How to Pay Off Student Debt Fast: 13 Proven Strategies to Eliminate Your Loans

When I discovered how to pay off student debt fast, everything changed. I’d been staring at my friend Mandi’s $75,000 student loan balance, watching her make $300 minimum payments that would keep her trapped until 2046-30 years of debt slavery. The math was sickening: she’d pay $96,000 extra in interest alone, turning $75,000 into $171,000 total. I knew there had to be a faster way out.

Everything shifted when I realized: understanding that fast student loan repayment isn’t just a dream reserved for six-figure earners. After analysing dozens of real success stories, I discovered people who crushed their debt in shockingly short timeframes. Marissa paid off $87,000 in just 2.5 years. Katie eliminated $27,000 in 14 months on a $40,000 salary. Phil knocked out $30,000 in 12 months.

The difference between decades of debt and a couple years of freedom isn’t income. It’s strategy.

I’ll show you 13 proven student loan repayment strategies combining official financial advice with real success stories.

Some of these methods will feel extreme. Others are simple tweaks that save thousands. You won’t use all 13, but you’ll find the repayment plan combination that fits your situation and helps you achieve financial freedom years faster than you thought possible.

Why Learning How to Pay Off Student Debt Fast Saves You Thousands in Interest

I need to explain loan amortization the concept that completely changed how I approached every single payment. Understanding how your principal balance decreases (or doesn’t) early on is why speed matters more than anything else.

Let me show you exactly where your money goes with a standard $30,000 student loan at 6% interest over a 10-year loan term. Your standard monthly payment would be $333.

In your first year of payments, you’ll pay about $4,000 total. Sounds great, right? The reality hits hard: $1,700 of that $4,000 goes straight to interest. Only $2,300 actually reduces your principal balance.

Now jump to year 10. You’re still paying $333 per month, but something dramatic has changed. Now only about $150 of your annual payments goes to interest. The rest finally attacks your principal balance.

This is called front-loaded interest, and it’s exactly why learning how to pay off student loan debt faster isn’t just about feeling free sooner. It’s about protecting the investment you made in your valuable education by saving thousands that would otherwise go to interest charges on high interest rate loans.

The $333 Payment Breakdown (Where Your Money Actually Goes)

I want you to visualize your very first loan repayment versus your very last payment on that $30,000 loan.

Month 1: Your $333 payment splits roughly $150 to interest and $183 to principal. The interest rate is eating nearly half your payment.

Month 120 (final payment): Your $333 payment splits maybe $2 to interest and $331 toward your principal balance. You’re finally making real progress, but the loan is almost gone anyway.

This front-loading is brutal. In the early years, you’re running on a treadmill, paying hundreds to the bank while your actual debt barely budges.

I remember looking at my own loan statement in month six and feeling confused. I’d paid nearly $2,000, but my balance had only dropped about $1,100. The rest disappeared into interest charges.

Why $1,000 in Extra Payments Today Beats $1,000 Extra in Year 5

This realization made me change my entire approach to early payoff. Every extra dollar you pay toward principal today saves you from paying interest on that dollar for the remaining loan term.

Making a principal prepayment of $1,000 in month one means you won’t pay 6% interest on that $1,000 for the next nine years and 11 months. That’s roughly $600 in interest you just avoided with one payment.

Make that same extra $1,000 payment in year five? You save maybe $300 in interest because there are only five years of compound interest left.

Same $1,000. Half the impact.

This is why I became obsessed with accelerated student loan repayment early in the loan term. The bottom line: early principal prepayment has an outsized effect on your total interest paid.

Before You Start Your Student Loan Repayment Plan: 3 Critical First Steps

I learned this lesson the hard way. You can’t just start throwing money at your student loan balance without proper preparation. I’ve seen people backslide into worse financial situations because they skipped these critical first steps.

Before you attack your debt aggressively, you need a foundation starting with an emergency fund that protects you when unexpected expenses hit.

Build Your $1,000 Safety Net First

I know $1,000 doesn’t sound like much of an emergency fund. You’re absolutely right. It’s not enough for a major crisis.

What I discovered: that small buffer prevents drowning when your car needs a $400 repair or your laptop dies. Without it, you’d put that emergency on a credit card at 22% interest, completely sabotaging your progress in paying off debt.

The $1,000 number comes from people who’ve successfully navigated aggressive debt payoff. It’s intentionally uncomfortable. That discomfort motivates you to get out of debt faster so you can build a proper six-month emergency fund.

I kept my $1,000 in a separate savings account that I didn’t touch unless something was truly urgent. Not “I really want new shoes” urgent. More like “my refrigerator died and food is spoiling” urgent.

Once your debt is gone, you’ll rebuild this into a real emergency fund. For now, this thin cushion protects you while you sprint toward being debt-free.

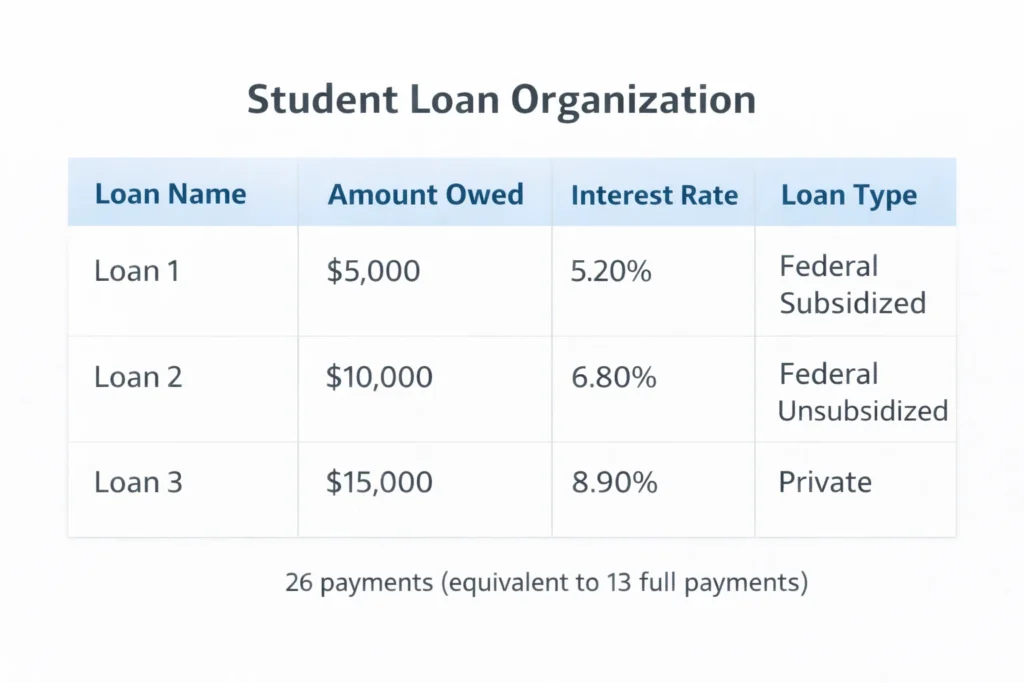

Organize Your Student Loan Balance Like a Pro (The Spreadsheet Method)

This step is absolutely critical. You need to know exactly what you’re fighting.

I created a simple spreadsheet with four columns: Loan Name, Amount Owed, Interest Rate, and Loan Type. This took me about 20 minutes and saved me from costly confusion later.

Here’s what mine looked like:

Loan 1: $8,400 at 6.8% (Unsubsidized)

Loan 2: $5,200 at 4.5% (Subsidized)

Loan 3: $12,100 at 5.3% (Unsubsidized)

Having this visual made everything clear. I could see which loans were costing me the most. I knew my total student loan balance. I understood the battlefield.

Contact your student loan servicer and ask for a complete breakdown if you don’t have this information whether you have federal student loans, private student loans, or both. They’re required to provide it. Log into your account online and you can usually export this data directly.

Update your spreadsheet every month. Watch those numbers drop. I found this incredibly motivating.

Know Your Loan Types: Federal Student Loans vs. Private Student Loans

This matters more than you think because different loan types deserve different repayment strategies.

Federal student loans come from the Department of Education. These have fixed interest rates and qualify for income-driven repayment plans and potential loan forgiveness programs. Most people with student debt have these.

Private student loans come from banks or other lenders. They typically have fewer protections and different repayment rules. You might have these if federal loans didn’t cover your full costs.

Within federal loans, you have subsidized and unsubsidized. Subsidized loans don’t accrue interest while you’re in school or during your grace period. Unsubsidized loans start accumulating compound interest the day you receive them—often at higher interest rates than subsidized loans.

I prioritized my unsubsidized loans because they’d been racking up compound interest since my freshman year. My subsidized loans had lower effective costs because of the years without interest charges.

Check your loan documentation or ask your student loan servicer if you’re not sure which types you have. This classification will guide several repayment plan decisions coming up.

The 2 Core Student Loan Repayment Strategies (Snowball vs. Avalanche)

I spent weeks researching student loan repayment strategies before I understood that among all the repayment options available, everything basically comes down to two proven methods: the debt snowball method and the debt avalanche method. Every expert, every success story, every financial advisor recommends one of these two approaches.

Both methods work. The real question is which one matches your personality and keeps you motivated.

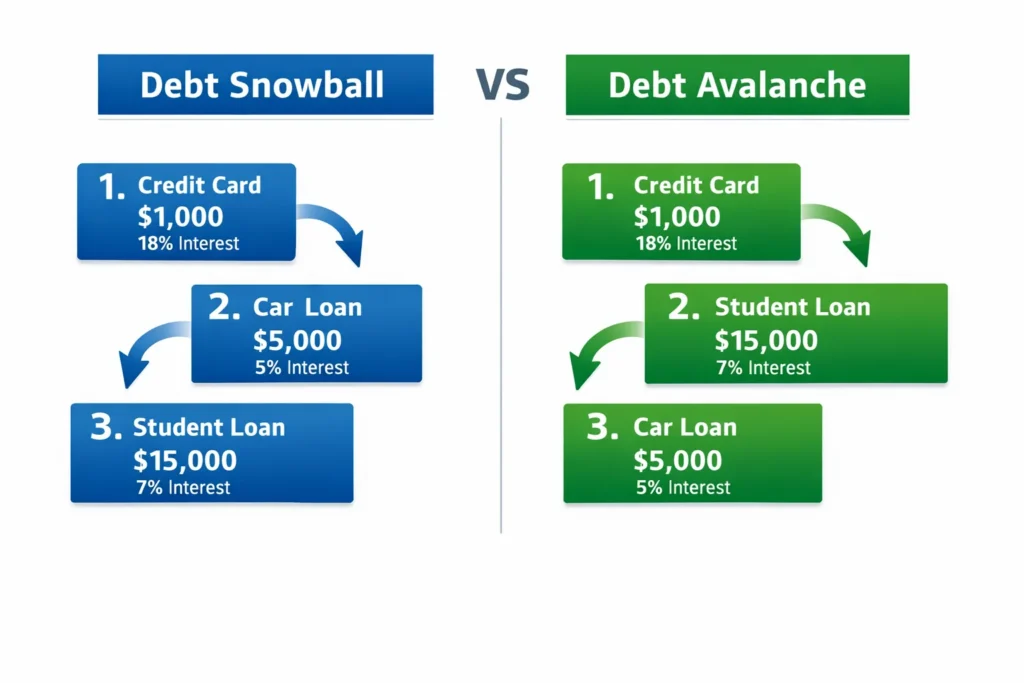

Debt Snowball: Smallest Balance First (The Motivation Method)

The debt snowball method tells you to ignore interest rates completely and focus on one thing: pay off your smallest student loan balance first.

Here’s how I would apply this to my example loans:

Step 1: Attack the $5,200 loan with every extra dollar while making minimum payments on the others.

Step 2: Once that’s gone, attack the $8,400 loan.

Step 3: Finally pay off the $12,100 loan completely.

The logic here isn’t mathematical. It’s psychological.

When I paid off that first small loan in just a few months, something shifted in my brain. I actually called the servicer to confirm the balance was zero because I couldn’t believe it. That rush of accomplishment was addictive.

Suddenly paying off debt wasn’t this abstract decade-long slog. It was a series of concrete victories. I’d eliminated one loan completely. The number of loans I owed dropped from three to two. That felt incredible.

The debt snowball method builds momentum. Each payoff makes the next one faster because you roll that eliminated monthly payment into your next target. Your payment snowball gets bigger as it rolls.

This approach costs you more in total interest paid compared to the avalanche method. But I’ve seen people stick with snowball who would have given up on avalanche. Motivation matters.

If you need wins to stay focused, use snowball.

Debt Avalanche: Highest Interest First (The Math Method)

The debt avalanche method is ruthlessly logical. You rank your loans by interest rate and attack the highest rate first, regardless of balance size.

Using my example loans, the order would be:

Step 1: Attack the $8,400 loan at 6.8% interest.

Step 2: Attack the $12,100 loan at 5.3% interest.

Step 3: Finally pay off the $5,200 loan at 4.5% interest your lowest interest rate loan.

Mathematically, this approach makes the most sense. You’re eliminating your most expensive debt first, which minimizes your total interest paid over your entire loan term.

I calculated my own scenario both ways. The avalanche method would have saved me about $640 in interest compared to snowball. That’s real money.

What I discovered, though: that first loan payoff took me seven months instead of three. Seven months of grinding with no victory. Just watching balances slowly decrease on a spreadsheet.

Some people have the discipline for this. They’re motivated by efficiency and spreadsheets showing optimized interest savings. If that’s you, avalanche is your method.

I’ve seen engineers and accountants thrive with avalanche. I’ve seen teachers and artists thrive with snowball. Neither is wrong.

Which Method Should You Use? (The Decision Tree)

I’m going to make this simple.

Use the debt snowball method if you struggle with motivation, need quick wins to stay committed, have similar interest rates across your loans, or have ever started and quit a student loan repayment plan before.

Use the debt avalanche method if you’re self-motivated by math and optimization, have significantly different interest rates where the highest is 2%+ above the others, can stick to a repayment plan even without early victories, or want to save the absolute maximum on interest.

My honest recommendation: if you’re not sure, start with snowball. The best repayment plan is the one you’ll actually complete. I’ve watched people save $600 in interest with avalanche but give up after a year. I’ve watched people pay an extra $600 in interest with snowball but pay off their student loans completely in two years.

You can even create a hybrid. Pay off your smallest loan first for that motivational win, then switch to avalanche for the rest. There’s no debt payoff police enforcing rules.

7 Payment Tactics That Accelerate Your Student Loan Payoff

Once you’ve chosen your overall strategy, these tactical payment methods amplify your results for early payoff. I use several of these together for accelerated repayment, and each one shaves months off your loan term.

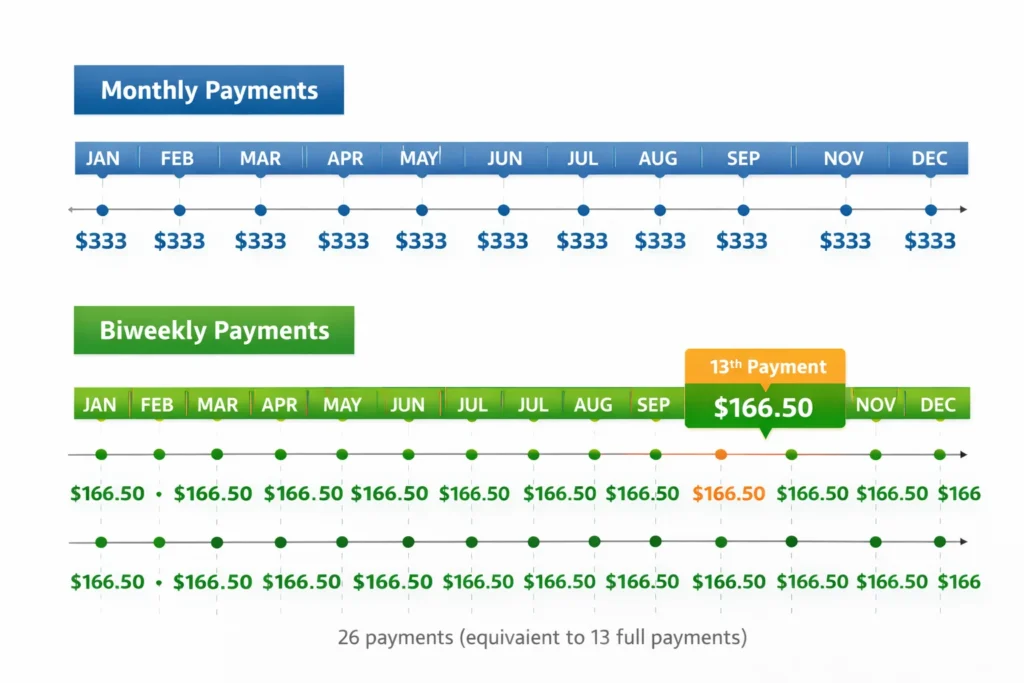

Switch to Biweekly Payments (Get 13 Payments Per Year)

This strategy is my favorite because it’s nearly invisible but incredibly effective.

Instead of making your full monthly payment once per month, you pay half of your standard monthly payment every two weeks.

Here’s the magic: there are 52 weeks in a year. Paying every two weeks means you make 26 half-payments, which equals 13 full payments instead of 12.

You just made an extra full payment without really noticing it because you’re aligning payments with your biweekly paychecks anyway.

On a $30,000 student loan at 6% interest rate, this single change cuts about 18 months off your loan term and saves roughly $1,400 in interest I calculated this using the Department of Education’s loan payment calculator to verify the math.

I set this up by contacting my student loan servicer and asking if they offered a biweekly payment option. Some do it automatically. Others required me to set up the schedule manually through my bank’s bill pay system.

One warning: make absolutely sure your servicer processes biweekly payments correctly. Some will hold your first half-payment and not apply it until they receive the second half, which eliminates the benefit. Ask them explicitly how they handle biweekly schedules before you set this up.

The Autopay Interest Rate Discount Most People Miss

I kicked myself when I realized I’d been leaving free money on the table for eight months.

Most federal student loans and many private student loans offer a 0.25% interest rate reduction just for enrolling in autopay this is confirmed by the Federal Student Aid website and most major loan servicers.

That sounds tiny. It is tiny. But I’ll take free.

On a $30,000 loan, that 0.25% discount saves you about $200 over a standard 10-year term. If you’re paying it off faster, the savings are smaller but still free.

The bigger benefit for me was behavioral. Autopay removed the monthly decision of whether to make my monthly payment. The money left my account automatically the day after payday, before I could spend it on something else.

I set up autopay through my student loan servicer to withdraw my minimum payment automatically, then I made additional manual principal prepayments whenever I had extra money. This gave me the discount and the consistency while maintaining flexibility for extra payments.

Check with your loan servicer about their autopay discount. It takes about five minutes to enroll.

Pay Immediately After Payday (The “Out of Sight” Method)

This sounds almost silly, but it completely changed my relationship with money.

I moved my student loan payment date to the day after my payday.

Before this, I got paid on the 15th and my student loan payment was due on the 5th of the next month. That meant my paycheck sat in my account for three weeks before my monthly payment. Three weeks to look at that money and think of creative ways to spend it.

After I changed my payment date, the sequence became: paycheck deposits Friday, loan payment withdraws Saturday. The money barely touched my account.

One person online called this the ‘pay your student loans before you can be stupid with the money’ method. I laughed, but they were absolutely right.

When my student loan payment disappeared immediately, I budgeted the rest of the month with what remained. I didn’t miss money I never really had.

This psychological trick helped me increase my monthly payment from $380 to $520 without feeling like I was sacrificing anything. That extra $140 went to loans automatically before I could spend it on restaurant meals and random purchases.

Not every student loan servicer lets you choose your payment date, but many do. Call and ask. The worst they can say is no.

How to Apply Bonuses and Windfalls

I made a rule for myself that changed my student loan payoff timeline by over a year: every dollar I didn’t earn through my regular paycheck went directly to my principal balance for early payoff.

Tax refund? Straight to loans.

Work bonus? Straight to loans.

Birthday money from grandparents? Straight to loans.

Sold old furniture? Straight to loans.

These windfalls feel like ‘free money’ psychologically, which makes them incredibly easy to waste on things other than student loan payments. I’d convince myself I ‘deserved’ to spend my tax refund on a vacation because I worked hard all year.

The reality hit me: my regular paycheck already covered my regular life. These windfalls were opportunities to make massive principal prepayments that would save me years of compound interest.

I tracked this for one year. Between a $1,800 tax refund, a $1,200 work bonus, $300 in birthday money, and about $500 from selling things I didn’t need, I put an extra $3,800 toward my student loans that year.

That single year of windfalls eliminated almost eight months from my loan term.

I’m not saying you can never enjoy a bonus. But while you’re in aggressive debt payoff mode, these lump sums are your secret weapon for making progress that would take years through monthly payments alone.

Round Up Every Payment

This tiny tactic requires almost zero sacrifice but compounds beautifully over time—similar to how compound interest works against you.

Whatever your student loan monthly payment is, round it up to the next $50 or $100.

If your payment is $267, make it $300.

If your payment is $412, make it $450 or $500.

I rounded my $267 student loan payment to $300, which meant an extra $33 per month or $396 per year. Over three years, that was an extra $1,188 in principal prepayment that I barely noticed.

The beauty of rounding is that it’s automatic. Once you set it up, you don’t make a decision every month. You just pay the round number.

I combined this with the “pay immediately after payday” method, and together they created a system that required no willpower or monthly motivation. It just happened.

Throw All Raises at Your Student Loans

When I got a $3,000 annual raise, I made what felt like a painful decision. I pretended the raise never happened and redirected that entire amount to my student loans.

My logic was simple: I’d been surviving on my previous salary. I wasn’t struggling. A raise was lifestyle inflation waiting to happen, not a necessity.

That $3,000 annual raise became $250 per month in extra payments. Combined with my existing $300 payment, I was suddenly paying $550 per month on a loan that required only a $267 minimum payment.

This single decision cut my remaining loan term from 68 months to 34 months. I cut my time in debt in half by living like I hadn’t gotten a raise.

I’m not suggesting you do this with every raise forever. But while you’re in debt elimination mode, raises are rocket fuel for your payoff timeline.

Once I was debt-free, my next raise went straight into my pocket for enjoyment and savings. But during my debt sprint, raises went to buying my freedom.

Use Cash-Back Rewards for Student Loan Payments

This is a small tactic, but I’m including it because every bit helps and it’s completely passive.

I put all my regular expenses on a 2% cash-back credit card, paid the balance in full every month to avoid high interest rate charges, and once per quarter applied the accumulated cash back to my student loan principal balance.

Over three years, this generated about $900 in extra principal payments. That’s not life-changing, but it’s $900 I didn’t have to earn separately.

The key rules for this to work: you must pay your credit card in full every month, you must not spend more just to earn rewards, and you must actually apply the cash back to your loans instead of spending it.

If you have any tendency to carry credit card balances, skip this tactic entirely. Credit card interest at 18-25% destroys any benefit from 2% cash back.

But if you’re disciplined with credit cards, this is free extra payment money generated by spending you were already doing.

Make Sure Extra Payments Actually Reduce Your Debt (The Payment Allocation Trap)

I need to warn you about something that makes me genuinely angry. This is a trap that costs borrowers thousands of dollars, and I almost fell into it myself.

When you make an extra payment above your minimum, your student loan servicer will ask you a seemingly helpful question: “Would you like us to advance your due date?”

This sounds great. It sounds like you’re getting ahead. You’re prepaying future months so you could even skip a payment later if you needed to, right?

Wrong. This is a trap.

When your servicer “advances your due date,” your extra payment doesn’t reduce your principal balance immediately. Instead, it’s being held to cover future minimum payments. Your loan balance stays high, which means you keep paying interest on money you’ve already sent them.

I discovered this when I made an extra $500 payment and checked my balance a week later. My principal had only dropped by about $320. Where did the other $180 go? It was being held to cover future interest charges.

The Deceptive Servicer Question (And How to Answer It)

Here’s the exact situation you’ll face. You make an extra payment. Your servicer’s website or representative will ask something like:

“How would you like to apply this payment?”

“Would you like to advance your next due date?”

“Should we apply this to next month’s payment?”

The correct answer is: “Apply this payment to principal only. Do not advance my due date. I want my next payment to remain on the regular schedule.”

You have to be explicit about principal prepayment. Many servicers have this buried in their payment interface as a checkbox or dropdown menu that defaults to the wrong option.

I now log into my servicer’s website, navigate to “Make a Payment,” enter the extra amount, then specifically select “Apply to principal only” before submitting. Then I verify.

Some servicers make you call them for extra payments to ensure proper application. Yes, this is inconvenient. Yes, they know it’s inconvenient. Do it anyway.

How to Verify Your Extra Payment Worked

Making the payment correctly is step one. Verification is step two.

I check my account three to five days after making an extra payment. I look at two specific numbers:

First, my principal balance. It should have decreased by the full amount of my extra payment, not just a portion.

Second, my next due date. It should not have changed. If I was due to make my next payment on June 15th before my extra payment, I should still be due on June 15th after my extra payment.

If my due date has moved to July 15th, my payment was misapplied. I call immediately and say: “I made a principal prepayment on [date] for [amount]. This was incorrectly applied to advance my due date. I need this corrected to apply to principal only.”

I’ve had to make this call twice. Both times the servicer acted like this was an unusual request, which told me most borrowers never notice or never complain.

Keep records of your extra payments. Screenshot your payment confirmations. This protects you if there’s ever a dispute about how payments were applied.

This might sound paranoid, but I’ve read too many stories of people making aggressive extra payments for years only to discover their servicer misapplied everything and their balance barely moved.

When Refinancing Makes Sense (And When It Doesn’t)

Student loan refinancing is one of those topics where I’ve seen people make both brilliant decisions and catastrophic mistakes. The difference comes down to understanding exactly what you’re trading.

Refinancing means taking out a new loan from a private lender to pay off your existing student loans. You’re hoping to get a lower interest rate, which reduces your total interest paid and potentially your monthly payment.

This can save you thousands. It can also cost you tens of thousands if you do it wrong.

The 3 Refinancing Rules (Don’t Break These)

I learned these rules from people who’d been through the refinancing process multiple times, and they’ve saved me from expensive mistakes.

Rule 1: Only refinance once. Every time you refinance, you pay fees and go through credit checks. More importantly, rates don’t continuously drop forever. Pick your best opportunity and execute once.

Rule 2: Only accept a fixed interest rate. Variable rates might start lower, but they can increase dramatically. I’ve seen variable student loan rates jump from 4% to 8% in two years, destroying people’s budgets. Fixed rates give you certainty.

Rule 3: Only refinance if your new rate is meaningfully lower. I set my personal threshold at 1.5 percentage points minimum. Refinancing from 6% to 5.7% isn’t worth the effort and risk. Refinancing from 6% to 4% absolutely is.

If you can’t meet all three rules, don’t refinance.

Should You Refinance Federal Loans? (The Risk Analysis)

This is where refinancing gets dangerous, and I need you to pay careful attention.

When you refinance federal student loans with a private lender, those loans stop being federal. They become private loans. You cannot undo this.

Here’s what you lose:

You lose access to federal repayment options like income-driven repayment plans that can lower your payment if you lose your job or take a pay cut.

You lose Public Service Loan Forgiveness eligibility if you work for a nonprofit or government employer.

You lose deferment and forbearance options that let you pause payments during hardship without defaulting.

You lose any chance of future loan forgiveness programs that Congress might pass.

These protections have real value. During economic uncertainty, they’ve saved people from default and bankruptcy.

So when does refinancing federal loans make sense? Only when all of these are true:

You have a stable, high income that you’re confident will continue.

You don’t work in public service and never plan to.

You’re committed to aggressive payoff in 2-4 years maximum.

You can get at least 2% lower rate.

You have an emergency fund to cover payments if something goes wrong.

I chose not to refinance my federal loans because I valued the safety net more than saving maybe $800 in interest. Someone else in a different situation might make the opposite choice and be completely correct.

Best Candidates for Refinancing

Private student loans are much safer to refinance because they don’t come with federal protections anyway. You’re not losing anything except possibly a relationship with your current lender.

The ideal refinancing candidate looks like this:

You have private student loans or you’ve already decided federal protections don’t matter for your situation.

Your interest rate is above 6%.

Your credit score has improved significantly since you first took out the loans.

Your income is stable and sufficient to make payments even if rates were slightly higher.

You’re planning to pay off the debt in 5 years or less anyway.

I’ve seen people with 8-9% private student loans refinance down to 4-5% fixed rates. That’s life-changing savings, sometimes $15,000 or more over the loan term.

Companies like SoFi, Earnest, and Laurel Road specialize in student loan refinancing. I’d get quotes from at least three lenders to compare. They’ll do soft credit pulls for quotes that don’t affect your credit score.

One person I know refinanced $65,000 from 7.2% down to 4.1% and saved over $11,000 in interest while cutting two years off their payoff timeline. That’s a good refinance.

Another person refinanced federal loans at 5.5% down to 4.8%, lost all federal protections, then lost their job eight months later and had no forbearance options. That’s a bad refinance.

The decision is entirely about your specific situation and risk tolerance.

Live Like a Broke Student (Even With a Full-Time Job)

This is the section that separates people who dream about being debt-free from people who actually get there. I’m not going to sugarcoat this. What I’m about to describe is uncomfortable and requires sacrifice.

But it works faster than any other strategy.

The principle is simple: just because you graduated and got a job doesn’t mean you need to upgrade your lifestyle. Live on the same budget you had as a student, and send every dollar of the difference to your loans. I’ll show you specific ways to implement this through strategies for reducing your monthly expenses, which can cut your timeline by years.

The $1,450 Apartment That Killed Rachel’s Progress

I listened to a call-in show where a woman named Rachel was trying to figure out why her loan payoff had stalled. She’d been making $1,000 monthly payments on her $38,000 balance, which would have eliminated her debt in about four years.

Then she moved into a new apartment. The rent was $1,450 per month, up from her previous $750 rent. That extra $700 in monthly rent forced her to drop her loan payment from $1,000 back down to barely above the minimum.

Her projected payoff timeline went from four years to eleven years because of one housing decision.

That extra $700 per month over seven years is $58,800. Her loan balance was only $38,000.

I’m not saying you need to live in a terrible apartment. But I watched this happen over and over. People graduate, get a job, and immediately rent a nice place because they feel like they’ve earned it. That decision alone destroys their ability to attack their student loan balance.

If keeping your housing cost low means staying in that mediocre apartment for two more years, you’re buying yourself a decade of freedom by giving up 24 months of upgraded space.

Should You Move Back Home? (The 12-18 Month Strategy)

I know this suggestion makes some people cringe. Moving back in with parents or family after graduation feels like failure.

But I studied someone named Phil who graduated with $30,000 in debt. He moved into his father’s basement and paid $500 per month in rent and expenses. His take-home pay was about $3,000 per month.

That left $2,500 per month for debt payoff. He eliminated his entire $30,000 balance in 12 months.

If he’d rented his own apartment for $1,200 per month plus utilities and living expenses, he’d have maybe $800 per month for loan payments. That same $30,000 would have taken over four years.

Phil traded 12 uncomfortable months for three years of freedom.

I’m not saying everyone should move home. But if you have that option and the relationship is healthy, the math is overwhelming. Living rent-free or low-rent for 12-18 months can eliminate debt that would otherwise follow you for a decade.

You’re not moving home forever. You’re executing a strategic financial sprint.

The $40k Salary Budget That Paid Off $27k in 14 Months

Katie called into a financial advice show with $27,000 in student debt and a $40,000 salary. She was told to do something that sounded impossible: live on $1,500 per month and put $2,000 per month toward her loans.

Her take-home pay after taxes was about $2,700 per month. The budget forced her to live like she was still in college, sharing a cheap apartment with roommates, cooking every meal, spending nothing on entertainment that cost money.

Fourteen months later, she was completely debt-free at age 24.

Here’s what made this possible. She kept her housing cost at $500 per month with two roommates. She spent $300 per month on groceries by meal planning and never eating out. She drove a paid-off car that she’d had since high school, so her only car expense was insurance and gas.

Everything else was stripped to bone. No cable. No subscriptions. No shopping. No bars or restaurants. No vacations.

For 14 months.

Then she was done. At 24 years old with no debt, she could start building wealth while her friends were still making minimum payments that would last until they were 40.

I’m showing you this extreme example because it proves what’s possible. You might not be willing to go this hardcore, and that’s fine. But even implementing a lighter version of this, living on 60% of your income instead of 90%, will dramatically accelerate your timeline.

The question I had to ask myself was: would I rather live like a broke student for 18 months or live like a debt-burdened employee for 10 years?

3 Ways to Increase Your Income for Faster Payoff

I’ve talked a lot about cutting expenses, but there’s a limit to how much you can cut. You can’t reduce your rent below zero or stop eating.

Income has no ceiling.

Every extra dollar you earn can go straight to principal prepayment because your existing income already covers your expenses. This is how people with average salaries pay off massive balances in shockingly short timeframes.

Side Hustles That Paid Off $102k in Debt

Mandi graduated with $75,000 in student loans, then continued graduate school and ended up with $102,000 total student debt. Her full-time job paid decently, but not well enough to eliminate six figures of debt quickly.

So she added side income. Dog walking. Cat sitting. Babysitting. Freelance writing.

None of these were glamorous. Many required working evenings and weekends when she was already tired from her day job. But every side hustle dollar went directly to her highest-interest loans.

She didn’t track exact numbers, but estimated her side income added about $800-1,200 per month depending on the season. Over five years, that was roughly $50,000-70,000 in extra debt payments she wouldn’t have made otherwise.

The beautiful thing about side income for debt payoff is you don’t need to sustain it forever. This isn’t about building a side business empire. It’s about a temporary income boost during your debt elimination sprint.

I picked up freelance work in my field for about eight months. I hated it. I was tired all the time. But I made an extra $6,500 that went straight to my loans, shaving seven months off my payoff date.

Then I quit the side work once my main debt was manageable. The temporary sacrifice created permanent results.

The 6-Month Overtime Push That Eliminated $18k

I read about someone online who worked overtime at their job for six straight months. Five to six days every single week, 50-55 hours instead of 40.

They were exhausted. They had no social life. But they earned an extra $18,000 in six months and completely eliminated their remaining student loan balance.

Then they went back to normal work hours with zero debt instead of years of payments still ahead.

This strategy obviously requires a job that pays overtime or has extra shift opportunities. Not everyone has this option. But if you do, a focused overtime push is one of the fastest ways to generate large extra payments.

I talked to a nurse who picked up extra shifts for four months and paid off $12,000. A retail manager who worked every holiday and weekend for one year and eliminated $15,000.

These aren’t pleasant stories. They’re effective stories.

The key is setting a specific timeline. “I will work extra for six months” is sustainable. “I will work extra until the debt is gone” with no end date burns people out and they quit.

Does Your Employer Offer Student Loan Assistance?

This is free money that many people don’t even know exists.

Some employers now offer student loan repayment assistance as a benefit. They’ll contribute $100-200 per month directly toward your student loans, similar to how they might match retirement contributions.

I checked with my HR department and discovered my company offered $100 per month in student loan assistance after one year of employment. I had been there 14 months and had no idea this existed.

That’s $1,200 per year I was leaving on the table.

The programs are becoming more common, especially in competitive industries trying to attract young talent. Tech companies, hospitals, law firms, and even some government agencies offer this.

Check your employee handbook or ask HR directly. If your company offers this benefit, enroll immediately. If they don’t, it might be worth asking if they’d consider adding it, especially if competitors offer it.

Even $50-100 per month from your employer is $600-1,200 per year in free principal prepayment. That’s not enough to eliminate your debt alone, but combined with your other strategies it’s meaningful acceleration.

Advanced Strategy: Velocity Banking for Student Loans

I’m going to share something that most people have never heard of, but for certain situations it can dramatically speed up debt elimination. This is an advanced method that requires financial discipline, so pay careful attention to whether this fits your situation.

Velocity banking uses a line of credit to pay down your student loan debt faster by leveraging cash flow rather than just monthly payment amounts.

How Velocity Banking Works (The 9-Month Example)

Let me walk through a real example I studied.

Someone had a $10,743 student loan balance. They opened a line of credit with a lower interest rate than their student loan. Then they executed this system:

Month 1: Deposited entire monthly income of $8,536 into the line of credit, immediately reducing the balance by that amount. Then withdrew $7,494 for monthly living expenses. This left $1,042 reducing the LOC balance.

They repeated this every month, depositing all income into the line of credit and only withdrawing what they needed for expenses.

After just 3 months, they’d paid off $10,743 using this method. Then they moved additional student loan debt into the line of credit and continued the process.

The key is that your income sits in the line of credit reducing the balance and accruing less interest than it would on your student loan, while you only withdraw money as you actually spend it rather than all at once.

This works because interest on lines of credit is calculated daily based on your average daily balance. By keeping your income deposited as long as possible before withdrawing for expenses, you minimize interest charges.

Over nine months, this person eliminated significantly more debt than they could have with traditional monthly payments, even though their income and expenses didn’t change.

Who Should (and Shouldn’t) Use This Method

Velocity banking is not for beginners or people who struggle with money management.

This method works if you have access to a line of credit with a lower interest rate than your student loans, you have stable and predictable income, you have a detailed budget and track every expense, and you have the discipline not to overspend just because credit is available.

This method does not work if you tend to overspend, you don’t have a clear budget, you can’t get a line of credit with a lower rate than your student loans, or your income is irregular or unpredictable.

The risk is obvious: if you lose discipline and start spending more because you have access to a line of credit, you’ll end up in worse debt than when you started.

I’m including this strategy because for the right person in the right situation, it’s incredibly powerful. But I’d estimate only about 20% of people have the financial discipline to execute this successfully.

If you’re not sure whether you have that discipline, you probably don’t. Stick with the conventional methods.

When You Should NOT Pay Off Student Debt Fast

This might seem contradictory in an article about fast payoff, but I need to be honest with you about situations where aggressive student loan repayment is actually the wrong financial move.

Not everyone should be sprinting to pay off their debt. Sometimes the slow path is smarter.

If You Qualify for PSLF, Pay the Minimum (Not Extra)

Public Service Loan Forgiveness (PSLF) is a program where federal student loans are completely forgiven after you make 120 qualifying monthly payments while working full-time for a qualifying employer.

Qualifying employers include government organizations at any level and 501(c)(3) nonprofit organizations.

If you’re a teacher, nurse, social worker, public defender, nonprofit employee, or government worker, you might qualify.

Here’s the critical part: PSLF forgives your remaining balance after 10 years of payments. Every extra dollar you pay beyond the minimum is a dollar you’re throwing away because it would have been forgiven anyway.

I talked to someone who paid an extra $15,000 toward their loans before they realized they qualified for PSLF. That $15,000 bought them nothing because their remaining balance was forgiven anyway.

If you qualify for PSLF, you should be on an income-driven repayment plan that minimizes your monthly payment, pay exactly the minimum for 10 years, and let the government forgive whatever remains.

This is the opposite of everything else in this article, but it’s the mathematically correct move for PSLF-eligible borrowers.

Verify your eligibility through the Department of Education’s PSLF Help Tool and submit employment certification forms annually to make sure you’re on track.

Don’t Skip Your 401k Match to Pay Debt

Some employers match your retirement contributions. If you contribute 5% of your salary, they’ll contribute another 3-5% on top.

That match is free money and an immediate 100% return on investment.

If you stop contributing to get the match so you can put that money toward debt instead, you’re making a mistake. You’re turning down free money that also grows tax-free for decades.

I maintain that you should contribute enough to get the full employer match, then put any additional money toward debt payoff. Don’t leave free retirement money on the table.

After your debt is eliminated, you can increase retirement contributions. But while you’re paying off loans, get the match and nothing more.

When Income-Driven Repayment Makes More Sense

Income-driven repayment plans calculate your monthly payment based on your income and family size rather than your loan balance.

If your income is low relative to your debt, IDR plans can reduce your monthly payment to $0-50 per month. After 20-25 years of payments, any remaining balance is forgiven.

Let’s say you have $100,000 in student debt but work in a low-paying field earning $35,000 per year. An income-driven repayment plan might set your payment at $150 per month based on your income.

At $150 per month, you’d pay only $36,000 over 20 years before the remaining $64,000 plus accumulated interest is forgiven.

Trying to aggressively pay off $100,000 on a $35,000 salary would devastate your quality of life for a decade or more.

In this scenario, IDR with eventual forgiveness is smarter than aggressive payoff.

The tax situation is worth noting: forgiven amounts under IDR are currently treated as taxable income, though this rule keeps changing. Still, paying taxes on $64,000 of forgiven debt is better than actually paying $64,000 of debt.

This strategy works best for people with high debt relative to income who don’t expect major salary increases and aren’t pursuing PSLF.

5 Costly Mistakes That Slow Down Your Payoff

I’ve made several of these mistakes myself. I’ve watched friends make all of them. Each one added months or years to debt payoff timelines.

Mistake #1: Letting Your Rent Eat Your Debt Payments

I mentioned Rachel earlier who upgraded her apartment and killed her debt progress. This deserves emphasis as mistake number one because it’s incredibly common.

Housing is your biggest expense. If that expense consumes too much of your income, you have nothing left for aggressive debt payoff.

The general rule I follow: housing should be no more than 25-30% of your take-home pay while you’re in debt elimination mode. If you’re paying 40-50%, you’re going to struggle.

I kept my rent at $625 per month when I could have afforded $1,000. That extra $375 per month went to loans. Over two years, that was $9,000 in extra principal prepayment.

Those two years in a mediocre apartment bought me eight years of freedom from debt payments.

Mistake #2: The Payment Allocation Trap (Covered Earlier)

I covered this in detail earlier, but it bears repeating in a mistakes section.

If you make extra payments without explicitly directing them to principal, your servicer will likely misapply them in a way that doesn’t reduce your balance as much as it should.

Always specify principal-only application. Always verify the payment reduced your principal balance by the full amount.

This mistake alone has cost people thousands of dollars in unnecessary interest.

Mistake #3: Lifestyle Inflation Right After Graduation

You graduate, get your first real job, and suddenly you have more money than you’ve ever had. The temptation to upgrade everything is overwhelming.

New car. New furniture. New wardrobe. Nicer apartment. Restaurants instead of cooking. Subscriptions to everything.

Within six months, your new higher income is completely absorbed by your new higher expenses, and you’re still making minimum payments on your student loans.

I watched a friend get a $55,000 job after graduation. Within four months, he’d bought a new car with a $420 monthly payment and moved into a $1,300 apartment. His student loan payment stayed at $280 per month because he had no money left.

If he’d kept driving his old car and stayed in a cheaper apartment for two years, he could have been debt-free. Instead he’s still making payments seven years later.

Delay lifestyle inflation until after you’re debt-free. The time to upgrade your life is when you have no debt payments competing for your income.

Mistake #4: Using Forbearance When You Don’t Need It

Deferment and forbearance let you temporarily pause student loan payments during financial hardship.

These programs exist for real emergencies: job loss, medical crisis, genuine inability to pay.

What they’re not for: “I’d rather spend my money on other things this month.”

During forbearance on most loans, interest continues accumulating. When forbearance ends, that accumulated interest capitalizes, meaning it’s added to your principal balance and you start paying interest on the interest.

I’ve seen people use forbearance casually, treating it like a payment vacation. They pause payments for six months, interest piles up, and when payments resume their balance is higher than when they paused.

One person paused payments on $42,000 in loans for one year at 6% interest. That’s $2,520 in interest that capitalized, increasing their principal to $44,520. They now pay interest on that higher amount for the remaining loan term.

Use forbearance only for real emergencies. If you can possibly make your payment, make it.

Mistake #5: When Your Minimum Doesn’t Cover Interest

This is a nightmare scenario that happens more often than it should.

If you’re on an income-driven repayment plan with a very low payment, it’s possible your monthly payment is less than the monthly interest that’s accruing.

Example: Your loans accrue $200 in interest per month, but your income-driven payment is only $150.

Every month, you pay $150, but your balance increases by $50 because the unpaid interest gets added to principal.

You’re making payments and going backward.

I read about someone who made payments for two years and their balance increased from $65,000 to $71,000.

If you’re in this situation, you have three options: increase your payment above the interest accrual amount if possible, pursue loan forgiveness through PSLF or IDR programs where this is expected, or accept that you’re pursuing forgiveness and the growing balance will be forgiven anyway.

What you can’t do is ignore it and hope it gets better. It won’t.

Check your loan statements to see how much interest accrues monthly. Make sure your payment exceeds that amount unless you’re specifically pursuing a forgiveness strategy.

How Fast Can You Really Pay Off Your Debt? (Set Your Realistic Timeline)

I’ve shown you strategies and mistakes, success stories and warnings. Now let’s talk about what’s actually realistic for your specific situation.

The Simple Payoff Formula

The basic math is straightforward: your total student loan balance divided by months equals your required monthly payment.

Want to pay off $30,000 in two years? That’s $30,000 ÷ 24 months = $1,250 per month.

Want to pay off $60,000 in three years? That’s $60,000 ÷ 36 months = $1,667 per month.

This is simplified because it doesn’t account for interest, but it gives you a starting framework.

A student loan payoff calculator will give you the exact number including interest charges. You’ll find your actual required payment is slightly higher than the simple division because you’re also covering interest that accrues during repayment.

Real Payoff Timelines by Income Level

I’ve studied dozens of real payoff stories, and patterns emerge based on income levels and intensity.

On a $40,000 salary with take-home around $2,700 per month:

If you live extremely frugally and pay $1,500-2,000 per month, you can eliminate $27,000-35,000 in 12-18 months.

On a $60,000 salary with take-home around $3,800 per month:

If you maintain student-level expenses and pay $2,000-2,500 per month, you can eliminate $45,000-55,000 in 18-24 months.

On an $80,000+ salary with take-home around $5,000 per month:

If you avoid lifestyle inflation and pay $3,000-3,500 per month, you can eliminate $70,000-85,000 in 24-30 months.

These timelines assume aggressive commitment. More moderate approaches take proportionally longer.

Phil paid off $30,000 in 12 months on roughly $36,000 income by living in a basement for $500 per month.

Katie paid off $27,000 in 14 months on $40,000 income by living on $1,500 per month.

Marissa and her partner paid off $87,000 in 2.5 years by dedicating about 50% of their combined income.

One person on Reddit paid off $100,000 in 1.5 years, but had a high income and lived extremely minimally.

Your timeline depends on three variables: your total debt, your income, and your willingness to sacrifice.

Use These Free Payoff Calculators

Don’t guess at your timeline. Calculate it precisely.

The Federal Student Aid Loan Simulator lets you enter your federal loans and compare different repayment plans with exact timelines and total interest paid.

Unbury.me is a free calculator specifically designed for debt payoff. You can enter multiple loans and compare snowball versus avalanche methods with visual timelines.

These calculators let you experiment with different payment amounts to see how extra payments change your timeline. I spent hours playing with different scenarios before I committed to my strategy.

Seeing that increasing my payment from $300 to $500 would eliminate my debt four years earlier was the motivation I needed to find that extra $200 per month.

Start Your Debt-Free Journey Today

I’ve given you 13 strategies, warned you about five costly mistakes, and shown you real examples of people who went from overwhelmed by student debt to completely free.

The path isn’t mysterious. It’s just math and discipline combined.

You don’t need a six-figure salary. You need a plan that matches your situation and the commitment to execute it consistently for months or years.

Pick two or three strategies from this article that fit your life. Maybe it’s switching to biweekly payments and rounding up your payment amount. Maybe it’s the debt snowball method combined with living like a broke student. Maybe it’s side income plus applying all windfalls.

You don’t need to implement everything. You need to implement something and stick with it.

I think about Mandi, who paid off $102,000 and literally held a funeral for her student loans when she made that final payment. She can now save for a home instead of sending money to a loan servicer every month.

That’s what’s waiting for you on the other side of this. Not just a zero balance, but actual financial freedom to build the life you want.

Calculate your timeline today. Choose your strategy today. Make your first extra payment today.

The fastest way to pay off student debt is to start right now.

Frequently Asked Questions

Should I use the Debt Snowball or Debt Avalanche method to pay off my student loans?

Use Debt Snowball if you need motivation from quick wins by paying smallest balances first. Use Debt Avalanche if you’re disciplined and want to save the most money by paying highest interest rates first. Both work. Snowball provides psychological victories that help you stick with the plan. Avalanche saves more in total interest but takes longer to see your first loan eliminated. Choose based on your personality. If you’ve quit debt payoff plans before, snowball gives you early wins to maintain momentum. If you’re motivated by spreadsheets and optimization, avalanche is mathematically superior.

How do I make sure extra payments go toward my principal and not future payments?

When making extra payments, explicitly tell your loan servicer to apply the payment to principal only and do not advance your due date. Most servicers ask if you want to prepay future months, which sounds helpful but doesn’t reduce your balance. Log into your account and look for options like “apply to principal” or “principal prepayment.” If you can’t find this option online, call your servicer and state clearly that you want the extra payment applied to principal. Then verify within a week that your principal balance decreased by the full extra payment amount and your next due date didn’t change.

Should I use my savings to pay off student loans immediately?

Keep at least $1,000 for emergencies, then use remaining savings to eliminate your highest-interest loans or smallest balances depending on your chosen method. Rebuilding savings happens after you’re debt-free. The exception is if your loans are below 4% interest, in which case keeping a larger emergency fund makes sense. Never drain your savings completely because unexpected expenses will force you into high-interest credit card debt, sabotaging your progress. That $1,000 buffer protects you while you aggressively attack your student debt.

How much should I pay each month to pay off my student loans in 2 years?

Divide your total debt by 24 months to get the base amount, then add interest. For example, $30,000 ÷ 24 = $1,250 per month plus interest charges means you’d need roughly $1,350-1,400 monthly depending on your interest rate. Use a student loan payoff calculator to get your precise number by entering your exact balance and interest rate. The calculator accounts for how interest accrues and decreases over time as your principal drops.

When should I NOT pay off my student loans quickly?

Don’t pay extra if you qualify for Public Service Loan Forgiveness because extra payments reduce the amount that would be forgiven for free after 10 years. Don’t skip your employer’s 401k match to pay debt because that match is guaranteed free money. Don’t pay aggressively if you have high-interest credit card debt, pay that first. And consider income-driven repayment instead of aggressive payoff if your debt is much higher than your income and you work in a low-paying field where forgiveness makes more financial sense than repayment.

Does paying off student loans early hurt my credit score?

Paying off loans early may cause a small temporary credit score dip because you’re closing a credit account, but this impact is minor and short-term. Your score recovers quickly. The long-term benefit of being debt-free, having better debt-to-income ratio, and freeing up income far outweighs a 10-20 point temporary score decrease. Within a few months, your score typically rebounds and continues improving because you have lower overall debt.

Should I refinance my federal student loans to pay them off faster?

Only refinance federal loans if you have stable high income, don’t qualify for PSLF or need income-driven repayment, can get at least 2% lower fixed rate, and understand you’ll permanently lose federal protections like forbearance and forgiveness options. If you lose your job after refinancing, you can’t access federal relief programs. Refinancing makes sense for high-income borrowers with secure jobs who are committed to aggressive 2-4 year payoff and whose federal protections have little value. For everyone else, the risk usually outweighs the interest savings.

What’s the fastest anyone has paid off student loans?

Real examples include $30,000 paid in 12 months by living on $500 monthly expenses, $87,000 paid in 2.5 years by a couple dedicating 50% of income, and $100,000 paid in 1.5 years by earning high income and living extremely minimally. These timelines required intense sacrifice like living with parents, working multiple jobs, eliminating all discretionary spending, and maintaining laser focus. They prove rapid payoff is possible but required temporary extreme measures. More typical aggressive timelines are 2-4 years for balances between $30,000-80,000 on moderate incomes.