The 7 Key Components of Successful Budgeting (That Actually Work)

I will never forget the one statistic I heard over 78% of Americans living on the edge of paycheck to paycheck. It surprised me and it was logical. I had been there before, with my bank balance emptied out month after month, and saying to myself, “Where did all the money go? It’s when I realized that I needed to know the essentials of budgeting rather than just one-off pieces of financial advice that I never used.

An income is just a plan for your cash. It lets you know what you are spending your money on before you even spend it rather than at the end of the month wondering why you don’t have any.

Here are seven steps to successful, real-life budgeting that do work! These are not “pie in the sky” suggestions such as “spend less” or “save more. These are the specific elements of your personal budget that will form your plan that you can commit to.

I will also explain to you which of the budgeting methods will work best in your life, what is the biggest cause of most budgets failing and how to manage irregular income without the need to constantly worry. Budgeting is a first step in money management and financial literacy. It’s the quickest route to financial security, and beginning now, in any place, it changes everything.

This is a quick overview of the 7 Key Components of Successful Budgeting

Before I go into each of the seven parts of the personal budget you need to create a workable budget, let’s take a quick look at all seven. Here’s a few tips to keep in mind as part of your budget planning:

Income Calculation : Make sure that you know your pay in hand, not your gross salary and account for all sources of income.

Expense Categories : Categorize spending into fixed, variable, and the costs in most budgets that are left behind.

Financial Goals for Budgeting : Establish clear goals and priorities about saving up dollars.

Emergency Fund : Create an emergency fund to help you avoid debt in case of an emergency expense.

Spending Plan or Method : Select a spending system that fits your spending way of thinking.

Track your income and expenses : know where your money goes and make decisions, not educated guesses.

Budget Review Process : Review your budget each month to make adjustments to your budget as life and priorities change.

All of these elements are interdependent. If you miss one, your budget is in trouble. With all seven, you have a solid foundation that will move you towards true financial stability. Each component will be explained in the following sections, how it is set up, and where people tend to get it wrong.

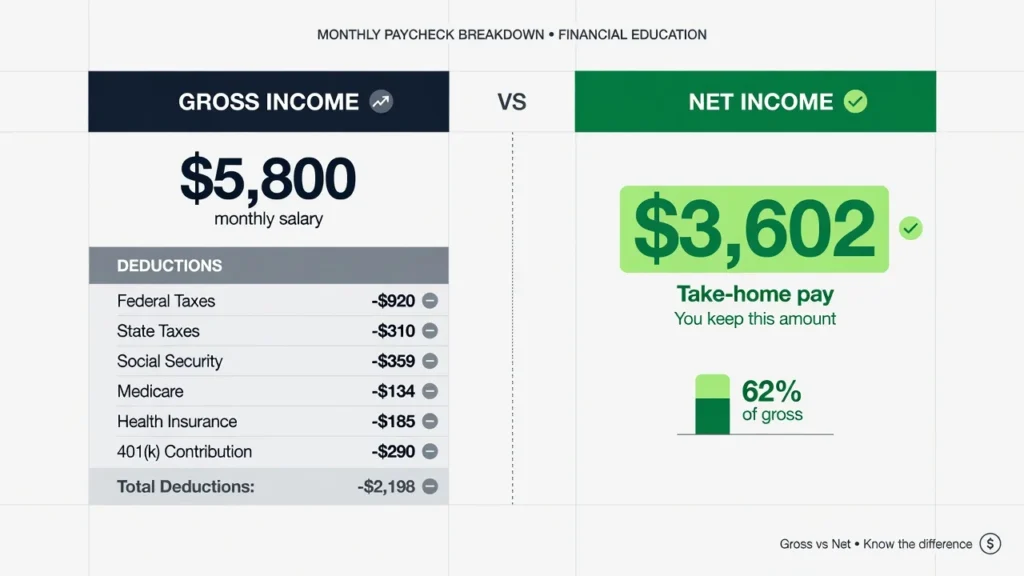

You are probably calculating your income wrong – and losing take-home pay

For the most part, the most major error that people make when they budget for the first time is that they take their gross income and not their net income.

Gross income is the amount of money you make before taxes, insurance, and retirement contributions if you want to see exactly how gross income is calculated from your pay, that breakdown is worth reviewing before you set your first budget number.

Your “take home pay” is your net income.

Anyone who plans by using gross income is planning to fail at the outset. You are attempting to use money that doesn’t belong to you.

This one I learned the hard way! When I used to see my pay and I thought I had room and I didn’t. Then I’d wonder why my budget never balanced. It was because I was using a number that wasn’t real.

If you’re creating your budget, begin by using your net income. The number that counts for cash flow management is that. Check your paycheck deposit or bank statement, not your offer letter.

Income includes more than just salaries. It encompasses any additional income (side income), any freelance income, any income from renting, any income from government benefits, payments received for alimony, payments received for child support, and all other income that is placed in your account. Without any of these sources, you’ll be off to a bad start when it comes to tracking your income and expenses.

What is considered income? (Don’t Leave Any Out)

If you are trying to determine total income, here are some things to take into consideration:

Earnings from primary occupation (salary or wages) after all deductions.

Other sources of income, such as freelance, gig or part-time work.

Income from rented, unoccupied property or rented room.

Payments made to you, as an unincorporated freelance, minus estimated tax if not withheld. If they will be frequent enough to count on, bonuses if they are, but I would still try to save for these separately.

Government benefits such as Social Security, disability, unemployment or child tax credits.

If you get child support or alimony payments on a regular basis.

If your income is not steady or any income is irregular, then use the lowest income you’ve received in a recent month, but do not use the average. This is so important to emphasize. Some people like to plan for what they think will be their best months and then you get the bad months and that doesn’t work out so well.

In the past, I made my budget based on a 19% average. Then I had 2 terrible months in a row and everything went on a complete spin. So, rather than turning to my ceiling, I’m turning to my floor. When I have more money, it goes towards my savings or towards my emergency fund. If I make less money, I’m still protected!

The basis is the calculation of net income. After getting this number, all is settled.

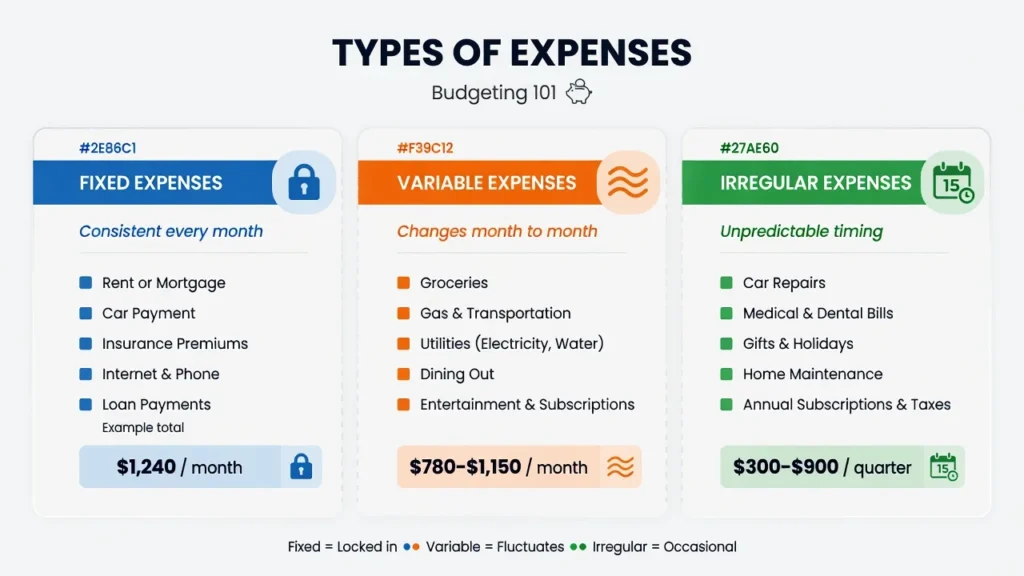

Fixed Expenses, Variable Expenses, and the Costs Most Budgets Forgotten

With a solid grasp of what income you have, you need to determine where the money is going. Most budgets separate the expenses into two categories, but I will show you three, because the third category are the expenses that cause the “emergency” expenses to blow up the budgets every month.

It’s important to know what is a fixed and variable cost. Fixed expenses are the same amount every month. Rent/Mortgage, Car, Insurance, Loan payments, subscription services. These remain steady and can be predicted.

Variable expenses are expenses that vary from month to month but still occur each month. Food, gas, bill, entertainment, and eating out. You can see them approaching but you can’t see how many they will bring. These are two critical budget items.

This is a fact that most people don’t know: variable does not equal optional. Foods vary but are necessities not luxuries. Gas is a variable, but if you drive to work it’s a must. Beware of the difference between “variable” and “discretionary spending.

There’s also the third type that no budget ever considers.

There are two types of expenses: fixed and variable. And that’s what they really mean

I have seen individuals getting these two mixed up a lot so I will explain the difference.

Fixed expenses:

Rent/Mortgage, Car Payment, Student Loan Payment, Insurance (Car, Health, Renters), Internet, Gym, Streaming Subscriptions, Childcare Costs.

These stay the same. You know how much you have to pay.

Variable expenses:

Food, gas/transportation, electricity, water, eating out, entertainment, clothing, personal items, household items.

These expenses vary from month to month, but are consistent each month. They can be guessed by looking at previous spending.

The needs vs wants framework comes in handy here.

Food is an essential requirement, and learning how to budget for groceries specifically can make a significant difference in how well you control this category month to month.

Eating out could be a necessity, or it could be because of a hectic lifestyle. Be honest and put things in categories, but not what you think you should put.

I would say that if something was fun I used to think that I wanted it, and then feel badly about it afterwards. But entertainment isn’t bad. It’s a part of a healthy life. The purpose is a raise the awareness, not shame.

Track both fixed and variable expenses in your spending categories. Add them up. This number is your starting point for the cost of living. Once you have it, you can start looking at practical ways to [reduce your monthly expenses] across each category.

The third category of expenses that most budgets overlook is “Irregular Expenses”

This is the one that was my problem with the budget before.

Irregular expenses include any costs that do not occur on a regular monthly basis, but are always there if you plan ahead. Car repairs. Annual car registration. Medical copays. Repair/replace appliances. Holiday gifts. Back to school costs. Subscription items such as Amazon Prime or Costco membership.

These aren’t emergencies. They are simply costs that occur at irregular intervals. However, if they are not planned for, they come across as emergencies, and that’s when people turn to their credit cards.

I have learned this from a professional budgeting person. He stated that one-time or capital costs are not included, thus avoiding unforeseen budget deficits. This is simple business budgeting and it’s directly applicable to personal finance.

What I do now. Estimate the cost of these “unexpected” expenses per year. Let’s assume that the average cost for maintaining your car is about $600 annually, and there are some annual expenses for gifts ($500), and some other random costs ($400). That’s $1,500 total.

I divide that by 12.I take that apart by 12. That’s $125 a month. This $125 I add to my monthly savings plan and deposit it into a savings account I’ve designated as my sinking fund. I use it for those odd bills when they occur. It’s already there. No stress. No debt on credit card.

I know one person who did the math on it and determined that he would pay more than $1,008 per year to purchase Starbucks coffee 3 times weekly, plus tip. When she saw the annual figure, she knew that there was a budget item to plan for or to cut namely, a little item that wasn’t regular or was irregular.

Include unusual costs under the budget headings. Treat them as the true recurring costs that they are, but over a longer time frame. I can’t say how many times I have saved my budget on planning for these!

Create Financial Objectives First, Write Any Number Second

The concept of budgeting was once in my mind only about monitoring spending. Then I realized, that if you don’t have any financial goals to budget towards then you are just filling out a spreadsheet without any direction.

Goals are what give your budget meaning. They are the reason you deny yourself one thing so you can have something greater at a later time. Budgets are like limitations without goals. Goals make it feel like “progress.

Setting SMART goals is the basis of any plan. That is, goals that are specific, measurable, attainable, relevant, and time-bound. Having a vague goal such as “save more money” fails because you’re not sure when you have or haven’t.

Having financial objectives when budgeting assists you to prioritize your expenditures and determine where your monthly savings allocation should really go. Transforms a budget into a roadmap.

I have two types of goals – short term and long term – that I support simultaneously. If you are not sure where to start with a long-term target, checking savings benchmarks by age can give you a useful reference point before you set your numbers.

Short-Term Goals vs Long-Term Goals (And How to Fund Both)

Short-term goals include objectives or actions that you wish to accomplish in the next 3-12 months.

Establish an emergency fund that has at least $1,000.Create a starter emergency fund of at least $1,000. Reach a credit card’s repayment plan. Set aside for a vacation or car repair money. Get rid of an old appliance. Save for a month’s worth of living expenses.

By having these goals, you’ll be motivated to save because you’ll see results quickly.

Long-Term Goals: Goals that require one year or more.

Save up for home down payment. Save for your retirement by making regular contributions. Start a college savings account for your children.

Settle your debts as soon as possible: car loans, and if student loans are part of your picture, there are specific strategies to pay off student loans faster that are worth building into your long-term goal timeline.

Become fully financially secure with 6 months of living expenses in savings.

I value each of my goals by assigning a dollar amount and going backwards. To save $3000 to take a vacation in 12 months, I must save $250 each month. For me, that $250 is a line item like paying rent.

I may only be able to save $50 to long-term goals some months, but that’s fine. Consistency not perfection is the point. Any amount you save each month is significant.

But when I put my budget in real terms for the goals I wanted to accomplish, everything fell into place. I wasn’t just cutting back on spending. I was funding a future that I really wanted. A budget is no longer a tedious task, but a powerful instrument to create the life you want by having your financial goals.

Most people seem to ignore the Emergency Fund in the budget

The Emergency Fund is the Budget Component most people flinch at. The difference between people who get out of debt, and those who remain in the cycle is the emergency fund.

An emergency fund is a fund of money that has been saved for unexpected expenses. Car repairs. Medical bills. Sudden job loss. Broken appliances. Not for vacations or for holiday gifts. It’s a failsafe that helps you to avoid using a credit card when life hits you with a curveball.

I would always think that I do not have enough money to save for an emergency fund. I was already living paycheck to paycheck and all the cash had been used. Here are some things I learned, however. Without an emergency savings account, you incur debt when it is needed the most. Debt also costs you a lot, in the long run.

A rainy day fund will give you comfort. Also, it helps to safeguard your credit score. If something comes up and you don’t have the cash, then you either skip a payment or overdraw your credit card. They are both bad for your credit. An emergency fund prevents the cycle from beginning.

How you use your available credit – your credit utilization ratio – accounts for 30% of your credit score. If you don’t have an emergency fund, and max out one credit card to pay for an unforeseen expense that ratio skyrockets and your credit score plummets.

I know one person that has two buffers. One that would pay her half of six months’ bills if she lost her employment. A smaller savings account that’s dedicated to emergencies such as car issues or appliance repairs — ideally kept in a high-yield savings account so your emergency fund is also earning interest while it sits.

She states those buffers are her protection and financial security, particularly following a layoff. An emergency fund of at least $1,000 can make a significant difference, as a 2023 Bankrate survey found that only 44% of Americans could afford to cover a $1,000 emergency using that amount from their savings.

This is where you should get started if you don’t have an emergency fund now. The vacation fund is established before the vacation. Before paying off debts that have a low interest rate. Construct the buffer first.

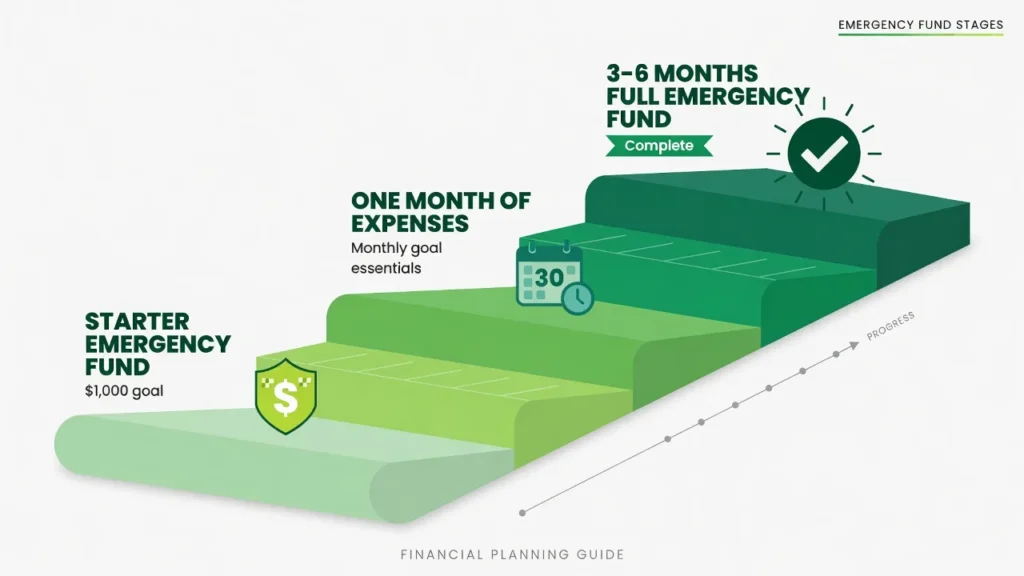

How much funding does an emergency need in a budget? (A 3-Stage Approach)

I suggest three steps when putting money aside for emergencies! For most of us it is impractical to save all six months’ worth of savings upfront. This is possible with smaller steps.

Stage 1: $1,000 starter fund.

This is your first objective: to keep the smallest of the issues out of debt. A car repair, broken phone, emergency dental appointment. You will NOT lose your money.

You don’t need to save $100 per month, $25 or $50 will be good. It will take some time, but you will eventually get there. The thing is to start!

To be honest, it’s difficult to survive and build your first $1,000 when you’re already stretched thin. It took me almost 8 months the first time. Once I had it though, I put my credit card away for everything but the big purchases, which saved me a lot more than $1,000 in interest.

Stage 2: The cost of the whole month.

After you reach $1,000, continue until you have saved enough to buy a month’s worth of expenses. Rent, utilities, food, insurance, you name it.

This level provides most short-term disruptions to or loss of income. It provides you with some space.

Stage 3: Costs of 3 to 6 months.

This is complete insurance coverage. When a job loss or major emergencies occur, you need not fret about covering your bills for three to six months.

This stage is a time-consuming process. For some, it takes a number of years. That’s okay. The purpose is to make progress, not to get it done quickly.

I know the argument. I’m not in a position to save at this time. I used to say so too. The reality, however, is that: When you’re not saving $25 per month, you’re certainly not saving $500 per month for an emergency. And it is coming.

Do what you can, $10/month is better than zero. Do it automatically before you see the money. Consider your emergency fund a payment to yourself. If you are working with a very tight budget, there are practical methods to save money on a low income that make even small contributions possible.

To be honest, this item has kept me out of debt more than any other item in my budget.

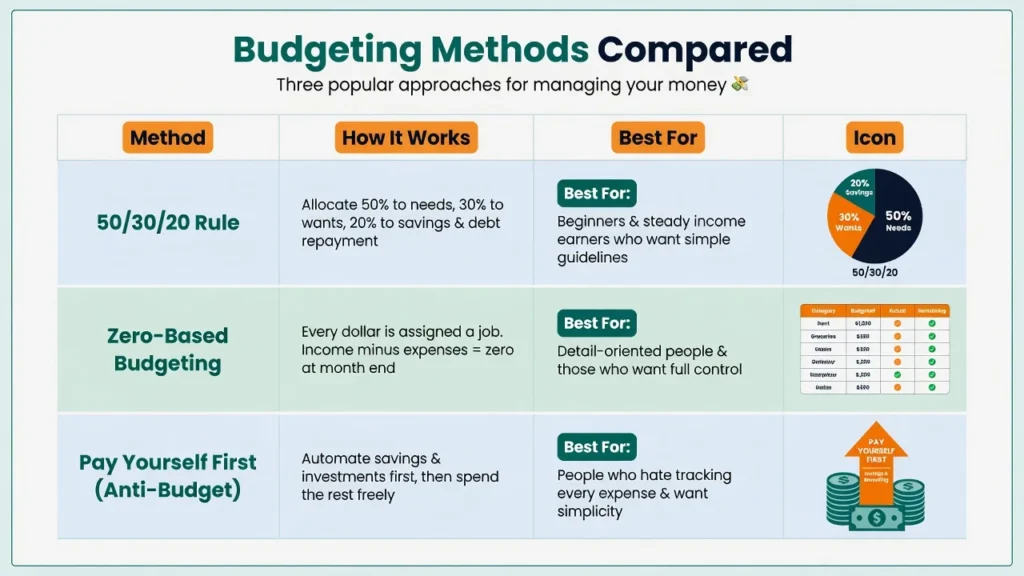

Which Budgeting Method is Right for You? (3 Options Side by Side)

This is one tip most budget planning articles won’t share with you. The idea that there is one correct way of budgeting is a myth. There are various strategies, and the most successful one is the one you’ll actually stick with.

Let me introduce you to three budgeting methods that work for different people so you can select the approach that aligns with your financial situation and your mindset. Do not push yourself into something that you do not feel comfortable in or that doesn’t match your circumstances. This is the way budgets go wrong.

The 50/30/20 Rule: Good for those who are beginning and want some structure

This is the easiest and most popular budgeting technique that you’ll find.

Your income is split into three categories. 50% goes to needs. 30% goes to wants. 20% is put aside for savings and paying off debt.

Needs are the necessities. Rent/mortgage, utilities, groceries, insurance payments, minimum (required) loan payments, transportation.

Wants are all other needs. Eating out, amusement, memberships, hobbies, traveling.

Your emergency fund, retirement plan contribution and other savings should be part of that 20 percent allocated to savings and debt repayment in your budget.

Best used if you have regular and predictable income and desire simplicity with minimal decision making.

The problem is that the payments required for costs of living can end up exceeding 50% of your earnings in high cost of living communities. In a city such as New York or San Francisco, the average renter puts 40-50% of his income into rent and the 50/30/20 rule is extremely difficult to apply without making some modifications. The percent structure is consistent, but may be moved around.

The 50/30/20 rule is the simplest budgeting system that I could follow when I first started budgeting. I was not making 100 decisions, 3 big buckets.

This is a good way to go for the beginner in budgeting. It provides clarity and makes it easy for you to discern between needs and wants without excessive thought. For a complete breakdown of how to apply it to your income, see the 50/30/20 budget rule in full detail.

Best for Detail-oriented People: Zero-Based Budgeting

Zero Based Budgeting is a financial budgeting method where every dollar of your income is designated to a different category until your income minus all your expenses and savings equals zero.

You’re not leaving money unassigned. Each dollar is doing a work.

This approach is borrowed from business budgeting, where each department is responsible for explaining the origin of each dollar that it is spending for the coming year. In personal finance, it makes you think about expenses that you automatically make that you may not think about anymore.

This approach takes more initial effort. All the money is supposed to be spent on something before the beginning of the month. It gives you maximum control and awareness, though! You can be certain of what you are doing with your funds.

The bright side is that in 2026 there are apps available which can do a lot of this rebalancing for you! The app can automatically debit from another category if you overdraw in one category so you don’t go negative. Helps to remove some of the manual load.

This system was the one I implemented for a whole year, and it transformed my perception of my spending categories. I realized that I was spending a lot more than I expected on subscriptions, and almost nothing on things that I said I cared about.

For those who like details and control, zero based budgeting will be satisfying. If you’re not into tracking and micromanaging, it’ll be a chore!

The Anti-Budget (Pay Yourself First): Best for People Who Hate Tracking

It is a new way of budgeting.

You transfer a specific percentage of your paycheck to savings, investments or debt payoff on payday. Any remaining is spent as you please. No tracking. No guilt. No spreadsheet.

The concept is if you’ve got a list of your financial objectives in the front of your mind, then the remainder of your cash is at your disposal without the guilt. You’ve already taken care of the important stuff.

It is a great way to go if you don’t like thinking in detail about your budget or going through it seems too arduous. If your income fluctuates, it’s also wonderful as it’s a percentage, not a set amount, that you are saving.

The problem with that is it isn’t going to make you more aware of your spending habits. You’re not going to be able to track where all your money is going, so you’ll have less ability to optimize or cut costs.

I know one person who practices this and says that his “walk around money” is the money that is left after doing this. He is aware he has money to cover his expenses, so he does not worry about anything else.

If you have previously done budgeting plans and have resented them, after that paying yourself first could be the one that sticks. Just be sure the percentage you’re saving is sufficient to help you achieve your goals!

There is a fourth option that I’m going to briefly mention. The envelope budgeting technique, which involves having physical or electronic envelopes for each expense category and filling them with cash. If no bills are placed in the envelope, then you do not make any payments in that category. Old fashioned but some folks believe in it.

Choose the technique that seems to be the least painful. Switching can be done at a later time.

Budgeting With Irregular Income: Calendar Sync Method That Works!

Most budgeting tips are worthless if you have a variable income. The 50/30/20 rule assumes you know what 50% is. The zero-based budgeting is based on the premise of having a fixed number to work with. What about if your salary changes each month? This is why it is crucial to have budgeting tips for people who have irregular income.

I get it. I’ve freelanced. I’m on a commission-based income. Have been employed in several part-time positions with changing hours.

It can seem like it’s impossible to budget when you have irregular income, but it isn’t. If you are also dealing with a lower overall income alongside the variability, there are specific strategies for budgeting on an irregular or low income that pair well with what I am about to show you.

There is a way that gets it done, and that’s the Calendar Sync System.

Here’s how it works. You connect your bank account to an online calendar. Your bills turn into calendar tasks that have due dates. You’re also also looking at expected paychecks, and that’s based on when you think you will receive paychecks.

This will provide you with a picture of how your cash is moving. You can view the cash flow and see where the money is going and coming from. Most importantly, you can visually note the lack between income and bills, the gaps.

When you’re able to see those dry spells, then you can plan around them. Consider postponing a non-emergency purchase for one week. Consider transferring funds from a prior paycheck to a holding account to fill in the gap. You are not taken aback anymore.

I began using this practice in the days when I had two clients working freelance with completely different payment requirements. It took me straight out of the panic station, one calendar for everything.

For a novice budgeter who has an irregular income, this is extremely practical since it is a system that is based on your reality rather than your reality being based on the system.

This is where the Anti-Budget method that I mentioned earlier is also applicable. If you have a fluctuating income, transferring a percentage straight to savings and goals the moment you receive your paycheck, even if it’s with a smaller percentage in the leaner months, will keep you consistent without the fatigue of the decision-making.

Create a budget for income that fluctuates from month to month

Let me show you how to do it.

Calculate your baseline income – Step 1.

Review your past six months’ earnings.

Use your worst, not average month. That’s your floor. Make your budget based on that number.

If your lowest month was $2,200 and your highest was $4,500, budget for $2,200. If it is more than that, it’s your extra money, not your regular income.

It is easy to prepare a budget based on the average. Don’t. If you’re budgeting more than you’re earning for the months when income is lower, then your budget plan will be ruined.

Step 2: Employ Calendar Sync approach.

Create an electronic calendar. Enter all the bills by the due date. Include any dates when you should expect paychecks, even if they aren’t the same amount.

Now take a look at the calendar. What are the constrictions? When does a bill “due” 3 days before your next paycheck? That’s a dry spell. It’s a matter of planning.

Perhaps you saved $100 out of your previous pay to make up that difference. Perhaps you call the business and move your due date one week.Perhaps you call the business and change your due date to one week later. The thing is, you’re no longer taken aback.

Step 3: If you have an extra bit of money to save in a high-income month, put it straight into saving.

It is easy to want to spend the extra when you’re having a great month. I’ve done it. But that’s how you remain fixed in place.

Rather, divert all the income above your needs and donate it to your emergency savings account or to your savings goals. If possible, make it automatic so that it can be done before you even think about it.

This is the actual showing of cash flow management. You’re filling in the bumps to cover the dips, you are smoothing the peaks to cover the dips.

Adjustment of your budget is normal if your income is irregular. Failure is not a necessary part of the system it’s how the system is designed to operate. The Calendar Sync method brings that adaptation into view and under control, rather than stressful and chaotic.

How to Track Spending Without Driving Yourself Crazy

Creating a budget is one thing and sticking to a budget is an entirely different story. The prettiest spending plan in the world can be put together, but if you don’t monitor what is happening, you don’t know if it is working. At the beginning I thought that was the only way to track, was by actually writing down every individual purchase in a notebook. It was very tiring and I stopped after 3 days. Then I thought, there was easier. Here are three ways that work and do not cause you to think of giving up. App-based tracking. Link your bank account and credit cards to a budgeting application. It automatically categorizes your spending. It’s only once a week that you go over it. This is the simplest and quickest way. Spreadsheet tracking. If you don’t trust apps, or you prefer a greater degree of control, download the transactions weekly and place them into a simple spreadsheet. Semi-manual, but you’re still in control of your data. Sub-Account Architecture. It’s my favorite way for those who don’t like Tracking. Explain this one, since it is a game changer.

The Sub-Account Method: Set It Up Once, Track Automatically

Let’s see how the Sub-Account method works.

You have different bank sub-accounts for different big expenses. One rental/mortgage unit. One for groceries. One for transportation. One for entertainment. One for miscellaneous bills.

When payday is here, you automatically transfer money to each account according to your spending plan: $800 to Groceries, $150 to Gas, $100 to Entertainment.

So, you make a purchase at the grocery store, you are using the grocery account. Once that account reaches zero, it’s the end of your month’s worth of groceries. The account you are interested in is your tracker. No app. No spreadsheet. Simply look at your balances.

In this approach, digital banking tools are employed to set up distinct envelopes for various spending categories. You are automating your transfer and paying your bills so that your essentials are always paid and you are able to see your funds that are available for discretionary use.

It is the envelope budgeting system for 2026. It’s also great for those who don’t like traditional tracking.

Many online banks allow you to make sub-accounts for free. The set-up time is about 20 minutes. Once you’re done, keeping track of your income and expenses becomes a fairly automated process.

The first month of tracking is a data gathering period. You don’t want to be a perfectionist. You’re trying to understand where all your money is going.

Many people have no idea of how they will be spending their money when they jump into a budget. They then put on unrealistic budget goals and feel like failures when they fail to hit them in week one.

Track first. Cut later. Look at the data, it will tell you where the issues are.

If you keep track of what you actually spend, compared to your budget, then you will keep your money under control and have a better idea of where you can save. While that’s a professional type of budgeting, tracking one’s budget obviously applies to one’s own monthly budget plan.

If you have followed for 30 days, you will have actual numbers. That’s where your budget becomes real, it’s not a guess. If you want to see how this tracking step fits into the full budgeting process from start to finish, that overview is worth bookmarking.

Read Your Budget Monthly (That’s What Makes The Difference!)

A budget isn’t a one-shot paper.

It is a tool that is alive and evolves along with your income, expenses, and priorities. When it’s set and forgotten for weeks, it’s useless.

I check my budget on a monthly basis. This will take approximately 10 minutes. And that habit is the one and only reason, that my budget works longterm.

I came across a word that I heard which I had not encountered before – Vibe Check Weekly Review. It was created for two people, but I have modified it to be used by one person. I review my spending every month to see if it aligned with my spending plans and long-term goals. No shame. No judgment. Just honest assessment.

This is done by the professionals in a systematic manner. They make budget adjustments as needs and priorities change. Personal budgets should be the same.

One person I know said it just right. Budgets are not a fixed plan. You need to check and update regularly with respect to the changes in prices and life. Pay an annual bill once and update your budget right away. This is what’s known as dynamic budget management.

Without a review, you’ll find yourself in excess of your budget. You will lose any chances of redirecting excess. And you will think that budgeting doesn’t work when, in fact, you weren’t paying attention.

You got a 10 Minute Monthly Budget Review (Simple Checklist)

I ask myself 5 questions at the end of each month. That’s it. Five questions, 10 minutes and I know where I stand!

(1) Was my salary as I thought it would be?

If you had less income, why? Where did the additional come from if you had more? This question holds your attention to income expectations.

2. What were the areas of my spending that exceeded my budget?

Examine your spending groups. Where did you go over? Don’t beat yourself up. Just notice it. If you have been finding that you’re spending more on food than you make, then perhaps your food spending is too low.

3. In which areas did I spend less than I needed to and can I bring forward the excess?

Suppose you had planned to spend $100 on entertainment, but you actually only spent $60, you then have $40 to go someplace else. Perhaps it’s put into your emergency savings. Perhaps it helps lower the debt. Don’t allow money to go to waste. Assign it.

4. Contributed to emergency fund and savings goals?

This is the one question that does have to be answered. If it’s no, determine what the problem is and correct it during the next month. It is not an option to not save.

5. Do I have the same goals or have they changed?

Perhaps you’ve had one of those raises. Perhaps you saw an increase in rent. Perhaps you’re just in a different world by now. Update the budget to reflect your life now, not 3 months ago.

This budget review process is not a judgment process. It’s a question of learning and adapting. You learn a little more about your spending each month you are reviewing. Problems are identified early. You celebrate progress.

And that is how it is. Overspending prevention takes place in the review, too. If you notice a trend, it can be corrected a long time before it becomes a problem.

Make reviewing a habit. Put it on your calendar. Think of a meeting with yourself. It’s that 10 minutes per month that helps your monthly budget stay on track.

Individuals who audit budgets are successful. Those who fail to quit. It’s that simple.

Why Budgets Fail (And the Mistakes That Cause It)

I want to explain why budgets fail because if you’ve tried budgeting in the past, which you have, it’s not a character flaw. It is typically an easily corrected error.

Let’s look at the top six budget-busters based on actual events, actual people.

The first mistake is to take on a budget without first keeping track of it

Many people make a budget, but don’t know how their money is being spent. They venture a hypothesis for categories. They have set random numbers. Then they spend the entire budget in week 1 and they feel like they are failures.

This is exactly what I did when I first started budgeting! My grocery budget is $200 – that seemed like a fair number, and I spent $380 during the first week. I felt I was a failure until I realized it wasn’t me, it was the budget!

The solution is simple. Monitor for a full month prior to establishing budget constraints. Let the facts tell you the truth! Then set realistic budget targets based on your actual spending, not what you want you spent.

Mistake #2: Forgetting to include whole categories of expenses.

I know someone that planned their budget for renting, paying their car, paying their utilities, and then forgot to pay for food. His budget just didn’t seem to be working out until someone noticed he had a problem.

Go back to the expense section. Be sure to include all fixed costs, all variable costs and all oddball costs. If it’s going to cost money, it goes in the budget.

Error #3: Having the budget too tight to allow for breathing room.

If you use your budget as a guideline and can’t afford to go out to dinner, can’t afford a cup of coffee, and can’t afford to buy a dollar of fun, you will have to break it. Then you will think that it’s too difficult to manage the budget.

What’s the truth, you will require cash to stroll around with. Allow yourself a small amount of money to spend while keeping the ‘fun money’ label off of it, perhaps $50 a month. And if your budget has been too tight for a while and you have been reaching for your credit card to fill the gaps, it is worth checking how much credit card debt is too much before you finalize your numbers.

An expenditure that doesn’t require any reason or tracking. That limited freedom helps to keep the rest of the budget in check.

I was told by one that it took him three months to get into his stride. That’s normal. Be kind to yourself and allow yourself time.

Temptation #4: Exposure to temptation all the time.

One person said the battle stops when the temptation isn’t present. She put down her purse.She came to a halt to window shop. Avoided shopping at non-essential stores. Not subscribed to promotional emails.

You are just making it harder on yourself if you are trying to reign in money spent and you are still receiving offers and swiping through shopping apps. Remove the temptation. It becomes simpler to budget when your environment is supportive.

Error #5: Not anticipating minor, ongoing expenses.

The following is a great example. Three $6 coffees per week plus a tip equals more than $1,008 per year. That’s real money. However, it is small and comes often and so it remains ‘invisible’.

These costs can be seen when calculating annual costs. Take the number of daily or weekly activities and multiply by 365 or 52. Once you have a total of the annual numbers, you will be able to determine whether or not it is worth it. Sometimes it is. Sometimes it’s not. At least you are making a choice, you’re not floating around.

Error #6: Late start.

More than 78% of Americans earn and spend their income without a surplus. Many of them are awaiting the “right time” to begin budgeting. After the holidays. After tax season. Once they’ve settled that bill.

The key to ending the paycheck-to-paycheck cycle is to get a budget. There is no right or wrong time. Get a head start today, whatever you have, and with what you have.

Being short on money doesn’t mean you lack willpower. It’s about method. Once the method is fixed and the budget is in play, they take off.

You have just been introduced to the 7 steps of effective budgeting

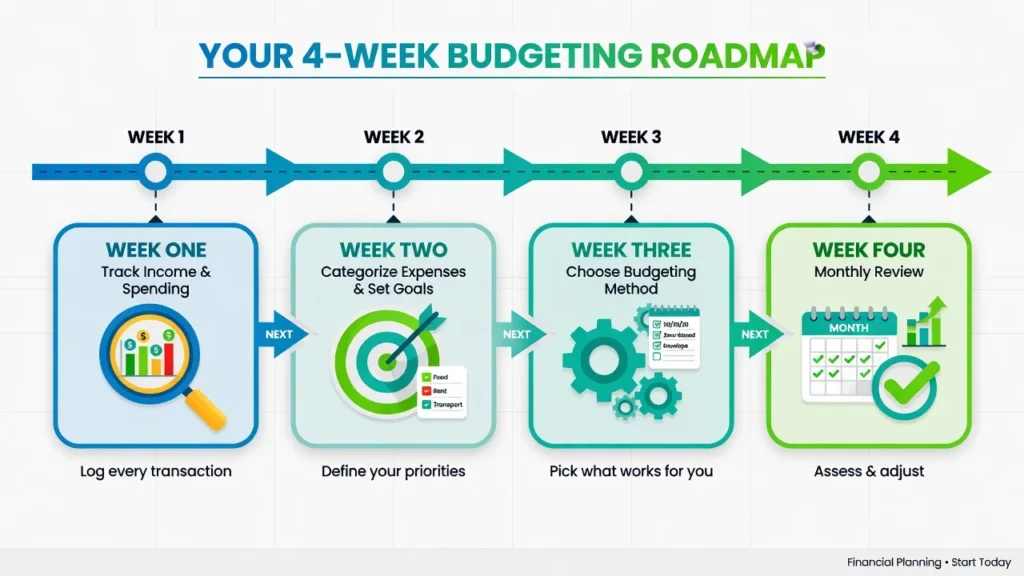

Now let’s give you a quick first month’s action plan that brings them all together

Consider this your financial plan roadmap. Don’t attempt to do it all at once. Take it on a weekly basis.

Week 1: Document all the income and expenditures you make during the week.

Record the amount of your net income from each pay source. Next, keep a record of all the money you spend over the course of one week. Use an application, a spreadsheet or simply your bank statement. You’re gathering information, not making judgments about yourself.

Week 2: Classify expenses and create objectives.

Use spending information from week 1 to categorize it. Fixed expenses. Variable expenses. Irregular expenses. Add up the totals. Next, set 2-3 financial goals. One short, one long. Be specific, and assign a dollar value to them.

Week 3: Select your budgeting approach and establish your budgeting system.

Choose one of the three ways I demonstrated to you. 50/30/20. Zero-based. Anti-budget. The one that is the least painful.

Set up your system. If you’re using an app, connect your accounts. If you have chosen the Sub-Account method, then you have to open the accounts and automate the transfers. For a spreadsheet, create the spreadsheet template.

Match each dollar to income, expenses and goals.

Week 4: Check-in, tweak and solidify the monthly habit.

At the end of the month conduct the 5 question review checklist that I provided you with earlier. See what worked. See what didn’t. Make the necessary calculations for next month.

Then make a commitment to conduct this review EVERY MONTH. Schedule a date for it. Make it non-negotiable.

That’s it. Four weeks. Seven components. One working budget.

This isn’t magic. Not a quick get rich program. It’s simply a lifestyle choice of living within your means, and doing so month after month.

There was a guy that I had heard who had been budgeting for 53 years. He stated that it was not a secret anymore. He and his partner just decided to live within their means. For decades. That was it.

Financial planning and money management is what it is! Making small, regular choices that lead to financial stability in the long run.

The first and foremost habit to get out of the paycheck-to-paycheck cycle is to get started on a budget. It’s the core of monetary administration, and it’s the instrument which constructs the life you truly wish to have.

Don’t expect perfection. All you have to do is get started. Apply these 7 principles of effective budgeting! Track your progress. Adjust as you go. And gift yourself with knowing where your money’s going and where your money is going. That’s the way you create real financial stability.

That’s the budgeting we know how to do.

A series of questions that are commonly asked about budgeting

What exactly is meant by the 50/30/20 rule and is it effective for everyone?

The 50/30/20 rule allocates 50 percent of your income to needs, 30 percent to wants and 20 percent to savings and debt repayment.

It’s a good template to start with, but it is not universal. The typical division of income is between needs and disposable income is not always possible, especially in higher cost of living cities, where disposable income can be 60-70% of income. In those situations, manipulate the percentages, maintaining the framework. The rule is most effective for those who have a consistent and predictable income. If your income fluctuates, it’s a guideline and not a rule.

How to build a budget when you don’t have a steady monthly income?

Your budget should be based on your bottom line income, not your average income, for the lowest month of the last twelve months. This will prevent you from committing too much during quieter times of the year.

Instead of a fixed dollar amount, allocate percentages to your budget to adjust as you earn more or less income. One practical tool: Calendar Sync System – keep your bank account and digital calendar synced for a clear view of future bills and income shortfalls. This is a shift from reactive to proactive money management.

Should I pay off my debt or add money to my emergency savings account first?

It is recommended to have a small, initial emergency fund, usually $1,000. Next, take on your high-interest debt aggressively.

The reason the order is important is that there is no such thing as an emergency if you don’t have an emergency fund. The starter fund changes that. After paying off high-interest debt, make the same payments to your emergency fund until you have 3-6 months of living expenses saved.

So what is zero-based budgeting, and is it worth it?

With zero-based budgeting, you give every dollar of money you bring in a job, a goal: to save, to pay bills, to buy groceries, to go for entertainment, to pay off debt, to pay for a wedding, etc., until all the money that comes in is gone. There is no dollar that is not accounted for.

It takes a bit more work to get set up in the first place, however, the majority of the rebalancing is automated with modern budgeting applications. It pays off in terms of increased awareness and control over your finances. It works especially well if you’re looking to make aggressive debt repayments or maximize your savings. If you want to know exactly where each and every dollar goes, it’s worth the effort.

How many months before a budget really starts to pay off?

People typically see actual results in 60-90 days.

Avoiding the first month will be a little awkward and imperfect, but it’s normal. Do not consider the first month as a performance – it is a collection of data. You aren’t doing everything you planned, you are learning your actual spending habits. By month three, most people have sorted themselves out and the monthly review routine is fast and routine. The purpose of the month one is information and not perfection.

What are the primary reasons why people have trouble keeping their budgets?

Here are five reasons for most budget failures: Spending Without Knowing Any Baseline Data — You can’t make an accurate budget without tracking the spending baseline. Being too restrictive – no fun means no sustainability – Irregular costs that burst budgets, such as car repairs, medical costs or yearly subscriptions With the incorrect approach — a system that’s not suitable for you, it’s not going to work! Leaving after the first month — most quit right before the first month; quitting is always the hardest month. All of these can be solved once they can be named.

What are key elements to Ramsey’s successful budgeting?

The five principles of Ramsey’s rule are: give less than you earn, make a monthly budget that includes giving, saving, spending, paying yourself first (save first, spend second), and avoid debt and use windfalls and income increases strategically. His four walls approach to spending priorities includes food, utilities, shelter, and transportation first. These are non-negotiables. All the other walls are turned to after securing the 4 walls.