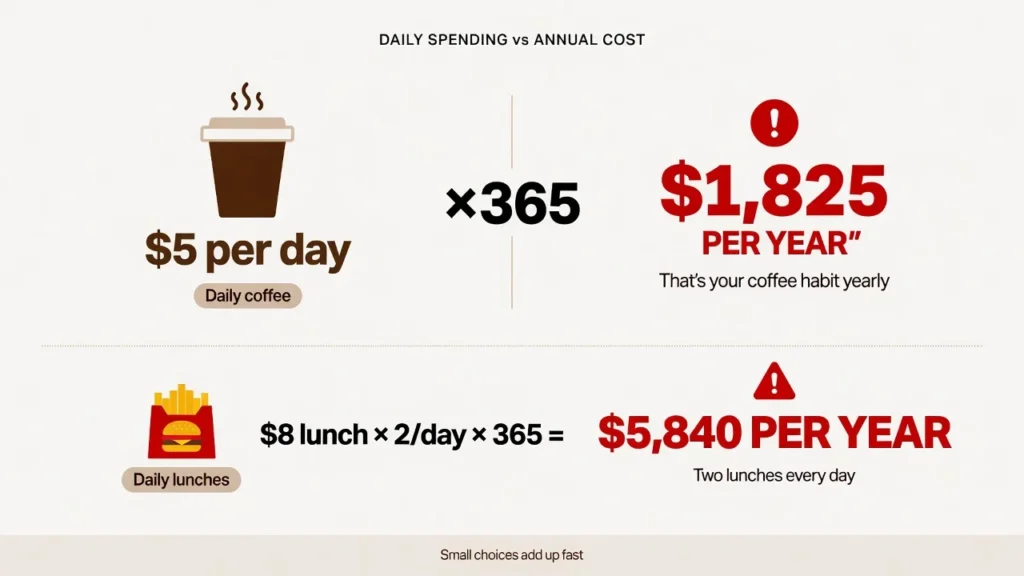

Tip 1: Calculate the Yearly Cost of Daily Habits

A daily cup of coffee costs $5, which equals to $1,825 per year. If you are buying an $8 fast food lunch twice per week, that’s $832 per year. They are small purchases, which seem innocent to the individual. They are computed every year and give rise to the “aha moment” which many young adults need to reconsider their habits.

Not all coffee needs to be given up. Only understand the true annual expense before determining whether it is worthwhile.

Tip 2: Use the SODAS Method for Big Purchases

If you are buying something that is more than $100, go through this framework before you buy it:

S: What’s the Situation? (Which item am I thinking about purchasing and why?)

O: What are my Options? (Purchase, wait, purchase used, do not purchase, purchase something lower in price)

D: What are the Disadvantages of each option?

A1: What benefits do you see with each choice?

S: What’s the Solution?

This 5-step program helps change impulse decisions into conscious choices. The majority of purchases that make it through the SODAS process really are worth purchasing.

Tip 3: Itemize Your Splurges

If you are keeping a tab on your dining out category, make sure you don’t simply record “dining out: $240.” Record each transaction: Chipotle- $12, Coffee Shop- $6, Pizza Delivery- $35, Brunch- $47, Sushi- $38.

Multiple mentions of restaurant names is a psychological barrier. When you have a picture of your spending habits, it is easier to see that you can’t keep spending without thinking.

Tip 4: The Physical Savings Box Trick

If you have a tendency to make regular withdrawals from your digital savings accounts, have a physical cash savings box at home too. A box can be opened in a matter of taps on your phone, but a seal or a box can break apart.

This strategy has enabled individuals to save $10,000 over a period of five months by keeping the money inaccessible, except when essential needs are met.

Tip 5: Never Buy on Discount Unless You Already Wanted It

“50% off” does not equal “savings. It’s saving you money that you’re not used to spending. If you spend $150 on sale items you weren’t planning to buy, you spent $150 that you didn’t need to spend!

The trick is to wait for items that are already in your shopping list to go on sale, and not purchase items due to discounts. If it’s a sale, it’s not a smart choice if it’s an impulse buy.

Tip 6: The Debt Payoff Decision Framework

Not every debt is created equal. A great first step is to understand what your debt-to-income (DTI) ratio is, which is your total monthly debt payments compared with your monthly take-home pay. If it is more than 35% don’t focus on paying off debt, but instead focus on other priorities like paying off your car. Now it depends on the interest rate and what you miss out on. I believe it’s in three levels:

Any debt with interest rates greater than 6% (credit cards and private loans): Do this first. The elimination of this interest is a sure thing and more than most investments.

Medium interest debt (4% – 6%): Work to reduce the debt and still earn the employer match on 401k contributions.

If you are in debt with an interest rate of less than 4% (most federal student loans): Pay off as much interest as you can, but invest the rest, as the market has outpaced this interest rate over the long haul. For specific student loan payoff strategies, including income-driven repayment options and forgiveness programs, see our detailed guide.

Tip 7: Good Credit Score Equals Real Savings

So, using standard mortgage amortization calculations, a .5% difference in mortgage interest rates on a $400,000 mortgage saves about $44,000 over a typical 30-year mortgage term. This is the monetary repercussion of your credit score.

Establish good credit from the start in your 20s by paying credit card debt in full each month. Your credit utilization ratio (the amount of credit you’re using versus the amount of credit you have available) makes up approximately 30% of your FICO score. Utilization of less than 30% and preferably less than 10% is the quickest way to increase your score.

Tip 8: The $250 Per Month Wealth Gap

The power of compounding, when you save just an extra $250 a month for 10 years from now until you retire, is incredible. That extra 10 years of savings can be hundreds of thousands of dollars more when it comes to retirement.

Saving $100 in your 20s is about ten times as valuable as saving the same $100 in your 50s. Start small. Start now.

Tip 9: Increase Income, Not Just Cut Expenses

Budgeting can be used both ways. Reducing expenses matters. Increasing income is just as important.

Ask for raises. Learn higher-paying skills. Create an extra stream of income for yourself that brings in just $300-$500 a month. An increase in income of 10 percent can help you more than do extreme spending reductions which you cannot sustain.

Tip 10: The 24 to 48 Hour Rule for Impulse Purchases

If the item is not essential (under $50), then put it in your shopping cart or save it to a wish list. Then close browser window, and wait 24-48 hours.

If you still desire it, if within your budgets, and if you are thinking it through, purchase it. Just often the impulse dies down. Almost no sacrifice, hundreds of dollars saved per year.

Tip 11: Automate Everything Possible

Saving transfers, paying bills, paying minimum debt, saving for retirement. Automate all of it.

By eliminating repetitive will decisions that cause slip-ups, automation helps. It’s set and will run. You no longer incur late fees. You never forget to save for college again.No more saving for college! You no longer make emotional purchases on money that you already have planned to spend.

Tip 12: Learn to Cook, Actually

Not “eat at home, rather than out.” This will serve them for about 2 weeks, and then some resentment will set in.

Really create 5-7 simple recipes that you can truly enjoy preparing. Cooking is a skill and a way to care for yourself, not a punishment for lack of funds. Eating out is not a way of getting out of your own way of cooking if you love what you are making at home.

The savings are significant. More importantly, the behaviour sticks.

Best Budgeting Resources for Young Adults (Apps, Tools, and Free Templates)

Best Personal Finance Apps for Tracking

Monarch Money (Free Trial, then around $14.99/month) – The best automated tracking application around these days. Links to your accounts (bank and credit card), auto-categorizes transactions and provides a full-customizable visual spending dashboard. No ads, cleaner interface than older tools and really useful trend reporting. A worthwhile investment for automation without any compromises.

YNAB — You Need A Budget (around $15/month) best for those who want to be as aware as possible about how they spend their money. You manually enter transactions – this means you always know what you have bought. Zero based budgeting approach: Each dollar is assigned a purpose. There is a learning curve and the monthly fee, but many users say it pays for itself the first month since it brings to the surface expenditures they had not noticed.

Copilot (iOS only – around $13/month): A neat, speedy service for iPhone users who wish to have tracking done automatically, but with an extremely nice user interface. Great for seeing where money is going at a quick glance and not overwhelmed by data.

For simple zero-based budgeting, EveryDollar (Free and Premium versions) is best. The free version can only be entered by hand. Clean, simple interface. Suitable for those who appreciate structure but don’t want complexity.

Best for knowing how much money you have remaining after paying your bills and after you have met your savings goals is PocketGuard (Free and Premium). A good solution for those who want to know if something is OK to purchase at any given time.

Note: App features and price may vary. Be sure to check the latest rate and availability before committing to any subscription model with a paid tool.

Free Spreadsheet Templates

If you are looking for a 100% customization but don’t want to pay a subscription, a free budget worksheet in Google Sheets is a great choice and it can be more flexible than any app. Well-designed templates are available for an easy search, or can be created from scratch, based on categories that correspond to real-life situations.

One good point of using a spreadsheet is that you can control everything. The downside is that it takes more work to do, and it doesn’t link to your accounts automatically.

Browser Extensions for Spending Awareness

Some great features of the Honey and Rakuten integration at checkout include the ability to find and apply coupon codes automatically, and the ability for the Rakuten to return cash back for eligible purchases. Trim detects when a subscription is recurring and can help cancel unused subscriptions. These do their job silently in the background and make savings without significant behaviour change.

Physical Tools (Envelopes, Cash Box, Budget Binder)

Physical systems are good for learners who prefer to learn through physical manipulation and are not used to digital systems. All that is needed for a cash envelope system is cash envelopes and categories. The physical savings challenge box makes it harder to make spontaneous withdrawals. For some, a budget binder with printed out monthly pages gives them the chance to delve deeper into the numbers than a pho

Common Budgeting Mistakes Young Adults Make (And How to Avoid Them)

Mistake 1: Budgeting Based on Gross Salary Instead of Take-Home Pay

Making mistake #1 is when they allocate a budget based on their gross salary rather than their take home salary. Mistake #1 is where they budget based on gross salary instead of take-home salary. A $40,000 salary is not $40,000 to spend.

Once you subtract the taxes and deductions, it’s more like $30,000. When you create a budget using your gross income, you are making 25% too much each month and saying to yourself, “How is it that I am always spending more than I make?

Always use actual income; what you see in your bank account.

Mistake 2: Trying to Match Friends’ Spending

You have no idea what your friends are doing with their money to make ends meet; or whether they are going on credit; or whether they’re earning more than you. They’re spending money according to their situation, not yours.

Keep it with yourself and your own individual situation.

Mistake 3: Not Having Any Emergency Fund

If you don’t have an emergency fund, then an unexpected bill is paid with your 20% interest credit card bill. If the car repair costs $600 and takes a while to pay back off, it will cost more than $720.

Even $500 is the turning point. Start there.

Mistake 4: Carrying a Credit Card Balance

Credit card interest rates usually fall within 18% to 30% or more, depending on the particular card and credit history. A balance is the amount you are paying a lot of interest from each year.

If you are not able to pay off your credit card debt each month, then you are spending money that you don’t have. Avoid using credit for purchases that you don’t have cash for in your checking account. If you’re already carrying a balance, learn how much credit card debt is too much to assess whether you need urgent debt payoff action.

Mistake 5: Lifestyle Inflation

Each raise is a chance to increase your wealth or to get used to your increased spending. Most people opt for the latter without much thought, if any.

If your income goes up, try to keep your minimum or essential expenses the same and try to save and invest the additional income. This is the best wealth building strategy anyone on an ordinary income can have.

Mistake 6: Buying Things Because They’re On Sale

A discount on something that you hadn’t planned to buy is not a saving. It’s a purchase that sounds like a profit. Real savings are only from sales on items you have on your list.

Learn to see the urgency as a tactic being used to sell you something and not just “on sale” when you see it written like that.

Mistake 7: Not Taking Employer 401k Match

Your employer matches your contribution at 3% and you contribute at 6%, then you’re getting a 50% return on your contribution. There’s no investment that does as well.

Always make the minimum contribution to match the employer. Each dollar that passes you by isn’t a dollar that is yours.

Mistake 8: Using Buy Now Pay Later Services

Affirm, Afterpay, Klarna and others allow for the purchase of items you don’t have the money for at this moment in time. They do this by breaking up payments over weeks and weeks and make the full price less of a psychological ordeal.

This leads to indebtedness that isn’t obvious. You may be paying for four different services, but not realize that you’ve already paid for part of next month’s income. These services are designed to go against budgeting discipline. Save up for things. Practice purchasing at the time of the money.

Your Next Steps: Put This Into Action Today

You now have all the pieces you need for budgeting when you’re a young adult: how taxes affect your take home pay, what kinds of budgets work for you, examples of what actual budgets look like and actual dollar amounts, and what to do if you get off track.

You’ve got to start looking at your bank statements and doing the first half hour’s work, and you’ll have the financial confidence you’ve been looking for.

Here is the 7 day plan to get you from here to here:

Day 1: Log into bank account and credit cards. Download or Check previous 3 months of transactions.

Day 2: For each transaction, identify its category and sum up the average transaction amount for each category for the month.

Day 3: Decide on your budgeting system. For those who are just getting started, use the 50/30/20 rule.

Day 4: Set up your tracking tool. Make a YNAB or Monarch Money account or use the Google Sheets template.

Day 5: Develop your budget categories and put in a realistic dollar value in each category.

Day 6: Automate it by transferring it to another savings account, whether it’s $25 every pay, or just $5. On

Day 7, start recording your spending for the month and check your spending at the end of the week.

Being a young adult budgeter doesn’t have to be a perfectionist. There will be budget issues with your first budget. There’s a category you’ll miss out on, an item you’ll overspend and, of course, a category you’ll forget about. It is not the ones who don’t make any mistake that build financial stability. It’s those who adapt and persevere.

In 6 months, you’ll have a clear idea of where your money has been spent. A year in the future you will see that the toughest thing wasn’t the spreadsheet. Was the decision to look.

Frequently Asked Questions About Budgeting for Young Adults

Q: What’s the easiest budgeting method for complete beginners?

The 50/30/20 rule is the easiest to begin with. Half of your after-tax paycheck is spent on needs such as rent, groceries, utilities and the minimum debt payments. Thirty percent is for desires such as eating out, entertainment and subscriptions. 20% is put aside for savings and additional debt payoff. It’s much less overwhelming than more detailed methods because there are only three categories to deal with. After successfully using it for three to six months, if you wish to have more control, you can use something more granular.

Q: How much emergency fund do I really need as a young adult?

Start with $500 to $1,000. For most young adults, that’s what you’ll get in two to four months, and it should cover most real-world emergencies such as an accident with car repair bills or an emergency medical visit. After this cushion, expand to 1 month of expenses then 3 months. Work up to six to twelve months total security. What matters is to get a reasonable goal and begin now, not when you can save a big sum.

Q: How do I budget when my income changes every month?

Make a basic budget that includes only the essentials such as rent, utilities, essential groceries, insurance, and minimum debt payments. Calculate the total. What is the minimum amount you need to earn each month to get the basics? Use the lowest income of the last six months. During a normal or good month people have income in excess of that base and can use it for wants or accelerate their savings. Also establish a separate buffer account with one to two months of normal living expenses so as to cushion the impact of slow months.

Q: What should I do when I overspend in a budget category?

Don’t lose heart about the entire budget. Transfer funds from other flexible categories to pay off the over spending for the month. Do not avoid the consequence, such as having to give up another purchase for the month. Next, consider why it happened: Was the budget insufficient or is it a problem category that should be addressed through a cash envelope, or was it a one-time exception? Learning from it, fix a more successful expenditure limit next month.

Q: Should I pay off debt or save for an emergency fund first?

First build up your $500 to $1000 starter emergency fund. If not, each and every unaffordable cost will be a liability in your account. After that, pay off high interest debt with a rate exceeding 6%. Then, make enough extra contribution to your employer’s retirement plan to maximize the match; you cannot pass on that 100% return! When high-interest debt is eliminated, start to increase an emergency savings account to 3 months of living expenses, and then move to more aggressive savings and investing.

Q: Why is my first paycheck so much smaller than my salary?

There are a few required deductions that will take a bite out of your gross pay before it goes to your account. Social Security and Medicare taxes remove 7.65%, federal income tax can be 10-22% based on the tax bracket, state income taxes remove an additional 5% in most states, and health insurance premiums would further decrease the amount. The amount of $40,000 a year is about equal to $30,000 after taxes, or approximately $2,500 a month. Always plan on after tax income. When calculating based on gross pay, you will be spending 25-30% more than you need each month.

Q: What budgeting app should I use?

It will depend on your personality. If you prefer to have automated linking of your accounts and a graphical dashboard with minimal work, go with Monarch Money. If you’re looking for deeper engagement with every spend manually, then you’ll want to use YNAB because automation doesn’t allow for that. If you’re looking to fully customize your budget without any cost, then use a budget worksheet from Google Sheets. Regardless of the digital solution you choose, if you have an area that you spend more money on than you should, make sure to use physical cash envelopes for that item.

Q: Is living with my parents to save money a good idea?

Yes, if the relationship is healthy and you have a specific financial goal, and a time frame in mind. While most renters can only save 10% to 15% of their income, by living in a home you can save 30% to 40%. Help with the household finances, even if it is a small amount, in order to take responsibility and develop respect. Make the arrangement have a purpose and a date for moving out, whether 12 months or 24 months – not an indefinite time frame. If you develop good money-saving habits that time, they will stay with you after you move out.