How to Budget Money on Low Income: 7 Strategies That Actually Work

How to Budget Money on Low Income: Why Standard Rules Don’t Work (And What Does)

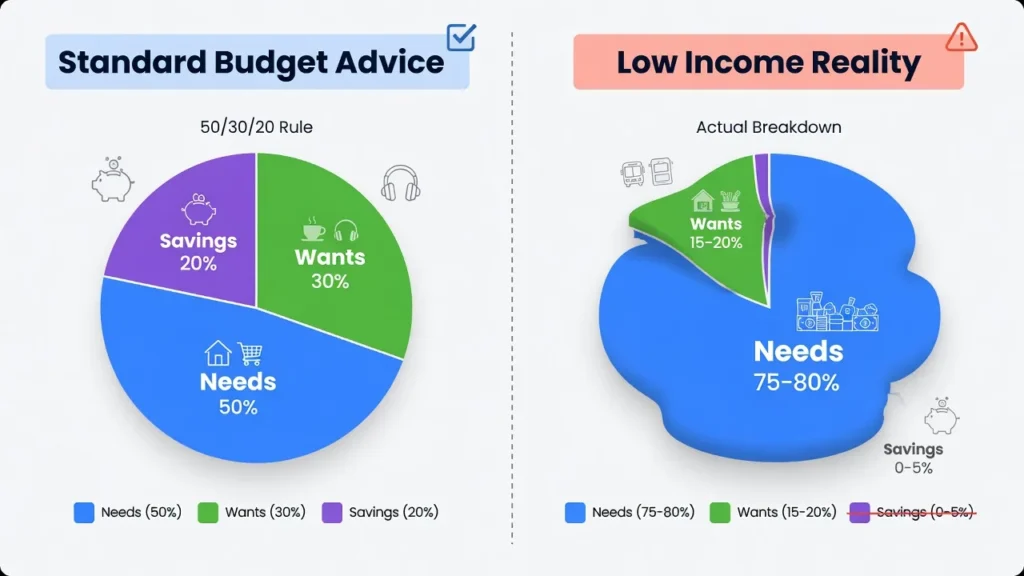

I remember the frustration of sitting at my kitchen table, trying to figure out how to budget money on low income, staring at yet another budget worksheet that simply didn’t match my reality. The popular 50/30/20 rule 50% needs, 30% wants, 20% savings mocked me from the page. With my limited income, my essential needs were consuming nearly 80% of what I brought home. It wasn’t for lack of trying. I was cutting corners everywhere possible.

If you’re struggling to stretch a small paycheck, you already know the frustration. Most budgeting advice assumes you have financial breathing room that after covering your bills, something is left over. When you’re working with limited income, that assumption falls apart fast.

Budgeting on a low income is fundamentally different from standard financial advice. It’s high-stakes one blown tire or an unexpected medical bill can completely derail an entire month and send your finances into a tailspin of financial stress. When you’re living close to or below the poverty line, conventional wisdom falls short because it wasn’t built for your reality.

Why the 50/30/20 Rule Fails When You’re Budgeting on Low Income

The 50/30/20 rule breaks down completely at lower income levels. When I was making just above minimum wage, my rent alone consumed nearly 50% of my take-home pay. Add utilities, basic transportation costs, and the cheapest grocery options I could find, and I was already above 70% spent on absolute necessities before a single want was considered.

Percentage-based budgeting assumes you have discretionary spending left after covering the basics. It assumes your housing costs, grocery budget, and transportation costs fit neatly into the recommended slices. When your limited income barely covers essentials, those assumptions create financial stress rather than financial stability.

How to Budget Money on Low Income for Beginners: Your First Steps

When I first tried to get a handle on my money, I didn’t download an app or build a spreadsheet. I just needed to know where my cash was actually going. That single realization that I had no real picture of my spending was the beginning of every change I eventually made.

I started by how to calculate your actual monthly income using my take-home pay not the gross amount. I started by calculating my actual monthly income using my take-home pay not the gross amount. Budgeting based on money you never actually see leads straight to frustration. For me, this meant adding up my real paychecks after taxes and deductions, which was often $200–$300 less than what I thought I was making.

Next, I committed to expense tracking for a full month every single purchase, no matter how small. Yes, it was tedious. But the patterns it revealed were things I never would have noticed otherwise. I used a simple notebook: one column for the date, one for what I bought, one for the amount. No app needed. No technology required.

Start With a Simple Expense Tracking System (No App Required)

You don’t need anything fancy to begin. I started with paper and pen: three columns date, expense description, and amount. That’s the whole system. For income tracking, I added a separate section at the top of each week’s page to log my pay dates and exact deposit amounts.

After just one week of consistent tracking, I started seeing patterns I never expected. I was spending almost $60 a month on convenience foods grabbed on nights I was too exhausted to cook. For groceries specifically, a grocery budget calculator can help you quickly see where your food spending is going. Small purchases I’d written off as nothing were eating into my grocery budget in ways I hadn’t noticed.

I carried the notebook everywhere and recorded purchases immediately, while they were fresh. Later, I moved everything into a simple budget template in a spreadsheet but the notebook phase was where the real awareness happened.

Which Budgeting Method Works Best for a Low Income Budget?

After trying several approaches, I found that zero-based budgeting works far better than percentage-based methods when income is tight. This approach gave every dollar a specific job before I spent it which mattered enormously when I had so few dollars to work with.

Zero-based budgeting means your monthly income minus every expense, savings contribution, and debt payment equals zero. It’s not about spending everything. It’s about building a spending plan so intentional that nothing gets wasted including the money you’re setting aside.

Here’s exactly how I built my zero-based budget each month:

- Write down my total monthly take-home pay as my starting number.

- List every essential expense rent, utilities, groceries, transportation costs with exact dollar amounts.

- Add all other budget categories: debt payments, savings, and any discretionary spending.

- Keep assigning dollars to categories until the total equals zero.

If I ran out of categories before I ran out of money, that leftover went straight to my emergency fund or smallest debt.

This method forced me to face reality about what I could truly afford, and it eliminated the guilt of not meeting arbitrary percentage targets.

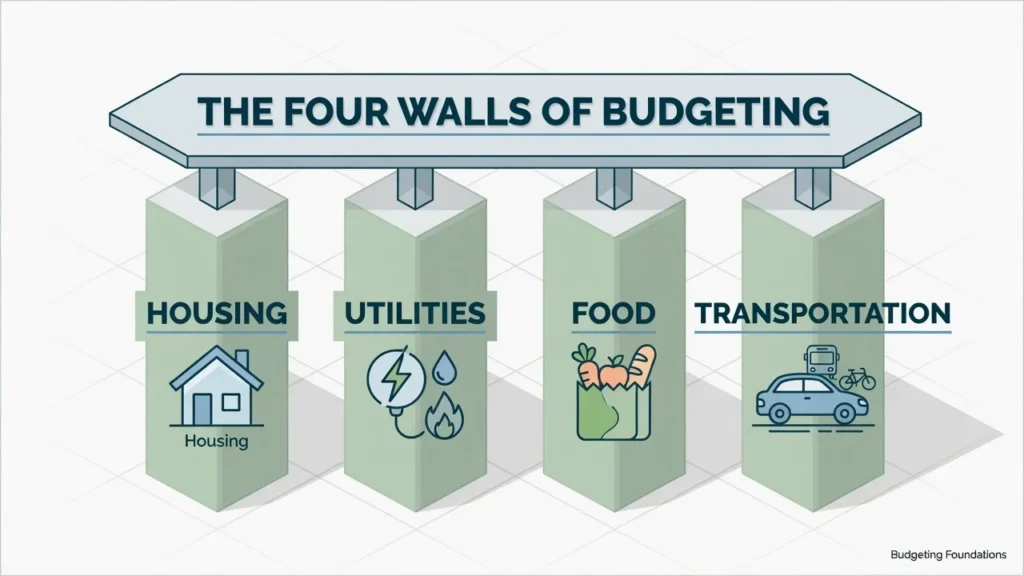

The ‘Four Walls First’ Approach to Covering Essential Expenses When Money Is Tight

When I hit my financial rock bottom, I had to decide which bills to pay first. The ‘Four Walls’ approach gave me a clear answer and it changed everything about how I managed bill payment under pressure.

The Four Walls are your most critical essential expenses, the ones you protect no matter what: housing costs (rent or mortgage), utilities (electricity, water, heat), food (groceries not restaurants), and transportation costs (car payment, gas, or public transit to get to work).

I learned to secure these four areas before spending a single dollar elsewhere. This meant sometimes having to make difficult calls about other bills, but it ensured I maintained the basic necessities for survival.

When my car broke down and I faced a $600 repair bill, I temporarily reduced my grocery budget and negotiated a payment plan on a medical bill. Everything else got paused. But by protecting my Four Walls first, I kept a roof over my head and kept my job which meant I still had income to recover with. That’s the whole point of the strategy.

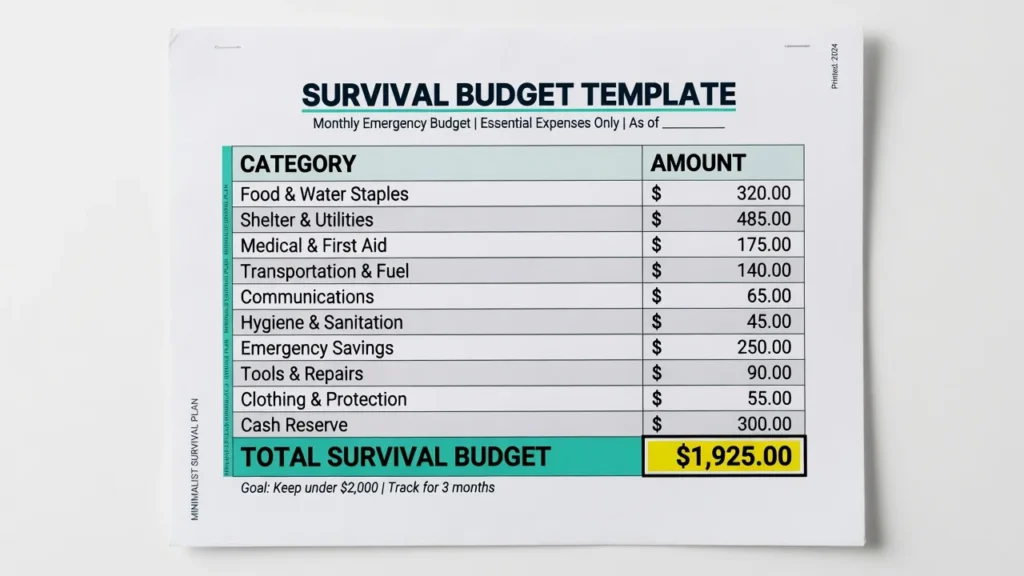

Creating Your Bare Minimum “Survival Budget”

The exercise that gave me the most clarity was calculating my absolute bare-minimum monthly expenses the rock-bottom number I needed just to keep the Four Walls intact. Here’s what mine looked like:

- Rent: $875

- Utilities (average): $180

- Groceries (basic necessities only): $200

- Transportation (gas to work + bus pass): $160

- Phone (cheapest plan): $40

- Minimum debt payments: $75

Total: $1,530/month

Knowing this number changed how I thought about money. It separated my fixed expenses (rent, phone, minimum payments) from my variable expenses (groceries, gas) and showed me exactly where I had flexibility when things got tight.

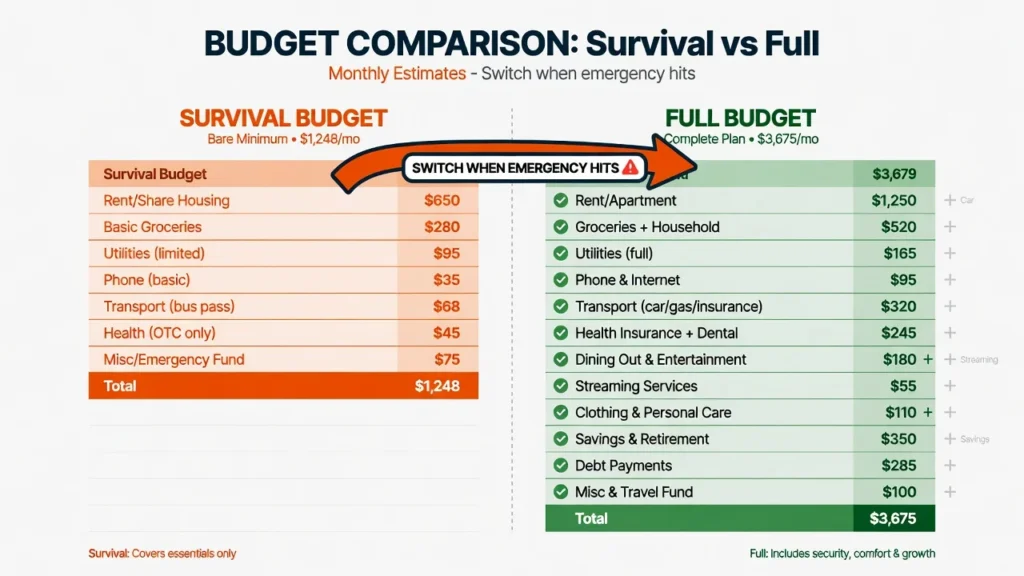

The Two-Budget System That Transformed My Household Budget

The approach that changed everything for me was running two budgets side by side: a Survival Budget and a Full Budget. The Survival Budget covered only my Four Walls and minimum debt payments around 80% of my income during tight months.

Nothing extra. No flexibility. Just survival. The Full Budget used the same foundation but added real-life budget categories on top: a small entertainment line, slightly better groceries, savings contributions, and the occasional takeout meal. Having both pre-built meant I was never scrambling when things went sideways.

What made this system work was the absence of decision-making in a crisis. When an emergency hit, I didn’t have to think I just switched budgets. That alone cut my financial stress in half. No scrambling. No guilt. Just a pre-made plan I’d already thought through when I was calm.

When to Switch Between Your Two Budgets

I developed clear triggers for switching from my Full Budget to my Survival Budget:

- Unexpected expense over $100 : anything that breaks my variable expenses plan for the month

- Reduction in work hours : even one less shift can shift the math significantly

- Seasonal income fluctuations : certain months are always slower; I planned for them

- Necessary car or home repairs : these hit hard because they’re urgent and non-negotiable

- Medical expenses : copays and prescriptions that fall outside my normal monthly expenses

If any of these hit, I switched budgets immediately no debate.

When my hours got cut during a slow stretch at work, I switched to my Survival Budget the same day. That meant pausing the streaming subscription, trimming my grocery budget by $50, and putting off a planned clothing purchase. I didn’t have to agonize over any of it the decisions were already made. My household budget stopped feeling like a fragile plan and started working like a system I could actually trust.

How to Save Money on a Low Income Budget: Emergency Fund Strategies That Actually Work

Building savings on a small income felt impossible for a long time. The standard advice like what savings goals and targets suggest for different ages and income levels felt laughably out of reach when I was barely making it to the next payday. So I stopped trying to follow that advice and built my own savings strategies around what I could actually do. I started with a first savings goal of just $200 to $300: enough to handle the small, random expenses that used to derail my whole month.

This wasn’t enough for major emergencies, but it could cover many of the small crises that previously sent me into a financial tailspin – like a car repair or urgent dental work.

Here’s exactly how I built that first cushion, one small move at a time:

- $5 per week to savings : just $20 a month, transferred manually after each paycheck

- Banking ‘fifth week’ paychecks : some months have five paydays; I treated that extra check as off-limits for regular spending

- Coin jar deposits : I emptied my change into a jar and deposited it monthly; it averaged $15–$25

- Redirecting windfalls : any rebate, refund, or cash gift went straight to savings before I had a chance to spend it

Having even that small cushion shifted something in my brain. The constant financial stress eased not completely, but enough that I stopped dreading every unexpected bill. One minor crisis no longer had the power to unravel the whole month.

The ‘Pay Yourself First’ Rule: A Savings Strategy for a Tight Budget

For years, I tried to save what was left over at month’s end. The answer was almost always nothing. So I reversed course: I made savings the first bill I paid before anything else. I set up a manual transfer of just $10 on payday to a separate savings account one where I could actually track how much interest your savings will earn, even if it’s just a few pennies at first.

That was it. Small enough not to hurt, but consistent enough to build a habit. As my income improved, I bumped it up in $5 increments and kept my financial goals in view. The habit matters far more than the amount especially at the start.

Creative Ways to Cut Expenses on a Low Income Without Feeling Deprived

The strategy that made the biggest difference was what I call ‘selective downgrading.’ Instead of cutting entire categories which is one of the most common mistakes in ways to reduce your monthly expenses I looked for one item per category where I could step down without feeling it. This approach to cutting expenses keeps frugal living practical rather than punishing.

Here’s what it looked like in practice:

- Downgraded my cell phone plan but kept my smartphone

- Mixed store-brand and name-brand groceries rather than switching entirely to store brand

- Found a cheaper car insurance provider while keeping identical coverage levels

- Cut cable but kept one streaming service

- Reduced restaurant meals to once a month but made that meal worth it

This selective approach let me maintain some small pleasures while still reducing my overall spending. The cumulative savings were significant without the feeling of constant deprivation.

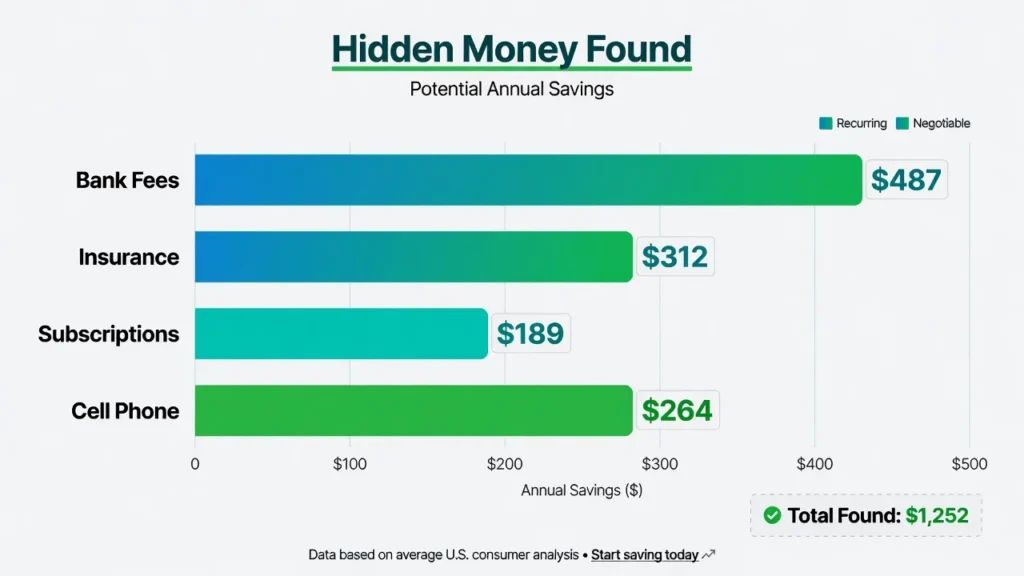

Finding Hidden Money in Your Current Budget Through Smarter Money Management

A single afternoon of financial planning reviewing every recurring expense line by line uncovered over $800 a year I didn’t know I was losing. Here’s where I found it:

- Bank fees: I was paying $12 monthly for a checking account. Switching to a free credit union account saved $144 per year.

- Insurance bundles: Combining my renter’s and auto insurance saved nearly $200 annually.

- Subscription creep: Three small subscriptions I’d forgotten about $7.99, $4.99, and $9.99 per month were quietly draining nearly $300 a year.

- Cell phone optimization: Dropping to a lower data tier saved $15 per month, or $180 per year.

None of these changes affected my daily life. The services stayed the same. The cost didn’t.

Income Optimization: How I Boosted My Personal Finance Without Finding a New Job

The approach that worked best was identifying my existing skills and offering them as occasional paid services nothing formal, no business registration, just neighbours helping neighbours for fair compensation. When your cost of living barely leaves room to breathe, even $50 from a Saturday of pet sitting makes a real difference. Here’s what I actually did:

- Basic computer troubleshooting for elderly neighbors ($20–$30 per visit)

- Pet sitting during holiday weekends ($25–$40 per day)

- Social media management for a local small business ($50–$75 per month)

- Seasonal retail work during peak periods ($12–$15/hour)

How to Find Money When You Need It Tomorrow

When I needed money fast within 24 to 48 hours without touching credit card debt or payday loans, I had a mental list of options I’d already thought through:

- Local marketplace apps (Facebook Marketplace, OfferUp) : I’d clear out unused items and typically make $30–$80 within a day

- Same-day gig work (TaskRabbit, or just texting people I knew) : lifting, cleaning, assembling furniture

- Weekend childcare : families in my neighborhood often needed short-notice sitting for $10–$15/hour

- Plasma donation : paid $50–$70 per session in my area; I used this only occasionally

- Cash day labor : yard work, moving assistance, basic handyman tasks through neighborhood apps

Having this mental list ready meant I never felt completely helpless when faced with an unexpected expense. It also helped me avoid the debt cycle that had trapped me previously.

Debt Management on a Low Income: The ‘Minimum Plus’ Strategy

Managing debt on a low income requires different financial planning than what the standard debt snowball or avalanche methods assume. Those strategies are built for people with surplus cash to throw at debt which wasn’t my situation. My ‘Minimum Plus’ strategy works differently:

- Make all minimum payments first : this is non-negotiable and protects your credit.

- Add $5–$10 to each minimum payment when possible : even this small amount reduces total interest significantly.

- Direct any windfall money to your smallest debt : not the highest interest, but the smallest balance, for a fast psychological win.

It’s slower than the debt avalanche. But it’s a strategy you can actually maintain on a tight budget and sustainable beats optimal every time.

This method doesn’t eliminate debt as quickly as concentrated approaches, but it was sustainable on my limited income. Even adding $5 to a minimum payment significantly reduces the overall interest paid and shortens the repayment period.

To put numbers on it: on a $1,000 credit card debt at 18% interest, adding just $10 to your minimum monthly payment can cut repayment time from several years down to roughly 18–24 months and save $150 or more in interest charges. If you’re unsure whether your total credit card debt falls into a manageable range, how much credit card debt is manageable provides guidance on that assessment.

Negotiating With Creditors to Reduce Your Bill Payment Burden: What Actually Worked

When I genuinely couldn’t make a payment, I picked up the phone before missing it. That one habit calling ahead opened more doors than I expected. Many creditors have hardship programs they never advertise, but will offer them the moment you ask. Here’s the exact script I used:

‘I’m experiencing financial hardship due to [brief explanation]. I want to honor my commitment, but I need temporary assistance. What programs do you offer for customers in my situation?’

Calling before missing payments and being specific about asking for hardship options got me:

- Interest rate reductions on two credit cards

- A three-month payment deferral on a personal loan

- A zero-interest payment plan for medical bills

- Waived late fees on multiple accounts

The key was always calling before missing a payment, not after.

The key was calling before missing payments, being honest about my situation, and specifically asking what hardship options were available.

Building Sustainable Money Management Habits on a Limited Income

Three habits built my financial literacy more than any app, book, or budgeting template ever did. They’re simple enough to maintain even during my busiest weeks and that’s exactly why they worked.

Weekly money check-ins: Every Sunday evening, I spent 15 minutes reviewing my spending, updating my tracker, and planning the week ahead. This consistent awareness stopped financial surprises before they started.

The 24-hour rule: For any non-essential purchase over $20, I waited 24 hours before buying. That cooling-off period eliminated about 80% of my impulse spending not because I was disciplined, but because I usually forgot I wanted the thing by the next day.

Monthly budget adjustments: I stopped chasing the ‘perfect’ budget and accepted that mine needed tweaking every single month. The first of each month, I looked at what worked, what didn’t, and adjusted for the next 30 days.

How Changing the Way I Thought About Budgeting Made It Finally Stick

Budgeting clicked for me when I stopped treating it as a list of things I couldn’t do. I started calling it a spending plan instead of a budget same math, completely different feeling. A spending plan is something I build. A budget is something imposed on me. That one reframe turned a monthly chore I dreaded into something I actually did.

A budget doesn’t need to be perfect. It just needs to keep you aware. When I overspent and I did, regularly I knew exactly where and by how much. That awareness is the foundation of real money management. Without it, you’re just guessing and hoping. With it, you can adjust.

Budgeting on a low income isn’t about following someone else’s financial rules. It’s about building a system around your actual life your income, your bills, your emergencies. The strategies in this guide aren’t theoretical.

I used every single one of them when my income was at its lowest. Financial stability is possible even when your numbers seem too small to matter. Start with just one thing: calculate your Four Walls number today. That single step changes how you see your money.

How to Save Money on a Low Income Budget: Micro-Strategies That Add Up

The hardest part of saving money on a tight budget isn’t the math. It’s the feeling that the amounts are too small to matter. I spent years thinking that. Then I discovered that small and consistent beats large and occasional every single time especially when your income is limited.

The ‘Round-Down Transfer’ Method: How I Save Without Feeling the Pinch

Here’s how the round-down transfer works: every day, I check my account balance and transfer anything above the nearest $5 or $10 mark to savings. If I have $127.83, I move $2.83. If I have $243.76, I transfer $3.76.

These are amounts I genuinely wouldn’t notice dropping on the sidewalk. But last month, those tiny daily transfers added up to $46.21 without me ever making a deliberate ‘savings decision.’ My brain treats the rounded number as my real balance. The cents quietly pile up.

Why a $200 ‘Weird Little Expenses’ Fund Matters More Than a Full Emergency Fund

I reached $200 in about eight weeks. I remember the first time a surprise expense hit after that a $47 prescription I wasn’t expecting.

Old me would have panicked. Instead, I just moved money from the fund and kept going. That’s it. No crisis. That was the first time budgeting on a low income actually felt like it was working not in theory, but in real life.

7 Ways to Cut Expenses on a Low Income Budget Without Feeling Deprived

Cutting expenses doesn’t have to mean living a joyless existence. Through careful analysis of where my money was actually going, I identified several opportunities to reduce spending while maintaining (and sometimes improving) my lifestyle.

I focused first on optimizing my three biggest expense categories – housing, transportation, and food – before tackling discretionary spending. This approach gave me the biggest return on my effort.

The ‘Hours of Life’ Rule: My Most Powerful Tool for Cutting Discretionary Spending

The concept that most changed my spending was converting every price tag into hours of my life. After calculating my real hourly take-home pay after taxes and commuting costs the math got sobering fast.

That $14 fast food meal cost me nearly two hours. The $60 new release video game? Almost a full day of labor. This is the kind of financial literacy no one teaches you in school, but it’s the most practical tool I found for cutting discretionary spending intentionally.

Finding Hidden Money in Your Fixed Expenses

I applied the same approach to my cell phone plan, internet service, and even negotiated a lower rent by offering to sign a longer lease.

These efforts required just a few hours of focused work but continue to save me money every single month. Unlike cutting daily pleasures, these savings are completely painless – I receive identical services for significantly less money.

Budgeting Tips for Low Income Families With Children

Raising children on a limited income means the budget has to stretch further and the stakes feel higher. Unexpected school expenses, kids’ clothing, medical copays these costs don’t pause just because money is tight.

What I found, though, is that bringing my kids into age-appropriate money conversations actually reduced the household financial stress. They weren’t confused about why we said no to things. They understood. And that changed the dynamic.

Managing School Expenses on a Tight Budget Without Getting Blindsided

School-related costs used to blindside me every few months until I added a dedicated education line to my budget categories. Now I set aside $5 each week for school expenses about $20 per month which covers most small needs without disrupting the rest of my household budget.

For larger costs like field trips, I contact teachers early. Most schools have support resources for families who ask proactively. And my local Buy Nothing group has been a goldmine for free school supplies, sports gear, and kids’ clothing things that would otherwise spike our cost of living unexpectedly.

What to Do When Unexpected Expenses Break Your Household Budget

Financial emergencies happen car repairs, medical bills, household breakdowns. I’ve faced all of them on a tight income. What shifted things for me wasn’t preventing these emergencies (you can’t), but changing how I responded.

A broken budget is not a moral failure. It’s a signal that you need a recovery plan and building that plan is the real work of financial planning on a limited income.

The 48-Hour Emergency Response Plan for Budget Crises

Here’s exactly what I do within the first 48 hours of an unexpected expense:

- Assess urgency. Is this a true emergency requiring immediate payment, or can it wait until the next paycheck? Many ‘urgent’ expenses can actually hold for a few days.

- Check the mini emergency fund. If I have one, this is exactly what it’s for. I use it before touching a credit card.

- Switch to survival mode immediately. I activate my Survival Budget and halt all non-essential spending for the rest of the month no debate.

- Identify what to cut. I look at my spending plan for the remaining days of the month and find categories I can reduce to compensate.

- Rebuild first. Once the month resets, restoring my emergency fund becomes the top priority before anything else gets funded.

The critical step is deciding quickly every day of normal spending after an emergency compounds the problem.

How to Budget and Save Money on Low Income for Long-Term Success

Sustainable progress on a limited income is a two-sided game: defense (budgeting, cutting costs, saving what you can) and offense (finding ways to grow your income over time). The strategies in this guide focus on defense getting the most from what you have.

But financial stability comes faster when you can also nudge income upward, even slightly. And the thing that makes all of it work? Consistency not perfection, not grand gestures, just showing up to your budget week after week.

When Budgeting Isn’t Enough: Ethical Ways to Increase Your Income and Improve Your Personal Finance

Here’s the honest truth about budgeting on a very low income: at some point, the math stops working. You can cut every possible expense and still come up short because there’s a floor to how low your cost of living can go.

When I hit that floor, I stopped trying to squeeze the expense side and started looking for the shortest path to additional income. Not a second career. Not a business. Just: what skill do I have that someone nearby would pay me $20 for today? That question led me back to the same small services I’d offered before computer help, pet sitting, handmade items but now I pursued them with more intention, and they built on each other.

Managing expenses carefully while slowly growing income is what finally broke the paycheck-to-paycheck cycle for me. I reached a point where the math actually worked not because I earned a lot more, but because I knew exactly where every dollar was going. That’s the real financial goal: not wealth, just control.

Frequently Asked Questions

Is it even possible to save money on a very low income?

Yes. Start with $3-$10/week. First goal: $200-300 for small emergencies, not 3-6 months expenses.

What if I can’t even cover my basic bills on my current income?

Prioritize Four Walls: housing, utilities, food, transportation

Cut costs: budget billing, basic groceries, public transit

Use assistance: food banks, SNAP, rental assistance programs

Increase income: gig work or sell items

Should I use cash envelopes or digital apps for budgeting on low income?

Both. Cash for problem categories (groceries, eating out). Digital/auto-pay for fixed bills. Track everything in a free app.

How do I handle variable or irregular income when budgeting?

Budget based on your worst month in past 6-12 months

Make two budgets: survival (low months) and full (good months)

Extra money priority: $500 emergency fund → high-interest debt → irregular expenses

Keep baseline expenses flat

What’s the best budgeting method when income barely covers expenses?

Zero-based budgeting. Assign every dollar a job until income = $0. Forget percentage rules like 50/30/20.

How do I recover when unexpected expenses break my budget?

Switch to survival budget immediately

Use emergency fund or redistribute remaining money

Track what breaks your budget monthly

Add line items for recurring “unexpected” expenses

Is it worth automating savings on a very low or variable income?

No if income is tight/variable risk overdraft fees. Save manually after bills are paid. Automate only when income stabilizes (start at $5/paycheck). Always automate bill payments to avoid late fees.