50/30/20 Budget: Simple Rule to Manage Your Money

If you’ve been struggling to make your money work, the 50/30/20 budget rule might be exactly the framework you’ve been missing.

I still remember that Tuesday night third week of the month, sitting at my kitchen table with my banking app open, watching that number: $47. Payday was still nine days away.

I wasn’t broke by any definition. I had a steady paycheck coming in every two weeks. But somewhere between rent, groceries, and what I told myself were “small purchases,” the money just evaporated. Every single month.

That’s when I stumbled onto the 50/30/20 budget rule, and it genuinely changed how I relate to money. Not in a dramatic overnight way more like a slow exhale after months of holding my breath.

In this guide, I’ll walk you through exactly what this rule is, how to calculate it for your actual income, and how to apply it in real life whether you’re making $30,000 or $100,000 a year. No jargon, no complicated formulas.

What Is the 50/30/20 Budgeting Rule?

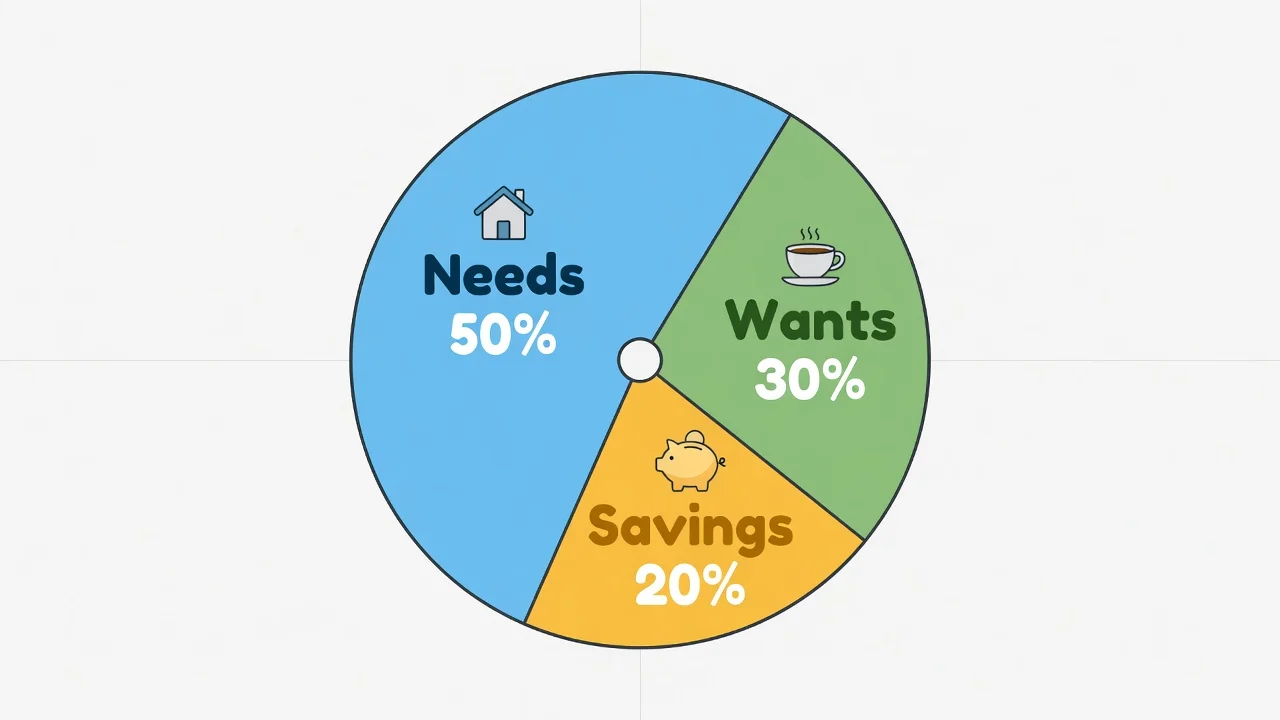

The 50/30/20 budget rule is a straightforward formula for dividing your monthly take-home pay into three categories. Half goes to needs the things you’re obligated to pay. Thirty percent goes to wants the things that make life enjoyable. And 20% goes to savings and debt repayment the part that builds your future.

Simple? Yes. But don’t let that simplicity fool you into thinking it’s not powerful.

The rule was created by Senator Elizabeth Warren when she was a Harvard bankruptcy law professor. She introduced it in her book All Your Worth: The Ultimate Lifetime Money Plan, co-written with her daughter Amelia Warren Tyagi after years of researching why Americans went broke. Their conclusion: most financial disasters weren’t caused by bad luck. They were caused by the absence of a simple, reliable framework for money management.

What makes this particular budgeting method work long-term is the built-in permission to spend. The 30% wants category isn’t a guilt trap it’s a protected allowance. You’ve already covered your obligations and your future. That remaining 30% is yours to enjoy freely, without second-guessing every purchase.

Most budgets eventually fail because they treat financial wellness as pure restriction making you feel guilty about every coffee, every dinner out, every small pleasure. That constant guilt is exhausting, and eventually, you just give up entirely.

The 50/30/20 budget framework is different. It gives you structure without requiring you to track every single dollar. I don’t need to know exactly what I spent on lunch last Thursday. I just need my three category totals to stay in range by month’s end.

One honest caveat before we go further: this budget framework works best for people who aren’t in extreme financial crisis. If you’re underwater with debt or barely covering basic bills, a different strategy may need to come first I’ll address that specifically later in this guide.

For most people who simply need a clear system for managing their personal finance situation, though, this rule hits the right balance between structure and flexibility. Think of it as guardrails on a mountain road. You have room to move, but you won’t go off the edge.

How the 50/30/20 Budget Breakdown Works

Let’s get into the actual mechanics. I’m going to walk you through each of the three categories with real dollar amounts because when I was starting out, abstract percentages didn’t help me at all. Seeing $1,200 for rent and $300 for groceries in a real budget made everything click in a way that “50%” never did.

One thing I genuinely appreciate about this framework: the percentages stay fixed regardless of your income level. Whether you get a raise, switch jobs, or move to a more expensive city, the three categories scale automatically. Your dollar amounts shift, but the structure never does.

50% for Needs: Your Essential Monthly Expenses

Your needs category covers roughly half of your take-home pay specifically, the essential expenses you’re obligated to pay regardless of how you feel about them. Miss these and there are real consequences: eviction, repossession, late fees, or disruptions to your ability to work.

Here’s what goes in this category:

Housing: Rent or mortgage, property taxes if you own, renter’s insurance. For me, that’s $1,400 a month for a one-bedroom apartment.

Utility bills: Electricity, water, gas, trash service. I budget about $120 a month, though it jumps in summer with air conditioning running constantly.

Groceries: Basic food for cooking at home. Notice I said basic the fancy organic olive oil and artisan cheese go in wants. Regular staples are needs. I spend roughly $300 a month here and use a grocery budget calculator to stay on track.

Transportation: Gas, car payment, insurance, maintenance, or public transit whatever gets you to work. My car is paid off, but I still budget $250 monthly for gas, insurance, and repairs.

Insurance premiums: Health insurance, life insurance. Mine runs about $180 a month after my employer’s contribution.

Minimum debt payments and this is the categorization that trips people up most: your required minimum payment on credit cards, student loans, or car loans goes here in needs. The extra amount you voluntarily pay above the minimum belongs in your 20% savings and debt repayment bucket. More on that in a moment.

One thing that genuinely changed how I thought about this category: the word “needs” is slightly misleading. A more accurate label would be “obligations.” These are things you’re legally or contractually required to pay regardless of whether you chose wisely when you originally signed up.

If you’re renting a luxury apartment with a gym and rooftop pool, you don’t technically “need” those amenities. But you signed that lease, so the full rent is an obligation until it expires. It goes in the 50% needs category. Understanding this distinction removes a lot of the stress around categorizing monthly expenses.

To put this in perspective: someone bringing home $5,000 a month who allocates $2,500 to needs paying $1,800 in rent and $350 for transportation has $350 left for groceries and utility bills combined. That’s about $85 per week for food. Tight, but workable. That’s the honest reality of the 50% ceiling in a high cost of living area.

If your essential expenses already exceed 50% of your paycheck, you’re not alone and you’re not doing it wrong. I’ll walk through exactly what to do about that later in this guide.

30% for Wants: Discretionary Spending You Choose

This is the category that makes budgeting actually sustainable the 30% you get to spend on things that bring you genuine enjoyment without any obligation to justify them.

Your discretionary spending covers everything that improves your quality of life but isn’t a contractual obligation. You could theoretically live without these things. You simply don’t want to, and the 50/30/20 framework says that’s completely fine.

What falls into this category:

Dining out: Restaurants, delivery apps, lunch with coworkers. I budget about $200 a month here and don’t track it obsessively because it’s already accounted for.

Entertainment expenses: Movies, concerts, sporting events, streaming services. Yes, Netflix and Spotify go here, not in needs. I know they feel essential, but you wouldn’t die without them. I budget roughly $150 monthly for subscriptions and occasional events.

Non-essential shopping: New clothes when your current wardrobe is fine, the latest phone when your old one works, home decor, gadgets anything you want rather than strictly need.

Hobbies and recreation: Gym membership, craft supplies, books, video games, whatever you do for fun. My gym costs $45 a month. I keep it in wants because free exercise options exist I just choose to pay for the gym.

Travel: Weekend trips, flights home for the holidays, that vacation you’ve been planning.

Upgrades on things you need: This one surprises people. You need food, but you don’t need the premium version. You need clothes, but you don’t need the designer label. The gap between the basic option and the upgraded choice? That gap is a want.

When I first started honestly categorizing my spending, the number stopped me cold. I’d thought of myself as pretty frugal, but my wants were running at 41% not 30%. That’s not a small rounding error. That’s an entire budget category sitting in the wrong place.

Cutting back was uncomfortable at first. But knowing I still had a full 30% to spend made it manageable. I wasn’t giving up everything I was just getting more deliberate about which wants actually mattered to me.

Last month I bought concert tickets without that familiar knot of anxiety about whether I could afford it. I already knew I could. Spending money without that background hum of financial anxiety that’s what a working budget actually feels like.

20% for Savings and Debt Repayment: Building Your Future

This is the category that actually builds your financial foundation. Every dollar that flows here whether into an investment account, an emergency fund, or toward eliminating credit card debt is doing work on your behalf while you sleep.

Here’s what belongs in this 20%:

Emergency fund first. Before investing a single dollar, build a cushion for the unexpected. I started with a $1,000 goal enough to cover a car repair or a surprise medical bill without going into debt. Now I’m working toward six months of living expenses. Many people wonder how much you should have saved by age 30 this article helped me set realistic targets while my emergency fund grows.

Retirement contributions beyond your employer match. If your company matches 401(k) contributions, capture that match first it’s literally free money. Any additional retirement savings beyond that match comes from this 20%. I’m contributing an additional 5% of my net paycheck to retirement accounts beyond my employer match.

Investment accounts. Index funds, stocks, whatever your long-term financial planning strategy looks like. I invest $200 monthly in index funds nothing complex, just consistent contributions that compound over time.

Extra debt payments above the minimum. The required minimum payment belongs in needs. This 20% is where you attack the principal making extra payments on credit card balances, student loans, or your car loan to eliminate debt faster.

A question I get constantly: where exactly does debt fit in this budget? The answer is both places, depending on the payment type.

Say you have a credit card with a $100 minimum payment and you want to pay $300 total this month. The required $100 goes in needs. The voluntary extra $200 comes from your 20% savings and debt repayment allocation. Why does extra debt repayment count as savings? Because eliminating high-interest debt delivers a guaranteed return equal to that interest rate. Paying down a credit card at 22% interest is equivalent to a guaranteed 22% investment return which is better than virtually any market option available to everyday people.

One more thing worth emphasizing: 20% is the floor, not the ceiling. I started at exactly 20% when I was first getting my finances in order. As I’ve trimmed some discretionary spending and grown my income, I’m now closer to 25%.

But even at a consistent 20%, the financial goals you’re working toward become achievable. The compounding math behind that consistent savings rate is dramatic enough that I’ll walk through actual projections at different income levels toward the end of this guide.

How to Calculate Your 50/30/20 Budget (Step-by-Step)

One of the biggest reasons people abandon budgeting early is that articles explain the concept but skip the actual math behind paycheck allocation. They tell you to spend 50% on needs but leave out the most basic question: 50% of what, exactly? Your salary before taxes? After? What if you get paid every two weeks or pick up freelance work on the side?

I had every one of these questions when I started. Here’s the step-by-step process I actually use — no assumptions, no glossed-over steps.

One thing I genuinely appreciate about this framework: the percentages stay fixed regardless of your income level. Whether you get a raise, switch jobs, or move to a new city, the structure scales automatically. The dollar amounts change; the framework never does.

Step 1: Calculate Your After-Tax Income

This is where most beginners go wrong myself included the first time I tried this.

Your gross income is what your employer pays you before deductions hit. Your net income, or take-home pay, is what actually lands in your bank account after federal and state taxes, Social Security, Medicare, health insurance premiums, and any other pre-paycheck deductions come out.

Always base your 50/30/20 calculations on your net income. This is non-negotiable.

Why it matters: if you earn $60,000 a year, your gross monthly income looks like $5,000. But after all deductions, your actual take-home might be $3,800 to $4,200, depending on your tax situation and benefits. If you build your budget around $5,000, you’re planning with money you never actually see. I made exactly this mistake my first month felt great about my budget plan, then ran out of money two weeks in.

To find your real after-tax income: pull up your most recent pay stub and look for the line that says “Net Pay.” That’s your number. If you’re paid every two weeks, multiply it by 26 and divide by 12 to get your monthly figure. Paid twice a month? Simply multiply by 2.

Quick note on 401(k) contributions: if your retirement savings come out before taxes and never touch your bank account, you have two valid options. You can use your actual take-home pay and not count those contributions toward your 20%, since they’re already being funded automatically. Or you can calculate based on your pre-retirement-deduction income and include the 401(k) in your 20% savings target. Both methods work just pick one and stick with it consistently.

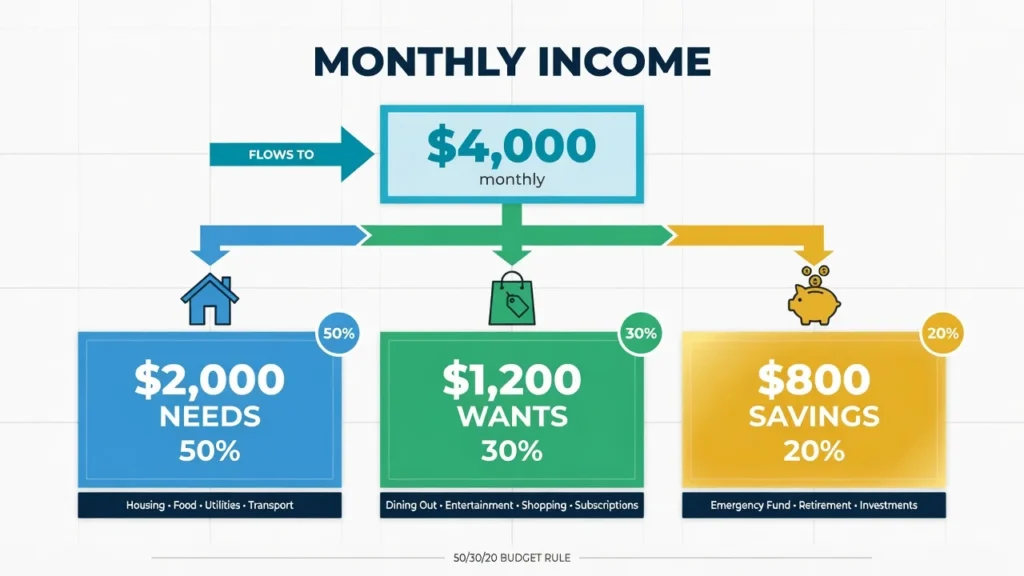

Step 2: Calculate Your Three Category Budgets

Once you know your monthly take-home pay, the actual math takes under a minute. Multiply your income by three numbers:

- Income × 0.50 = Needs budget

- Income × 0.30 = Wants budget

- Income × 0.20 = Savings target

Using a $4,000 monthly take-home as an example:

- $4,000 × 0.50 = $2,000 (Needs)

- $4,000 × 0.30 = $1,200 (Wants)

- $4,000 × 0.20 = $800 (Savings)

Your entire monthly budget in three lines. $2,000 for obligations, $1,200 for enjoyment, $800 toward your future. Over a full year, that $800 per month becomes $9,600 saved.

The first time I ran these numbers for my own income, I genuinely sat there waiting for the catch. There isn’t one that’s the whole calculation.

If you prefer a tool to do the split for you, NerdWallet offers a free budget calculator specifically built around the 50/30/20 rule. Enter your income and it outputs your three category targets instantly. That said, doing the math by hand at least once helps you actually internalize the numbers which makes you far more likely to maintain the budget long-term.

Step 3: Track Your Current Spending

Most people skip this step entirely and it’s the one that makes everything else actually work.

Before you try to change your spending, spend one to two months simply tracking what you already spend. Categorize every expense into one of the three buckets: needs, wants, or savings. Don’t change anything yet. Just watch.

This baseline exercise shows you the real picture of your money habits and most people are surprised by what they find. Either their needs are consuming well over 50%, or their wants have silently crept up to 40% or higher without them ever consciously deciding that.

I went back through three months of my own bank statements before setting my first real budget. What I found: my needs were actually reasonable at about 52%. But my wants were running at 41%, and I was only saving 7%. My budget categories were completely out of balance, and I had no idea.

Seeing those numbers written down changed my behavior without anyone lecturing me. The data did the work.

How you track is up to you. A budgeting app connected to your bank account does the categorization automatically. A spreadsheet gives you more control and visibility. A notebook and pen works if technology feels like friction. I’ve used all three at different points the key is picking one and staying consistent for at least 60 days before deciding whether it suits you.

Real-Life 50/30/20 Budget Examples by Income Level

What most budgeting articles skip and what actually helps people implement the rule is seeing real dollar amounts at different income levels.

Percentages mean different things depending on what you earn. A $500 grocery budget feels very different on $2,500 a month versus $8,000 a month. Same percentage, completely different reality.

Below are four income-level examples with actual dollar allocations. Find the one closest to your take-home pay and treat it as a starting template adjust the individual line items to match your real monthly expenses.

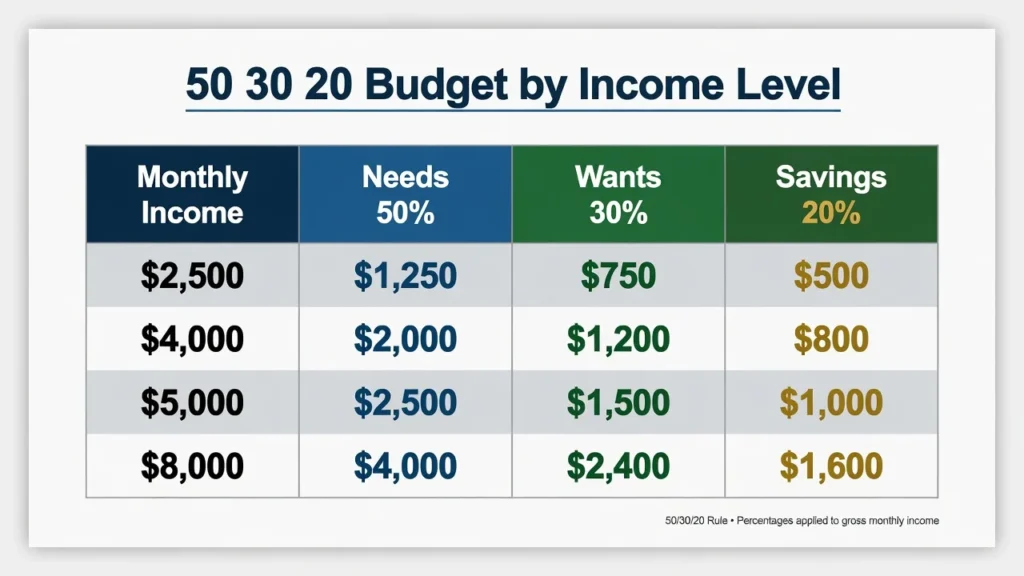

Example 1: $2,500 Monthly Take-Home Pay (Around $30K Per Year)

This is a tight budget and I’m not going to dress it up as anything else. But it’s absolutely workable, especially in areas with lower housing costs.

Needs (50%) = $1,250

- Rent: $800

- Utilities: $150

- Groceries: $200

- Transportation (gas + insurance): $100

Wants (30%) = $750

- Dining out (1–2 times per month): $80

- Streaming service: $20

- Hobbies and personal care: $100

- Flexible buffer for irregular expenses: $550

Savings (20%) = $500

- Emergency fund contributions until you reach three months of living expenses, then redirect toward retirement or debt repayment

That $550 flexible buffer in your wants category sounds generous until you realize it needs to cover everything from a new pair of shoes to a friend’s birthday dinner to quarterly car registration. At this income level, pre-planning for those irregular expenses not treating them as surprises is the difference between a spending plan that holds and one that collapses every other month.

Even so, $500 saved every month adds up to $6,000 in a year. If you’re working with even tighter numbers, see our guide on how to budget money on a low income. That’s a fully funded starter emergency fund within months and the beginning of a savings habit that will compound significantly as your income grows.

Example 2: $4,000 Monthly Take-Home Pay (Around $48K Per Year)

At $4,000 a month, the 50/30/20 rule starts to show its full potential. There’s enough income to cover solid essential expenses, maintain a genuine wants category, and still save meaningfully without constant financial stress.

Needs (50%) = $2,000

- Rent: $1,200

- Utility bills: $180

- Groceries: $350

- Transportation: $150

- Health insurance (out-of-pocket): $120

Wants (30%) = $1,200

- Dining out: $300

- Entertainment expenses and events: $150

- Non-essential shopping: $200

- Gym membership: $50

- Hobbies: $200

- Flexible buffer: $300

Savings (20%) = $800

- Emergency fund first, then retirement contributions and accelerated debt repayment

The wants category here gives you real breathing room. $1,200 a month on discretionary spending means you can eat out regularly, maintain your gym membership, fund hobbies, and still have $300 left over for irregular purchases without tracking every single coffee or impulse buy.

And $800 monthly into savings starts doing serious work over time. Within a year, you’ve built nearly $10,000 enough for a fully stocked emergency fund with room left over for investment contributions.

Example 3: $5,000 Monthly Take-Home Pay (Around $60K Per Year)

At $5,000 a month, the most important behavioural shift is automation. When you earn enough to feel comfortable, the temptation to delay savings transfers grows. Setting them up to happen automatically on payday before you ever see the money removes that temptation entirely.

Needs (50%) = $2,500

- Rent: $1,500

- Transportation (car costs or transit): $650

- Groceries (roughly $85/week): $350

Wants (30%) = $1,500

- Fixed lifestyle costs (gym, streaming services, personal care): $400

- Flexible weekly spending (dining out, events, shopping): ~$275 per week (divide the remaining $1,100 by 4 weeks)

Savings (20%) = $1,000

- Index fund investments: $250 (5% of income)

- Retirement contributions: $250 (5% of income)

- Emergency fund: $500 (10% until fully funded, then redirect to investments)

The weekly spending approach for your wants is something I’ve found particularly practical. Once you subtract your fixed lifestyle costs gym membership, streaming subscriptions, regular services — from the $1,500, divide what’s left by the number of weeks in the month. That number becomes your weekly discretionary budget. Spend it how you like, without tracking every individual purchase. Simple and surprisingly effective.

Example 4: $8,000 Monthly Take-Home Pay (Around $96K Per Year)

At $8,000 a month, the 50/30/20 rule creates genuine financial momentum but only if you resist the pull to let every income increase translate directly into lifestyle upgrades. (I’ll address this phenomenon, called lifestyle inflation, in depth in the common mistakes section.)

Needs (50%) = $4,000

- Mortgage or rent: $2,200

- Utility bills: $250

- Groceries (family): $600

- Car payment and transportation costs: $500

- Insurance premiums (health, auto, home): $300

- Minimum debt payments: $150

Wants (30%) = $2,400

- Dining out and food experiences: $400

- Travel fund contributions: $300

- Entertainment and events: $200

- Non-essential shopping: $400

- Hobbies and personal development: $300

- Flexible buffer and lifestyle upgrades: $800

Savings (20%) = $1,600

- Max out retirement contribution limits first, then invest beyond them through individual investment accounts. At $1,600 per month invested consistently over 30 to 40 years, you’re building genuinely life-changing wealth through the power of compounding.

The key discipline at this income level isn’t the budgeting math it’s staying aware that the wants category grows in dollar terms as income rises. The 50/30/20 budget framework keeps it proportional to savings rather than consuming everything a raise produces.

Needs vs Wants: How to Categorize Any Expense

The single biggest challenge I hear from people trying the 50/30/20 budget for the first time: they can’t figure out whether something counts as a need or a want.

Some expenses genuinely sit in a gray area depending on your specific circumstances. What helped me most was reframing the question entirely. Instead of asking “is this a need or a want?” I started running three questions in sequence.

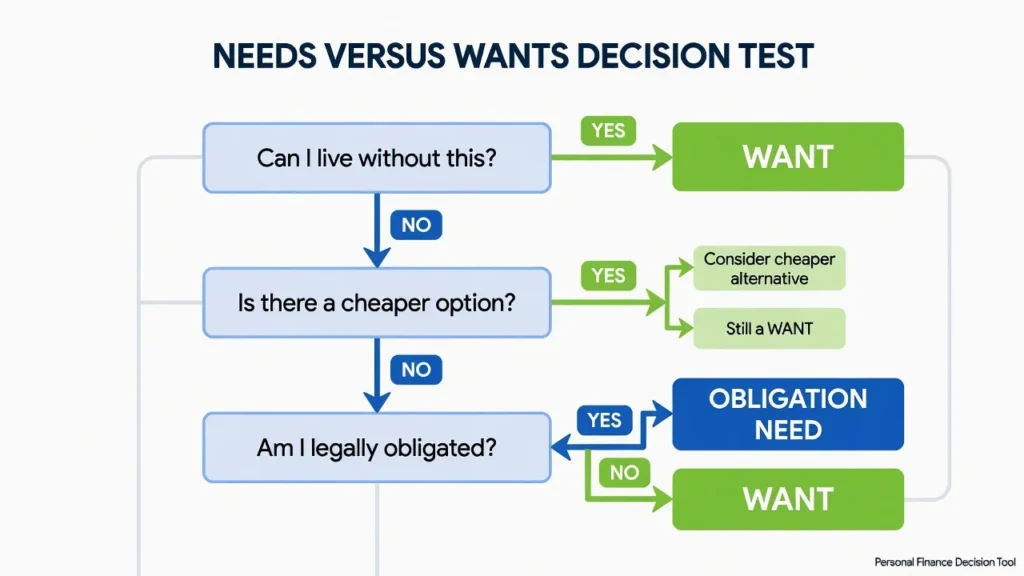

The Three-Question Categorization Test

Question 1: Can I live and do my job without this expense?

If yes it’s a want, full stop. A gym membership? Free exercise exists. Streaming services? You’d survive. Premium coffee? Definitely a want. If the answer is genuinely no, move to Question 2.

Question 2: Is there a significantly cheaper way to meet this same requirement?

If you need transportation but you’re driving a $600/month new car when a reliable used car would cost $200, only the basic transportation requirement is a need. The upgrade is a want. Where possible, mentally split the expense: categorize the baseline cost as a need and the premium above that as a want.

Question 3: Am I legally or contractually obligated to pay this?

Here’s where the “obligations” framework becomes genuinely useful. When you signed a one-year lease on an apartment you didn’t strictly need at that price point, the decision to choose it was a want-level choice. But the moment you signed, the monthly payment became an obligation. It goes in the 50% needs category until the lease ends.

This reframe eliminates a lot of self-judgment. You stop re-litigating past financial decisions and focus instead on accurately categorizing what you’re obligated to pay right now.

Common Gray-Area Expenses : Where They Actually Belong

Here are the expenses that cause the most confusion and where they actually belong:

Internet service: Lands in needs for most people today, especially if you work from home. A basic plan is genuinely necessary for most working adults. However, if you’re upgrading to the gigabit ultra-fast plan when a standard plan would do the job, that upgrade cost is a want.

Gym membership: Generally goes in wants. Exercise itself is essential for health, but a paid gym membership is not the only way to exercise. For most people, the gym is a lifestyle choice and belongs in discretionary spending.

Car payment: Once you sign a car loan, the monthly payment is an obligation and goes in needs. But the choice of that specific car was heavily influenced by wants a useful reminder for future decisions.

Phone plan: A basic smartphone plan is a need. The premium unlimited-everything plan with annual phone upgrades is a want. Most people can function on a mid-tier plan; the extra cost for premium features is discretionary spending.

Pet care: Once you have a pet, essential costs food, basic veterinary care, necessary medications — go in needs. You took on responsibility for a living creature, so those costs are now obligations. Premium pet services like grooming, luxury beds, and specialty food brands go back in wants.

Clothing: Basic clothing you genuinely need meaning you don’t have it and the season requires it — goes in needs. Replacing items that still have plenty of life left, buying trending styles, or shopping for things you simply want all belong in wants.

Streaming services: These go in wants, full stop. It’s entertainment spending and belongs in your 30% discretionary budget alongside your other entertainment expenses.

The goal of this framework isn’t to make every enjoyable purchase feel like a guilty admission. It’s to give your budget categories enough accuracy that the whole system actually reflects your life which makes it far more likely to work.

50/30/20 Budget Templates, Spreadsheets, and Apps

Once you understand the rule and have your numbers, you need a budget planner or tracking system to put it into practice consistently. This is where a lot of people stall they spend more time comparing budgeting tools than they do actually budgeting.

Here’s my honest take after trying four different methods: the best system is the one you’ll open consistently. A straightforward tool you use every week beats a sophisticated one you abandon after two weeks.

Free Spreadsheet Templates (Excel and Google Sheets)

Building your own 50/30/20 budget worksheet or spreadsheet is worth doing at least once the process of setting it up forces you to think carefully about your expense categories in a way that using a pre-built template doesn’t.

Basic setup: Create four columns across the top Category, Budget Amount, and one column for each month of the year. This gives you a full year of tracking on a single tab.

Rows: List your income sources at the top, then create three labeled sections: Needs, Wants, and Savings. Within each section, give every expense its own row (rent, groceries, Netflix, and gym all get separate rows).

Three formulas you need:

=SUM(range)to total each expense category automatically=(category total / total income)formatted as a percentage to check your ratios in real time=(income − total expenses)to see your monthly surplus or deficit at a glance

Practical tips that save time:

- Freeze the header row (View → Freeze Panes) so column labels stay visible as you scroll through monthly data

- Color-code by type: green for income rows, light orange for expense rows, grey for totals

- Add “Annual Total” and “Monthly Average” columns at the far right these reveal spending patterns you’d never catch month-by-month. I discovered I spend nearly twice as much on groceries in December as in March. That single insight changed how I plan for the holiday season entirely.

Google Sheets works identically to Excel for this purpose, with the added benefit of automatic cloud saving and access from any device. I switched two years ago and haven’t looked back.

Best Budgeting Apps for the 50/30/20 Rule

If spreadsheets feel like too much work, budgeting apps handle most of the heavy lifting automatically. They connect to your bank accounts, import transactions, and categorize spending so you’re not manually logging every purchase.

YNAB (You Need A Budget): The most comprehensive 50/30/20 budgeting app available. Every dollar gets assigned a job before you spend it, and real-time tracking keeps you aware of your position at all times. There’s a monthly subscription fee, but many users report it pays for itself within the first month through spending awareness alone.

EveryDollar: A solid choice with both a free version (manual transaction entry) and a paid version (automatic bank sync). Built around assigning every dollar before the month begins which maps naturally to the 50/30/20 method.

PocketGuard: The most visual and minimal of the three. It shows exactly how much money you have available to spend after bills and savings goals are funded. Good for quick daily check-ins without deep category analysis.

NerdWallet’s free budget calculator: Not a full tracking tool, but excellent for the initial calculation step. Enter your monthly income and it instantly shows your three category targets useful when you’re just getting started.

A word of caution on apps generally: automation can create passive budgeting. When the app categorizes everything for you, it’s easy to stop thinking about individual purchases. I use an app for tracking but still do a manual review of my category totals once a month to stay genuinely engaged with where my money goes.

Using Notion to Track Your Budget

Notion has become popular for budgeting among people who like flexible, customizable systems. If you already use Notion for work or personal organization, adding a budget tracker there makes sense your systems stay consolidated and you won’t need to open a separate app.

The basic setup involves two linked databases. One holds your budget categories with planned amounts. The other holds individual transactions with date, amount, and category. Link them so each transaction connects to its category, then use Notion formulas to compare actual spending against planned budgets in real time.

The main advantage is flexibility you can build it exactly the way your brain works. The main disadvantage is setup time. It takes a few hours to configure properly and doesn’t connect to bank accounts, so you’ll enter transactions manually.

If you’re not already a Notion user, don’t start using it just for budgeting. The setup time isn’t worth it when a spreadsheet or dedicated budgeting app will do the job more quickly.

Simple Pen-and-Paper Method

Don’t underestimate this option. I started with a small notebook, and for the first three months of budgeting, it was the most effective tool I used.

The method is simple. At the start of each month, write your three category budgets at the top of a new page. Needs: $X. Wants: $Y. Savings: $Z. Throughout the month, every time you spend money, write down the amount and which category it came from. Run a quick weekly tally to see where you stand.

The main disadvantage is that manual math and missed logging days can create gaps that make the monthly total inaccurate. But if digital tools have consistently failed you whether from technical friction, app fatigue, or just disliking screens for this kind of task a notebook is not a fall back. It’s a legitimate system that works. Build the habit with pen and paper first. Once tracking feels natural, you can migrate to a digital tool if you want.

What to Do When Your Needs Exceed 50%

Here’s something most budgeting guides skip: the 50/30/20 rule doesn’t work perfectly for everyone right now. Not because the framework is flawed, but because housing costs, childcare, and debt payments in many parts of the world don’t cooperate with neat percentages.

If you ran the numbers and your needs came out to 65% or 70% of your take-home pay, you’re not doing it wrong. You’re dealing with a genuinely difficult financial situation that millions of people share.

High Cost-of-Living Adjustments

In cities where rent or mortgage alone consumes 40–50% of take-home pay, the standard 50/30/20 split simply doesn’t have room to breathe. Someone paying $2,200 in rent on a $4,500 monthly income is already at 49% before buying a single grocery item. That math leaves no space for the standard budget breakdown to function properly.

Practical options to consider or reduce your monthly expenses in other areas.

Get a roommate. Splitting rent can cut housing costs by 30–40% immediately the single fastest adjustment available.

Move slightly farther from the city center. A longer commute that adds $100/month in transportation might still save $300–400/month if rent drops meaningfully.

Temporarily modify your target ratio. There’s no shame in running a 60/25/15 or 65/25/10 split while you work toward reducing fixed costs. Saving 10–15% consistently is infinitely more valuable than saving nothing while waiting for perfect conditions.

The financial goals don’t disappear. You’re just on a longer timeline. As income grows or costs come down, you adjust the ratio back toward the ideal.

When Debt Makes the Rule Impossible

High minimum debt payments are the other common reason the 50/30/20 split breaks down. According to the Federal Reserve’s Survey of Consumer Finances, average American household debt payments — including credit cards, auto loans, and student loans frequently exceed $1,000 per month for middle-income families. At that level, debt payments are consuming what should be your wants and savings categories before you’ve made a single discretionary choice.

If that’s your situation, I’d recommend treating aggressive debt payoff as a temporary Phase 1 before adopting the full 50/30/20 structure. Put as much as possible toward eliminating your highest-interest debt. Keep a minimal emergency fund even just one month of basic expenses so that unexpected costs don’t push you further into debt. Once your required debt payments shrink to a manageable portion of your take-home income, the 50/30/20 framework becomes not just achievable but relatively easy.

Think of aggressive debt payoff as the prerequisite for 50/30/20, not a sign that the framework has failed you.

Modified Ratios That Still Work

The underlying principle matters more than hitting exact percentages. That principle: cover your obligations, enjoy life in moderation, and always save something for the future.

Here are ratios real people use successfully in difficult financial circumstances:

- 60/30/10: For high cost-of-living areas where housing alone pushes needs above 50%

- 70/20/10: For people with significant debt or high childcare costs

- 55/25/20: For people who want to protect the 20% savings floor while needs run slightly high

The most important thing is having a conscious, intentional spending plan even an imperfect one. An active 65/25/10 budget beats an abandoned 50/30/20 budget every single time.

50/30/20 vs Other Budgeting Methods

Something I’ve come to believe after years of tracking my finances: the 50/30/20 rule is a starting framework, not a permanent destination. As you become more fluent with your money, you’ll naturally develop a more personalized system that reflects your specific income, goals, and lifestyle. But you need somewhere to start, and this is one of the best options available.

Here’s how the most popular budgeting strategies compare.

50/30/20 vs Zero-Based Budgeting

The 50/30/20 method groups your spending into three broad categories and checks percentages. Zero-based budgeting works completely differently. With zero-based budgeting, you assign every single dollar of your income to a specific purpose before the month begins, so that income minus all assigned expenses equals exactly zero.

In practice, the two methods feel completely different day-to-day.

With 50/30/20, you might say “I have $1,200 for wants this month” and spend freely within that category without tracking individual purchases closely. With zero-based budgeting, you’d assign $300 to dining out, $150 to entertainment, $200 to clothing, $100 to hobbies, $50 to personal care, and so on until every dollar has a specific job.

The 50/30/20 approach is more forgiving and requires far less time. You don’t need to predict every expense category perfectly. If you spend more on groceries and less on gas this month, it doesn’t matter as long as your total needs category stays within 50%.

Zero-based budgeting rewards detail-oriented people and those with irregular or variable income. Freelancers, contractors, and commission-based workers often prefer it for this reason.

If you’re new to budgeting or find granular tracking overwhelming, start with 50/30/20. It builds awareness and habits without burning you out. If you’re already in control of your spending and want more precision or if your income varies significantly month to month zero-based budgeting gives you that tighter grip.

The two methods aren’t mutually exclusive. I use 50/30/20 as my primary framework but apply zero-based principles to my food spending specifically the one category I’ve always struggled to keep in check. Knowing your options lets you build a hybrid that fits your actual habits.

50/30/20 vs Envelope Method

The envelope method is one of the oldest budgeting strategies around. You take cash out at the start of the month and physically divide it into labelled envelopes one for groceries, one for gas, one for entertainment. When an envelope is empty, that category is done for the month. No exceptions.

The difference from 50/30/20 is striking. The 50/30/20 budget works seamlessly with digital money direct deposit, debit cards, online payments. The envelope method is cash-based and tactile. You can physically see how much money is left in each category.

The spending discipline behind the envelope method is powerful for one specific reason: it makes overspending impossible. You can’t spend money you don’t have in the envelope. There’s no mental math required, no app to check, no willpower needed. The envelope is empty, so you stop.

Behavioral economics research including work by MIT’s Drazen Prelec and Duncan Simester has documented that people consistently spend less when paying with cash versus cards. The physical act of handing over bills makes the cost feel more real and immediate.

In my experience, the envelope method works best for people who consistently overspend in specific categories despite tracking. If your wants category keeps blowing past your budget no matter what, try going cash-only for just that one bucket. Keep needs and savings as normal digital transactions, but pull out your monthly wants money in cash at the start of each month.

This hybrid approach gives you cash-based discipline for the category that causes trouble while keeping the convenience of digital for everything else.

50/30/20 vs 70/20/10 Rule

The 70/20/10 rule is another percentage-based budgeting strategy. With 70/20/10, you allocate 70% of your income to all living expenses (combining what 50/30/20 separates as needs and wants into one bucket), 20% to savings and investments, and 10% to giving or donations.

The appeal is simplicity. Instead of separating needs from wants within that 70%, you just track everything together. Under budget for the month? Done.

This works well for people who find the needs-versus-wants distinction too stressful or too philosophical. The built-in giving category is another distinguishing feature if charitable giving is an important part of your financial values, 70/20/10 makes that a formal part of your budget framework.

Where 70/20/10 is weaker is in spending discipline. Without separating needs from wants, it’s easy to let lifestyle creep push your living expenses toward 70% even when your needs alone should only be 50%.

Quick-reference comparison:

- Choose 50/30/20 if you want clear separation between obligations and discretionary spending, if you’ve noticed yourself rationalizing lifestyle purchases as necessities, or if you’re building budgeting discipline for the first time.

- Choose 70/20/10 if you already have strong spending awareness, if charitable giving is a financial priority, or if the needs-versus-wants categorization feels too subjective to maintain.

- Choose zero-based budgeting if you want full control over every dollar, if your income changes month to month, or if simpler methods haven’t stopped your overspending.

- Choose the envelope method if you consistently blow a specific category and need a physical spending cap to break the pattern.

All of these budgeting strategies share the same core goal: spend less than you earn, save consistently, and be intentional about where your money goes. The method is just the vehicle. Pick the one that fits how your brain actually works.

Common Mistakes That Kill Your 50/30/20 Budget

Every mistake in this section is one I’ve either made personally or watched others make. None of them are moral failures they’re predictable patterns that derail good intentions, and knowing them in advance gives you a real advantage.

Mistake 1: Using Gross Income Instead of Net Income

This is the most common math error, and it throws off your entire monthly budget before you even start.

Gross income is your salary before taxes, health insurance deductions, and retirement contributions come out. Net income is what actually hits your bank account.

If you earn $60,000 per year, your gross monthly income looks like $5,000. But your actual take-home pay after all deductions might be $3,800 or $3,900. If you base your 50/30/20 split on $5,000, you’re budgeting with money you don’t actually have.

Always calculate your budget categories from your net income. Pull up your most recent pay stub, find the “Net Pay” line, and use that number as your starting point every month, without exception.

Mistake 2: Miscategorizing Wants as Needs

This one is sneaky because it feels completely rational in the moment. Your gym membership feels necessary for health. Your premium phone plan feels necessary for work. Your larger apartment feels necessary for comfort.

When too many wants move into the needs category, you blow past the 50% limit and feel confused about why the budget isn’t balancing.

The distinction between needs and wants isn’t about what feels important. It’s about what you’re genuinely obligated to pay versus what you choose to pay. The accuracy of your entire budget depends on honest categorization here. When in doubt, run the three-question test from the categorization section above.

Mistake 3: Trying to Use the Rule While Carrying Heavy Debt

As noted in the When Needs Exceed 50% section above, average American household debt payments frequently exceed $1,000 per month according to Federal Reserve consumer finance data — a level that can make strict 50/30/20 compliance nearly impossible.

When debt payments are this heavy, forcing yourself to follow the standard split often means underpaying debt to preserve a wants budget which costs you more in interest over time and keeps you in debt longer.

A more practical approach: temporarily treat aggressive debt payoff as your primary financial goal. Keep a minimal emergency fund throughout even just one month of basic expenses so unexpected costs don’t push you deeper into debt. Once your required debt payments drop to a manageable level, the full 50/30/20 structure becomes achievable.

Mistake 4: Not Automating Savings

I made this mistake for two full years. I’d tell myself I would transfer money to savings at the end of the month, after all my spending was done. And then at the end of the month, there was barely anything left.

When savings is manual and happens last, life gets in the way every single time a car repair, a friend’s birthday, a sale that seemed too good to miss.

Automation fixes this completely. Set up an automatic transfer that moves your savings amount to a separate savings account on the same day your paycheck arrives. Then budget and spend from what remains. Automating that transfer moving savings to a separate account the same day my paycheck arrives shifted my savings rate from inconsistent to reliable within the first month.

Mistake 5: Being Too Rigid with Percentages

The 50/30/20 rule is a guideline, not a law. When people treat it as an absolute rule that must be hit exactly every single month, they set themselves up for frustration and eventual abandonment.

Life doesn’t cooperate with perfect percentages. Some months your needs run 54% because your car needed maintenance. Some months your savings drops to 17% because a genuine emergency came up. That’s normal. That’s life.

What matters is the pattern over time. If you average close to 50/30/20 across three to six months, you’re doing excellently.

One rough month is data, not failure. It tells you something specific about where your plan doesn’t match your actual life and that’s useful information. Adjust one thing and move forward.

Mistake 6: Forgetting to Budget for Irregular Expenses

This one derailed my budget repeatedly before I figured out what was happening. Every month felt fine then a quarterly car insurance payment hit. Then a birthday gift I needed to buy. Then an annual subscription renewed.

None of these were genuine surprises — they were entirely predictable events I’d simply failed to plan for because they didn’t happen every single month.

The solution is to think annually, not just monthly. List every predictable irregular expense throughout the year: car registration, insurance renewals, holiday gifts, annual subscriptions, vacation deposits, medical copes. Add them all up and divide by 12. That monthly amount gets added to your budget as a “sinking fund” contribution money you set aside gradually so it’s already available when the annual or quarterly bill arrives. Think of it as pre-paying future expenses in small monthly instalments.

When the expense actually hits, the money is already waiting.

Mistake 7: Not Adjusting as Income Grows

This might be the most expensive mistake on this list, and it’s the least talked about.

When your income goes up which hopefully it does over your career there’s a powerful temptation to upgrade your lifestyle proportionally. Better apartment. Newer car. More dining out. Nicer vacations. All at once. This is lifestyle inflation, and it’s the primary reason people earn significantly more than five years ago but feel no more financially secure.

The 50/30/20 framework gives you the perfect tool to counteract this. When your income rises, your dollar amounts in every category increase automatically but your percentages stay fixed. Your wants budget grows, yes. But so does your savings. Both grow proportionally.

My personal rule whenever I get a raise: before I update a single line item in my wants budget, I increase my automatic savings transfer to reflect the new 20%. The wants category grows automatically from whatever remains. Savings grows first, on purpose.

I’ve seen people with identical salaries end up in completely different financial positions in their 50s. The difference almost always traces back to what they did with raises in their 30s whether they upgraded their lifestyle proportionally or let savings capture the gains first.

Why the 50/30/20 Budget Works Long-Term

We’ve covered a lot of mechanics in this article. But I want to close with the big picture, because that’s what keeps you motivated when the day-to-day feels tedious.

The 50/30/20 budgeting strategy works for two very different reasons. One is mathematical. The other is psychological. Both matter more than most people realize.

The Math: How 20% Savings Builds Wealth

The numbers behind consistent 20% savings are worth sitting with for a moment.

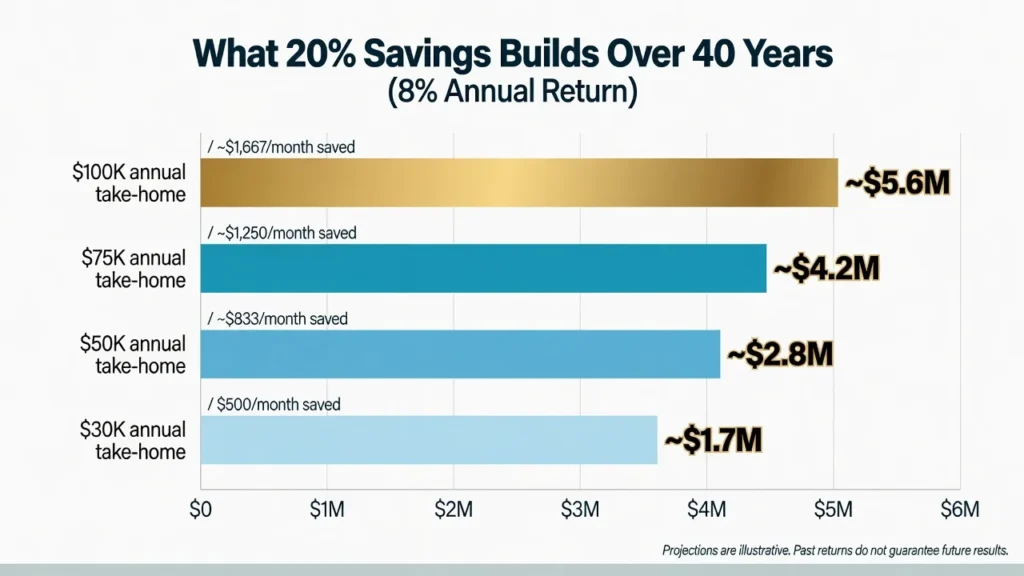

Using a standard compound interest calculation with an 8% average annual return consistent with long-term diversified U.S. stock market index fund performance historically, according to S&P 500 data here’s what consistent 20% savings produces at different income levels over 40 years:

| Annual Take-Home Pay | Monthly Savings (20%) | After 40 Years at 8% |

|---|---|---|

| $30,000 | $500/month | ~$1.7 million |

| $50,000 | ~$833/month | ~$2.8 million |

| $75,000 | $1,250/month | ~$4.2 million |

| $100,000 | ~$1,667/month | ~$5.6 million |

When I first calculated this for my own income, I honestly questioned the math it seemed too optimistic. But compound growth over decades is one of the few forces in personal finance that genuinely earns the word “powerful.”

Important caveat: these projections assume consistent contributions and an 8% average annual return consistent with long-term diversified index fund performance historically, but not guaranteed in any given period. They also don’t account for inflation; the actual purchasing power of $1.7 million in 40 years will be meaningfully lower than it sounds today. The point isn’t the exact figure. It’s the direction: consistent 20% contributions, regardless of income level, produce dramatically better financial outcomes than any amount of income without a savings habit.

One aspect of the 20% category that often gets overlooked: it works for debt payoff just as powerfully as for investment. Every extra dollar you put toward high-interest debt is a guaranteed return equal to that interest rate. Whether your 20% goes to investment accounts or debt repayment, it’s building your financial foundation in a real and measurable way.

The Psychology: Permission to Spend Without Guilt

Something that rarely gets mentioned when people explain the 50/30/20 rule: it’s actually designed to make spending feel good.

Most budgets focus entirely on restriction. Spend less here. Cut this. Give up that. After a few weeks of that mindset, you either rebel and blow the whole budget, or you white-knuckle through it miserably until you give up. Neither outcome builds lasting financial wellness.

The 50/30/20 budget framework is different because it builds in a 30% wants category and then tells you to spend it freely. That’s not a design flaw that’s the whole point.

When you know that $1,200 of your monthly income is legitimately yours to enjoy without guilt, something changes in how you feel about money. You stop making impulsive purchases to feel better. You stop avoiding your bank account because you’re afraid of what you’ll see. You stop counting the days until payday.

I remember what money felt like before I had a system. I bought things impulsively and felt vague guilt about it afterward. I avoided checking my balance because I was afraid of what I would see. After six months on the 50/30/20 budget, that anxiety mostly disappeared not because I had more money, but because I had clarity. I knew my needs were covered. I knew I was saving. And I knew that what I spent on wants was genuinely mine to enjoy.

One of the things I’ve come to believe strongly: people in their 20s and 30s should actually enjoy their income and the experiences it can fund not live in pure austerity accumulating regret about the life they never lived while dutifully saving for a future they can’t predict. There is a version of responsible money management that doesn’t require sacrificing your entire present for a future that is never guaranteed.

The 50/30/20 budget is that version a financial planning framework that balances present enjoyment with future security. Save 20%, cover your obligations with 50%, and spend the remaining 30% on what actually makes your life rich.

Sustainability is the variable that matters most in personal finance. Any budget you maintain for years beats any budget you abandoned after three months. The 50/30/20 rule earns its reputation not because it’s mathematically optimal in every situation, but because it’s sustainable and that’s what makes the math work over time.

Frequently Asked Questions About the 50/30/20 Budget

Should I use gross income or net income?

Always use your net income, which is your actual take-home pay after taxes, health insurance, and pre-tax retirement contributions are deducted. Budgeting with gross income means planning around money you never see in your bank account. Check your pay stub for the net pay line and use that number every month.

What if my needs are more than 50% of my income?

This is more common than you think, especially in high cost-of-living areas. First check that you have not accidentally classified wants as needs. Then look at reducing large fixed costs through options like getting a roommate or refinancing debt. If that is not possible right now, a modified ratio like 60/25/15 or 65/25/10 is perfectly acceptable as a temporary measure. Saving a smaller percentage is far better than saving nothing. The exact percentages are goals, not requirements.

Are minimum debt payments needs or savings?

Minimum payments go in the needs category because they are contractual obligations you cannot skip. The extra amount you choose to pay above the minimum belongs in your 20% savings allocation. For example, if your minimum payment is $100 but you pay $300, the $100 goes in needs and the extra $200 comes from savings. This distinction helps you track your obligations accurately while measuring real progress toward debt freedom.

Can I use this budget if I have significant debt?

You can try, but heavy debt payments often make the standard split very hard to maintain. When debt consumes your wants and savings categories entirely, focus on aggressive debt payoff first while keeping a small emergency fund. Once your payments shrink to a manageable level, the full 50/30/20 framework becomes much more achievable.

What is the best tool to track this budget?

The best tool is the one you will actually use consistently. Budgeting apps like YNAB or EveryDollar connect to your accounts and categorize transactions automatically. A spreadsheet in Excel or Google Sheets gives you flexibility and a full picture in one place. Notion works well if you already use it for organization. A simple pen and paper notebook works perfectly if technology feels like a barrier. Try one method for 30 days before deciding it is not working.

Is the 50/30/20 rule still realistic in 2026?

It depends on your income level and where you live. For people with moderate housing costs and manageable debt, the rule works very well. In expensive cities where rent alone approaches 40 to 50 percent of take-home pay, hitting the exact targets is genuinely difficult. Even a 60/25/15 or 65/25/10 split keeps the core principle intact: cover obligations, enjoy life within limits, and always save something. The principle matters more than the exact percentages.

Should I include my 401k contributions in the 20% savings?

This depends on how you calculate your income. If you use your take-home pay after 401k deductions, your retirement contributions are already funded before your budget begins, so you do not need to count them again in the 20%. If you calculate from your gross salary, include 401k contributions in the 20% savings target. Either method works. Just stay consistent and avoid double counting.

How long before I see real results?

Most people notice immediate clarity in the first month simply from knowing where their money is going. Meaningful results like consistent savings growth and reduced financial anxiety typically appear within three to six months. Significant milestones like a fully funded emergency fund, real debt reduction, or noticeable investment growth usually take one to two years of consistent effort.

The peace of mind from having a clear system shows up much faster than the numbers do. And that mental shift is what keeps you going long enough for the financial results to compound.